RBC - RBC Bearings: Performance Continues But Shares Aren't Cheap Enough

2023-03-06 20:00:11 ET

Summary

- RBC Bearings continues to show strong growth, both because of its major acquisition and due to organic strength.

- Long term, the company should fare well for its investors, but RBC stock isn't necessarily a great prospect.

- As things stand, it's a neutral play in my book because of how shares are priced.

While I do believe that value investing is the best and easiest way to generate market-beating returns, I do also acknowledge that there are some issues with the methodology. One of the biggest risks that you run into is underestimating how optimistic the market can get about a company that might look fairly valued or overpriced. This can lead to some attractive opportunities that are passed up on. And with good opportunities in short supply, that can limit your own potential to do well in the market. One company that has recently experienced quite a surge of enthusiasm from the market is RBC Bearings ( RBC ), an enterprise that produces highly engineered precision bearings, components, and essential systems that are used in the industrial, defense, and aerospace industries. Robust performance at both the top and bottom lines led to a spike in the company's share price. Previously, I took a rather neutral stance on the business, even though I saw that its health was quite solid. At the risk of repeating that mistake, however, I do believe that the stock looks more or less fairly valued at this time. So although the shares of the company have done quite well, I've decided to retain the ‘hold’ rating I assigned the stock previously.

Great results pushed shares higher

In the middle of December of last year, I found myself once again looking at RBC Bearings and deciding whether or not I felt the company had the potential to be a worthwhile investment. Prior to that point, I had rated the business a ‘sell’ since I viewed it as being overvalued. However, continued strong performance on both the top and bottom lines more than compensated for the company's operating history and led me to change my rating to a ‘hold’ to reflect my view that shares should generate upside or downside that would more or less match the broader market moving forward. Since then, however, the company has exceeded my own expectations. While the S&P 500 is up 1.3%, shares of RBC Bearings have seen upside of 12.3%.

