RYAM - Rayonier Advanced Materials: Improving EBITDA Free Cash Flow And Debt Ratios

2023-03-27 15:04:57 ET

Summary

- RYAM's net debt-to-EBITDA has been decreasing since 2019 and reached 4.16x at the end of 2022, which is anticipated to sit at 3.5x in 1Q 2023.

- In 2023, RYAM’s adjusted free cash flow should be way better than in 2022 and 2021.

- The global demand for high-purity cellulose is expected to increase in the following years.

- Due to the changing consumer behavior, and environmental trends, RYAM can likely benefit incrementally from higher prices of cellulose specialties products in the upcoming years.

- The stock is a buy.

From October 1 to December 30, 2022, Rayonier Advanced Materials ( RYAM ) stock price increased by more than 200% as the company's 2H 2022 financial results were relatively strong, then the stock price decreased. Year-to-date, the stock's price is down 36% as RYAM's 1Q 2023 financial results are not expected to be as strong as in 4Q 2022 and 3Q 2022. However, the company's full-year 2023 financial results are expected to be attractive. RYAM expects its 2023 adjusted EBITDA to be between $200 to $215 million, compared with 2022 adjusted EBITDA of 177 million, and 2021 adjusted EBITDA of $127 million. The market outlook for RYAM's high purity cellulose is strong. Also, RYAM can benefit from higher prices for its paperboard and high-yield pulp (as a result of increasing demand for packaging and commercial printing end markets, and also, improved productivity and logistics in China).

Quarterly results

In its 4Q 2022 financial results, RYAM reported net sales of $500 million, compared with 4Q 2021 net sales of $374 million, driven by increased high purity cellulose sales, paperboard sales, and high-yield pulp sales. In the full-year 2022, RYAM net sales increased by 22% YoY to $1717 million, as sales prices and volumes increased in 2022. However, it is worth noting that compared with 2021, RYAM's cost increased due to higher chemicals prices, increased wood fiber prices, and also increased energy and logistics costs. RYAM's operating loss of $14 million in 4Q 2021, turned into an operating income of $16 million in 4Q 2022. The company reported a full-year 2022 operating income of $26 million, compared with a full-year 2021 operating loss of $10 million. Furthermore, in the full-year 2022, in order to enhance reliability and productivity, RYAM used $138 million in its investing activities

Despite better financial results in 4Q 2022 compared with 4Q 2021, RYAM's results in the third quarter of 2022 were better than in the fourth quarter, as the average high purity cellulose and paperboard prices in the fourth quarter of 2022 were lower than in the third quarter due to lower demand). The company's adjusted EBITDA from continuing operations increased from $27 million in 4Q 2021 to $68 million in 3Q 2022, then decreased to $55 million in 4Q 2022.

"The quarter's financial results demonstrate the focus the RYAM team has on improving our operational performance and reducing our debt levels. Higher production volumes and improvements in our supply chain and logistics processes led to higher sales volumes and greater cash generation," the CEO commented.

The market outlook

In 2022, high purity cellulose sales accounted for 77% of RYAM's total sales (excluding eliminations). In 2023, the demand for construction ethers, food additives in microcrystalline cellulose, and tire cord may not be as strong as in 2022. Also, due to the higher interest rates in major economies, inflation, and the fear of a financial crisis, the demand for viscose was limited in the first months of 2023. But, the reopening of China may cause the demand for viscose to increase in the following months. Also, the demand for acetate, casings, filtration, and nitrocellulose is increasing. Thus, the prices of high purity cellulose are supported in 2023, in my view.

Moreover, sustainability issues have caused consumers to prefer paper packaging to plastic packaging in recent years and this trend is getting stronger. Thus, paper packaging is capturing a major share of the packaging industry. Also, in different industries like cosmetics, clothing, footwear, and food, companies are trying to eliminate plastic and use paperboards instead, as they are more environment-friendly and can increase the quality of products. Thus, higher paperboard demand can be expected in the following years.

