RNGR - Ranger Energy Services To Consolidate Before Any Acceleration (Rating Downgrade)

2023-07-12 02:08:28 ET

Summary

- Ranger Energy Services is expected to make strategic adjustments in 2023, relocating assets and crews to the Permian from Haynesville due to weak natural gas prices.

- Despite a strong balance sheet and positive Q1 cash flows, the company faces challenges due to pricing softness and lack of topline growth opportunities.

- RNGR stock is currently undervalued compared to its peers, but due to limited growth prospects, I recommend investors "hold" the stock.

Ranger Energy: The Wait May Stretch

My last article on Ranger Energy Services ( RNGR ) discussed the company's strengths and weaknesses. In 2023, it will make strategic adjustments related to its geographic asset positioning. Led by the natural gas price's weakness over the past year, it relocated some assets and crews to the Permian from Haynesville, where it is more confident about the growth prospect. In Q2 and Q3, its wireline operations can outperform what typically happened in the past.

On the other hand, the pricing softness continued as some of its competitors offered pricing readjustment and rig count exhibits weakness. The pricing environment has already been fragile following COVID-19'S low activity level. In Q1, its cash flows turned positive, which allowed deleveraging an already strong balance sheet. The company is well on its way to increasing shareholder returns through dividends and share buybacks. The stock appears undervalued compared to its peers. Nonetheless, due to the lack of topline growth opportunities, I expect returns to stay rangebound in the near-to-medium term. I would advise investors to "hold" the stock.

A Market Analysis

{kind=link}

EIA

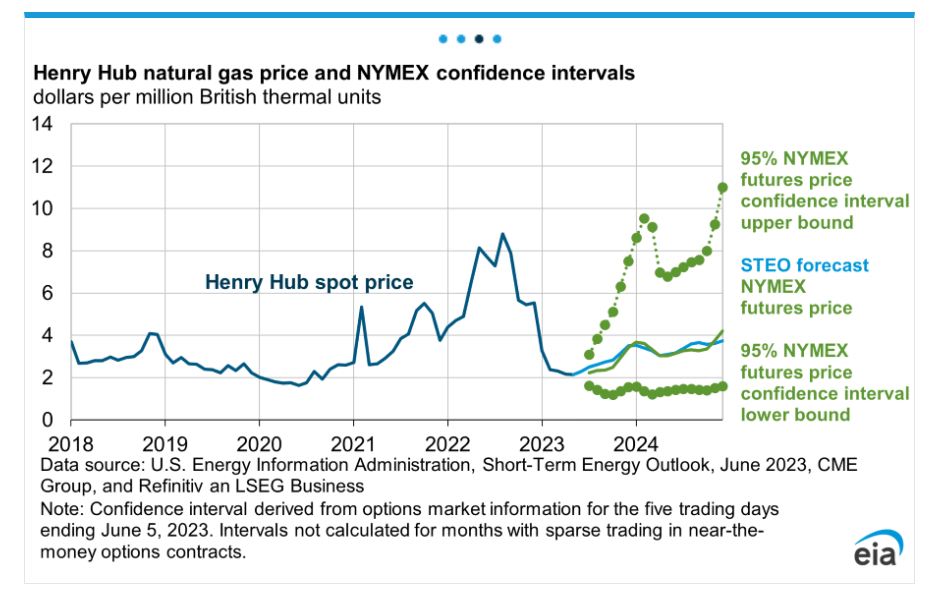

Natural gas price has posed a challenge to Ranger Energy over the past year. It declined steeply following lower European demand and concerns over global economic activity. In 2H 2023, the price seems to be heading for a recovery. The EIA forecasts the average to rise by 38% in 2H 2023, compared to the May average.

In 2024, the trend is expected to continue as the natural gas price can move north, up by 30%, compared to 2023. This can affect the LNG export capacity. The US rig count also weakened in 2013, declining by 13% year-to-date. The oil and gas prices ride a multi-year upcycle, so demand for its services may remain high in the medium term.

