RANJF - Randstad: Looking Cheap But Issues Potentially Ahead

2023-07-13 03:56:18 ET

Summary

- Randstad has grown revenue at a CAGR of 6%, with its strong business model implying this will continue.

- Randstad has a strong brand, diversified revenue, and deep expertise across several HR-related services.

- The industry experienced a spike in demand, implying a slowdown is ahead. Compounding this is an economic slowdown and consumer confidence declining, suggesting revenue will decline in FY23.

- Relative to its direct peers, the business looks undervalued, as it performs well.

- The issue is that we see no near-term positives to drive price action.

Investment thesis

Our current investment thesis is:

- Randstad is a well-positioned business, owing to a high market share, a well-regarded brand, and substantial scale.

- Relative to its directly comparable peers, the business looks attractive, with better growth and margins.

- The recruitment industry looks to be slowing, following an unexpected post-pandemic spike, a weakening of economic conditions, and reduced consumer confidence (less likely to move jobs).

- The business looks cheap but we think it will be dead money in the near term.

Company description

Randstad N.V. (RANJF) is a global leader in the HR services industry, providing a wide range of solutions in the areas of temporary staffing, permanent placement, and human resource consulting. With a presence in over 38 countries, Randstad connects employers and job seekers, supporting businesses in their talent acquisition and workforce management needs.

Share price

Randstad's share price has underperformed the market in the last decade, as despite a continuation of its positive trajectory, the company's returns have been mild.

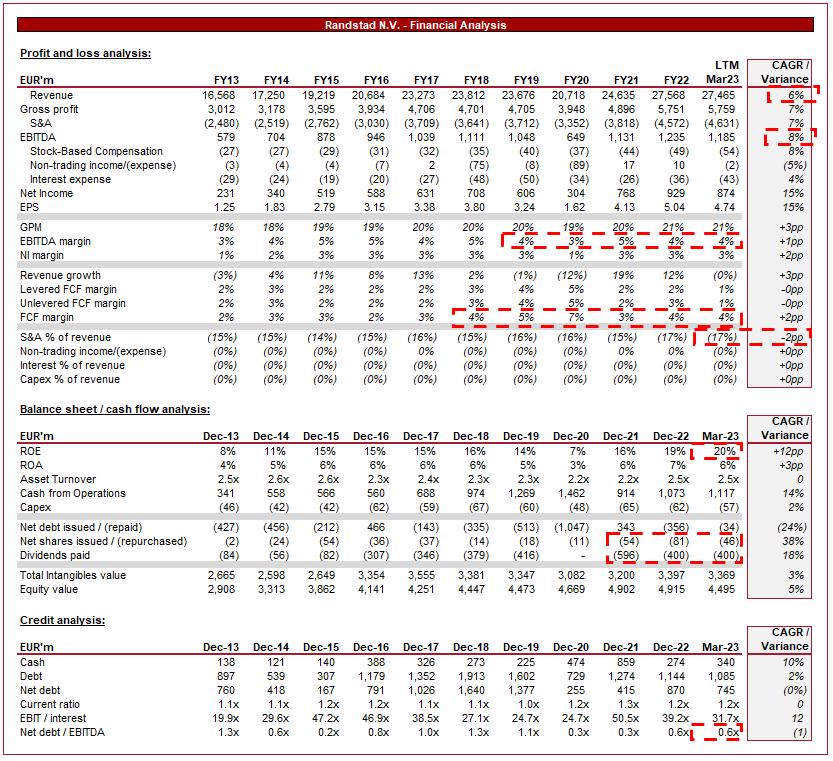

Financial analysis

Randstad financials (Capital IQ)

{kind=link}

Presented above is Randstad's financial performance for the last decade.

Revenue & Commercial Factors

Randstad's revenue has grown at a healthy CAGR of 6% in the last 10 years, with the occasional dip in revenue during this period. The company has successfully bounced back from the pandemic impact, experiencing an improvement in growth.

