METC - Ramaco Resources: Yet Another Disappointing Quarter

Summary

- Ramaco Resources produces coking coal, but some of its coal is sold based on a thermal coal index.

- After a weak Q2, I was expecting the situation to improve in the third quarter.

- I'm disappointed.

- The financial results are still excellent from an "absolute" point of view as the stock is priced at just 4X earnings, but the relative performance is weak as Ramaco hasn't met expectations for a while.

- I have no position, but I have written a bunch of put options of which some are in the money, others are out of the money.

Introduction

I originally was attracted to Ramaco Resources ( METC ) by its publicly traded debt ( METCL ). And although the share price is up 57% for a total return of 61.6% including dividends compared to August 2021, when my first article was published, there is a sour aftertaste. Despite outperforming the S&P by in excess of 70% in this 15-month time frame (which I really shouldn’t be unhappy about!), Ramaco is increasingly shaping up to represent "the story that could have been."

Although the metallurgical coal price performed very well and although Ramaco’s share price almost tripled since the August 2021 article was written, the share price never reached its full potential as Ramaco has a history of not meeting the market’s expectations. Q2 was light, but there were a few elements that I thought

The Q3 results were weaker than expected

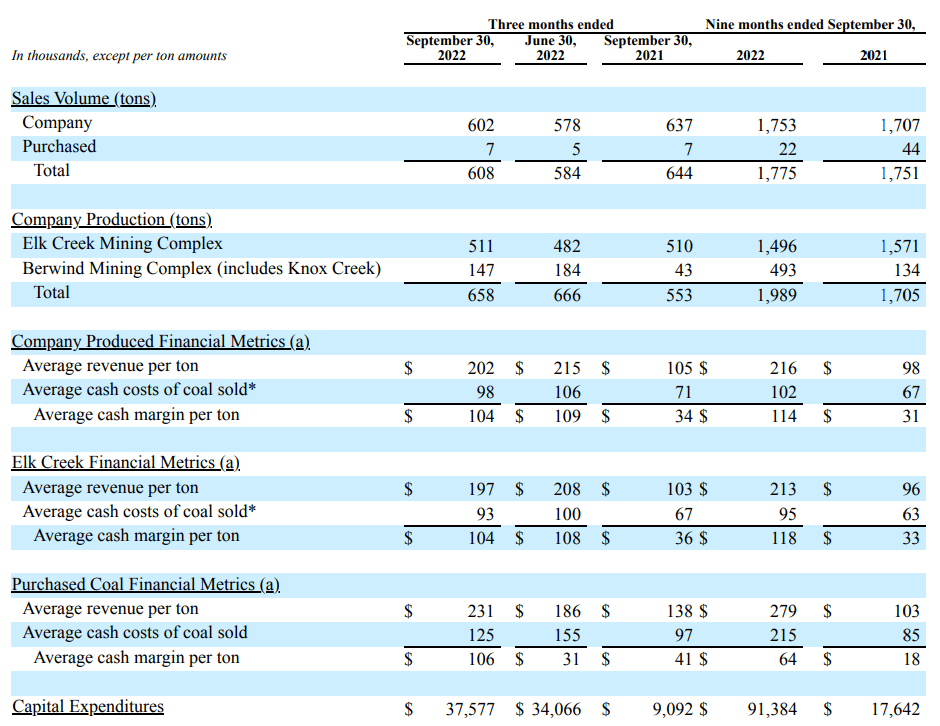

While the consensus estimates called for an EPS north of $1, Ramaco Resources royally missed those expectations. The company sold just over 600,000 tonnes of coal at an average price of $202/t. While I had expected the sales volume to be higher than the production volume (considering the company produced about 88,000 tonnes more than it sold in Q2), the final results actually shows a lower sales volume (602,000 tonnes) versus the production volume (658,000 tonnes). This means that the accumulated "excess" production in the first nine months of the year exceeds 200,000 tonnes. While it's great to build up inventory levels to be able to meet customer demands, I would have preferred the company to have sold the additional 135,000 tonnes in Q2 and Q3 as that would have resulted in an additional cash flow of north of $25M.