Pivoting The Outlook

{kind=link}

Ranger Investor Presentation June 2023

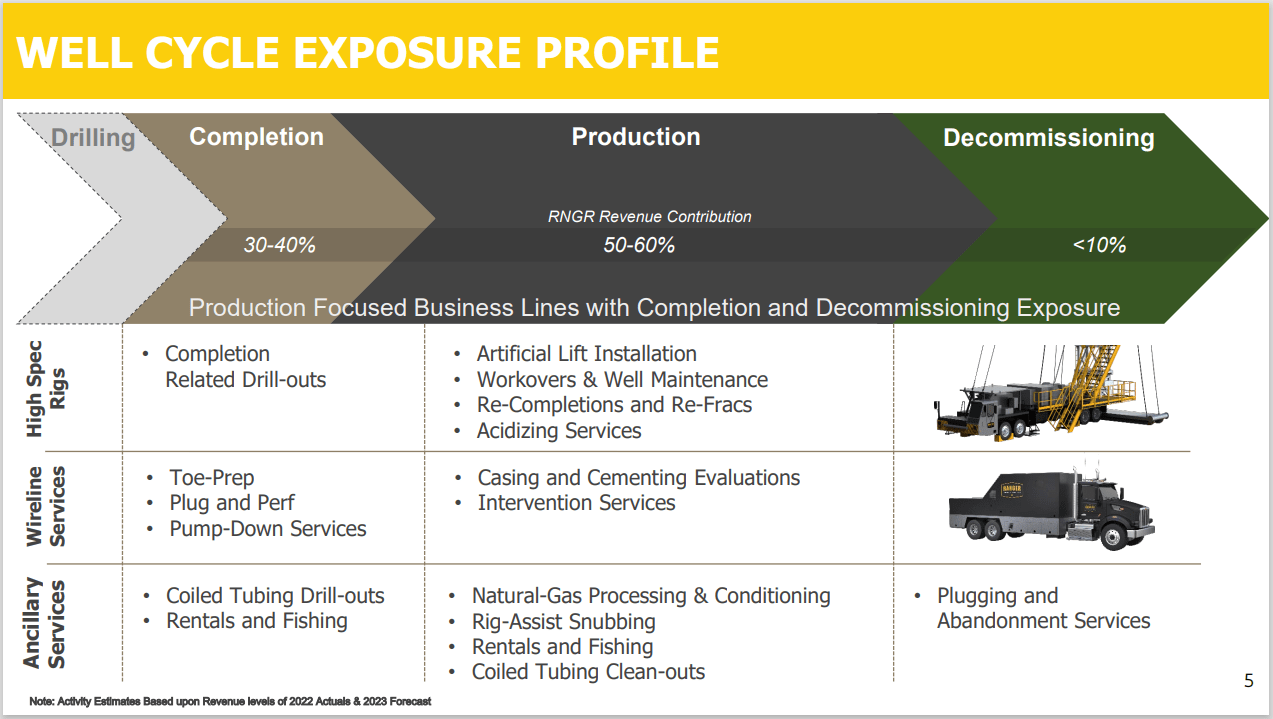

Some of the company's segments may see muted growth. Apparently, the company relocated some assets and crews to the Permian from Haynesville as dictated by the change in energy price dynamics (i.e., crude oil's relative resilience compared to natural gas prices). It helped keep utilization steady in Q1. The management appears to be confident about the growth prospect in 2H 2023. The company's Northern wireline operation has recently provided a robust growth opportunity. The wireline operations can exceed expectations in summer (i.e., Q2 and Q3).

{kind=link}

Ranger Investor Presentation June 2023

However, not everything went according to its script. Its wireline operations saw muted performance in the Permian, despite the region's limited exposure to natural gas. This was because supply exceeded demand when many operators shifted their assets here. On top of that, the market saw pricing softness when some of the company's competitors offered pricing readjustment. The pricing level is already low following COVID-19'S low activity level.

