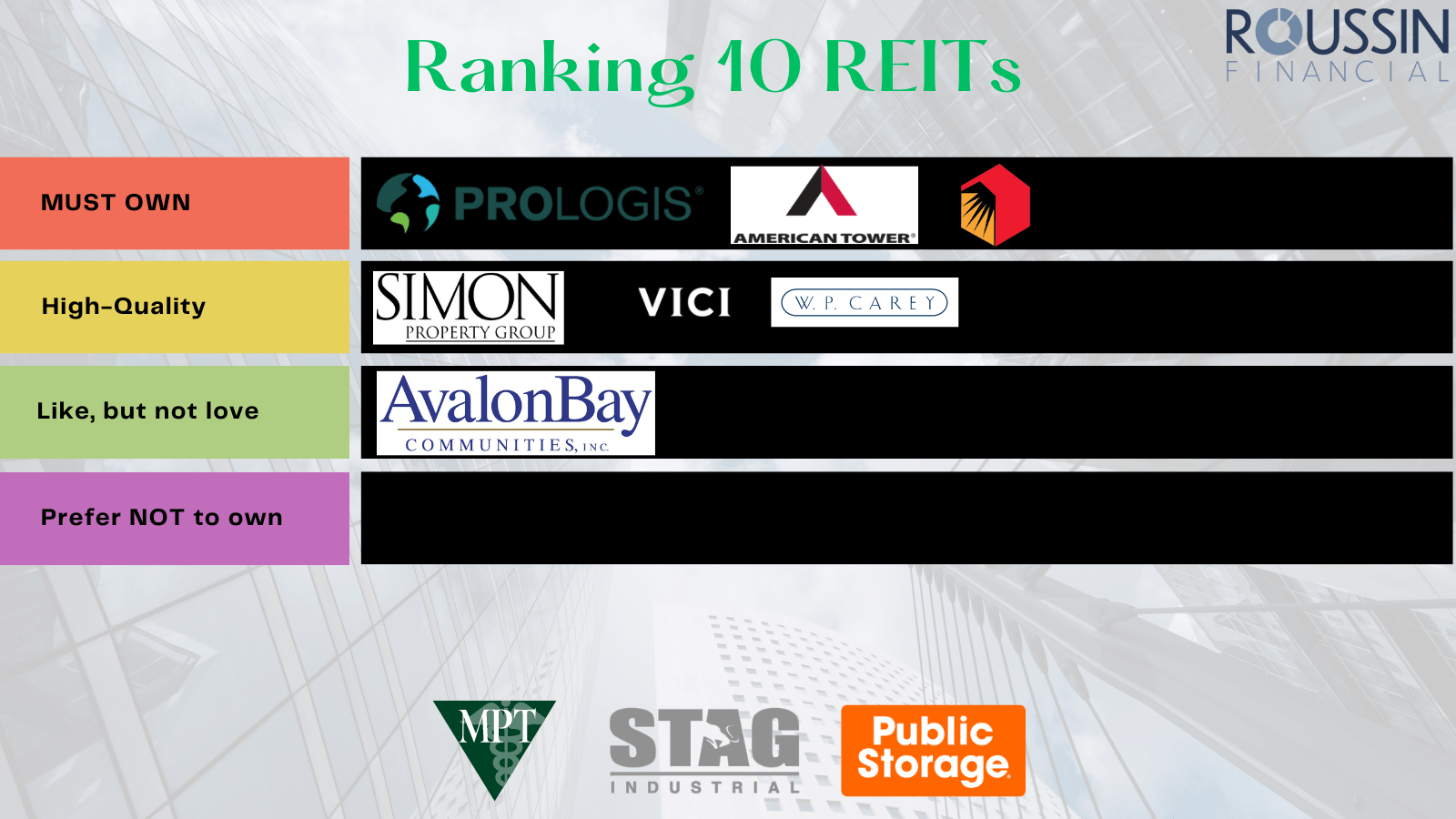

VICI - Ranking 10 REITs From Highest Quality To Lowest Quality

2023-06-16 09:38:00 ET

Summary

- Ranking 10 REITs solely based on quality and long-term viability.

- Many of these REITs are leaders within their particular sector, but not all are intriguing in terms of valuations.

- Only 1 REIT on the list is rated as a "PREFER NOT TO OWN" stock.

As we have seen over the past 12+ months, we have endured a fast raising rate environment that has seen the Federal Reserve increase the fed funds rate 14 consecutive times.

This has put intense pressure on many REITs given their reliance on debt to continue to grow. REITs are required to pay out at least 90% of their taxable income to investors in the form of dividends.

As a long-term investor, I tend to take a contrarian approach and instead of chasing hot sectors, I look for value in the beaten down sectors, one of which is the real estate sector.

