RJF - Raymond James Financial: 5 Reasons To Buy This Undercovered But Fundamentally Strong Bank

2023-06-17 00:07:02 ET

Summary

- Raymond James Financial receives a buy rating due to capital strength, revenue diversification, positive inflows, stable dividends, and a current price well below its 200-day SMA.

- The company's valuation seems slightly overvalued, when using P/E and P/B ratios.

- Risks to the bullish outlook include the firm's credit risk exposure, particularly non-performing loans and net charge-offs.

Summary.

Today I am rating financial sector stock Raymond James Financial ( RJF ), taking a modestly bullish sentiment on this company and giving it a buy rating due to 5 reasons: capital strength, revenue diversification, positive inflows, stable dividends, and a current price well below its 200 day SMA which I believe presents a value buy

Its valuation based on P/E and P/B ratios, however, seems slightly overvalued though.

Some of the risks to my modestly bullish sentiment are unique to the banking sector, but specifically for this firm it would entail credit risk from its portfolio of loan assets, which I will discuss further.

Company Brief.

Raymond James is a Florida-based firm tracing its roots back to 1962, and operates as a financial institution across several business segments including a private client group, capital markets, asset management, and banking.

In many cities in America, you can find a Raymond James branch where you can work with a financial advisor. In fact, I have passed by some of their branches in Austin, Texas many times, when I first got to know the brand.

Rating Methodology.

My updated rating methodology breaks down the analysis into the following 6 categories and scores each, with greater weight given to strong financial fundamentals, and less weight given to valuation and charting. The goal is to find an opportunity for value buyers based primarily on strong fundamentals.

- Capital Strength (20 points).

- Revenue Diversification (20 points).

- Net Inflows (20 points).

- Dividends (20 points).

- Valuation (10 points).

- Price Chart (10 points).

A cumulative score is assigned and a rating given based on that score:

(Strong Sell: 0 points, Sell: 10 to 20 points, Hold /Neutral: 30 to 80 points, Buy: 90 points, Strong Buy: 100 points).

Capital Strength is There.

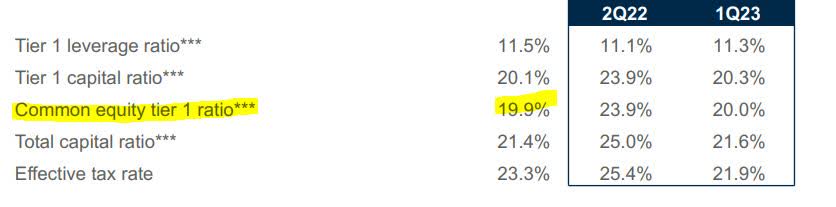

First, I am looking at the CET1 ratio in the most recent quarterly results :

Raymond James - CET1 (Raymond James - quarterly presentation)

{kind=link}

With a CET1 of 19.9% , this is significantly above the regulatory Basel III benchmark of 4.5%, so another sign they are well capitalized as a financial firm.

Importantly so, since Wikipedia lists this firm as #41 on the top banks by assets in the US.

From a forward looking perspective, I think this puts the firm on a firm footing to weather any financial shocks in 2023, which still has more than half a year to go.

Further, the banking sector panic in March may actually have worked in the favor of this firm, which clients saw as a safe port in the storm.

According to a March article in the Tampa Bay Business Journal , "Raymond James is among the larger institutions to receive deposits from angsty bank customers in recent days."

So, in terms of capital strength I would give it a score of 20 points .

Revenue Diversification is Strong.

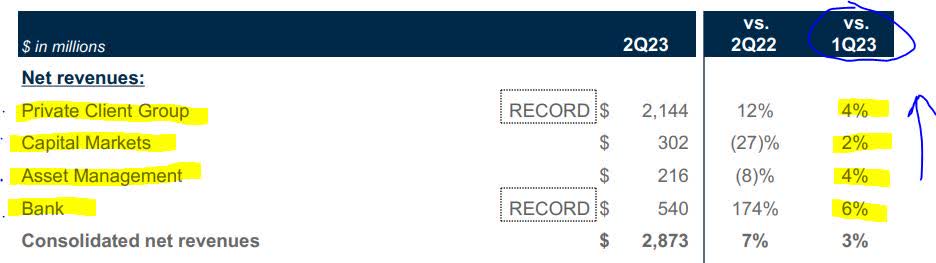

From the most recent quarter that ended in March (which was Q223 in this company's fiscal year), I see a highly diversified revenue base across 4 business segments:

Raymond James - Quarterly results - Revenue Diversification (Raymond James - quarterly presentation)

{kind=link}

One notable figure to point out is their banking segment saw 174% YoY growth in net revenue, however their private client group also did well at 12% YoY growth, while others fared better in QoQ comparisons.

What I am looking for in this firm is that it is not overly dependent on one business segment, geographic region, or revenue stream.