Analyzing Q1 2023 Results

{kind=link}

RNGR's Filings

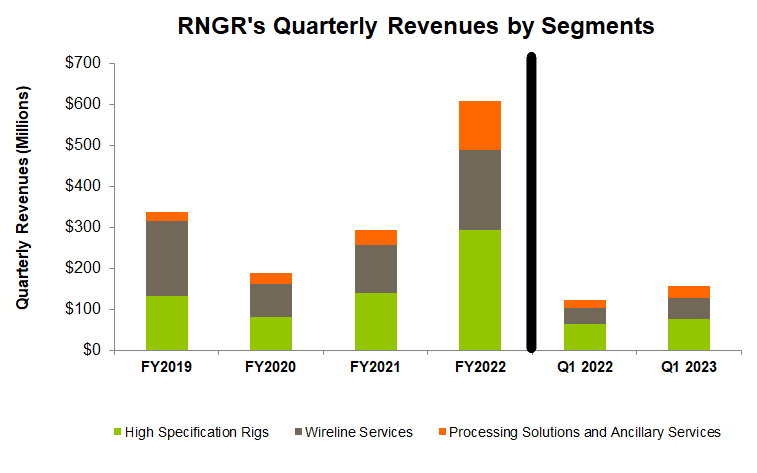

In Q1 2023, revenues in the High Specification Rigs segment increased by 19% compared to a year ago. Vigorous activity and significant pricing gains resulted in revenue addition. Adjusted EBITDA in this segment increased by 23% during this period. It integrated its businesses, reduced the number of operating facilities, and increased collaboration, which helped expand margin.

The Wireline Services segment saw 29% year-over-year revenue growth, while its adjusted EBITDA turned positive in Q1 2023. Increased activity levels in the production business and higher pricing in completions, productions, and pump-down business led to the topline and EBITDA improvement.

Revenues in the Processing Solutions and Ancillary Services segment witnessed nearly 50% growth year-over-year in Q1 2023. The adjusted EBITDA, too, increased by a similar margin. Synergies from integration led to a 400-basis point reduction in the cost of services, which benefited the EBITDA in this segment.

Cash Flows And Leverage

RNGR's debt-to-equity was 0.06x as of March 31, 2023. Its adjusted net debt reduced significantly over the past year (from $80 million to $10 million). Its liquidity was $68.4 million as of March 31, 2023. It has already committed to returning 25% of its annual cash flows through share repurchases and dividends. So, in Q4 2022, it began repurchasing shares. It will also evaluate its capital deployment options, including acquisitions while prioritizing shareholder returns. So, the financial risks are low.

In Q1 2023 2022, the company's cash flow from operations (or CFO) turned positive compared to a negative CFO a year ago due to the rise in revenues. So, its free cash flow (or FCF) also turned positive in Q1 2023, allowing for debt repayment and shareholder returns.

Target Price And Relative Valuation

{kind=link}

Seeking Alpha

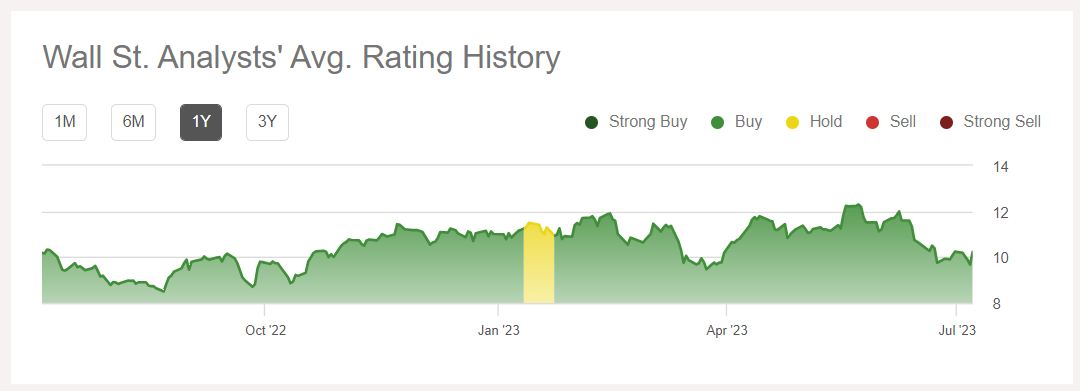

One sell-side analyst rated RNGR a "buy" ("strong buy"), while three recommended a "Hold." None recommended a "Sell." The stock's return potential using the sell-side analysts' expected returns is 42% at the current price.