{kind=link}

Author - SEC EDGAR Data

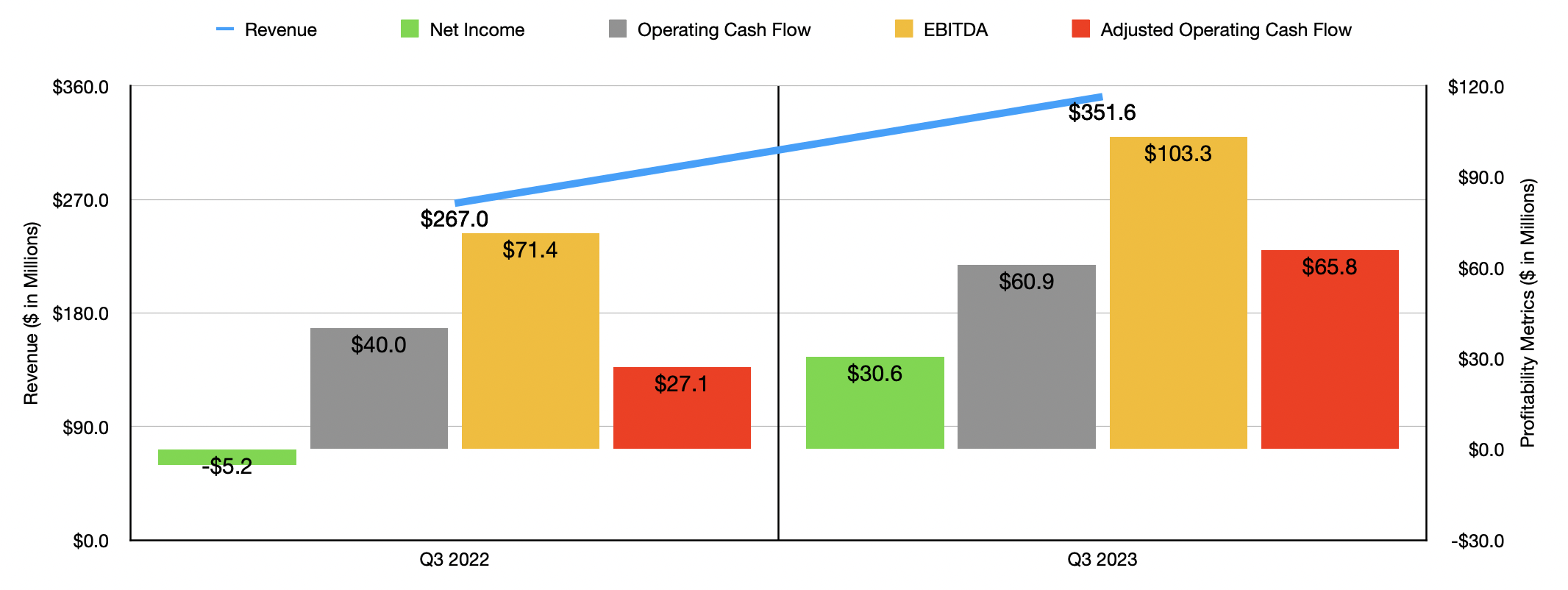

To understand why RBC Bearings has outperformed the market so much in such a short period of time, we need only look at data covering the third quarter of the company's 2023 fiscal year. According to management, revenue for that time came in at $351.6 million. That's 31.7% higher than the $267 million the company reported only one year earlier. The greatest increase for the company came from its acquisition of Dodge back in 2021. But even without that factored in, organic revenue spiked 12.7%. Excluding the Dodge acquisition, revenue associated with the company’s Industrial segment grew 12.3% year over year. This increase was driven by strong results in areas including the company's semiconductor, mining, energy, and general industrial markets. Under the Aerospace/Defense segment, revenue grew 11.6% year over year. This was driven by a 25.3% surge in the commercial OEM market thanks to a recovery in build rates for large OEMs and stability in aftermarket sales. Defense sector sales were down 7.3%, largely because of the timing of shipments associated with the company's marine business.

The rise in revenue for the company brought with it a drastic improvement in profits. The firm went from generating a net loss of $5.2 million in the third quarter of 2022 to generating a profit of $30.6 million in the third quarter of 2023. Operating cash flow spiked from $40 million to $60.9 million. If we adjust for changes in working capital, the picture would have been even better, with the metric shooting up from $27.1 million to $65.8 million. Meanwhile, EBITDA for the company expanded from $71.4 million to $103.3 million. Although the increase in revenue for the company certainly helped, there's no denying that the firm also benefited from a drastic improvement in its gross profit margin. During the quarter, this came in at 41.5% compared to the 35% it totaled one year earlier. Increased sales volumes and efficiencies achieved by the company that helped to reduce costs were instrumental in pushing margins up. The firm also benefited to the tune of $7 million in its gross profit from inventory purchase accounting adjustments associated with the aforementioned Dodge acquisition. Stripping this adjustment out of the picture would still have resulted in a gross profit margin in the final quarter of 39.5%.

{kind=link}

Author - SEC EDGAR Data

The third quarter for the company was not a one-time event. For the first nine months of the 2023 fiscal year as a whole, revenue for the company came in at $1.07 billion. That's 84% higher than the $584.1 million reported one year earlier. Without the aforementioned acquisition, sales were still up 11.9% year over year. Net income for the firm during this time spiked from $17 million to $100.3 million. Operating cash flow grew more modestly from $133.4 million to $149.3 million. But if we adjust for changes in working capital, it would have nearly doubled from $110 million to $210.5 million. And finally, EBITDA for their business shot up from $162 million to $312.8 million.

For the final quarter of 2023, management has provided some guidance . They expect revenue of between $375 million and $385 million. That stacks up nicely against the $358.9 million reported for the final quarter of 2022. Although this year-over-year growth rate looks slower than what we have seen for most of the fiscal year, that's because of the timing of the Dodge acquisition. In essence, pretty much all of this growth should be attributable to organic expansion. For those worried about the future of the business, it is worth noting the backlog still remains high. Although it did drop from $653.2 million in the second quarter of last year to $613.6 million in the third quarter, that is still comfortably above the $552.7 million reported for the third quarter of the 2022 fiscal year.