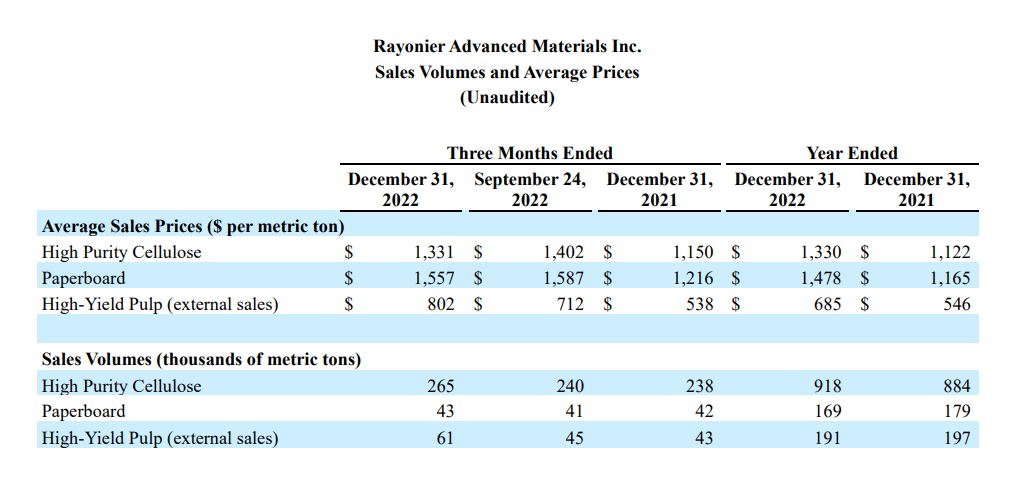

Figure 1 shows that RYAM's high purity cellulose sales volume increased from 884 thousand metric tons in 2021 to 918 thousand metric tons in 2022. Also, the company's high purity cellulose average selling price increased from $1122 per metric ton in 2021 to $1330 per metric ton in 2022. According to Expert Market Research , the global cellulose market is expected to grow at a CAGR of 4.1% from 2023 to 2028. Also, according to MarketsandMarkets , the global regenerated cellulose market was valued at $18.0 billion in 2022 and is projected to reach $27.3 billion by 2027, growing at a CAGR of 8.7%. The drivers of the cellulose market growth in the following year can be rapid urbanization and the changing consumer preferences in emerging economies, as regenerated cellulose is increasingly replacing petrochemical fibers.