{kind=link}

Author created and Seeking Alpha

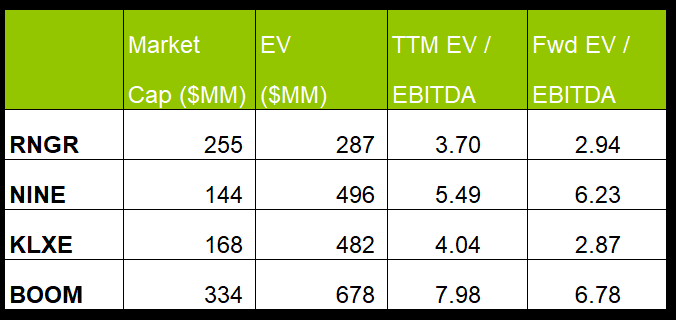

RNGR's forward EV/EBITDA multiple is expected to contract versus the current EV/EBITDA. Also, the fall will be steeper than its peers, indicating a sharper rise in EBITDA versus its peers. This typically results in a higher EV/EBITDA multiple than the peers. The company's EV/EBITDA multiple (3.6x) is lower than its peers' (NINE, KLXE, and BOOM) average. So, the stock is undervalued versus its peers.

Why Do I Downgrade The Stock?

In Q4 2022, RNGR benefited from various acquisitions, which helped expand the existing wireline business into production-related services. Its management also expected demand and pricing resilience because of market tightness in early 2023. It was also reaping the benefits of a strengthening balance sheet, including debt repayment and deleveraging. I wrote :