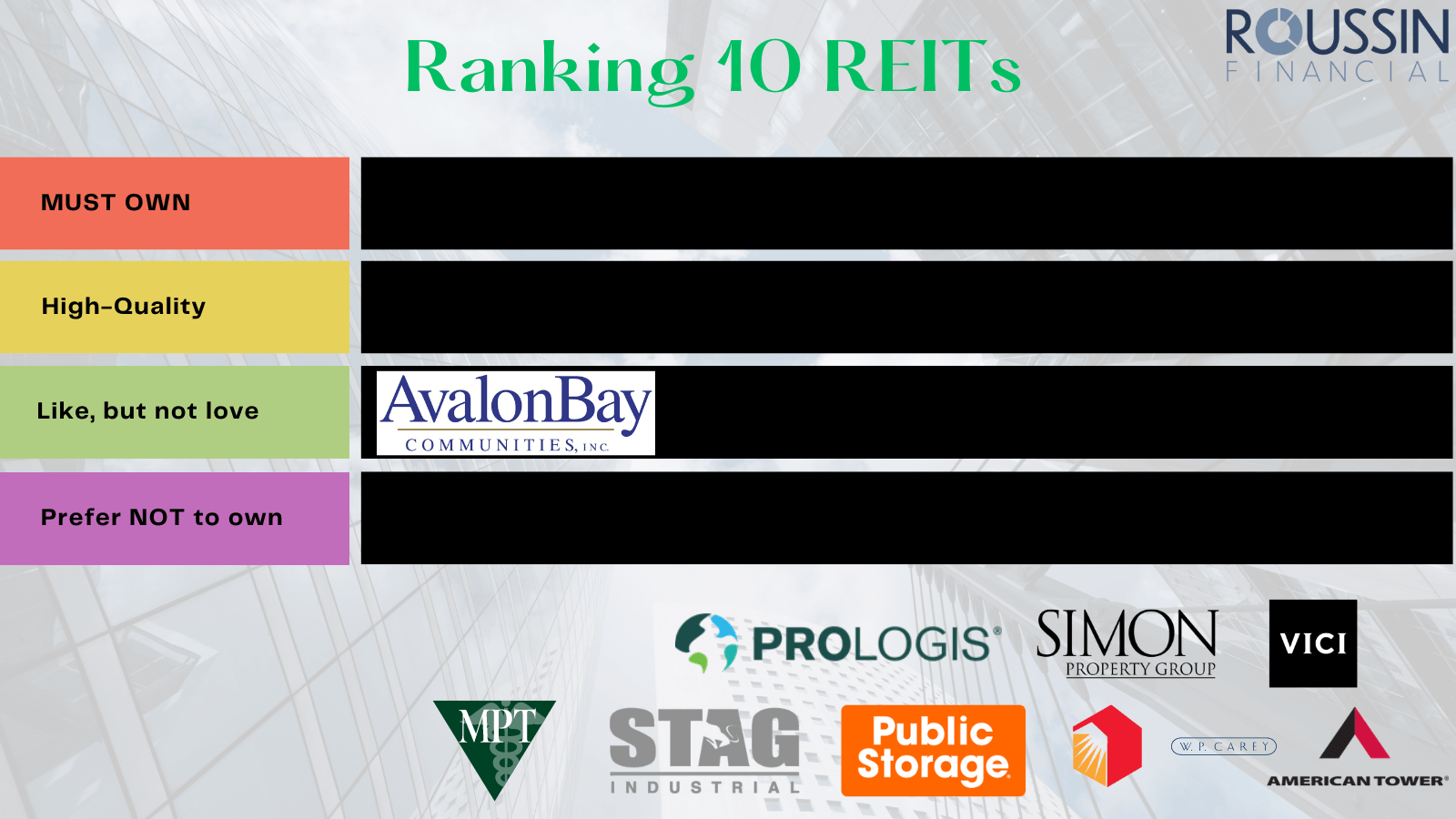

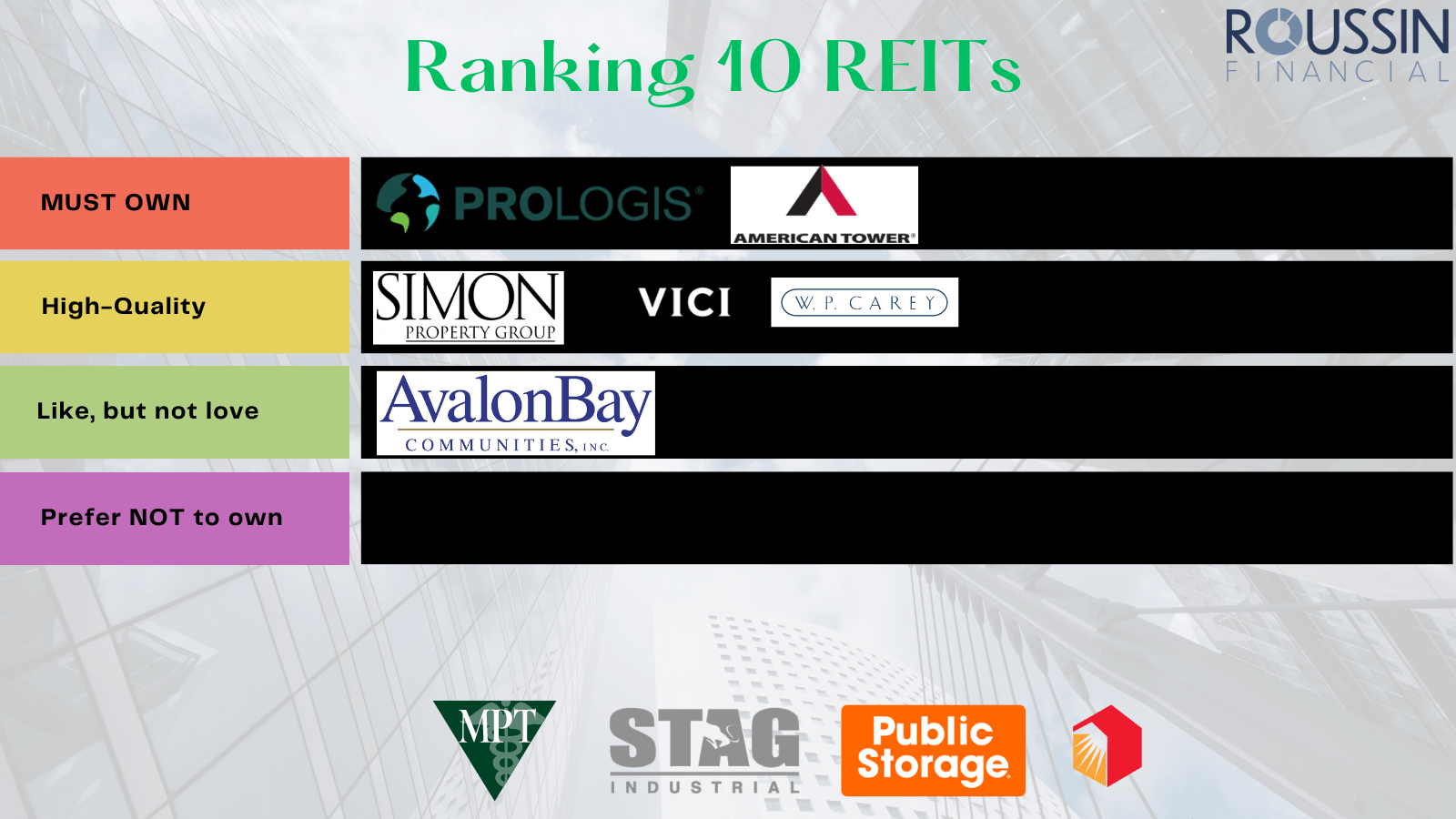

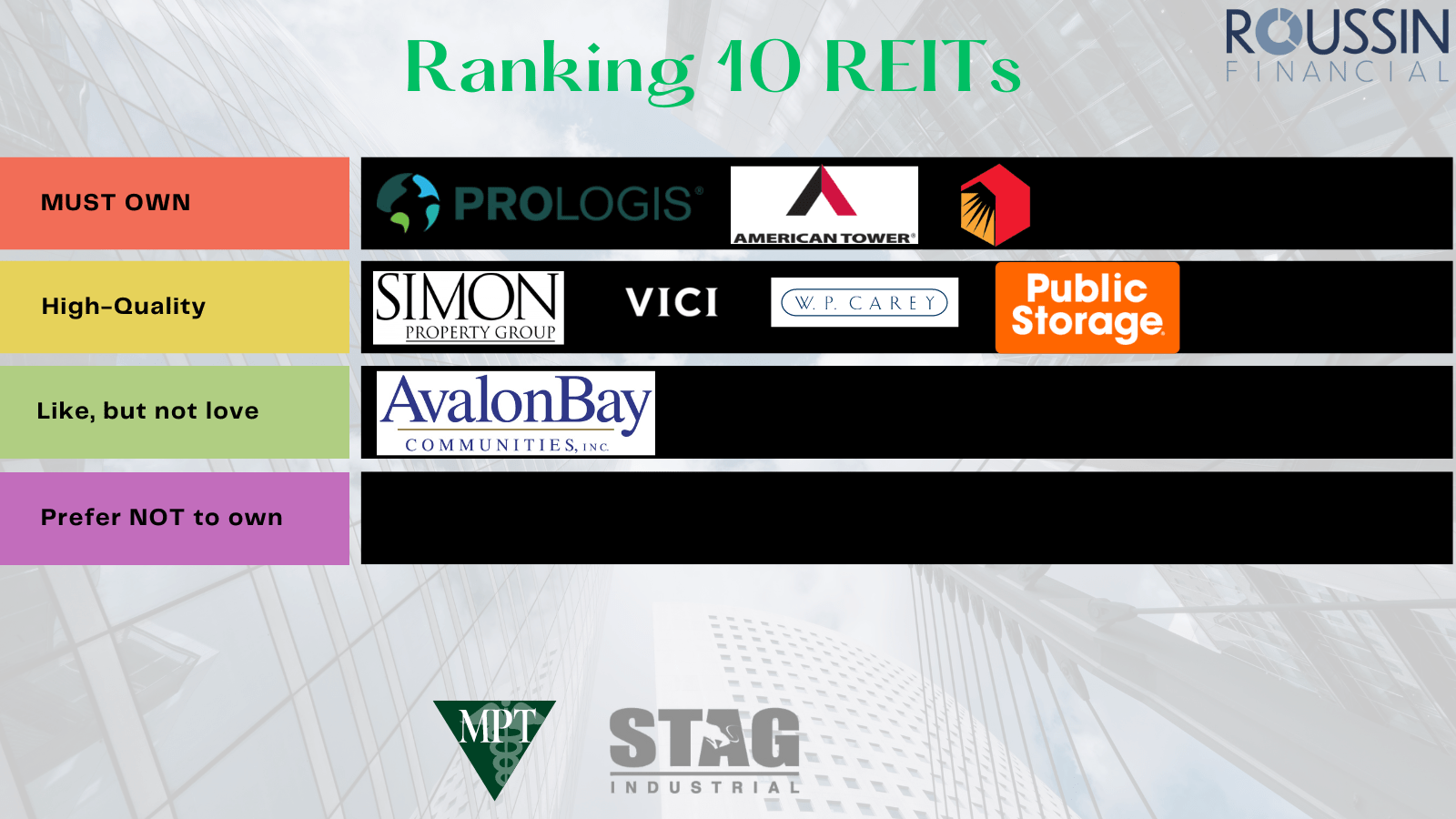

Today, we are going to look at 10 popular REITs and I will briefly touch on each of them and also rate them on the following scale:

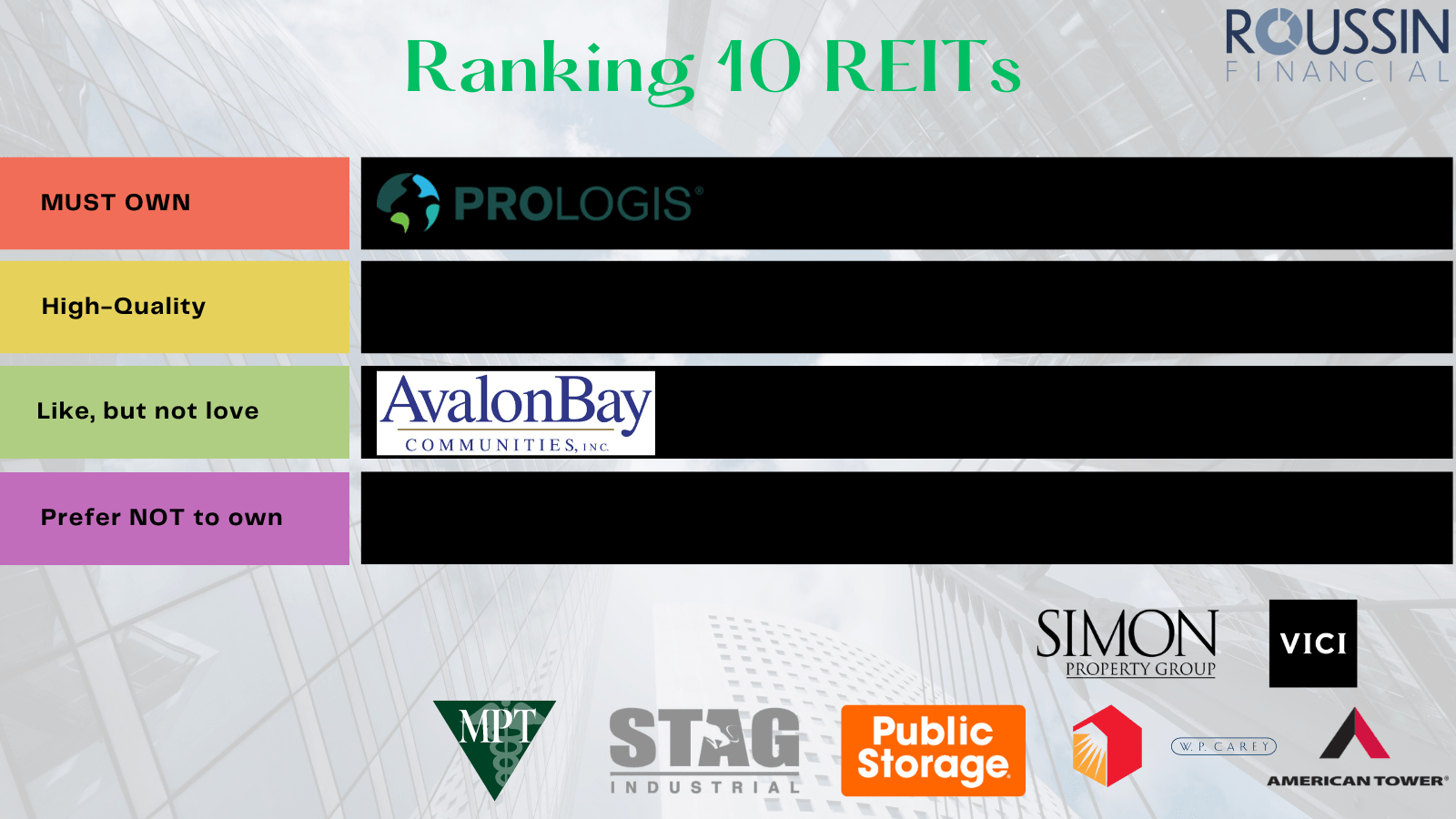

- MUST OWN - Pretty self explanatory, stocks of the highest quality that belong in MOST dividend portfolios

- High Quality - This is another great tier to be in, just a nudge below the BEST tier above it, so many great stocks or REITs here

- Like but not love - These are solid stocks, but not ones that are HIGH on my list, but still some quality names

- Prefer NOT to own - This is not a tier you want to be in, and not stocks I want to own

{kind=link}

As we go through these REITs, these ratings are obviously my opinion and my opinion only.

