RICK - RCI Hospitality: FY 2024 To Be A Pivotal Year

2023-12-26 13:42:28 ET

Summary

- RCI Hospitality reported a decline in same-store sales in nightclubs and Bombshell, but sales have improved and management is exploring strategic options for Bombshells.

- Resumption in growth is very likely in FY24 with further M&A and new developments.

- Current valuation is attractive at 12x PE considering its downside risks.

Overview

Since my last coverage back in Sep 2023 , RCI Hospitality (RICK) reported same-store sales (“SSS”) decline in nightclubs and Bombshell. During the 4Q23 earnings call, foot traffic, especially for blue-collar clubs, continues to be sluggish as well as into 1Q24. Sales have, however, improved and have passed their low points. Management also spoke about re-evaluating Bombshells as they are exploring other strategic options to sell/grow the division given the higher returns on capital earned in nightclubs and casinos.

FY23, wrapped up, was a particularly weak year for the company, with both divisions facing declining revenue and margin from FY22’s highs – not the ideal situation for investors. The main thesis is, however, still intact with the anticipated acquisitions and the opening of new clubs, bombshells, and casinos to drive further growth in EBIT and FCF in FY24.

4Q23 Financials

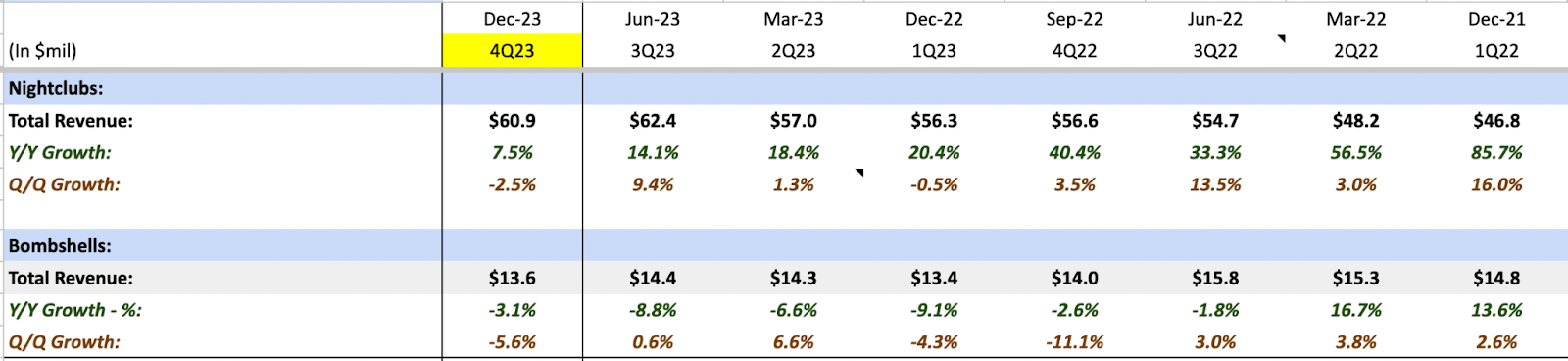

RICK revenue breakdown RICK’s 4Q23 Press Release

{kind=link}

{kind=link}

Nightclub revenue was $75.3 million, growing 7.5% YoY, but declined 2.5% QoQ from 3Q23 as inflationary pressures continue to take effect on most clubs, leading to a loss of high-margin service revenue. Similarly, Bombshell’s revenue declined 3.1% YoY and 5.6% QoQ to $13.6 million, coming off from its high in FY22.

Overall revenue was more or less in line, although it came in just slightly below my expectations. As we approached FY24, a resumption in growth will happen in both divisions as we lapsed FY23’s lows and the contribution from incoming acquisitions and the development of new clubs, bombshells, and casinos in the latter half of the year.

During the 4Q23 earnings call, it was also insightful to see the management breaking down the unit economics of slot machines, and its FCF opportunity:

“... we believe this represents a significant free cash flow opportunity… Our plan is for a total of 400 slot machines and 9 to 12 table games, as well as sports betting. Looking at the slots, they have been averaging $133 adjusted gross proceeds per day in Central City and $307 per day in nearby Black Hawk. Black Hawk is higher mainly because they run on a 24/7 basis, which we plan to do also.”