Business Model

Randstad provides services across the resourcing spectrum, describing itself as the "world's largest HR services provider". The company assists clients in finding permanent employees through targeted recruitment and selection processes. Further, It offers flexible staffing solutions, matching qualified temporary employees with businesses in need of temporary workforce support. Finally, Randstad provides a range of HR consulting services, including talent management, training, and workforce planning.

Randstad's revenue is generated from 4 segments:

- Staffing - Focus on recruiting candidates for manufacturing, logistics, and administrative jobs.

- Inhouse - An on-site solution for managing a client's workforce, aiming to improve clients' labor flexibility, retention, productivity, and efficiency.

- Professionals - Focus on recruiting experienced professionals and managers with academic or equivalent qualifications from a wide range of industry backgrounds.

- Global business - A range of HR services, such as managed services programs.

Revenue (Randstad)

Randstad's revenue profile is relatively diversified, with its largest segment comprising 46% of its total revenue. This said, the company is highly exposed to the demand for labor across its segments, regardless of if its direct recruitment or support services.

For this reason, it is critical that the company is geographically diverse, reducing any systemic concerns and cyclicality. This looks to be the case, with its largest region only comprising 20% of revenue.

{kind=link}

Regardless of this, we have seen some lumpiness in revenue growth, implying the diversification gains can only extend so far.

The provision of services across the HR industry is a highly lucrative business model in our view. This is because the recruitment industry is highly fragmented, with many firms specializing in industries or geographical locations. The development of a brand is difficult due to the financial investment required to achieve scale, as well as the nature of this industry, as employees only care about roles, not the recruiter. Randstad's significant scale through global expansion and the provision of related services has allowed it to develop a brand. A developed brand allows the business to win outsized mandates, as employers see a large, well-polished business that can provide them with a range of support services.

Recruitment Industry

The HR services industry is divided into three key segments: staffing, professionals, and executive search. Randstad primarily operates in the staffing and professionals segments. This strategy is the correct one as although executive search is lucrative, it is niche and lacks the ability to achieve sufficient scale.

The global staffing market is estimated to be worth €323bn, while the global professionals market is valued at around €224bn. This industry is materially linked to economic development and population growth, as the creation of new jobs proportionately grows open roles.

HR industry (Randstad)

Companies differentiate themselves through its customer reach, industry-specific expertise, and brand development. Randstad faces competition from global and regional HR services providers such as Adecco ( OTCPK:AHEXF ), ManpowerGroup ( MAN ), and Kelly Services ( KELYA ).

Randstad's impressive growth in the last 2 years is a reflection of the changing dynamics post-pandemic in the West. With a large number of redundancies and "pandemic checks", the labor market has been materially disrupted, with high wage inflation and record levels of people leaving their jobs (" the great resignation "). Randstad's significant scale allowed the business to exploit this, especially with the filling of temporary positions, which generally yield improved returns.

This said, the company has also felt the offsetting impact, struggling with talent acquisition and retention, as well as providing the roles employees are willing to take.

Our expectation is for this labor disruption to subside, as illustrated by the LTM revenue slowdown, as those who sought to move, have, and are now consumers turn their focus to developing within their roles.

Although the recruitment industry is linked to the economic development of nations, it does not necessarily mean Randstad is expected to grow at this rate. An attractive quality of the industry is the need to focus on building long-term relationships with clients, allowing for consistent new mandate wins, and reducing volatility on the growth curve. As the largest industry participant, Randstad is positioned well to win contracts from the largest businesses in its key markets, representing scope for consistent outperformance.

Across the last decade, a skills gap has developed in the West, with the number of STEM-qualified candidates unable to satisfy demand. This is in part due to technological and economic development, with a greater spread of individuals across roles, including a significant increase in creative roles. This should support further reduced volatility in the forward revenue curve, as demand remains strong due to the inability to wholly fill roles.

Economic & External Consideration

Current economic conditions are best described as weak and uncertain, although we have yet to enter an official downturn. With heightened inflation and elevated rates, consumers are facing significant financial issues.

