ROCC - Ranger Oil: Report Card Time

Summary

- Juniper is clearly playing to win the long game.

- Buying cheap acreage and then showing above average profitability takes time.

- The Denbury offer followed by fiscal year 2020 caused a price-earnings ratio collapse that has yet to be recovered.

- The money that Juniper invested (on top of the acreage acquired) clearly has been put to good use.

- Juniper is likely to be growing the company for some years to come.

Mr. Market cares a whole lot about results. Sometimes those results take time to appear so Mr. Market can get testy and temporarily "leave a stock for dead" until those results appear. Ranger Oil ( ROCC ) used to be Penn Virginia when it emerged from bankruptcy. The first order of business appeared to be to try to sell the company. But an offer from Denbury (DEN) collapsed. Then came Juniper. So now it's time to see how Juniper has been doing.

The Denbury Offer

Back in 2018, management received an offe r to combine with Denbury. My own estimation at the time was that this offer would leave the combined company far too leveraged for what was a really challenging time in the industry. Little did I know that Covid was yet to come. The offer was terminated in 2019. But the damage to the post-bankruptcy stock price was substantial.

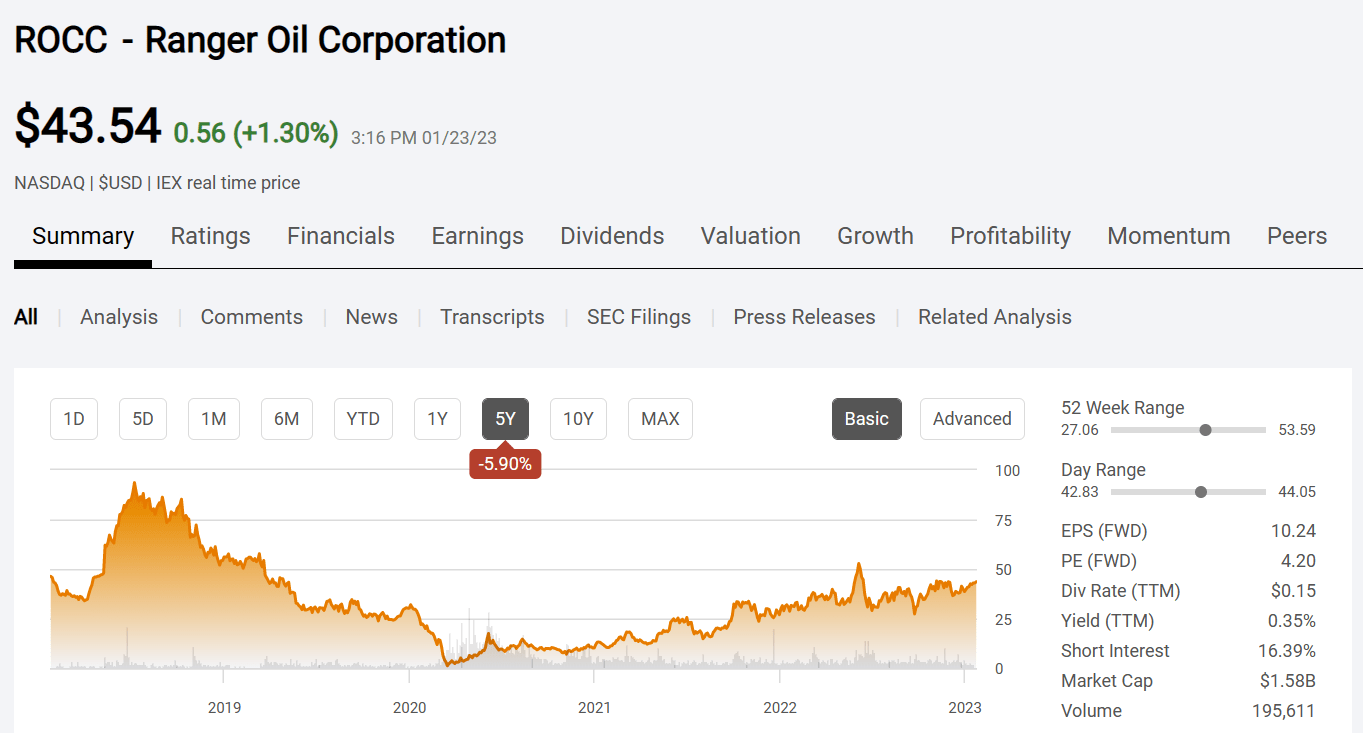

Ranger OIl Corporation Common Stock Price HIstory And Key Valuation Meaures (Seeking Alpha Website January 23, 2023)