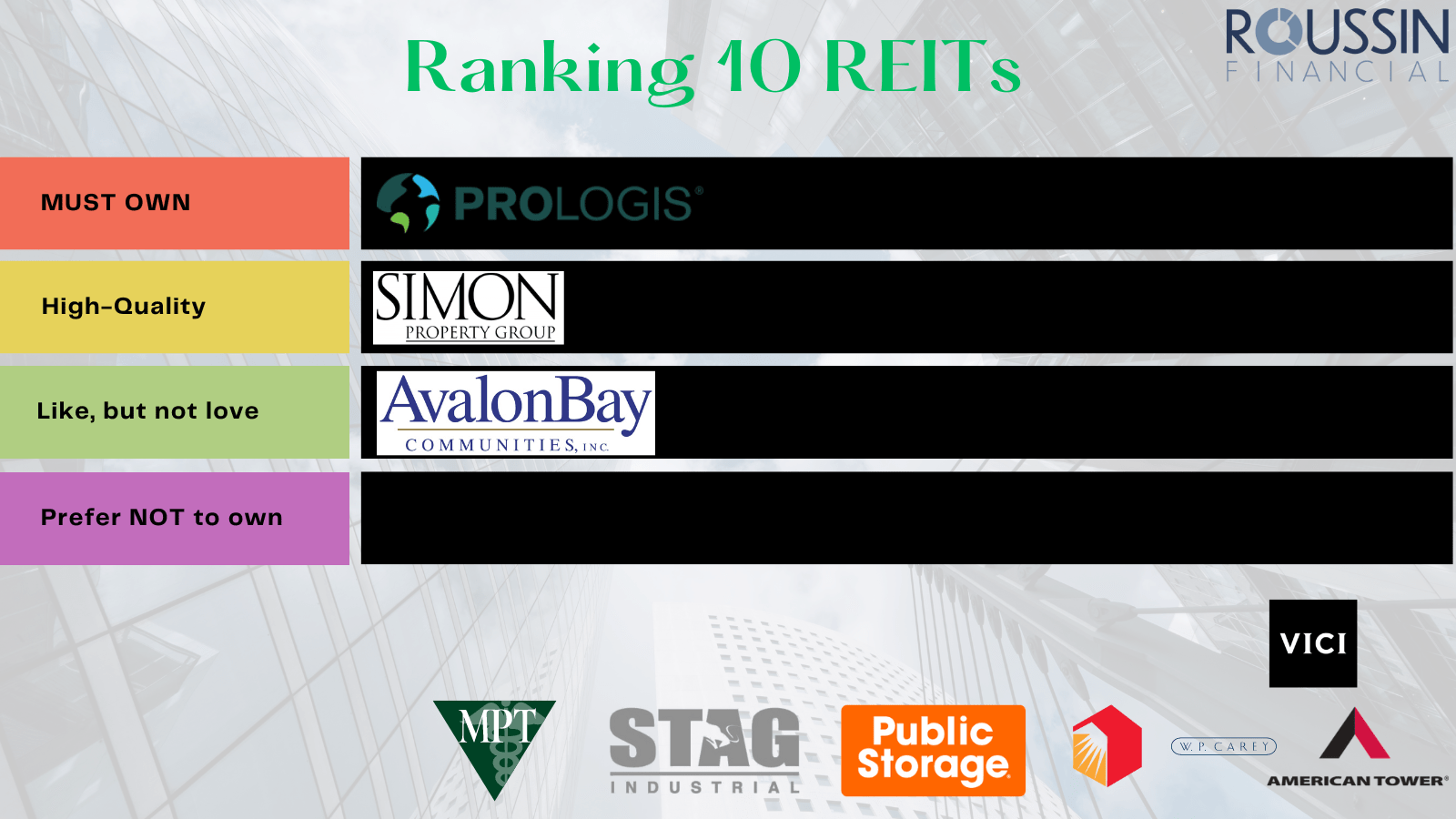

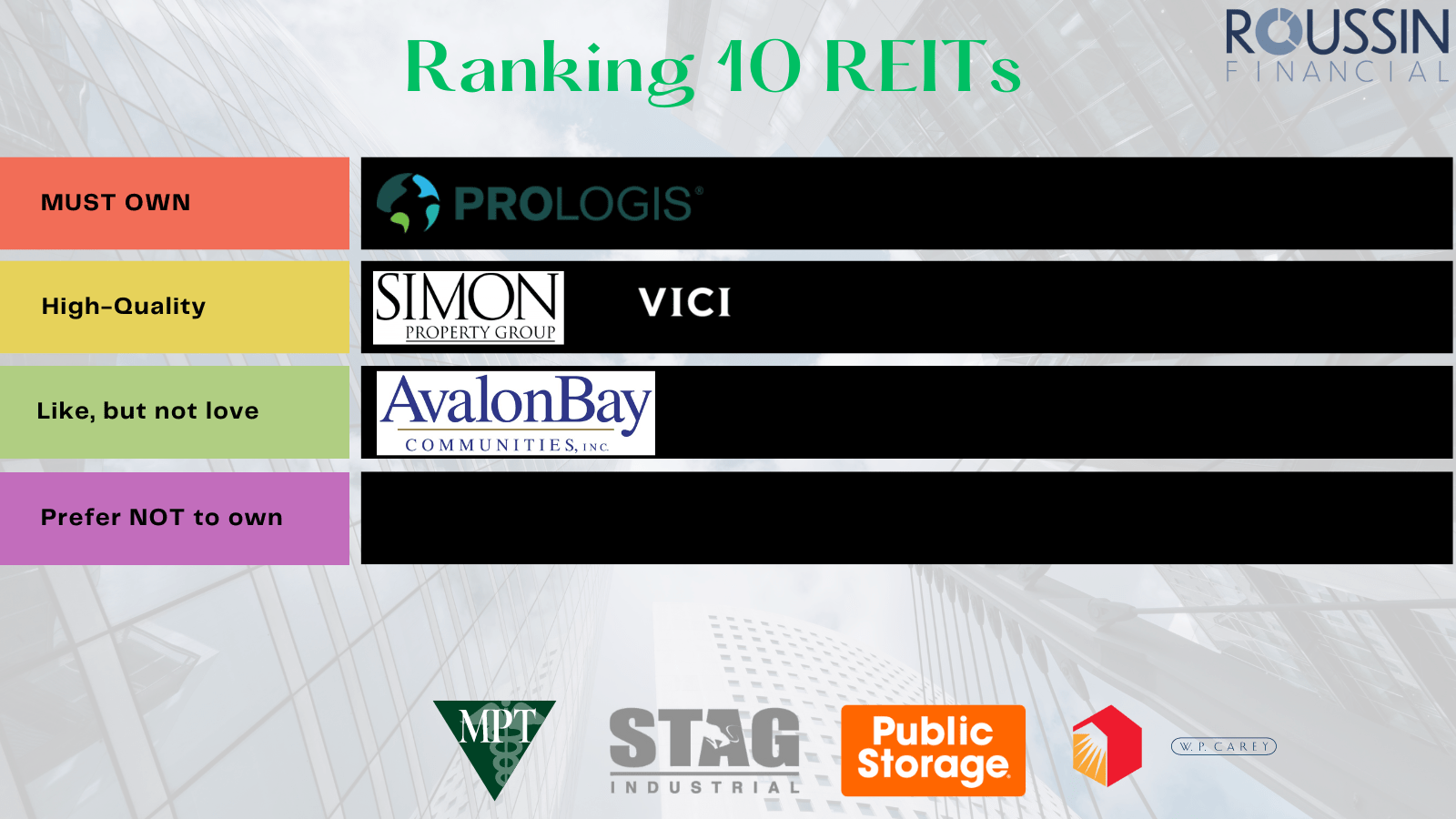

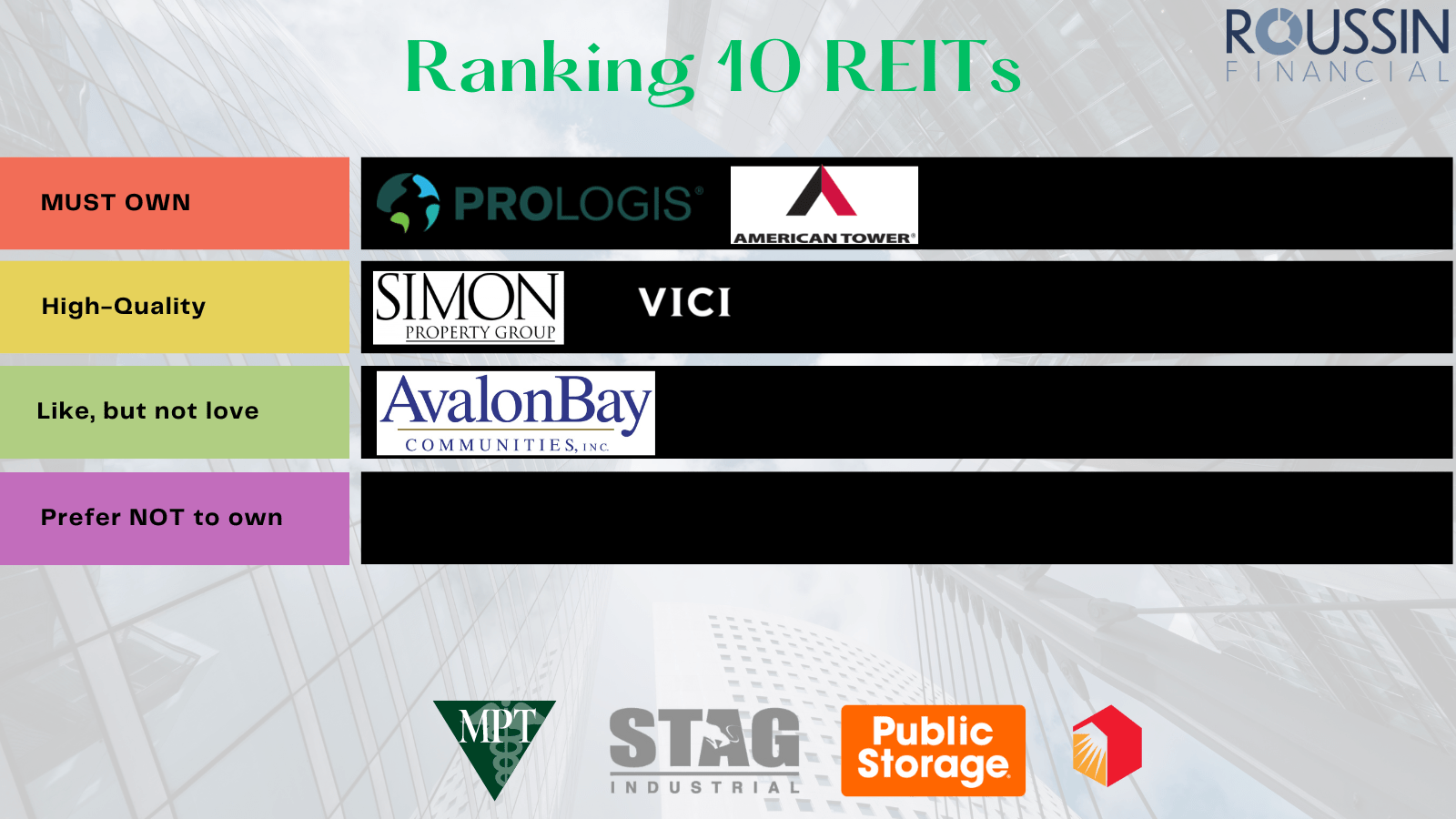

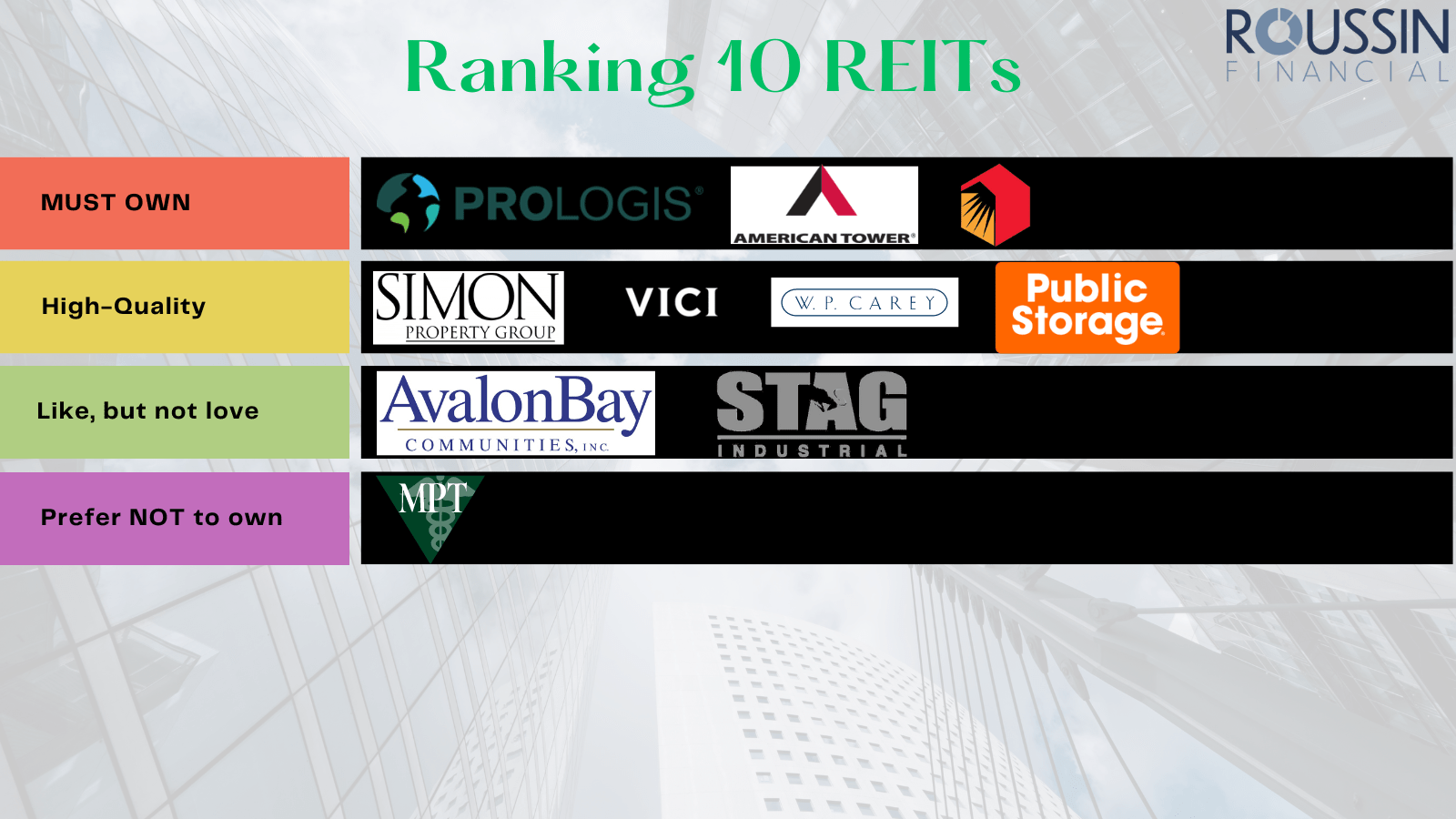

Now, here is a look at the 10 REITs we will be ranking today

- AvalonBay Communities ( AVB )

- Prologis ( PLD )

- Simon Property Group ( SPG )

- VICI Properties ( VICI )

- American Tower ( AMT )

- W. P. Carey ( WPC )

- Realty Income ( O )

- Public Storage ( PSA )

- STAG Industrial ( STAG )

- Medical Properties Trust ( MPW )

We will go through these in no particular order, and rate them as we go through them. The ratings are more focused on long-term quality and not necessarily a call to BUY at current valuations.

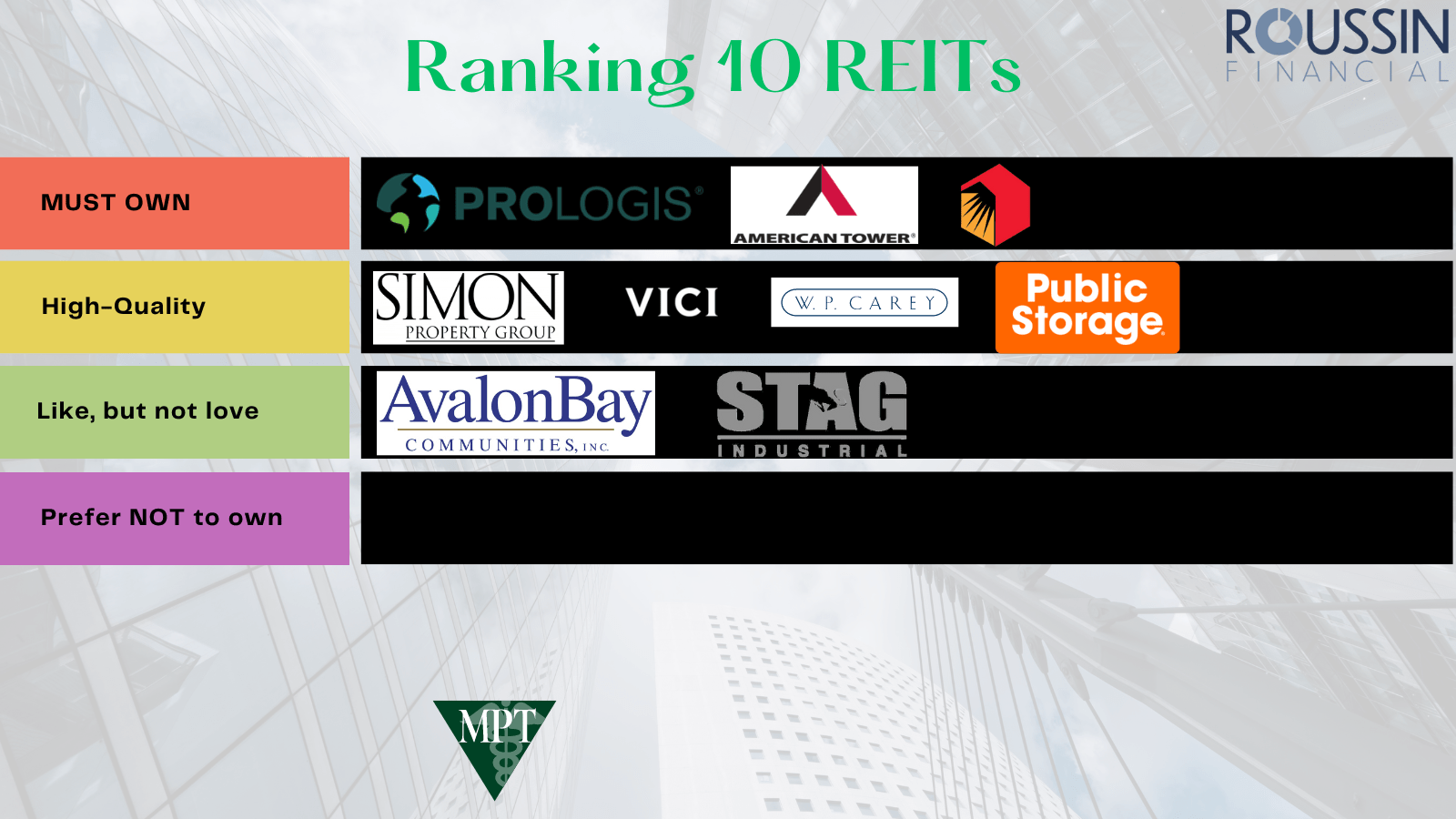

Ranking 10 REITs

REIT #1 - AvalonBay Communities

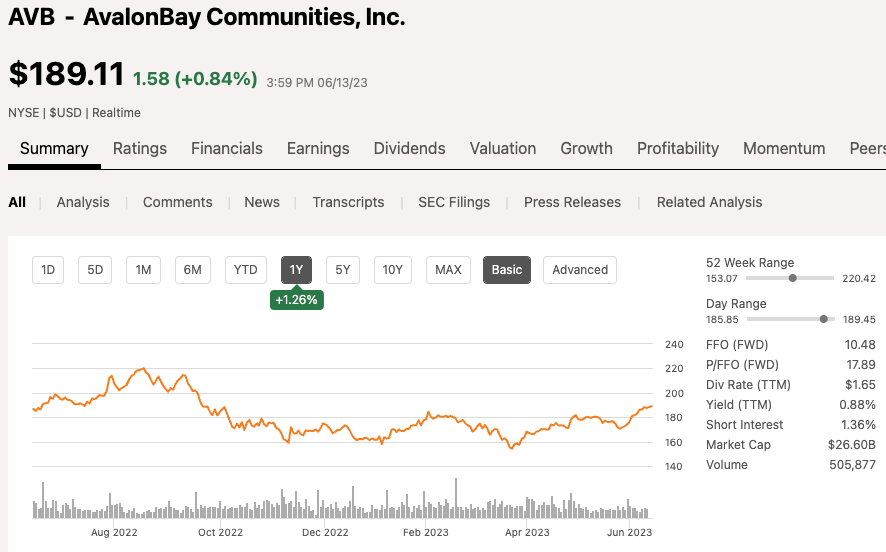

AvalonBay is one of the two largest apartment REITs in the US, and the 16th largest REIT overall. The company has a market cap of $26 billion. Over the past 12 months, shares of AVB are largely flat, up only 1%, however, year-to-date shares of AVB have climbed 17%.