Furthermore, management is also exploring other options for Bombshells, which makes sense to me as a shareholder as I would prefer them to focus on investments that yield a higher return on capital:

“For Bombshells, I'm currently exploring with private equity groups, partial sales of the concept, partnerships or mergers…all strategic opportunities out there that we can use to maximize the value of this asset and basically accelerate our growth. I think that the concept to be highly successful. We need to get into that 80 to 100 units…'d like to see us do that with capital outside of the company's capital, because I think we just have too many acquisition opportunities coming up, the expansion of the casinos, and I'd like to keep our capital more focused on those operations rather than expanding Bombshells”

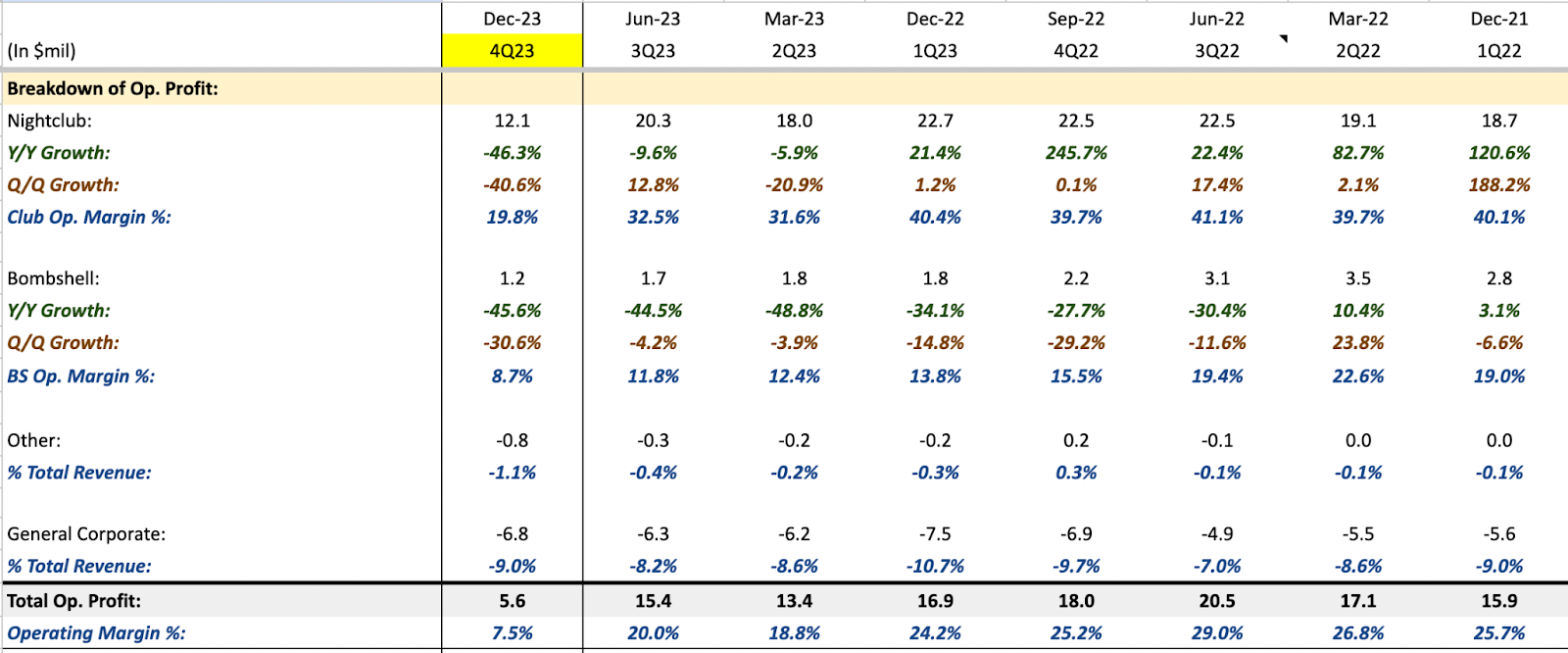

RICK Operating Profitability in the Past 8 Quarters

{kind=link}

Total operating profit was down 69% YoY and overall margins fell from 25.2% in 4Q22 and 20% in 3Q23 to 5.6% in 3Q23, largely due to the unusual $9 million of impairment of assets incurred for the nightclub division in the quarter. Respectively, club margin was down from 39.7% in 4Q22 to 19.8% this quarter, while bombshells margin was down from 15.5% in 4Q22 to 8.7% this quarter. Netting out the impairment of assets, margins will be relatively similar to 3Q23’s level.

Valuation

As of FY23, its operating profit totals $51.3 million, and with a current market cap of $621 million, RICK is valued at 12x PE in writing – which seemed rather attractive to me. Accounting for further EBIT growth in 2H24 via M&A and the development of new casinos, this makes its forward PE extremely attractive, in my opinion.

Risks

Some of the key risks, although not exhaustive, will include:

-

Continued inflationary pressure

-

Delayed rollout or building out of new locations for both divisions

-

Bombshells may take longer to turn around

-

Factors such as regulatory hurdles, and market conditions may result in slower-than-anticipated revenue contributions from casinos

Conclusions

All in all, the results aligned closely with what I had expected. With the developments for FY24 that seemed to be on track, a resurgence in growth is very likely and I believe it could be a pivotal year for the stock. At its current modest PE of 12x, and considering its downside risks, the valuation looks attractive in my view.

For further details see:

RCI Hospitality: FY 2024 To Be A Pivotal Year