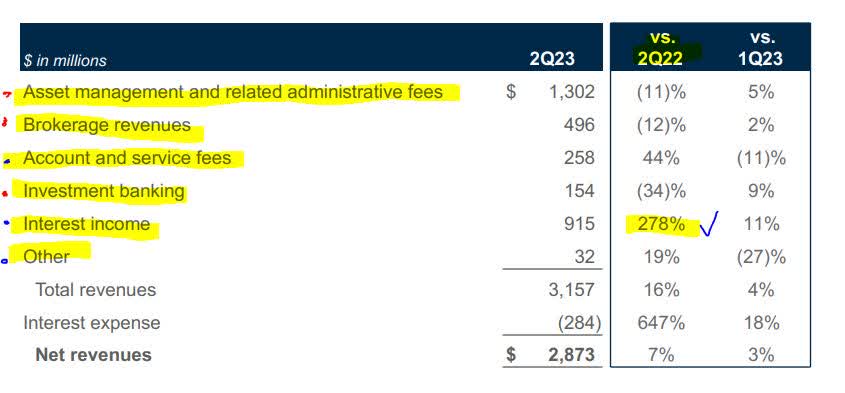

Drilling down further in their most recent quarterly earnings presentation, you can see diversification across multiple income streams:

Raymond James - quarterly results - interest income (Raymond James quarterly presentation)

{kind=link}

Most notably to point out here, is a 278% increase in interest income YoY.

However, interest income makes up only about 29% of the pot, with the leading revenue driver being asset management fees.

Staying on the topic of interest income, though, since it is a such a noteworthy discussion topic in the markets in the last year, we see a strong growth in NIM for this firm since 2022Q2, as evidence that the current rate environment is in its favor:

Raymond James - quarterly results - NIM (Raymond James Financial - quarterly presentation)

Therefore, because this firm can produce revenue not only from the current rate environment but also from several other revenue segments, I give this category a score of 20 points .

Net Inflows in Right Direction.

Unlike tech companies, which I also cover... having worked in the tech sector... which depend on selling of products and solutions, firms like Raymond James essentially make money by managing the capital of others. This type of business depends on inflows of client funds for Raymond James to look after. If suddenly a bunch of clients start pulling funds out, the firm is in trouble.. fast.

How are the net inflows going for this firm in the last quarter?

From the most recent earnings release,

The Domestic Private Client Group saw net new assets of $21.5B for the fiscal second quarter, 8.4% annualized growth rate from beginning of period assets.

CEO Paul Reilly in his earnings comments struck a positive tone:

We generated strong domestic net new assets of $21.5B during the quarter, an annualized growth rate of 8.4%, in spite of the volatile market conditions, as advisors continue to value our advisor- and client-focused culture, along with conservative financial management. The strong net new asset growth, along with the inflow of balances into the newly-launched Enhanced Savings Program in March, demonstrated our advisors and clients’ confidence in the firm’s strength and stability.

Also noteworthy is that their quarter ended with client assets under administration of $1.22T and financial assets under management of $194.4B.

These are quite impressive numbers.

Another Seeking Alpha analyst, Welbeck Ash Research , said it best in their April analysis :

Clients remain confident in RJF's ability to weather the coming bear market and the subsequent uptick in activity.

So, for this category I give it a score of 20 points.

Dividend Growth Stable and Reliable.

As a dividend-oriented analyst, I am always looking for stocks that generate a recurring quarterly dividend income just for holding on to them, but also have a competitive dividend yield among peers within the same sector, for comparison purposes.

Taking dividend info from Seeking Alpha , I see that this stock is paying $0.42 per share, with an upcoming ex-date on June 30th, and a dividend yield of 1.68% as of June 16th.

The dividend growth from January 2022 until now went from $0.34 to $0.42 a share, a 24% growth in 1 year.

One of its listed peers is Interactive Brokers Group ( IBKR ) with a paltry dividend of $0.10, and a yield of 0.49%.

Another peer is Robinhood Markets ( HOOD ) which does not pay a dividend at all.

So, when it comes to dividends I am going with Raymond James as the proven leader in this peer group, and so in the category of dividends I give it a score of 20 points.

Valuation.

From valuation data on Seeking Alpha , the two valuation metrics I want to look at is the forward P/E Ratio (GAAP method) and the forward P/B Ratio, as these are the two metrics I use for all companies I rate here.

This stock has a PE (price to earnings) ratio of 11.52, which is 21% over the median PE of its sector, however it is below the S&P 500 median P/E of 14.93, as of May 2023.

Its PB (price to book) ratio is 2.04, 106% above its sector's median PB ratio, and above the 1.0 benchmark , where anything above 1 starts to become overvalued.

So, based on valuation, I don't see it being highly competitive within its sector in terms of these two valuation metrics, so this category earns a score of 0 points .

Price Chart Still has Value Buying Potential.