{kind=link}

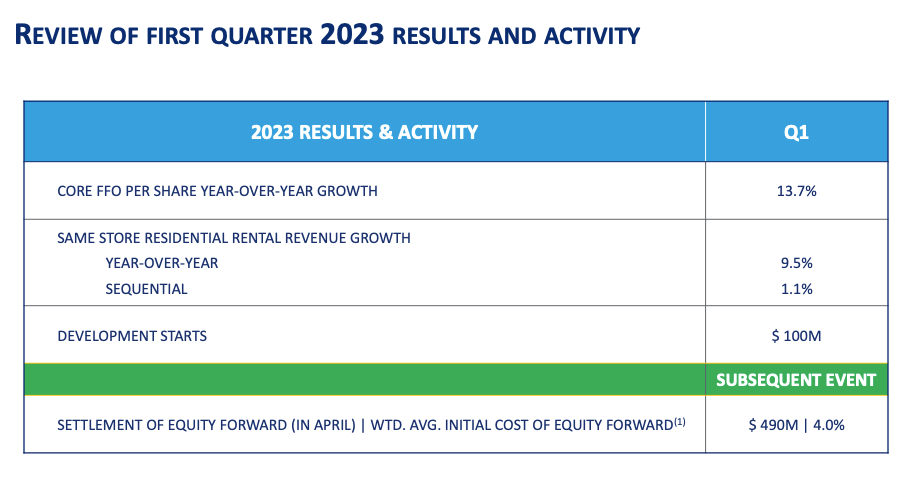

In Q1, the company reported 13.7% Core FFO per share growth and Same-Store rental revenue growth of 9.5%.

{kind=link}

REITweek, which is a large annual REIT conference, took place last week in New York where we got some updates from numerous companies. AvalonBay is one of those and management gave an operations update stating that through the first two months of Q2, rental revenues are up 6.5%, 80 basis points higher than management’s expectations. They also mentioned that occupancy levels ended May at 96.0%.

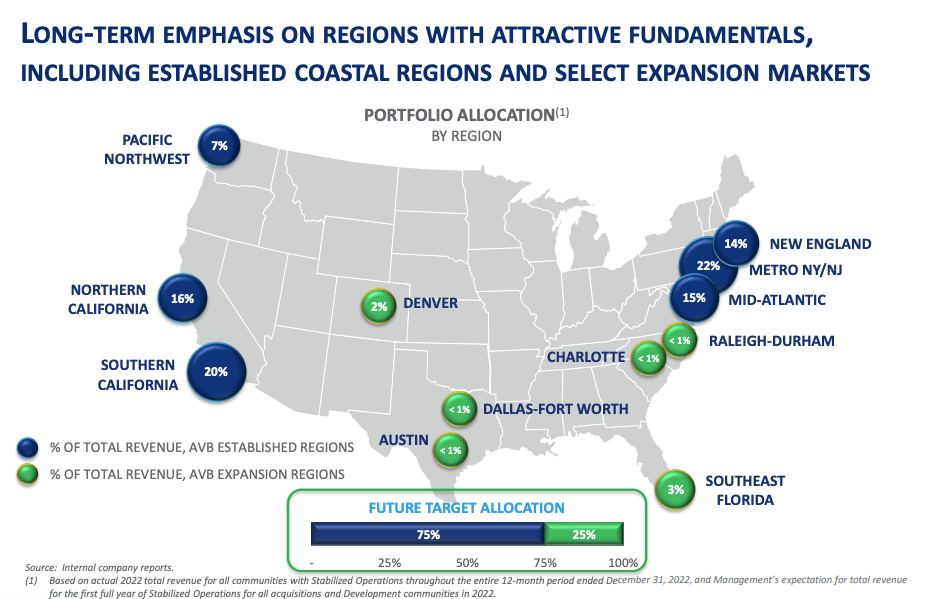

Looking at this chart you can see the majority of AvalonBay’s communities are found on both the West Coast and the East Coast

{kind=link}

AVB pays an annual dividend of $6.60 which equates to a dividend yield of 3.6%. AVB has been slow to raise their dividend over the years with a low five-year dividend growth rate of only 2%. The dividend recently got an increase but prior to that investors have not seen a dividend hike since 2019.

{kind=link}

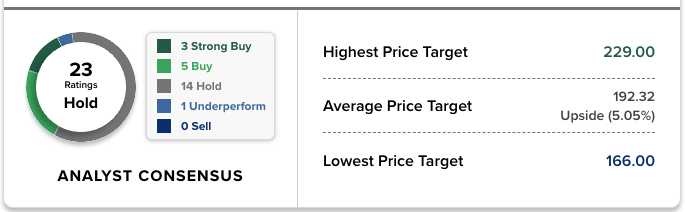

Analysts have a 12-mo average price target of $192, implying only 5% upside from current levels.

{kind=link}

So when it comes to rating AVB, I have to place them in the LIKE but not love category. They have a great portfolio and one of the largest Apartment REITs, but the lack of dividend growth and share price growth over the past decade is what has me placing the stock in this tier.

{kind=link}

REIT #2 - Prologis

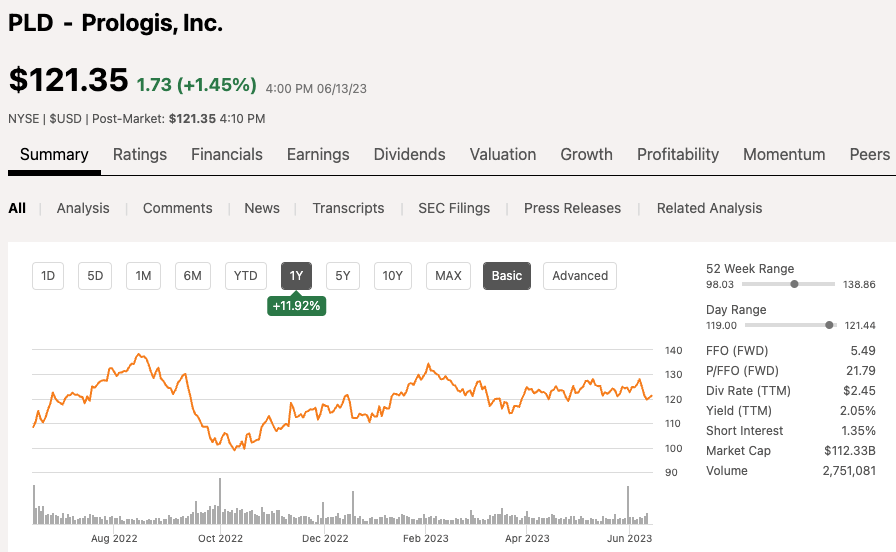

Prologis is the largest industrial and warehouse REIT in the US, a stock I own within my dividend portfolio. The company has a market cap of $112 billion. Over the past 12 months, shares are up 12%, and year-to-date shares of PLD are up 8%.

{kind=link}

One of the reasons I am so high on Prologis is due to the continued growth of e-commerce. If we fall into a recession, e-commerce sales are likely to slow, but long-term this is a trend that is expected to continue to go higher.

There are numerous ways to play e-commerce

- You can buy e-commerce companies like Amazon ( AMZN ) or Shopify ( SHOP )

- You can buy logistics companies like UPS ( UPS ) or FedEx ( FDX )

- A third way is buying the warehouse owners, like PLD

When you are a retailer that sells online, you need inventory. When you have a need for inventory, you have a need for space to store that inventory. When you need a place to store that inventory, odds are you call a company like Prologis to lease space.

Amazon is the company’s largest tenant, and not a bad tenant to have in terms of quality.

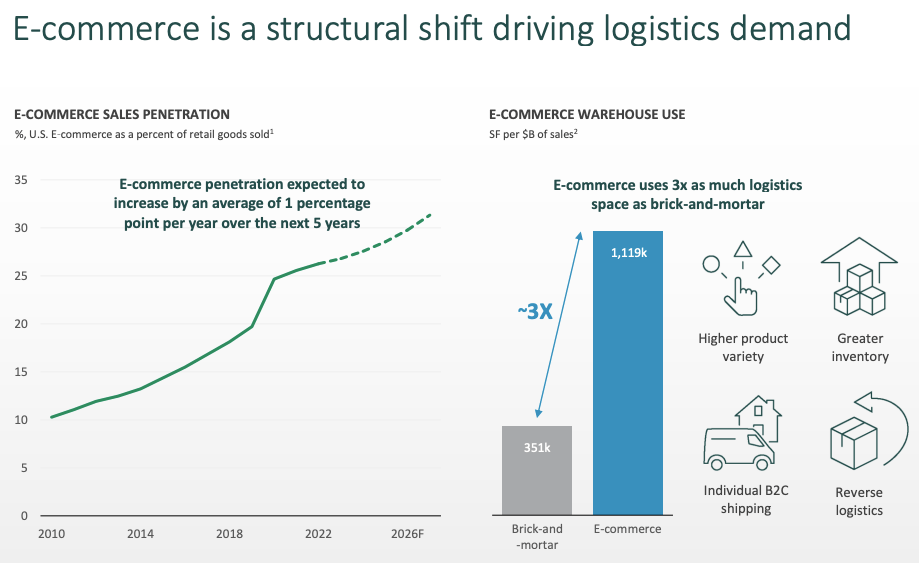

In 2010, e-Commerce sales accounted for only about 10% of retail sales. As of the end of 2022, e-commerce sales now account for a quarter of retail sales and economists believe growth will be about 1% per year over the next 5 years, which is enticing from an investor standpoint.

{kind=link}

E-commerce utilizes 3x more logistics space than brick and mortar, which makes sense because brick and mortar can hold inventory at their store and then do not have as big of a need for warehouse space, but e-commerce on the other hand needs to hold all inventory in a warehouse.

Looking at the dividend, Prologis yields a dividend of 2.8% and unlike AVB, Prologis has been growing their dividend at an average annual rate of 12.5%.

{kind=link}

Analysts have a 12-month PT of $145 on the stock, implying 15.5% upside from current levels.

{kind=link}

When it comes to rating, Prologis is a REIT I believe is one of the highest quality REITs on the market today and with the continued growth trend in e-commerce, this is a name I believe is a MUST own , so that is where we will put PLD, our first in that top category.

{kind=link}

REIT #3 - Simon Property Group

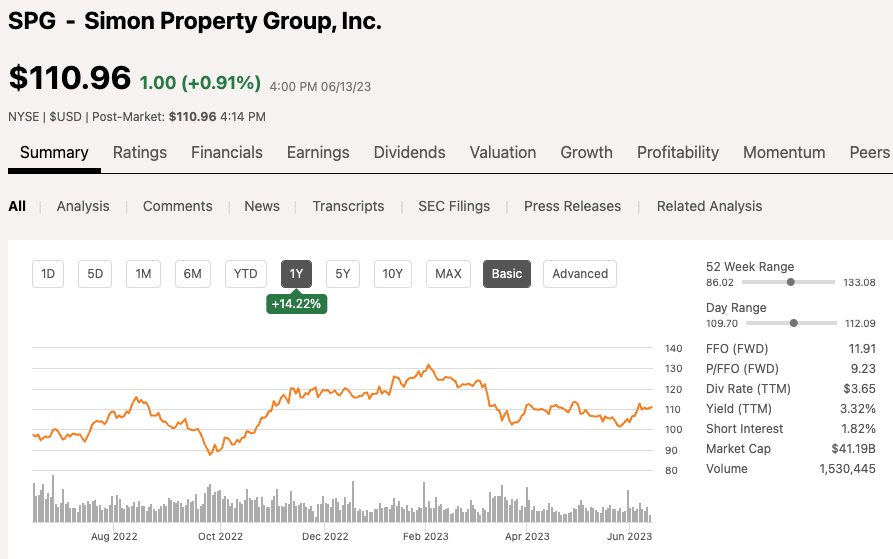

Now turning out attention to malls with SPG, who happens to be the largest and highest quality mall landlord on the market today. The company has a market cap of $41 billion. Over the past 12 months, shares of SPG have climbed 14%, but year-to-date shares are down 5%.

{kind=link}

If you are a believer that Malls are a thing of the past, then SPG is not a REIT for you. However, if you are like me and believe that high-quality malls still have a place on this earth, as not only a place for shopping, but also entertainment, and eating, well then SPG may be worth a second look.