{kind=link}

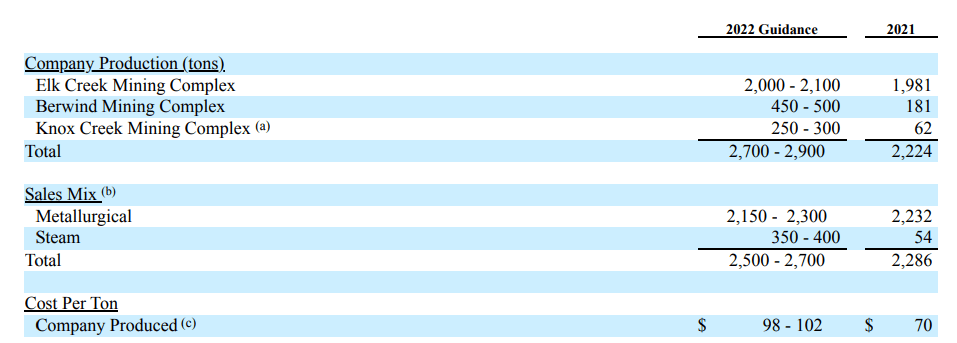

And it doesn’t look like the difference between tonnes of coal produced and tonnes of coal sold will change anytime soon as the official guidance now calls for a total production of 2.8 million tonnes (the mid-point) while only 2.6 million tonnes will be sold.

{kind=link}

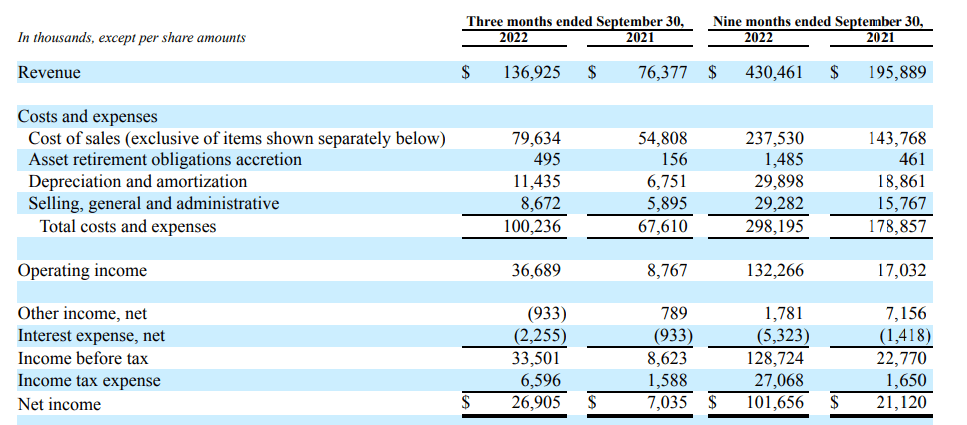

The total reported volume in the third quarter came in at just under $137M resulting in an operating income of just under $37M. After deducting the interest expenses and the taxes, the net income was $26.9M, which represents about $0.61 per share.

{kind=link}

That’s really not bad in absolute terms, but the expectations for Ramaco were quite a bit higher than that. And although the YTD earnings of just under $102M in net income and an EPS of $2.30 aren’t too bad, it didn’t meet the expectations.