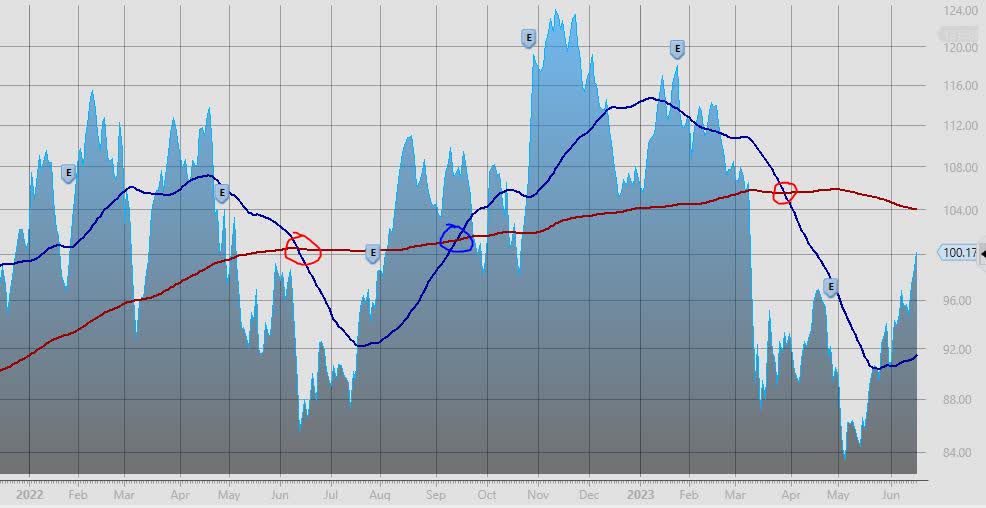

The following is the price chart at market open on Friday June 16th :

Raymond James - Price Chart on June 16 (StreetSmartEdge trading platform )

{kind=link}

In this chart, as in prior articles, I am tracking the 50 day simple moving average (solid blue line) vs the 200 day simple moving average (solid red line).

We see a death cross formation (red circle) in June 2022, followed by a golden cross (blue circle) in September 2022, and then another death cross in March 2023.

At the moment, the current death cross seems to be starting a reversal back upward in June, however I think there is still a buying opportunity that can be snagged.

I like this stock in the $92 to $100 range at this time, while it remains well below its 200 day SMA, offering a value buying opportunity to someone looking to add this stock to a mix of diversified financial sector stocks, if you are focusing on being an expert in one industry.

For this reason, in the category of price chart I give it a score of 10 points .

Risks to my Outlook.

The risk to my modestly bullish outlook on this stock are tied to the sector it is in, banking, and the unique credit risk that poses for a firm like this who has a major banking component.

Here are two metrics I am following: provisions for credit losses and net chargeoffs.

In the larger macro picture, a June article by S&P Global brought light to the larger macro issue:

Credit card delinquencies and net charge-offs are continuing to quickly climb back toward pre-pandemic levels, and major lenders are anticipating further deterioration if expectations for an increase in unemployment materialize.

The increase in jobless claims was pointed out also by a Reuters article on June 9th, saying claims are at a 1.5 year high.

Specifically to Raymond James, the question is how their own credit risk is impacted. The following is from their last quarterly results:

Raymond James Financial - net chargeoffs and PCL (Raymond James - quarterly presentation)

{kind=link}

When looking at the above, from that last quarterly presentation, their provision for credit losses increased by 33% YoY , and their net chargeoffs increased 1,900% YoY .

It will take a few more quarterly results to analyze, in my opinion, before seeing how much exposure this firm has in this space, but also how the larger macro picture effects this specific firm. A few more quarters that show increasing loan losses could make many investors bearish, countering my bullish argument on this firm.

On a positive note, which could calm down naysayers of this stock, is the firm's own earnings comments on criticized loans (an early warning indicator for credit stress):

The credit quality of the loan portfolio remained strong, with criticized loans as a percent of total loans held for investment ending the quarter at 0.92%, down from 2.63% at March 2022 and 1.01% at December 2022.

Therefore, their credit stress seems to be managed for now, and not a cause for overly bearish selling, although it does remain a risk worth noting.

In the next earnings release, I will be looking for the firm's leadership setting a confident forward-looking guidance when it comes to their credit risk. If they do so, this will help the bullish thesis.

Conclusion.

In conclusion, I reiterate my Buy rating for this stock, which scored 90% in my cumulative analysis.

Its 5 positives are capital strength, revenue diversification, positive net inflows, stable dividends, and current price range.

This is offset by showing slightly overvalued vs its sector median, when it comes to P/E especially.

Risks to my bullish outlook are that the larger macro picture affects this specific firm who has a major banking component and therefore subject to credit risk, particularly for nonperforming loans and chargeoffs. This risk is mitigated by what appears to be an improvement in the credit quality of their loan portfolio, although it is a risk worth keeping an eye on in the next quarterly results. Hence, I am avoiding a "Strong Buy" rating at this time.

In closing, this often undercovered stock (last coverage was April) should be given a closer look based on the evidence I showed. In addition, the money management space overall has for the most part, with some exceptions, proven it can weather the market shocks to the sector we saw in March, and come out of it as a value buying opportunity.

In particular, large money managers like this are not going away, I think, as there are literally trillions in capital in the economy that has to be parked somewhere, managed, and put to work.. and many of these needs go beyond just that of a what a traditional bank does. Further, the turbulence in regional banks this spring caused additional demand to park funds at more stable, established, bigger firms, which this one certainly is.

For further details see:

Raymond James Financial: 5 Reasons To Buy This Undercovered But Fundamentally Strong Bank