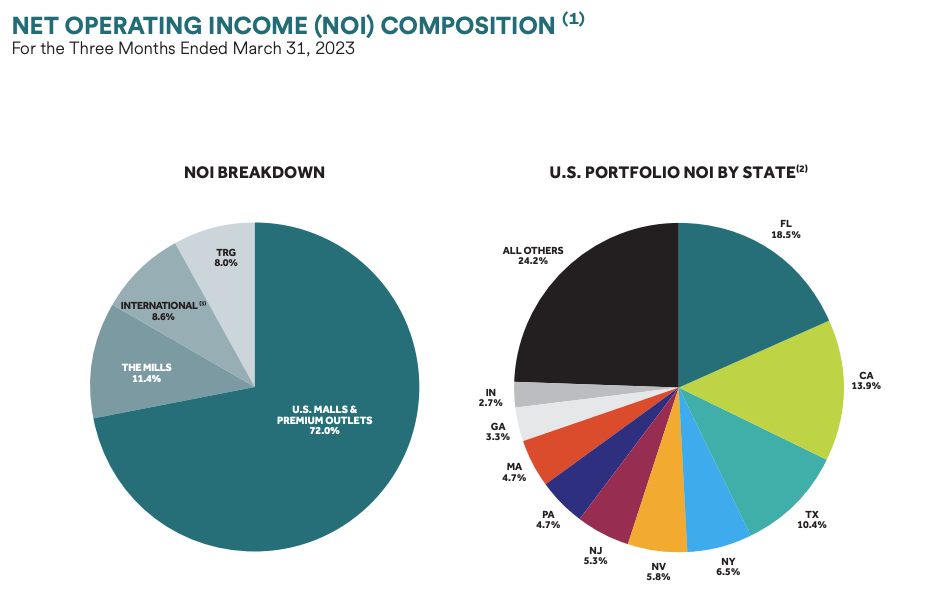

Looking at this chart you can see an NOI breakdown by property type as well as the REITs exposure by state.

{kind=link}

The majority, roughly 72% of the company's NOI comes from its mall and outlets portfolio. The top three states, accounting for 43% of NOI, are Florida, California, and Texas.

During the company's most recent quarter, SPG saw 4% portfolio NOI growth in Q1, which is a key stat to watch for SPG.

The company has a strong management team which has built a strong balance sheet and earned the company an A- credit rating to reflect its strength.

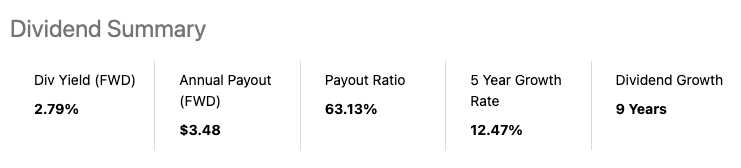

In terms of the dividend, SPG had to cut their dividend during the pandemic but they have quickly increased it back and now pay a dividend of $7.40 which equates to a yield of 6.95%.

Seeking Alpha

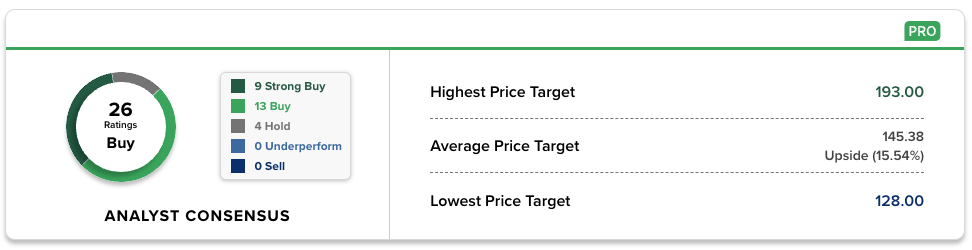

Analysts have a BUY rating on the stock with an average 12-month PT of $130, implying nearly 20% upside from current levels.

{kind=link}

Now for rating, I have owned SPG for quite some time now and have a cost basis in the low $50 range, so I have a lot of love for this REIT. As I mentioned earlier, I do not believe ALL malls will be around, but high-quality malls as a place of entertainment will be and SPG has the best mall portfolio around, so they are the only REIT I would trust in this sector. In addition, the company has a great management team, so because of all of that, I place SPG in the High Quality tier as they are best of breed within their sector.

{kind=link}

#4 - VICI Properties

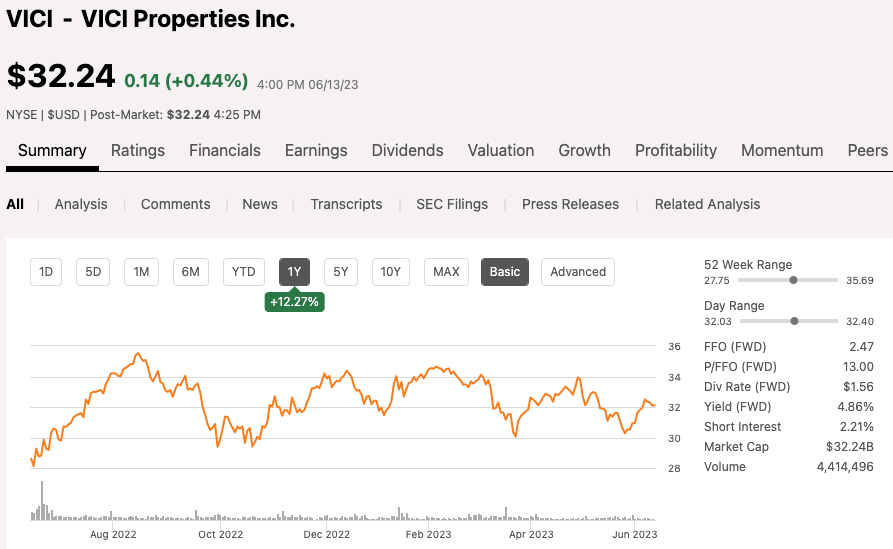

VICI Properties is a casino and hospitality REIT and the largest landlord on the Las Vegas strip. The REIT has not been around all that long, but they have hit the ground running, accumulating some of the best assets in its class. VICI currently has a market cap of $32 billion. Over the past 12 months, shares of VICI are up 12% and flat so far in 2023.

{kind=link}

As I mentioned, VICI is the largest landlord on the Las Vegas strip, an area that rarely EVER has FOR LEASE signs up because these operators enter into long-term master lease agreements of 20+ years.

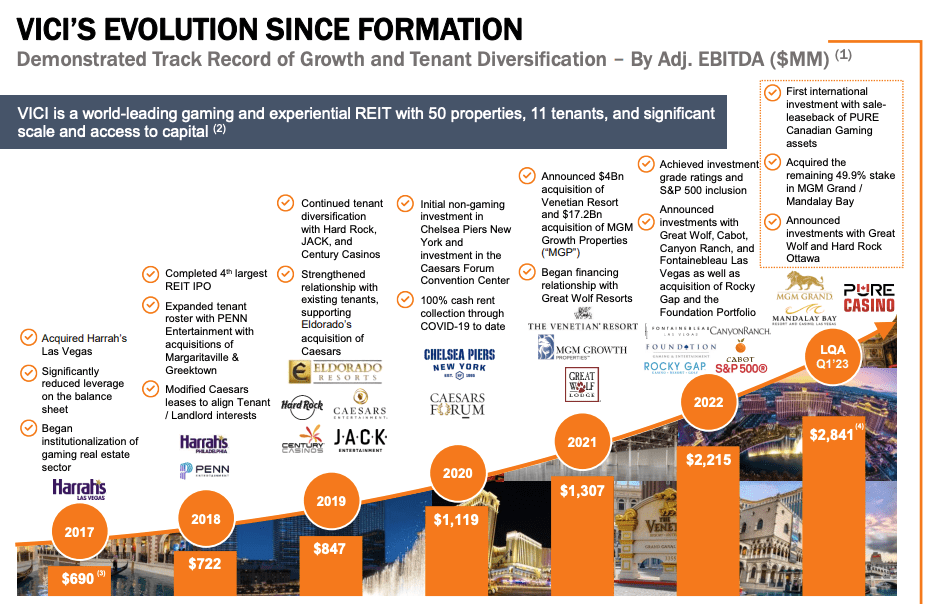

VICI went public in 2017 and has quickly been growing and expanding every year.

{kind=link}

The company currently owns great properties such as:

- Caesars Palace

- The Venetian

- MGM Grand

- Park MGM

- Mandalay Bay

- New York, New York

Not only has the company and portfolio continued to grow over the years, but so has the dividend, growing at a near 10% clip four out of five years. The dividend is well protected as even through the pandemic VICI maintained a 100% occupancy and rent collection rate. VICI currently pays an annual dividend of $1.56 per share which equates to a dividend yield of 4.9% and management has a target AFFO payout ratio of 75%.

Gambling and Casino traffic could stall if we fall into a recession, which would be unfortunate for the operators, but VICI is more focused on operators paying their rents, something they were able to do even through the pandemic. So, although operators could feel some pressure, odds have shown that even through a pandemic, these operators still made their monthly lease payments.

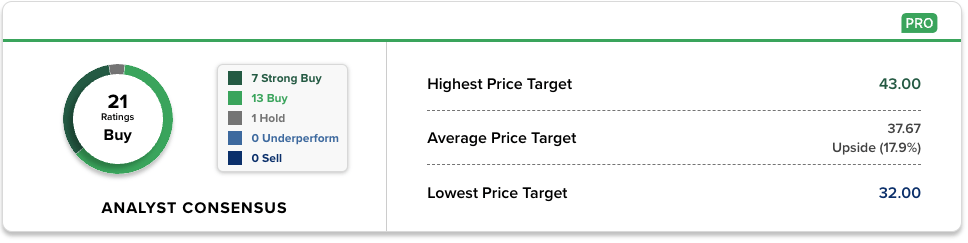

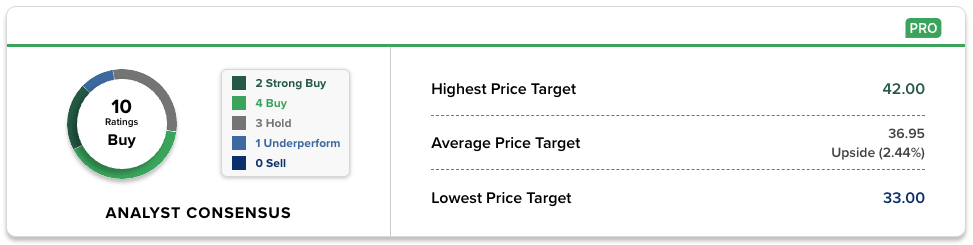

Analysts have a 12-month price target of about $38, implying 18% upside from current levels.

{kind=link}

Now for my tier rating. VICI is a stock I love, as it is actually my LARGEST individual REIT holding, but the track record is still early, so I will place them in the High-Quality tier and I will look for them to make the jump in the coming years if the results continue to impress.

{kind=link}

#5 - American Tower

American Tower is the largest cell tower REIT on the market today. The demand for sound data and cell service, as 5G and 5G continues to roll out around not only the US, but internationally, their is plenty of demand for a company like AMT.

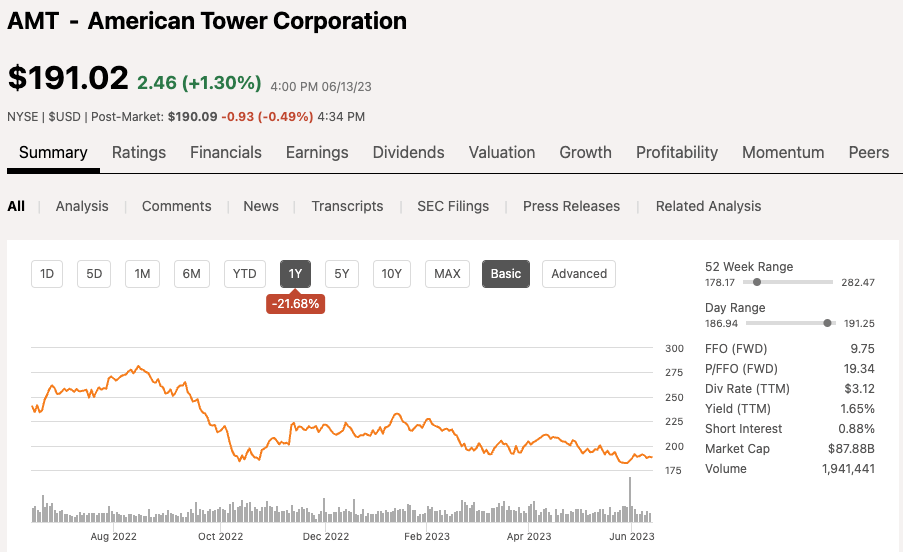

American Tower currently has a market cap of $88 billion. Over the past 12-months, shares of AMT are down a staggering 21%, falling 12% in 2023 alone.

{kind=link}

American Tower is another REIT that enters into long-term leases, leasing primarily to telecom giants like AT&T ( T ), Verizon Communications ( VZ ), and T-Mobile ( TMUS ).

When American Tower builds a cell tower, it has the ability to lease out up to three layers, which drastically improves the margins for that tower as the capex requirements are largely the same regardless of the number of tenants.

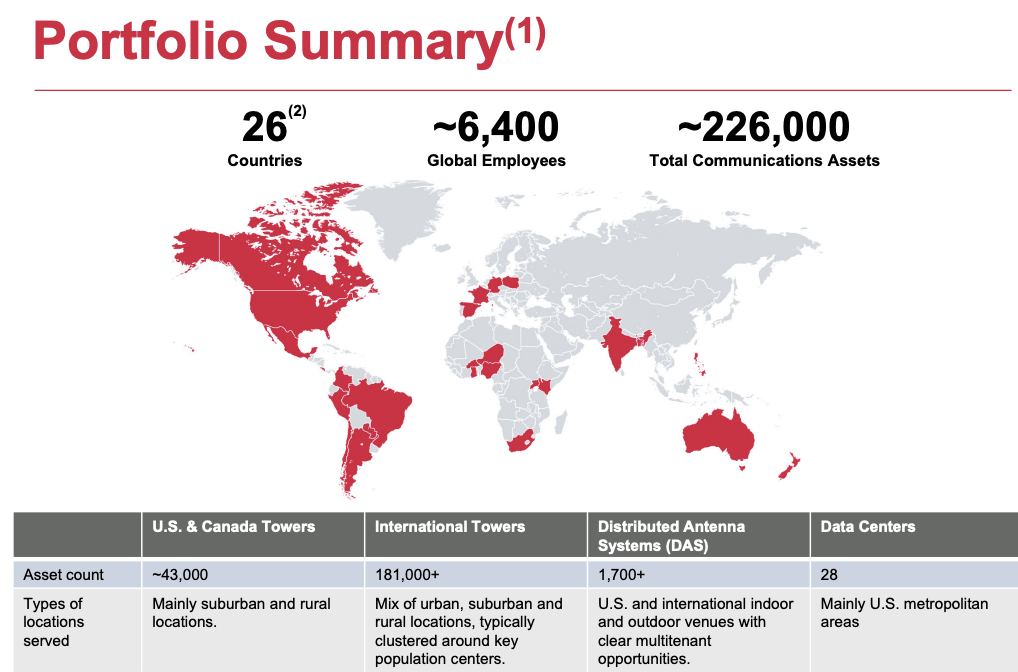

In addition to strong growth here in the US, American Tower continues to expand its reach internationally as well, which is another area that could provide a lot of growth for the company.