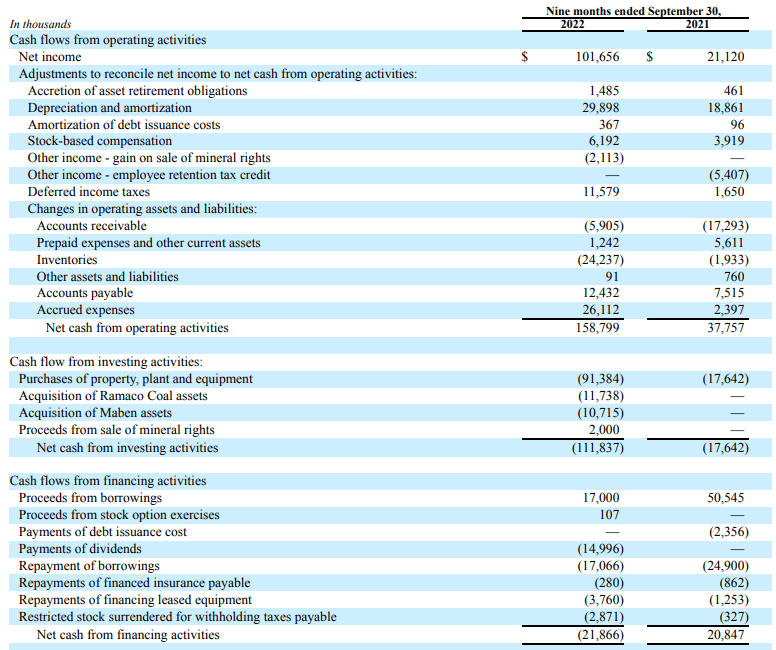

I was hoping the company’s cash flow result would have been better, but that isn’t really the case. Sure, we can be very happy with an operating cash flow of almost $159M and even after adjusting this result for changes in the working capital position and the lease payments, the adjusted operating cash flow of just over $145M is very respectable.

{kind=link}

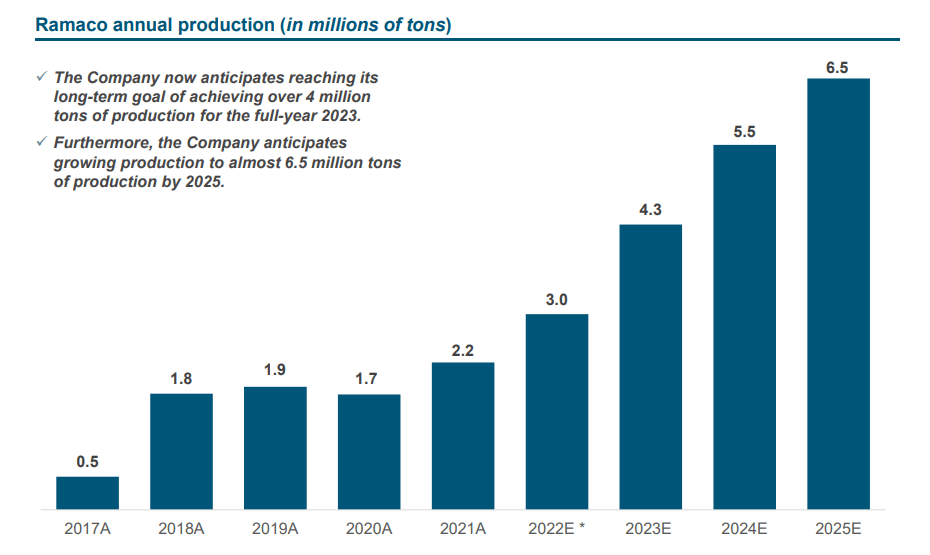

The total capex was $91M, but this obviously includes investments in growth initiatives as Ramaco is planning to increase its output to 6.5 million tonnes in 2025 . Note: the 2022 production result of 3 million tonnes will likely not be reached as the official guidance now calls for a full-year output of 2.7-2.9 million tonnes of coal.

{kind=link}

Fortunately, the balance sheet remains okay’ish although the majority of the debt that has been added to the liabilities is related to a few recent acquisitions. As of the end of September, Ramaco had about $47M in cash but also about $66M in short-term debt. That’s not an issue as the company remains cash flow positive and it also does not "have" to repay its ((METCL)) 9% bond in 2024 as that is just the call date. That’s the main reason why that note remains listed as a long-term liability. And although Ramaco has a negative working capital position and its current cash position is not sufficient to repay the $66M of debt within the year, I’m not particularly worried. Despite the earnings miss, Ramaco’s cash flows remain strong and I would be very surprised if the related party debt could not be extended.

Investment thesis

I like metallurgical coal. I like Ramaco’s balance sheet and growth plans. But the financial results have been underwhelming for quite a while now. The problem now is that these results are bad in relative terms (vs. the expectations) but aren’t bad in absolute terms: Even if the EPS only comes in at $3 this year, the current share price of $12/share means Ramaco is still cheap.

Even if the company continues to miss its earnings expectations, Ramaco should still be poised for a re-rating, especially as the production rate in 2023 will increase again. But I also understand the skepticism of the financial markets as it has been a while since Ramaco actually met the expectations.

That being said, I will likely continue to write P7.5s and P10s on Ramaco as I still think the company offers good value down here. But constantly missing expectations won’t help to change the market’s perception.

For further details see:

Ramaco Resources: Yet Another Disappointing Quarter