Figure 1 - RYAM's sales volumes and average prices

{kind=link}

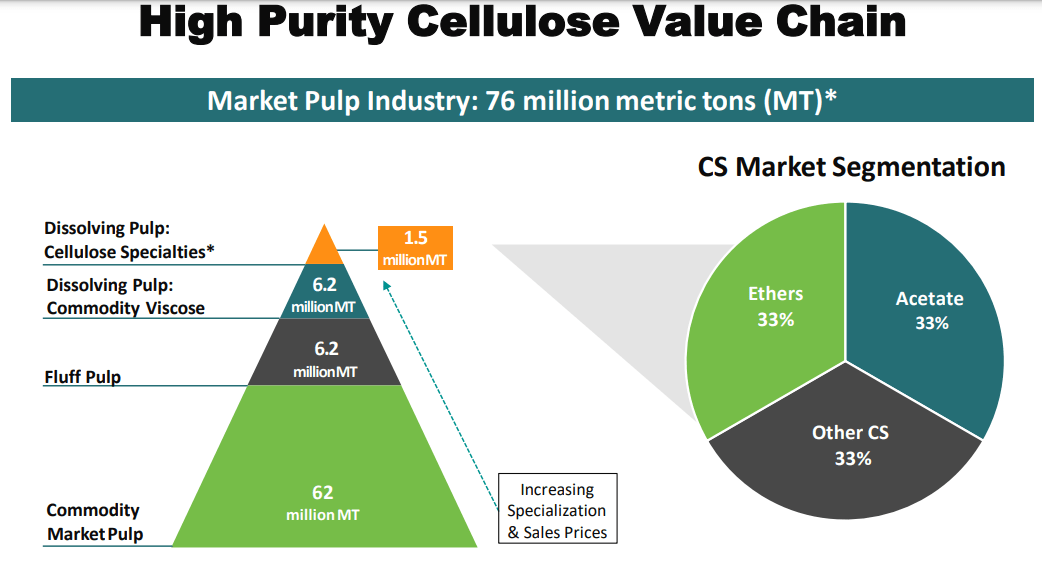

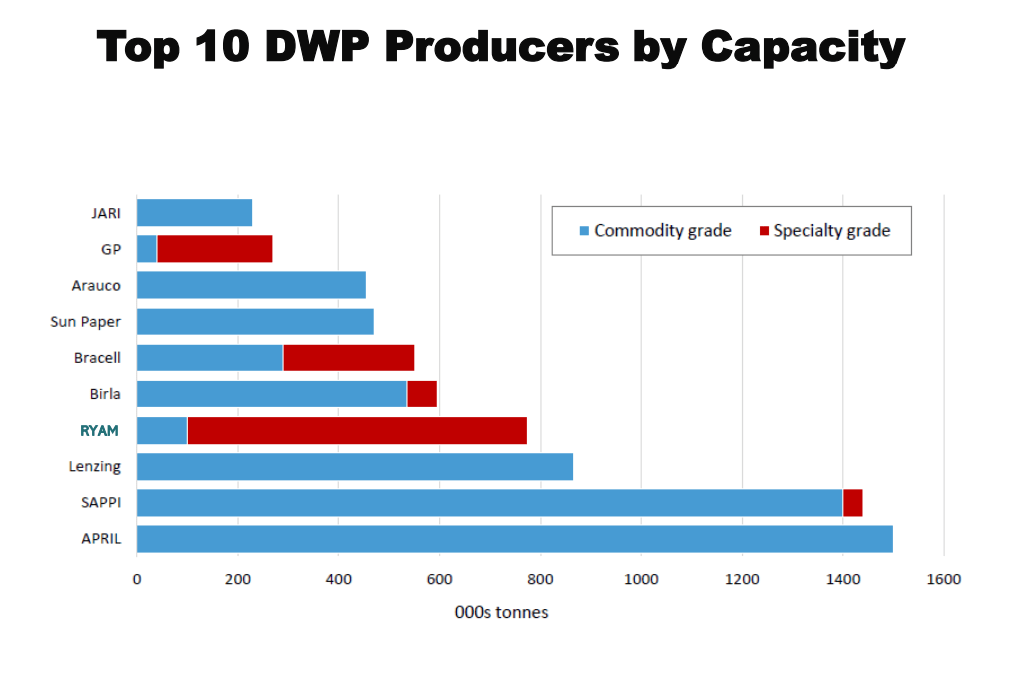

RYAM's high purity cellulose products are acetate, ethers, microcrystalline cellulose, high tenacity rayon, nitrocellulose, viscose, and fluff, which are used if tow, plastics, food, pharmaceuticals, tire cord, filtration, and industrial thickeners markets. According to Figure 2, Ethers and acetate account for 66% of the cellulose specialties ((CS)) market segmentation. With higher specialization, the sales prices increase and RYAM is the leader in cellulose specialties (see Figure 3) and is one of the Dissolving Wood Pulp ((DWP)) top 10 producers. The DWP market is forecasted to grow at a CAGR of 3.2% from 2022 to 2023, reaching $7623 million. It is worth mentioning that dissolving pulp contains high cellulose of more than 90% and is largely used in textile products. Figure 4 shows the dissolving pulp market share by application in 2028. We can see that the viscose sector is anticipated to lead the dissolving pulp market in the upcoming years.