{kind=link}

Author - SEC EDGAR Data

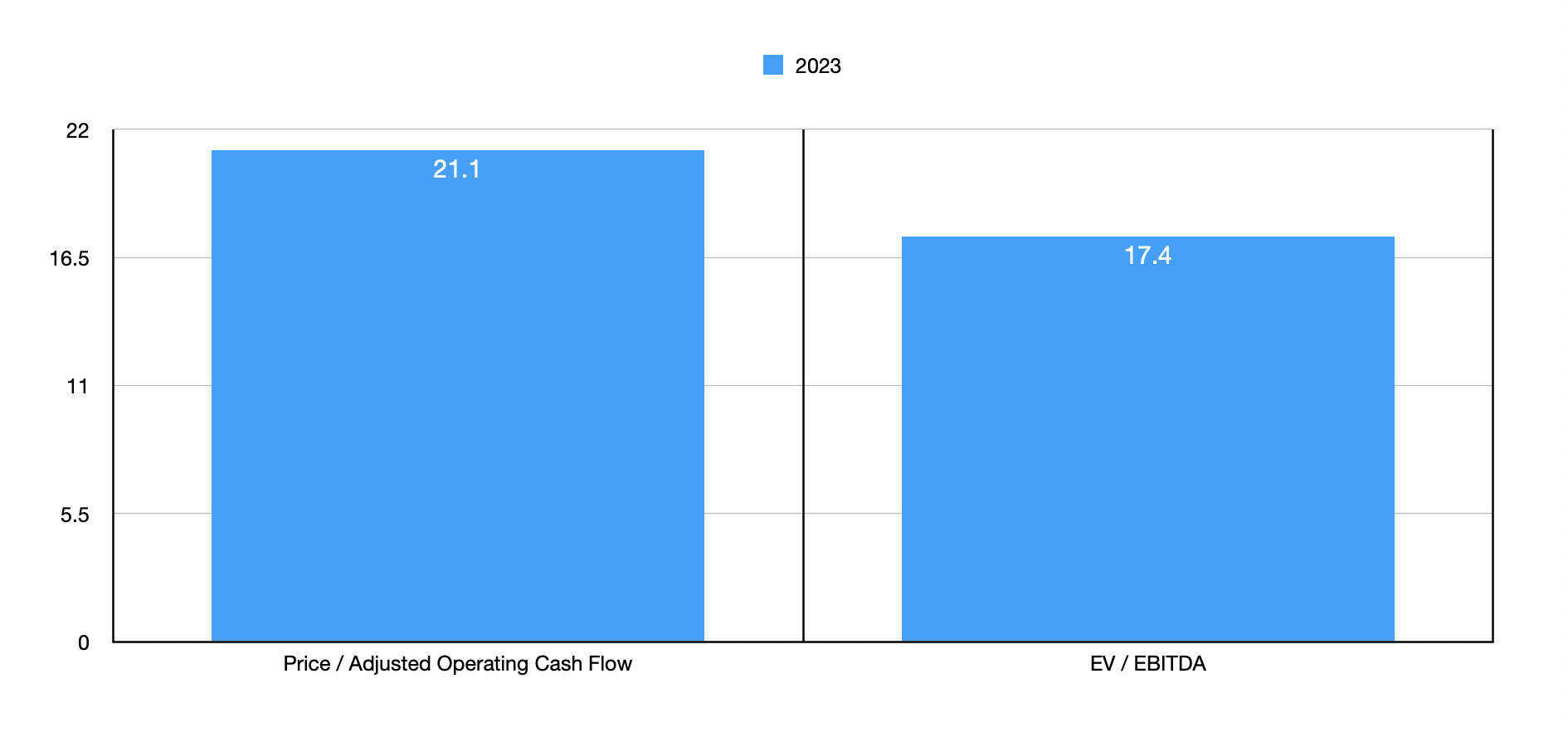

Management did not provide any guidance when it comes to bottom line results. But if we annualize results experienced so far, we should anticipate adjusted operating cash flow of $336.6 million and EBITDA of $514.6 million. Based on these figures, the company is trading at a price to adjusted operating cash flow multiple of 21.1 and at an EV to EBITDA multiple of 17.4. Normally, I would have looked at valuation metrics for other years. But because of how significant the acquisition of Dodge has been, I don't believe that those years are useful any longer when determining the value of the business. As part of my analysis, I did compare the company to five similar enterprises. On a price to operating cash flow basis, these companies ranged from a low of 15 to a high of 74.0. One of the five firms is cheaper than our prospect, while another is tied with it. Meanwhile, using the EV to EBITDA approach, we get a range of between 10.5 and 37. In this case, four of the five companies are cheaper than RBC Bearings.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| RBC Bearings |

| 21.1 |

| 17.4 |

| Pentair ( PNR ) |

| 25.7 |

| 16.0 |

| Donaldson Company ( DCI ) |

| 21.1 |

| 14.9 |

| Chart Industries ( GTLS ) |

| 74.0 |

| 37.0 |

| ITT Inc. ( ITT ) |

| 28.3 |

| 13.6 |

| Crane Holdings ( CR ) |

| 15.0 |

| 10.5 |

Takeaway

The past couple of years have truly been transformative for RBC Bearings and its investors. Clearly, the picture for the company is improving and it's likely that the long-term trajectory of the company will be positive. Growth achieved by management has been impressive and cash flows have become robust. However, shares aren't exactly the cheapest on the market. They look a bit lofty on an absolute basis and, using one of the two valuation metrics I looked at, they like to be priced near the higher end of the scale. Given these factors, combined with my decision to be a bit more cautious in general because of economic conditions, I would say that the firm makes for a better ‘hold’ candidate at this time than it does a ‘buy’.

For further details see:

RBC Bearings: Performance Continues, But Shares Aren't Cheap Enough