RICK - RCI Hospitality: Here's Why I Keep Buying As The Stock Falls

2023-11-13 10:00:00 ET

Summary

- RCI almost halved in value year to date, but I remain a buyer.

- I discuss what I believe to be the main issues: Debt and operational weakness.

- RCI is trading at an attractive valuation, given their wide moat business and ability to do accretive acquisitions.

RCI Hospitality ( RICK ), the only publicly listed US operator and acquirer of choice for night clubs, has been a high conviction holding in my portfolio for a while. Yet the stock has performed terribly over the last year, and shares have fallen by 35% and 20% since my previous coverage. Let's review if something changed and why I keep buying the stock as it falls.

{kind=link}

Why does the stock keep falling?

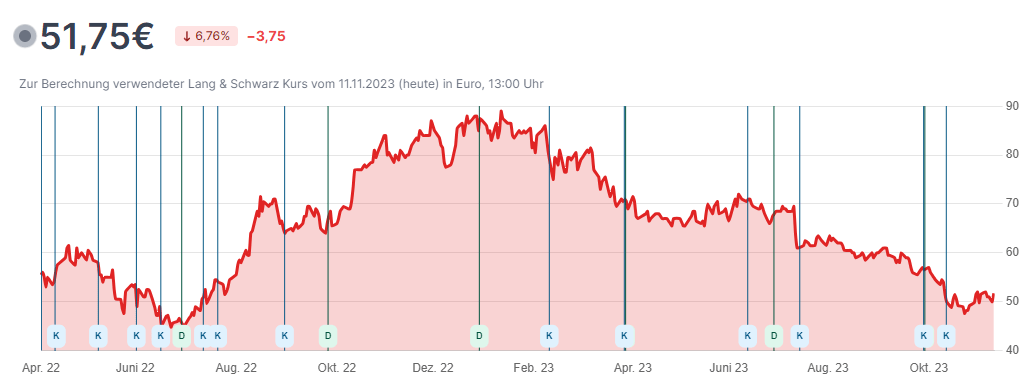

RICK peaked a little under $100 a share at the start of this year and has now almost halved in value. I started to build my position before the run-up and have continued to add to my position as the stock fell (in the screenshot below, K( Kauf ) means purchase and D represents a dividend payment). I'm currently down around 10% and look forward to averaging down more if we stay here.

{kind=link}

I believe that there are two main issues the market has with RICK right now:

Weak Operational performance

RICK has had a tough operational performance throughout the year, with Same-store sales (SSS) declining for the last few quarters. Q3 saw nightclub SSS fall by 7.3% and Bombshell SSS by 18.2%, while Q4 saw nightclub SSS fall by 9.6% and Bombshell SSS by 14.1%. While overall revenue grew due to acquisitions, the market wasn't happy with this decline.

Covid has been a tough time for RICK. Still, it also resulted in a honeymoon period as the US reopened. It led to record operating results in 2022, resulting in record margins above the long-term target of 30% for AEBITDA and 20% for FCF. As we returned to normality, these margins are reverting back a little. At 29% and 19%, respectively, margins are currently within the target but facing tough comps from 35% and 25% margin quarter a year ago.

Bombshells, in particular, had a great time as the US reopened. Restaurants were allowed to reopen sooner than bars and the state tried to keep Bombshells closed because they had full bar service. They also had a full-service restaurant, so the company sued and won the case. This meant they were the only bars allowed to open, which elevated alcohol sales from 50% to 85% liquor sales. This dramatically pushed operating margins as high as 28% for Bombshells. Operating margins had to decline as the competition reopened and regained these customers. Next quarter will likely see another SSS decline, but then we'll face easy comps again at the normal margins RICK expects its operations to have. So, really, the issue right now is that FY 22 was too good and operations reverted to the mean. From here on, RICK can continue growing and deploy its capital allocation strategy to drive 10-15% FCF/share growth; I explained this strategy in more detail in this article . Looking forward to FY 24 and beyond, it will be interesting to see how the Casino experiment is going. While it is a rather small investment, I don't want it to be a large distraction if it turns out as a failure. Investors should watch this risk going forward.

RICK margin performance (RICK Q3 Presentation)

Debt worries

As interest rates kept climbing, investors worried about levered companies like RICK. Usually, when RICK buys a club, they also purchase the underlying property, so they carry a lot of debt. I do not see this as a large issue because 85% of the debt is secured by real estate or seller financing. Furthermore, interest rates declined slightly over the last five years, as RICK gets better terms on its debt as the company grows and gets more stable. However, investors should watch the trend of rising total occupancy costs, which rose from 5.7% in Q1 21 to 8% this quarter. The maturity schedules aren't too bad right now, especially after the company pushed back the $15.7 million maturities from October 24 to October 2026 ($9.1 million) and November 2027($6.6 million) with the same interest rate of 12% unsecured. This was to free up cash to repurchase more shares at these levels. CEO Eric Langan stated that he is comfortable operating as long as they have $18 million cash on hand. Still, depending on the situation, he could go down as low as $14 million temporarily. Currently, cash is at $23.5 million, with FCF generation of over a million each week.

{kind=link}

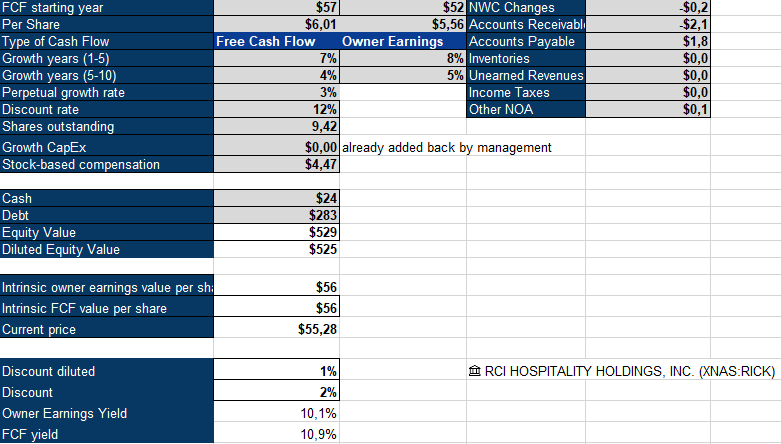

I'm buying more shares

To value RICK, I'm using an inverse DCF model. Management publishes Free Cash flow as Operating cash flow - Maintenance CapEx, so there is no need to subtract growth CapEx. Maintenance CapEx represents a small portion of the overall CapEx at around $6 out of $36 million. 2023 has been a year of investment for RICK, with a lot of CapEx flowing into club remodeling from acquired clubs and their Casinos. Adding these back makes sense and we will see the impact of those locations in the future. I use a 12% discount rate instead of my usual 10% to account for added risk from the slightly cyclical nature of RICKs business.

{kind=link}

We can see that the company is required to grow cash flows by 8% for the next five years, followed by a 5% growth rate. RICK aims to grow Free Cash Flow per share at 10-15% a year and I believe this is a realistic assumption. Acquisitions are highly accretive at 3-5 times EBITDA plus improved operations after that, which often drop the multiple to 2-3 times. RICK has shown that it can roll up this fragmented industry as the largest player with a good reputation in the industry and bank financing. The market is worried about debt, but given the superior returns from growth investments, I do not mind it. Operational weakness is more of a result of tough comps instead of declining business quality. I remain confident in the company and will continue building my position if the stock stays in this range.

For further details see:

RCI Hospitality: Here's Why I Keep Buying As The Stock Falls