Figure 2 - High purity cellulose value chain

{kind=link}

Figure 3 - Top 10 DWP producers by capacity

{kind=link}

RYAM performance

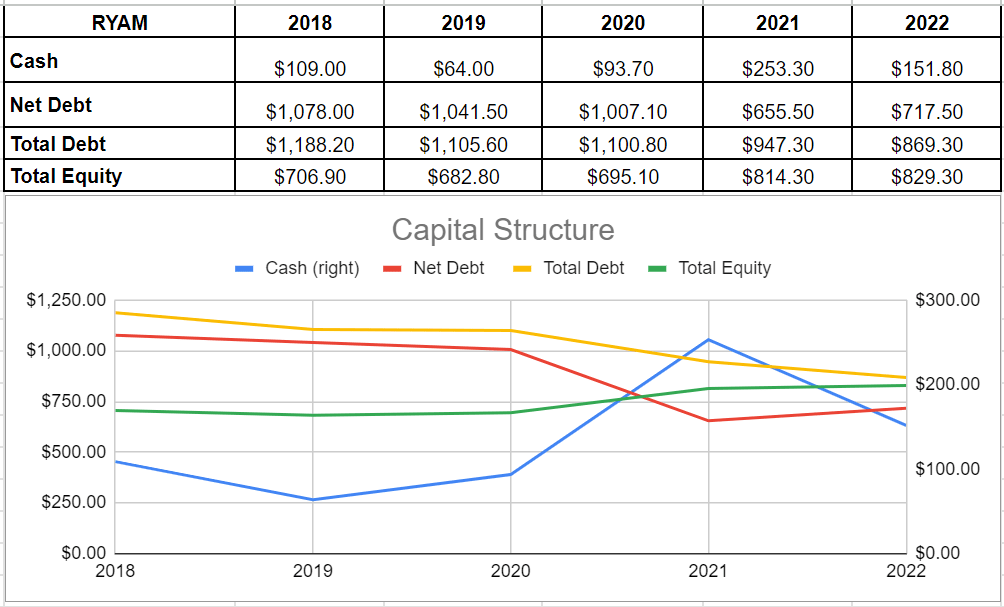

Since the end of 2021, the company's cash and equivalents have decreased by approximately 40%, from $253 million to $152 million in 2022. However, the company has managed to reduce its debt level by repaying debt in 2022, resulting in a drop from $947 million in 2021 to $869 million at the end of 2022. Due to the decrease in both cash balance and debt level, there has been a 9% increase in net debt level from $655.5 million in 2021 to $717.5 million in 2022. On a positive note, RYAM has increased its equity level from $814 million in 2021 to $829 million at the end of 2022, representing a modest increase of 1%. The net debt level is well below the equity level, providing ample opportunity for future risks and financing. The company plans to reduce its gross debt to approximately $840 million in 2023 and further down to $750 million within three to five years (see Figure 4).

Figure 4 - RYAM's capital structure (in millions)