{kind=link}

The stock price, which was in the roughly $50 range at the time of the offer obviously collapsed both from the failed takeover as well as the Covid challenges in fiscal year 2020. The drop in price happened not only from lower oil prices but also from a very pessimistic industry outlook that took hold to reduce price-earnings ratios at the same time. Industry wide, those lower price-earnings ratios really have yet to fully recover.

Juniper Capital

Juniper Capital came along at the bottom of the market with a proposal. The main purpose here is to see how things are going compared to when Juniper arrived. The complementary acreage did not appear to be a problem for many commenters to my articles at the time. Instead, it was the $150 million in cash at $8.75 a share that caused an uproar.

What is clear now is that Juniper did get in at a good time. But the guidance since then has been good enough for a stock outperformance in the industry.

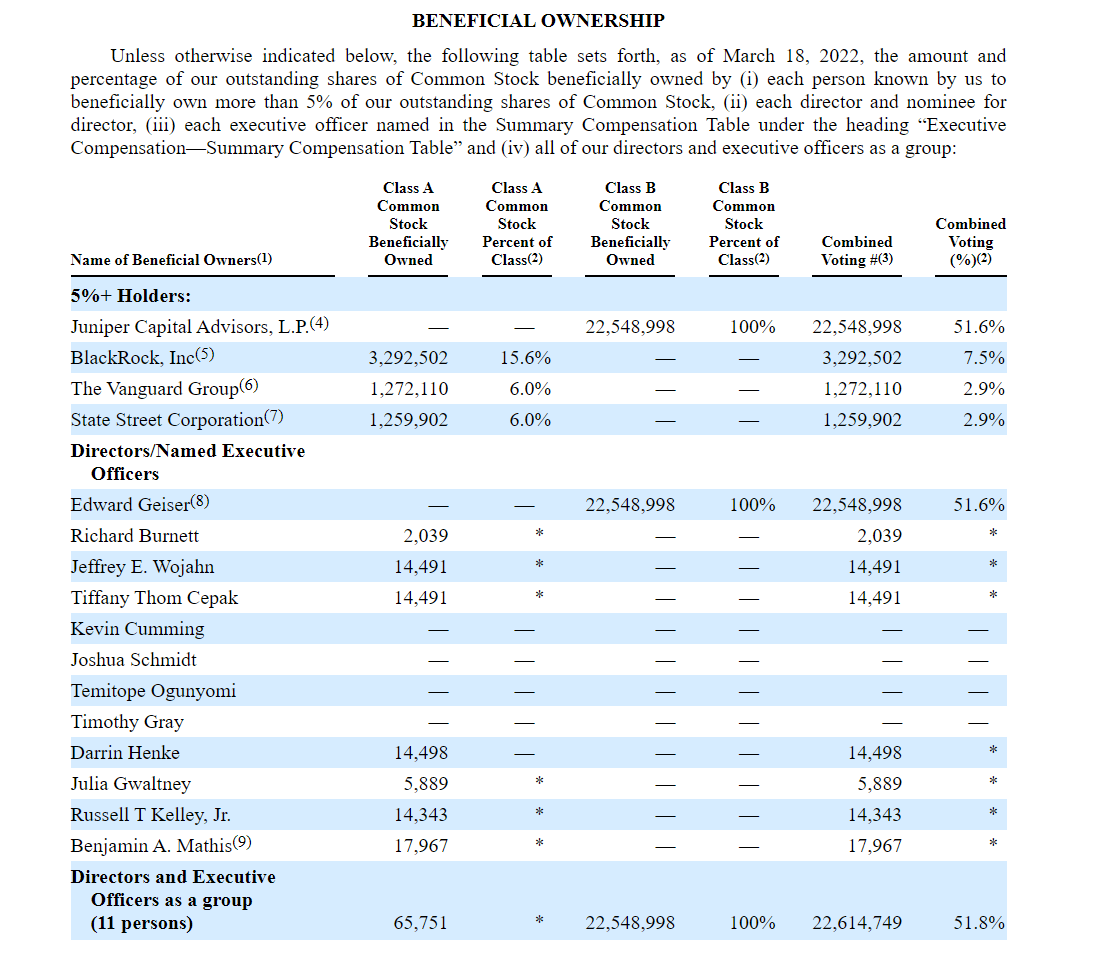

Ranger Oil 2021 Proxy Statement Major Shareholders (Ranger Oil 2021 Proxy Statement)

{kind=link}

Juniper is still clearly in charge as of the last proxy statement. So, shareholders can likely conclude that there is still more work to be done. A company like Juniper will either sell its position at a profit at the appropriate time or will (more likely) sell the entire company at a good price during a favorable part of the industry cycle.

People often ask me when the proper time is to sell. The proper time to sell is when insiders like Juniper decide it's time to go. Many times, those professionals know when a downcycle is on the way. Their timing is not perfect as a rule. But it is usually better than what an individual investor earns (generally).