American Tower has a presence in 26 countries and has over 226,000 communication assets.

{kind=link}

American Tower has had a rough go over the past 12 months, but at the same time, it has provided a great opportunity for long-term investors looking for a great entry point. American Tower acquired another cell tower REIT, Core Site, for $10 Billion at the end of 2021, which is proving pricey at the moment. Sure the acquisition was poor timing looking back, but it was a long-term play for management. As you can see here, management has generated strong growth across key metrics of the business for years.

{kind=link}

American Tower is unique in the fact that they are a dividend growth REIT, which is not something you see all that often given how REITs are structured.

AMT currently yields a 3.3% dividend, which is high for them and over the past five years, the dividend has grown at an avg annual rate of 17%. In addition, management has increased the dividend for 10 consecutive years and counting.

{kind=link}

20 analysts have a BUY rating on the stock with an average 12-month PT of $241, suggesting 27% upside from current levels.

{kind=link}

AMT is a hard stock to pass up at current levels and in terms of tier rating, data and mobile is only becoming more in demand, which means a need for more towers, especially internationally. In my viewpoint, I rate AMT as a MUST OWN REIT and especially at these cheap levels.

{kind=link}

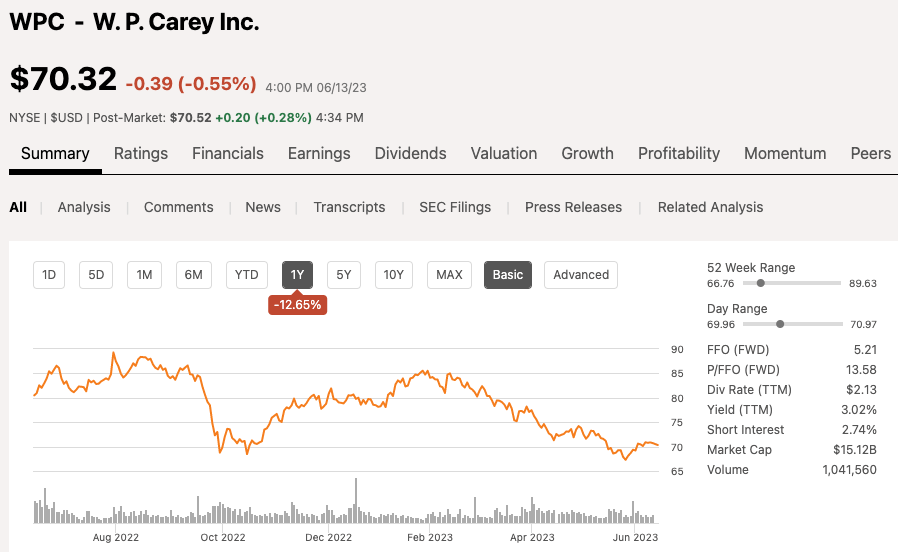

REIT #6 - W.P. Carey

W.P. Carey is a diversified REIT that has adjusted into becoming more of a player in the Warehouse and Industrial property sector over the past few years, a move that has proven to be quite positive.

WPC currently has a market cap of $15 billion. Over the past 12-months, shares of WPC are down 13%, including being down 10% this year alone.

{kind=link}

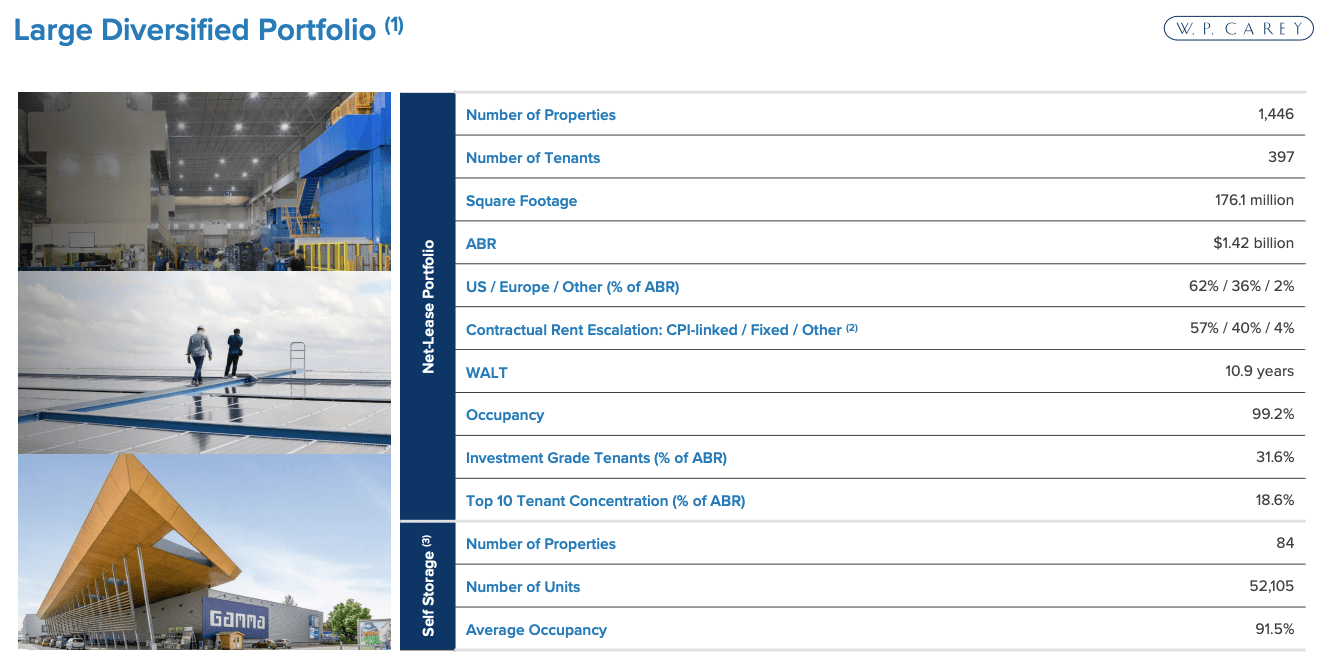

In terms of the portfolio, WPC has 1,446 net lease properties leased out to nearly 400 tenants. Those properties amount to 176.1 million sq ft and as you can see those properties are located not only here in the US but internationally as well, with the US accounting for 62% of ABR.

WPC enters into long-term leases and they currently have a weighted average lease term of nearly 11-years as of the end of Q1. The REIT operates with a very high occupancy rate of 99.2%.

{kind=link}

Here is a look at the Property Type Diversification based on ABR.

WPC Q1 Investor Presentation

As you can see, 51% ABR comes from Industrial and Warehouse properties with 17% each coming from both Retail and Office. Office is a number that has come down over the years, and a number I believe still needs to be reduced.

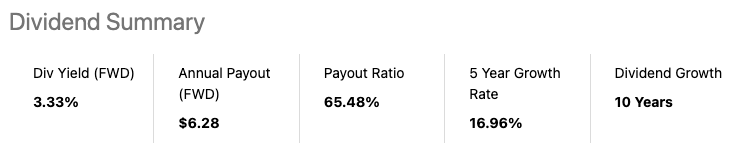

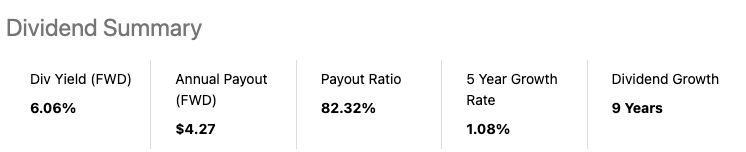

WPC has a high dividend yield of 6.1%, but that also comes with a low 1% 5yr DGR, which is often the case with higher yielding stocks

{kind=link}

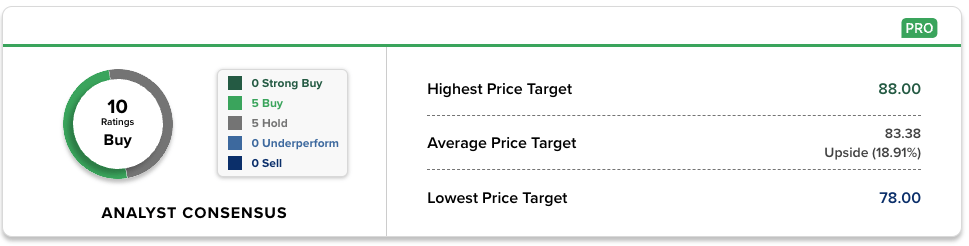

Analysts have an average 12-month PT of $83 for shares of WPC, implying 19% upside from current levels, which makes sense given their low multiple.

{kind=link}

The company is trading more in-line as an office REIT rather than an Industrial/Warehouse REIT, which provides for some great multiple expansion moving forward. Given that multiple expansion opportunity with their expansion in the Industrial and Warehouse sector, the stock is not a MUST OWN, but it is definitely in the High-Quality tier, which is where I placed them.

{kind=link}

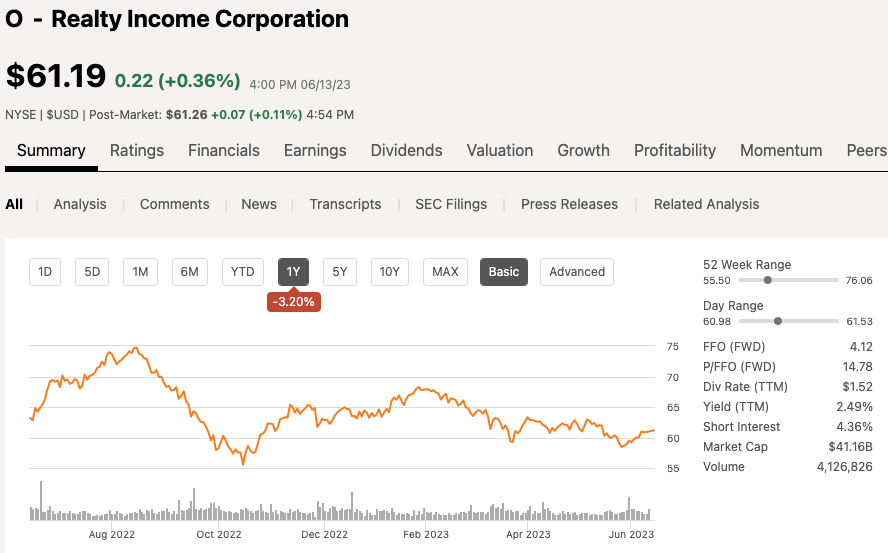

REIT #7 - Realty Income You can’t rank REITs without including The Monthly Dividend Company, Realty Income. I have covered Realty Income a number of times so I will not go into a ton of detail around the business, but they are what I refer to as the 'Gold Standard' when it comes to REITs.

Realty Income currently has a market cap of $41 billion. Over the past 12-months, shares of O are down 3%, and down 4% year to date.

{kind=link}

Even the best companies go through tough times, and Realty Income is no different. Over the years, anytime Realty Income's share price has fallen to where they yield a 5% dividend yield has proven to be a great entry point for long-term investors.

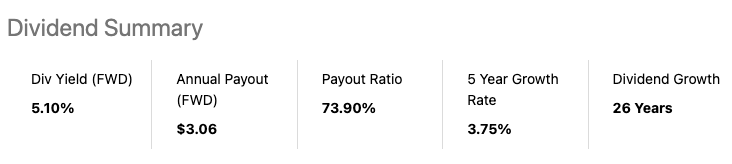

The dividend currently sits at 5.1% and that dividend is paid out on a monthly basis. The company is one of only 3 REITs on the Dividend Aristocrats list having increased their dividend for 25+ consecutive years. The dividend growth is low but consistent

{kind=link}

Realty Income partners with high-quality tenants, many being investment grade, which speaks to the safety of Realty Income. Here is a look at the top 10 tenants based on ABR:

Realty Income Investor Relations

Looking at the industry diversification, you can see how the company is well insulated from any pending recession in the US economy, given their sector exposure. The top industries, based on ABR, are grocery, convenience, dollar stores, and drug stores, which all scream recession proof to a degree.

Realty Income Investor Relations

Analysts have an average Buy rating on the stock with three analysts rating the REIT a strong buy. The average 12-mo PT from analysts is $69, which implies 15% upside from current levels.

{kind=link}

Realty Income is a best of breed REIT with:

- Strong Balance Sheet

- A rated credit rating

- Strong management team

- Proven Track record

- In demand Properties

This is one of those MUST OWN REITs in my opinion, which is exactly where I rate this stock probably, which probably does not come as much of a surprise.