{kind=link}

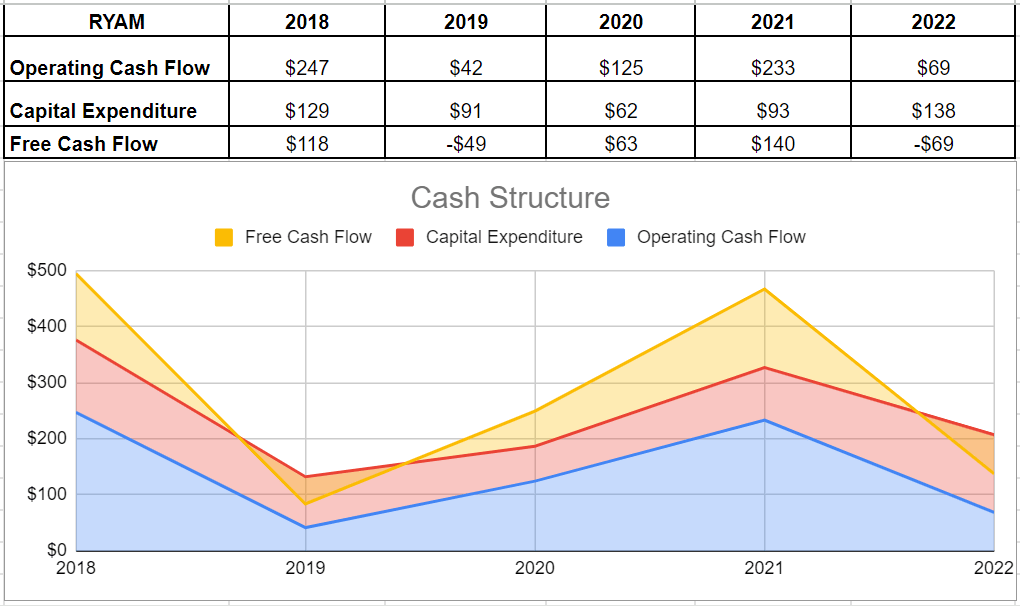

Furthermore, an examination of RYAM's cash structure reveals that the company's cash operations have declined in recent years, with a final figure of $69 million in 2022 compared to the previous year's $233 million. Additionally, the company's capital expenditures have risen by 48% to $138 million in 2022 from $93 million at the end of 2021. It is important to note that RYAM has invested in high-return internal strategic CapEx projects that will yield paybacks within three years and increase its return on equity ratio to over 20%. The company also plans to increase its capital expenditures to $140-145 million in 2023. However, the decrease in operating cash flow caused negative free cash flow of $(69) million in 2022. Nevertheless, according to their 2023 guidance, they anticipate generating positive free cash flow of $30-55 million and achieving adjusted free cash flow of $30-60 million (see Figure 5).

Figure 5 - RYAM's cash structure (in million)

{kind=link}

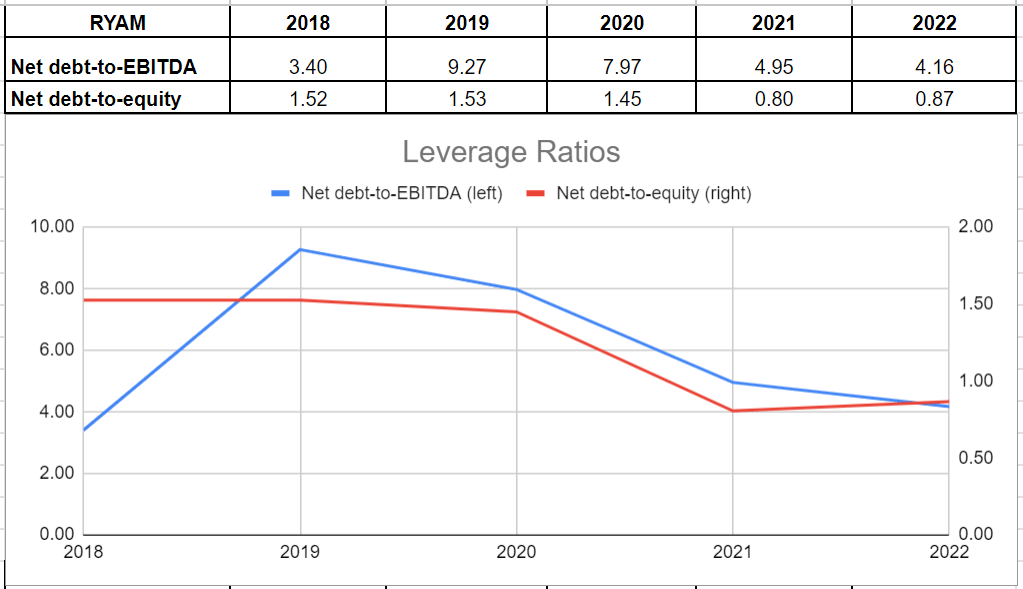

Furthermore, I have included some leverage ratios to demonstrate RYAM's credit ratings. It is important for investors to monitor a company's debt levels as high debt can hinder their ability to acquire new equipment or meet other obligations. Therefore, I assessed the financial health of RYAM by analyzing its leverage condition through net debt-to-EBITDA and net debt-to-equity ratios. The net debt-to-EBITDA ratio indicates the likelihood of defaulting on issued debt and can help determine how many years of EBITDA would be required for RYAM to repay its debt. It is evident that RYAM's net debt-to-EBITDA has been decreasing since 2019 and reached 4.16x at the end of 2022. Additionally, RYAM aims to achieve a net debt-to-adjusted EBITDA ratio of 3.5x by the end of the first quarter of 2023 and maintain this level throughout the year. The company's net debt-equity ratio also reflects its strong leverage position, measuring the proportion of net debt and financial liabilities to total shareholders' equity. This ratio is used to determine whether a company's capital structure leans towards debt or equity financing. RYAM has consistently reduced its net debt-to-equity ratio in recent years, with the exception of 2022 when it increased slightly to 0.87x from 0.8x in 2021 (see Figure 6).