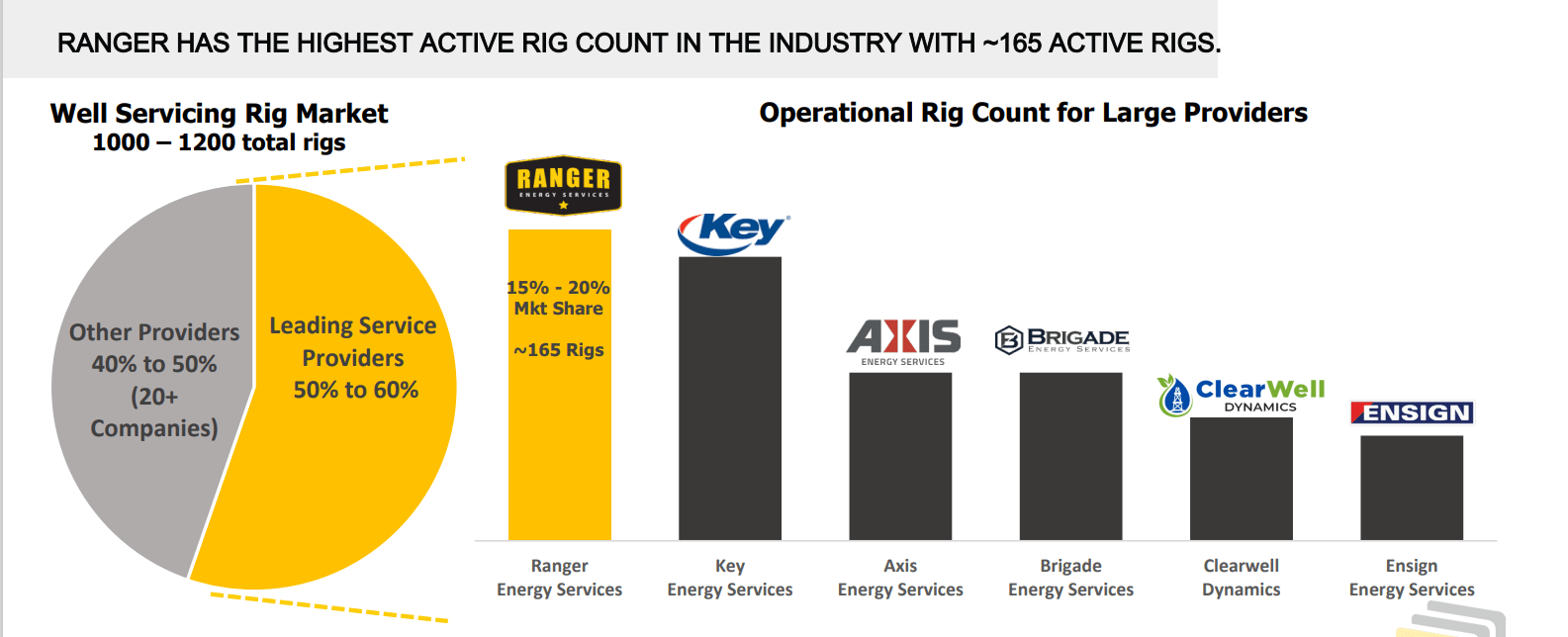

Over the past few years, RNGR added capacity through asset and business acquisitions without making significant capital outlays. It also strengthened its wireline services through the PerfX and XConnect acquisitions. It has the highest active high-spec rig count in the US in the wells servicing space.

In Q1 2023, some of the drivers followed through. The company changed its regional asset portfolio mix as the energy price balance shifted following the natural gas prices decline. Its wireline operations saw muted performance in the Permian. The market saw pricing softness when some of the company's competitors revised down pricing. Although the balance sheet continued to strengthen, I do not see sufficient drivers to suggest a "buy". So, I would downgrade the stock to a "hold."

What's The Take On RNGR?

{kind=link}

Seeking Alpha

In 2023 and 2024, the EIA forecasts the average natural gas price to rise from the current level. This can affect the LNG export capacity. Oil and gas prices ride a multi-year upcycle, so demand for its services may remain high in the medium term. RNGR changed its regional asset portfolio mix as the energy price balance shifted following the natural gas prices decline. Crude oil's relative resilience helped keep utilization steady in Q1. The management appears to be confident about the growth prospect in 2H 2023.

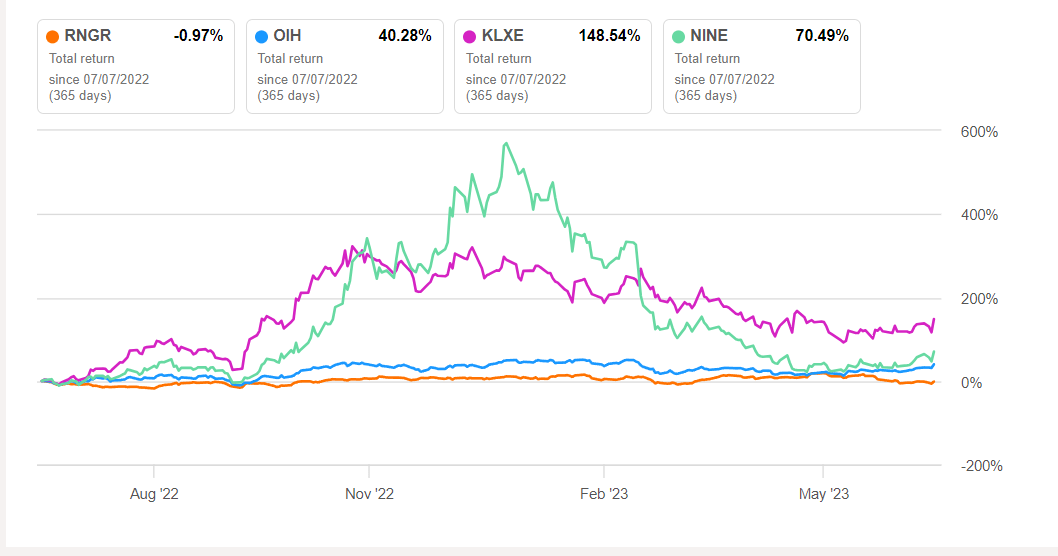

However, some of the company's segments may see muted growth. Supply may start exceeding demand in the Permian here when many operators shift their asset bases. So, the stock underperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year. It has committed to returning 25% of its annual cash flows through share repurchases and dividends. With a robust balance sheet, it should not be difficult for the company to improve shareholder returns. However, I do not see ample growth opportunities for the company to recommend a "buy," and I think a "hold" call would be appropriate at this point.

For further details see:

Ranger Energy Services To Consolidate Before Any Acceleration (Rating Downgrade)