{kind=link}

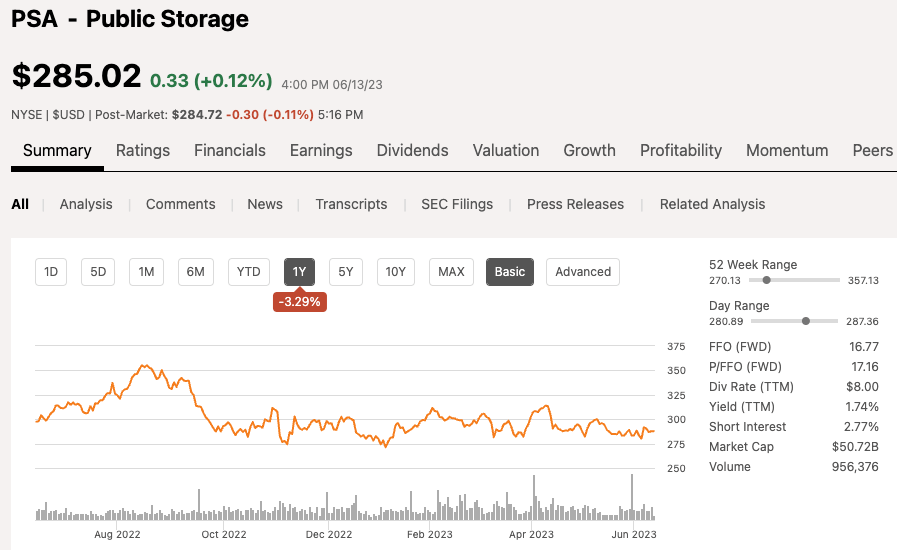

REIT #8 - Public Storage

Now we are moving into the Self-Storage industry with Public Storage, which happens to be the largest REIT in the sector by a pretty wide margin. However, the REIT does have plenty of competition from other REITs as well as private investors within the industry.

This has always been a favorite sector of mine because in a way, it is a recession proof business model, especially here in the US. Fact of the matter is, Americans have problems getting rid of stuff.

Public Storage currently has a market cap of $51 billion. Over the past 12-months, shares are down 3%, but up 4% in 2023.

{kind=link}

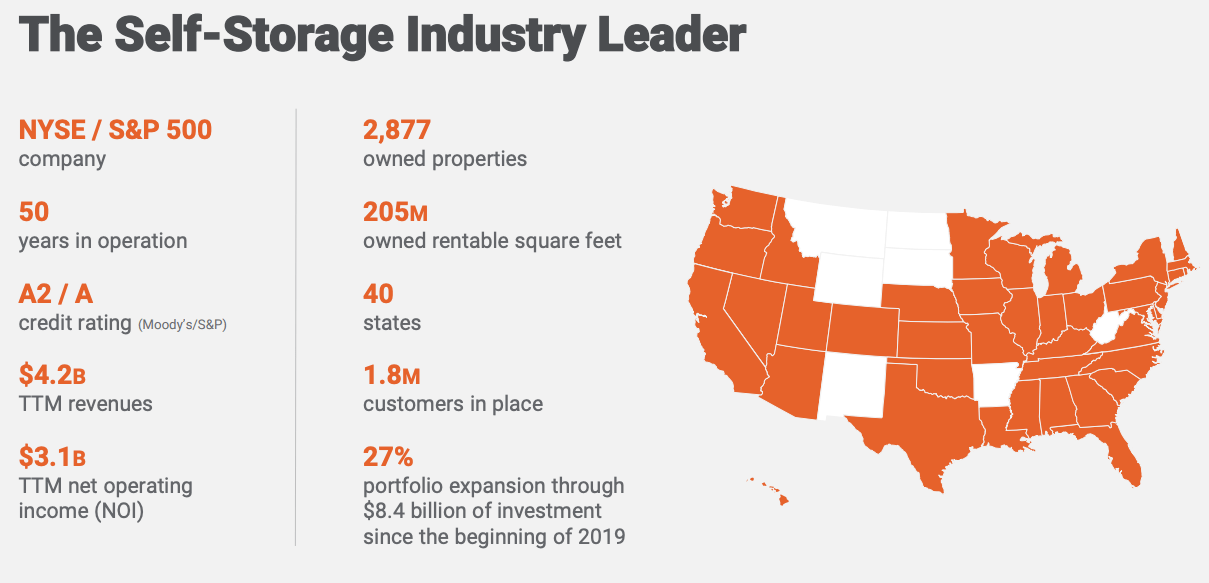

Public Storage has been in operation for 50 years now and they are the 4th largest REIT by Enterprise Value. The REIT also sports a high A credit rating based on its consistent performance and strong balance sheet. PSA has 2,877 properties within 40 states.

{kind=link}

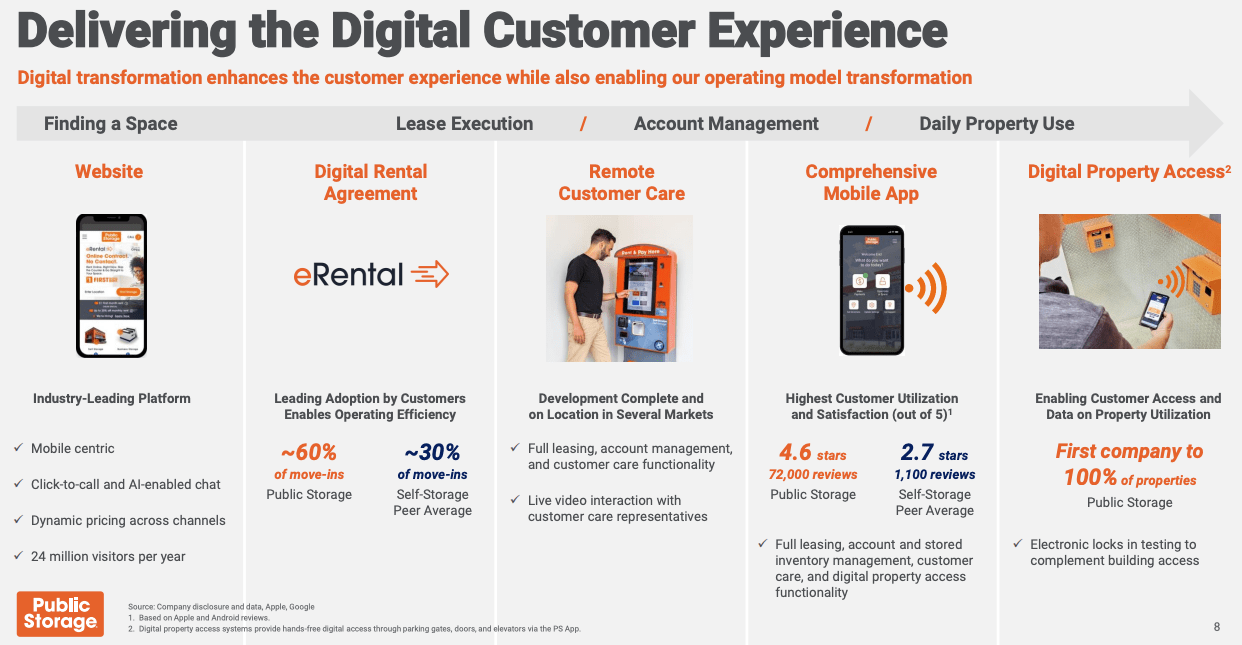

One of the drivers for the company in recent years has been their transformation to digital. You can literally rent a self storage unit without any human contact at all and go to your unit without interacting with an employee. PSA was the first company in its industry to have 100% of their properties have digital access.

{kind=link}

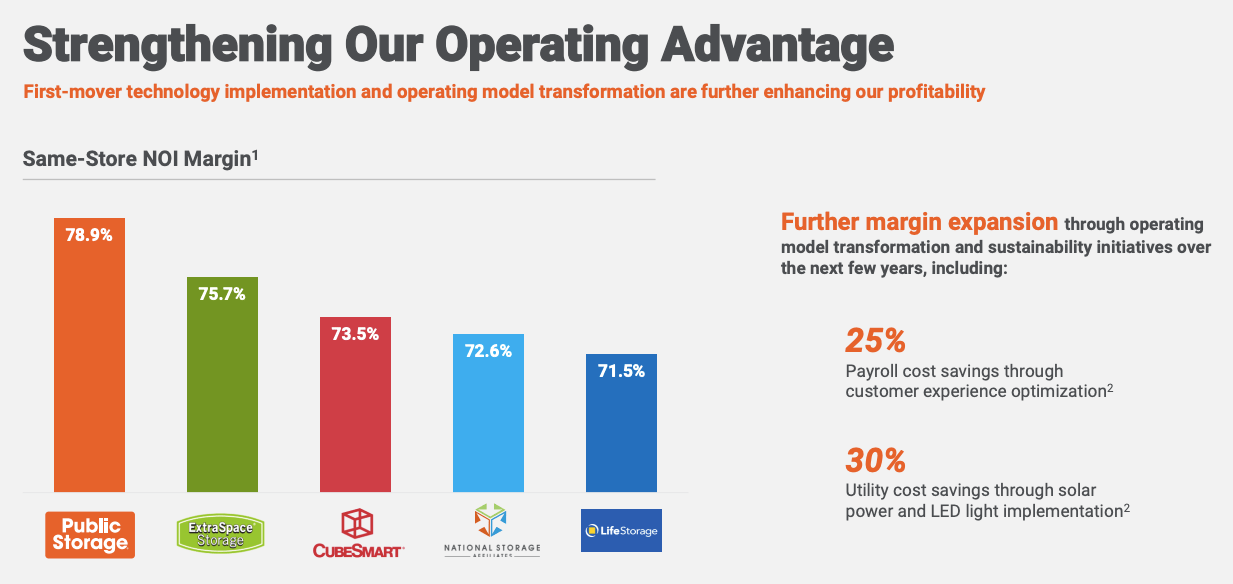

Given the presence and scale, Public Storage has been able to generate the highest Same-Store NOI margin, outpacing competitors such as Extra Space and CubeSmart, which is another self-storage REIT I like and own.

{kind=link}

The company continues to expand and develop to further grow their portfolio, outpacing the competition in terms of square feet by a wide margin.

PSA Investor Relations

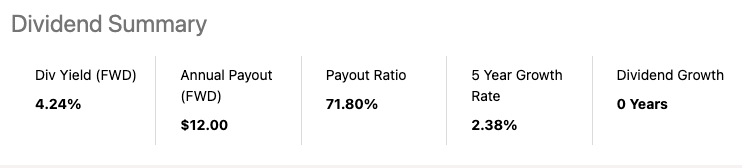

PSA pays an annual dividend of $12 which equates to a dividend yield of 4.2%. A solid yield, but where the company has been lacking has been in the dividend growth category as PSA only has a five-year dividend growth rate of 2.4%, however, in 2022 investors received a surprise $13.15 special dividend.

{kind=link}

Analysts are also high on PSA with 5 analysts rating the stock a strong buy and 4 a buy, with an average 12-month PT of $342, implying 22% upside from current levels.

{kind=link}

Public Storage is a very consistent company that is also more immune to economic slowdowns. As such, I place Public Storage in the High-Quality tier.

{kind=link}

REIT #9 - STAG Industrial

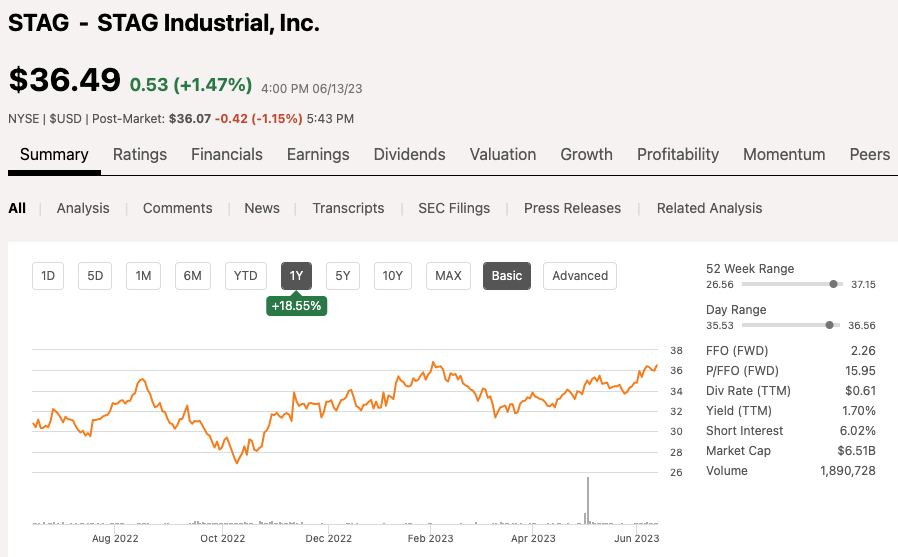

STAG Industrial, as you probably could guess, operates within the Industrial sector, competing with the likes of Prologis, a REIT we covered earlier. STAG currently has a market cap of $6.5 billion. Over the past 12-months, shares of STAG are up 19%, rising 13% in 2023.

{kind=link}

STAG is not at the same level as PLD but they have very similar qualities and tenants, AMZN also being a top tenant. I like STAG for many of the same reasons I mentioned with PLD in regards to e-commerce being a major reason and the growth expected over the next few years.