Figure 6 - RYAM's leverage ratios

{kind=link}

Valuation

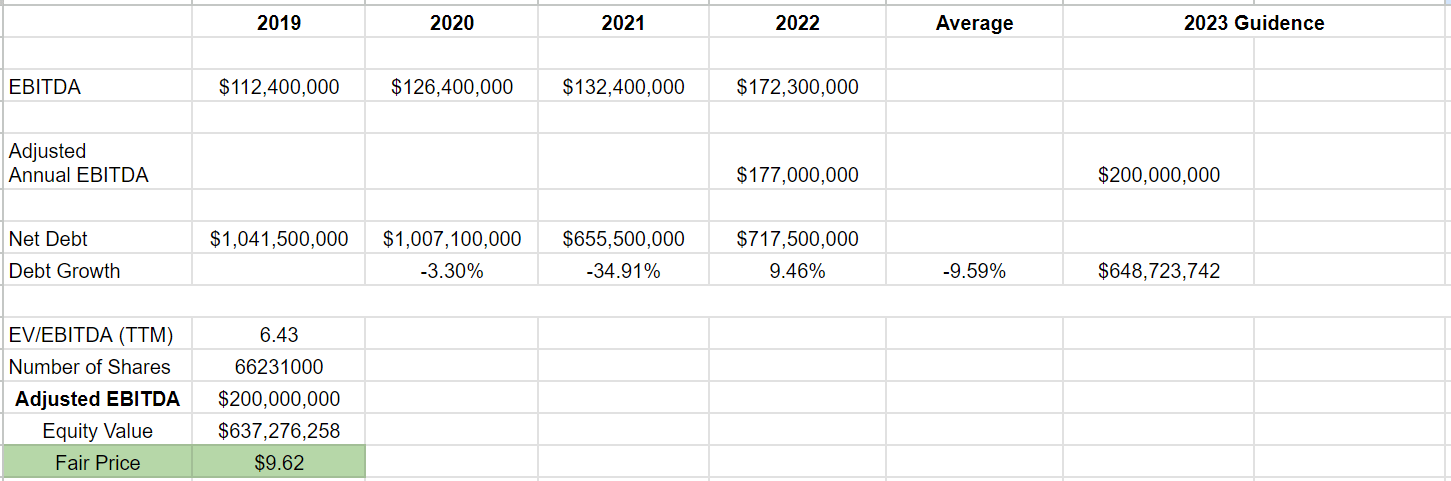

After watching RYAM's well-performed cash and capital structure, I evaluated its stock price by considering the company's ability to generate adjusted EBITDA and pay back net debt. Thus, based on the predicted adjusted EBITDA for 2023 and net debt amount during recent years, I evaluated the stock's fair price. The company's adjusted EBITDA guidance for 2023 is $200-215 million. Thus, according to such inputs, I evaluate the stock price has the potential to increase and reach $9 per share by the end of 2023 (see Table 1).

Table 1 - RYAM stock valuation

{kind=link}

Risks

The next significant debt maturity for RYAM is in June 2024. The company may need to use a part of its cash balance to repay its debt in 2024 or may need to refinance its debt. In 2022, RYAM's free cash flow was negative, and despite expectations for improving free cash flow in 2023, in case of lower demand for high purity cellulose and paperboard can decrease the company's ability to meet its obligations while staying in a healthy position. The inflation rate in major economies is still high and the monetary authorities are still stuck with high-interest rates to combat inflation. Also, the recent collapse of two U.S. banks sparked the fear of a financial crisis. An economic slowdown can hurt the demand for consumer products, and RYAM may not be able to improve its free cash flow as it expects. However, for now, the market outlook is in favor of the company's expectations.

Summary

RYAM has decreased its net debt-equity ratio during recent years, except in 2022 when it increased from 0.8x in 2021 to 0.87x in 2022. The company's capital expenditures have risen by 48% to $138 million in 2022 from $93 million in 2021 and are expected to reach $140-145 million during 2023. The long-term market outlook for RYAM's products is strong and due to its developments in specialization, I believe the company can benefit incrementally from the higher prices for cellulose specialties products in the upcoming years. The stock is a buy.

For further details see:

Rayonier Advanced Materials: Improving EBITDA, Free Cash Flow, And Debt Ratios