Uses For That Money

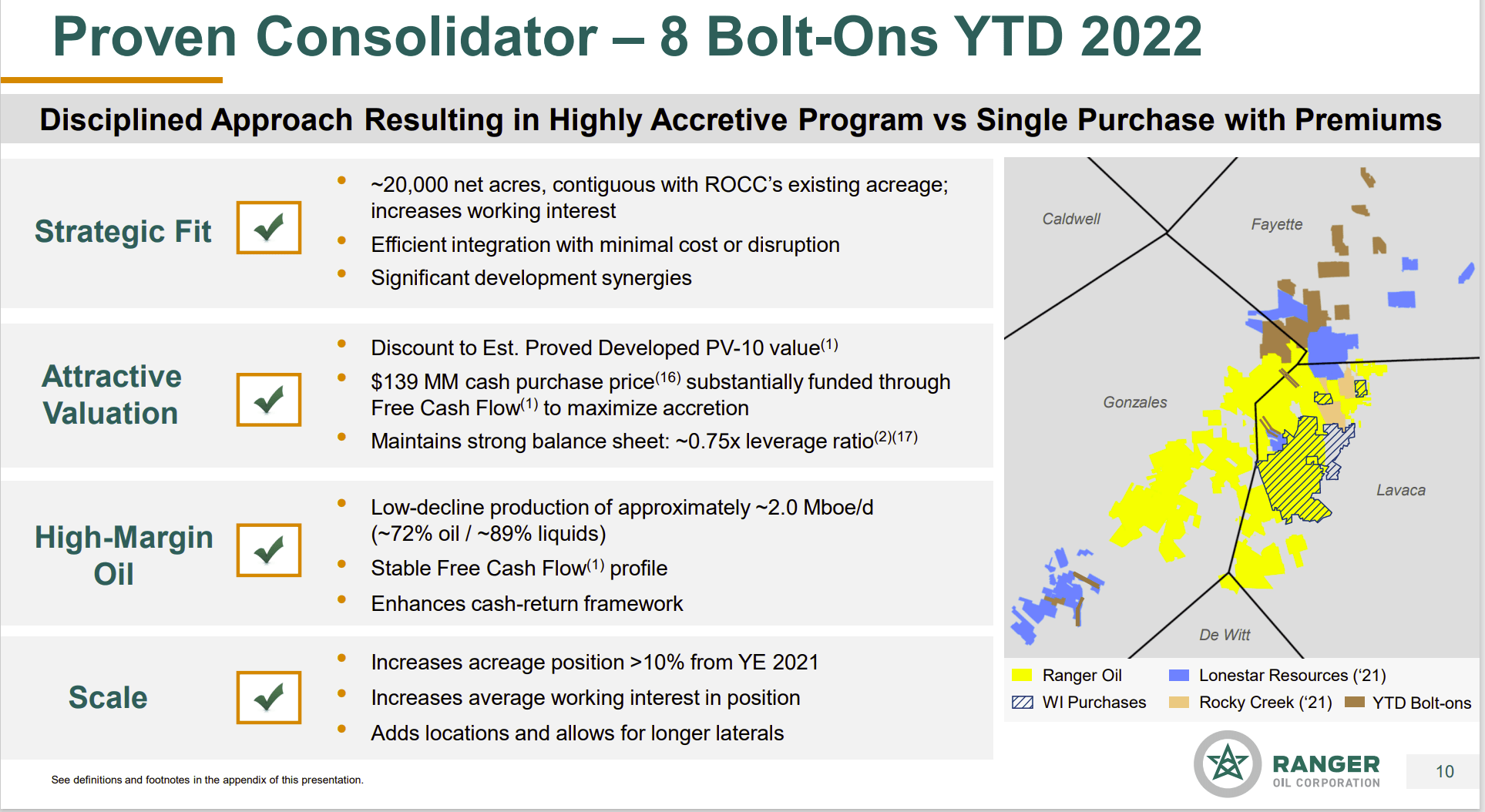

Juniper has the company consolidating small positions in the Eagle Ford to make larger contiguous (and far more marketable) acreage.

Ranger Oil Map Of Bolt-On Acquisitions (Ranger Oil Corporate Presentation At Capital One Energy Conference December 6, 2022)

{kind=link}

That cash and the resulting strong financial position allowed the acquisition of heavily leveraged Lonestar Resources. One of the things about distressed sellers is that they often want cash, and they want out "yesterday". But a company cannot take advantage of the situation unless that cash is already available. Many of the above transactions may not have happened had that cash infusion not been done initially.

There is the argument that the stock price is nothing close to the highs of the prior cycle as shown on Seeking Alpha (back in 2018) right after the company emerged from bankruptcy.

But for many cyclical companies, the comparison needs to be made using similar parts of the business cycle. 2018 was clearly a business cycle top. We still have a ways to go to "get there" with this cycle.

In the meantime, the company has been acquiring acreage for a small fraction of the cost of the more marketable plots. It has also been acquiring acreage that fits well with the acreage it already has. So, when the market top arrives, this is likely to be a far more valuable company than it was last time.

Similarly, the chart above also shows the purchase of probably illiquid small working interests that are worth more to the company than they were to the small owners.

Results

These are the kinds of things that shareholders often pay managements to do (but managements do not do it). It is painstaking work that takes time to show results. But the long-term result of this kind of strategy is often far more than Mr. Market immediately cares about.