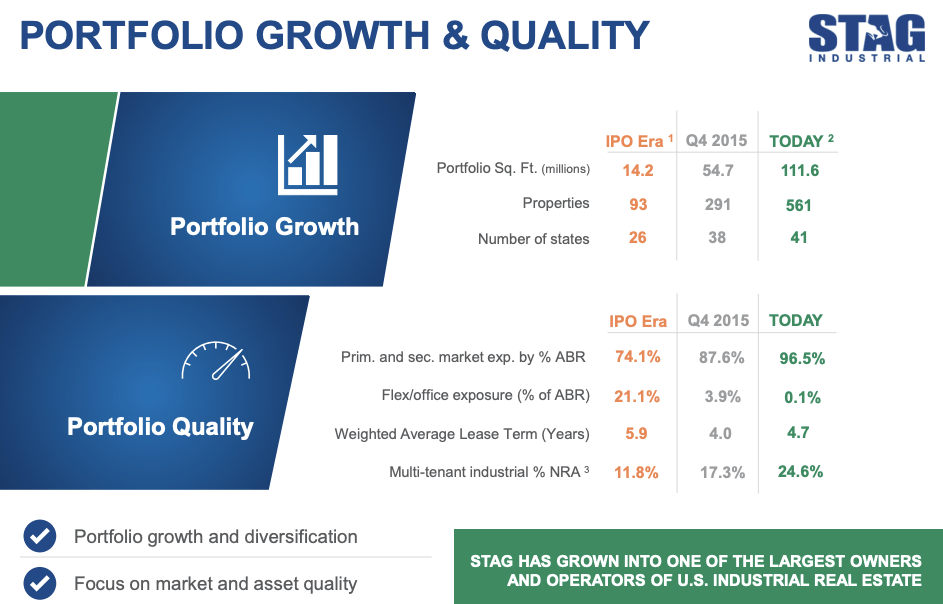

STAG is much smaller in size, but still growing. As you can see here when the company went IPO they had about 93 properties and today they have 561 properties within 41 states.

{kind=link}

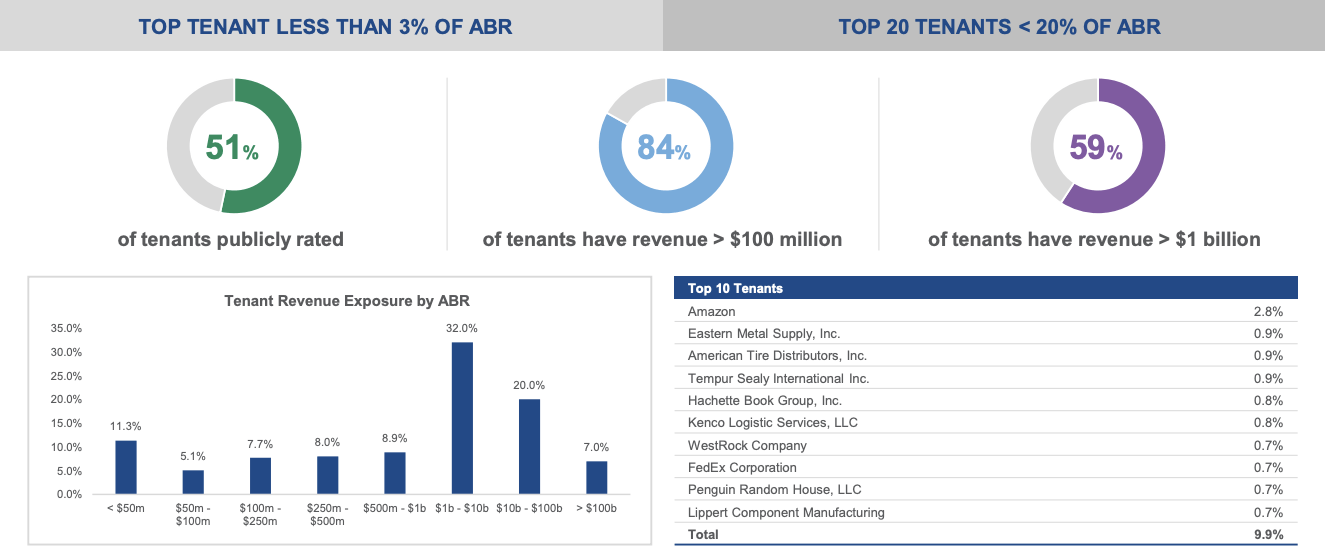

The REIT has a diverse tenant group with no tenant amounting to more than 2.8% of ABR, which is AMZN and the top 20 tenants account for less than 20% ABR overall.

{kind=link}

STAG pays a dividend yield of 4.2% with little to no dividend growth, which is not ideal. However, like Realty Income, STAG does pay out their dividend on a monthly basis which many retail investors like.

Analysts have a 12-month PT of $37 on the stock implying just 2.5% upside from current levels given the run the stock has already had this year, so valuation is not all that intriguing at this very moment, but that does not take away from the company as a whole.

{kind=link}

STAG is one of those companies that is just like AvalonBay. Consistent in nature, albeit STAG is still smaller and expanding, but they are not going to knock your socks off and in that sector, I much prefer Prologis, so in terms of rating, I place STAG in the Like, but do not love category.

{kind=link}

REIT #10 - Medical Properties Trust

We have reached the FINAL REIT on our list and I know many of you are eager to see where this REIT lands in my ranking. Medical Properties Trust is a REIT operating within the healthcare sector, primarily owning Hospitals and healthcare related facilities.

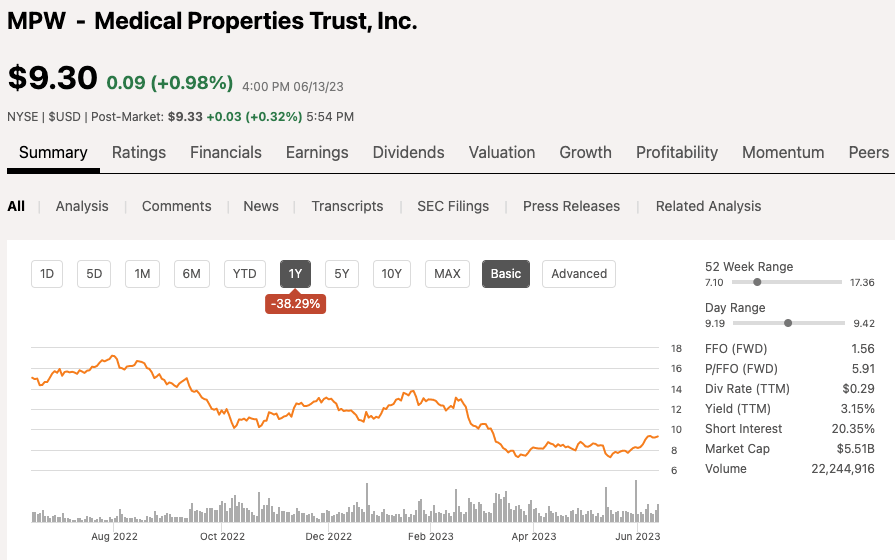

MPW currently has a market cap of $5.5 billion. Over the past 12-months, it has been a tough time for MPW shareholders as the stock has fallen nearly 40%, and is down nearly 20% in 2023 alone.

{kind=link}

There have been numerous reports that have come out over the past 12-18 months regarding analysts who have shorted the company. The reason has been related to management's lack of transparency as well as concerns regarding their overexposure to its top tenants.

On top of that, 2022 was one of the worst years in decades for the hospital sector in general.

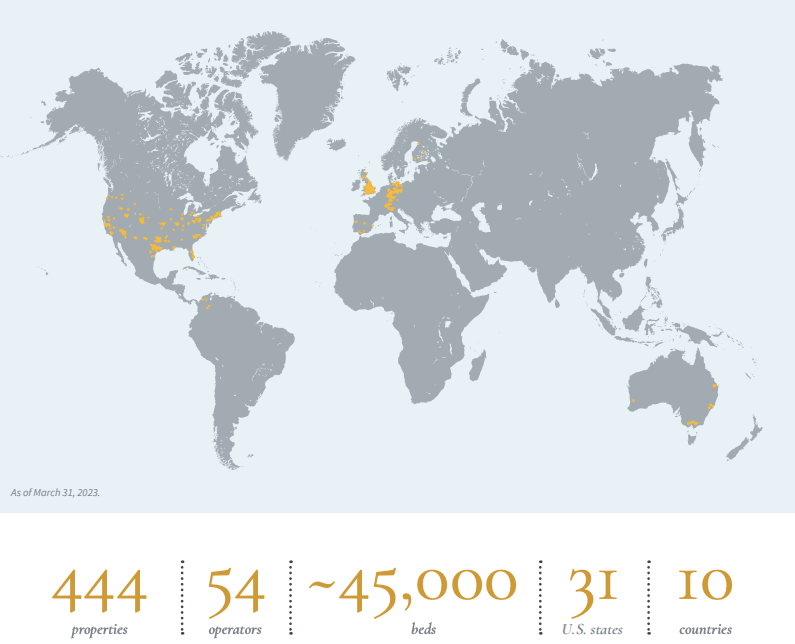

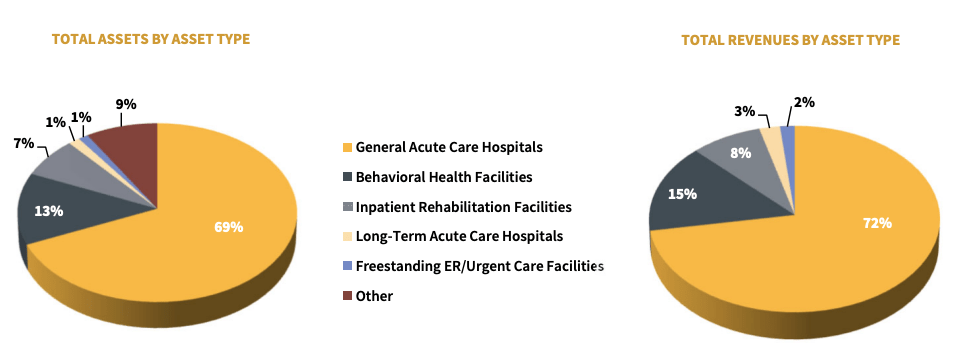

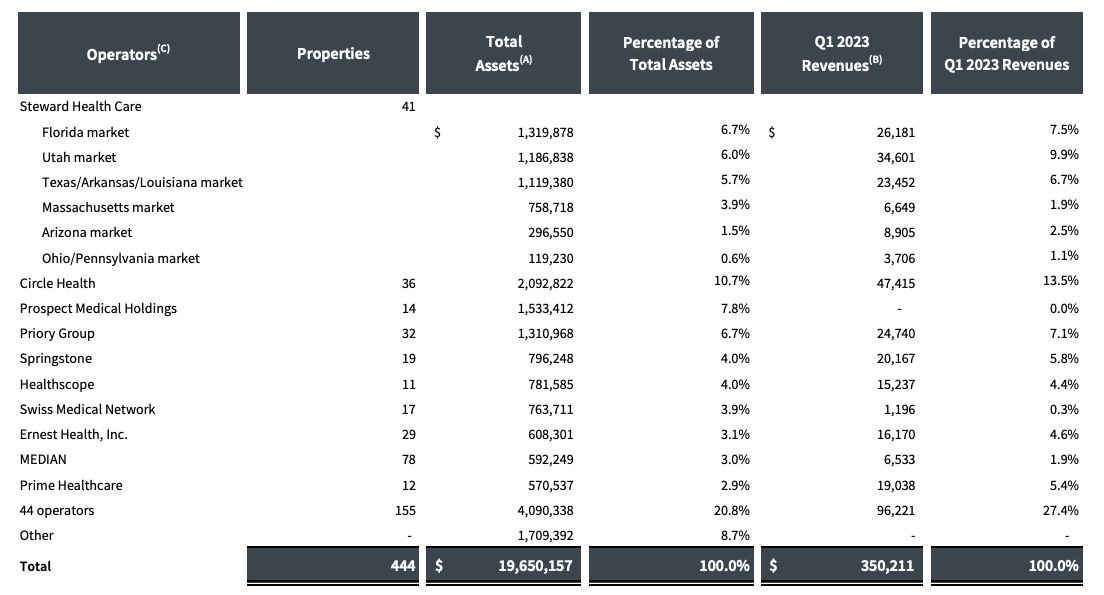

MPW has 444 properties leased out to 54 operators within 31 states.

{kind=link}

The majority of the revenue, about 72% comes from General Acute Care hospitals with 15% coming from Behavioral Health Facilities.

{kind=link}

MPW does not give you the total exposure by tenant, instead you have to do some additional work to add it up, but the REIT has large exposure to some of their top tenants, to which investors see as a red flag, especially when those tenants appear to be struggling.

{kind=link}

Hospitals are a necessity and will be around forever, but you still need a good game plan and management team to generate solid returns.

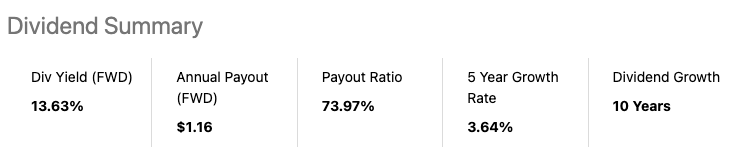

In terms of the dividend, after the stocks fall from grace, MPW yields a dividend of 13.6% which is EXTREMELY high. Management believes the dividend is sustainable, but I am not sold on that as much.

{kind=link}

This stock has too many red flags, but could be a candidate for a GREAT turnaround story if you are looking for riskier stocks like this. Do not let the yield fool you as you should NEVER invest based on yield alone.

Analysts are hoping for that turnaround with an avg 12-month PT of $11.67 implying nearly 30% upside from current levels.

{kind=link}

For me though, I have to rate this stock as a Prefer not to own just due to the lack of transparency, high exposure to single tenants, debt, and a lack of trust pertaining to the management team.

{kind=link}

Investor Takeaway

Today we looked at 10 REITs, ranking them based on quality and long-term viability of the company. This is not intended to be a buy list by any means, as valuations look intriguing for some and less intriguing for others.

In the comment section below, let me know what changes, if any, you would make to my ranking of these 10 REITs.

Disclosure: This article is intended to provide information to interested parties. I have no knowledge of your individual goals as an investor, and I ask that you complete your own due diligence before purchasing any stocks mentioned or recommended.

For further details see:

Ranking 10 REITs From Highest Quality To Lowest Quality