This is concerning for Randstad, as businesses feel this weakness via reduced demand, contributing to a lower need for heads. Conversely, consumers are more likely to search for and find new roles with higher pay, as unemployment remains low. Take the UK, for example. High inflation and a tight labor market contributed to wage inflation of 8.7% in May23 , over a year after inflationary pressures first began.

In the most recent quarter, Randstad experienced a decline in revenue of (2)%, (4)% on an organic basis. This is a relatively weak performance given we are still seeing health in the labor market, implying individuals are moving roles less as they become defensive. More concerning is that its largest segment declined by (8)% (staffing), implying a core weakness. This suggests a clear slowdown will occur in the current year, and potentially extend into FY24.

Margins

Randstad's margins have remained flat over the historical period, reflecting what is a highly competitive market despite the fragmentation. It is an industry where employers can easily obtain several quotes and compare prices, contributing to competitive price bands.

In the most recent quarter, margins slightly improved, driven by a change in sales mix. Randstad will have limited scope for material improvement due to personnel being its largest cost and thus impacted by offsetting compensation improvements as it grows.

Balance sheet & Cash Flows

Randstad is conservatively financed with low capex commitments, allowing the business to allocate capital to M&A and shareholder distributions. In the last decade, over €1bn has been spent on M&A and over €3bn on distributions.

Industry analysis

Human Resource and Employment Services (Seeking Alpha)

Presented above is a comparison of Randstad's growth and profitability to the average of the Human Resource and Employment Services industry, as defined by Seeking Alpha (21 companies).

Randstad underperforms the group, which we must be fair in stating includes several growth businesses. Its growth is significantly below the average, reflecting its market-leading position. Relative to Adecco and ManpowerGroup, Randstad outperforms.

Profitability is equally underwhelming, although the business is quite efficient compared to the average. Again, Randstad outperforms both Adecco and ManpowerGroup.

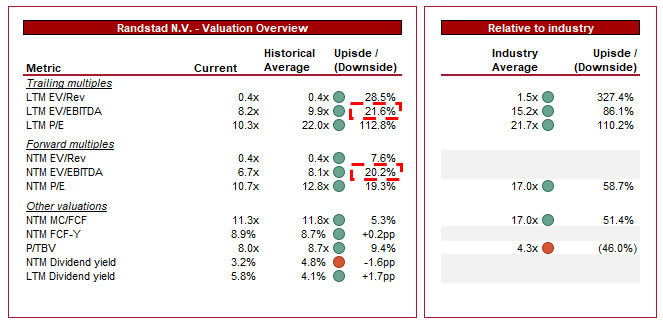

Valuation

{kind=link}

Randstad is currently trading at 8x LTM EBITDA and 7x NTM EBITDA. This is a discount to its historical average.

Our view is that in an upswing, Randstad would be attractively valued at its current share price, as its performance is in line with its historical average, implying upside of c.20%. Relative to peers, the business is at a substantial discount, well beyond justifiable given the performance delta.

When compared directly to Adecco and ManpowerGroup, Randstad is trading at a small premium to the average of the two, implying some upside.

Our key concern and cause for hesitancy is its recent performance, with its revenue decline implying an industry downturn may be ahead. Further, this restricts the potential for a positive catalyst, as it's becoming increasingly unlikely the business will achieve growth in FY23. For this reason, the stock looks to be a value trap in the coming year, until market conditions improve.

Final thoughts

Randstad has a wide moat, developed through its substantial scale and broadly-reaching business model. We expect the business to continue its strong growth trajectory over time, although the near-term looks highly concerning. Relative to its directly comparable peers, Randstad is performing well, but we are not overly convinced by its attractiveness. The business looks cheap on paper but the scope for positive price action v. negative looks weighted toward negative due to the weakening performance. We suggest patience with this stock.

For further details see:

Randstad: Looking Cheap But Issues Potentially Ahead