Many ask exactly when this will be reflected in the price. Part of the answer is the robust recovery of the stock price so far. Admittedly, many were hoping for an immediate return to the 2018 numbers. But that rarely happens when value declines like it had.

The other part of the answer will be the drilling results on that cheap acreage. Competitors often pay at least $50K for contiguous acreage that is large enough for those longer extended wells in sufficient quantities. This management is buying small holdings for as little as $7K.

For a management that pays $50K for wells on 100 acre spacing (as an example), the additional location cost to the breakeven calculation is $5 million dollars. Oil wells are rarely so profitable that they can handle that extra cost to still report a reasonable profit. Oftentimes, land is not depreciated so shareholders see something like this as either too much leverage from debt or a lower return on equity (depending upon the financing of the acreage acquisition).

This company on the other hand, with a cost at $7K per acre, only has to worry about $700,000 to be added to the breakeven of the usual well calculation for 100 acre, spacing. That is an amount that many wells in this area can easily handle.

So, the event that alerts the market to the value here is likely to be a rising ROC from the cheap acreage acquired. It takes time to acquire enough acreage to move the needle. Then it takes more time to drill enough wells on that cheap acreage to increase ROC. But clearly management is playing the long game and they are playing to win. It would appear that this is a very profitable long-term proposition.

For those willing to put up with the cyclical nature of the industry and the volatile commodity prices that make an even bumpier ride, this company is probably worth a look at current prices. The time to sell is when Juniper sells.

For further details see:

Ranger Oil: Report Card Time