RICK - RCI Hospitality Should Perform Well In 2023

Summary

- RCI Hospitality is set for strong revenue growth this year with free cash flow likely set for another record year.

- The valuation could move higher as continued share buybacks get aggregated with its highly cash-generative operational gearing.

- With the relatively uncontested roll-up of more adult nightclubs on the horizon, RCI forms a unique investment in an overlooked part of the economy.

I've started a position in RCI Hospitality ( RICK ) and now consider the company a top pick for 2023. There's a lot to like here as RCI's management continues to execute an extremely shareholder-friendly capital allocation strategy against an aggressive build-out of their portfolio of adult nightclubs and Bombshells, a military-themed chain of restaurants and bars. RCI plans to publish its 10-Q for its fiscal 2023 first quarter ending December 31, 2022, on Thursday 9th February but has already released sales figures for the quarter.

{kind=link}

Revenue from RCI's portfolio of adult night clubs came in at $55.9 million , an increase of 20.7% over the year-ago quarter. Whilst driven by the acquisitions of new clubs, same-store sales were still up 1.2% over their year-ago comp. This offset weakness from Bombshells which saw total sales drop by 9.7% from their year-ago comp. Overall, aggregate sales for the quarter at $69.2 million was up by 13.3% from the year-ago period. So why am I bullish?

Continued Acquisition Momentum Sets The Backdrop For 2023 Outperformance

RCI acquired around 15 nightclubs in fiscal 2022 and has maintained this buyout momentum with the purchase of five more adult nightclubs during the first quarter of its fiscal 2023. The company purchased three Chicas Locas and two Baby Dolls adults nightclubs in the Dallas-Fort Worth and Houston markets for $66.5 million and expects these clubs to drive $11 million in EBITDA in their first 12 months, eventually growing to around $14 million to $16 million after. This would represent a return of around 22.5% at the midpoint of this range. RCI financed the deal with around $25 million in cash, a 10-year 7% $25.5 million seller financing note, and 200,000 restricted shares.

Bears would of course point to a dilution of around 2.17% expected against average diluted shares outstanding of around 9.2 million as of the end of the RCI's fiscal 2022 fourth quarter. Indeed, whilst this would at a very high level seemingly go against the company's buyback strategy, the annual interest expense of the 7% seller financing note sits at around $1.75 million. Hence, the bulk of these earnings should feed through to free cash flows and allow the company to buy back more shares in the future.

Using the first quarter's revenue as a baseline and adjusting it for the feed-through of recent acquisitions I'd expected RCI's full fiscal year 2023 revenue to come in at around $300 million to $350 million, around 21% higher than its fiscal 2022 revenue at the midpoint of this range. To be clear here, this is entirely forecasted and actual revenue could be lower. Eric Langan during the first quarter sales update stated there has been some intermittent softness at some clubs.

Potential 2023 End Value On Forecasted Financials

With RCI currently trading at a market cap of $860 million against forecasted fiscal 2023 revenue of $325 million, its price-to-forward sales multiple at 2.65x is lower than the current retrospective multiple of 3.28x. Whilst this has been volatile, we could see the market cap move up just north of $1 billion, or around $108 per share for a 16% capital uplift if the retrospective PS multiple as of the end of RCI's fiscal 2023 reflects its current figure.

Bears would of course highlight the scope for the valuation to experience compression this year especially if the economy turns sour. RCI has been riding an upturn in investor enthusiasm since the summer of 2022 and this could turn back south on the back of broader macroeconomic conditions. That said, RCI has built its operations on an exceptionally cash-generative business and the company's return on its investments continues to come in at impressive levels.

{kind=link}

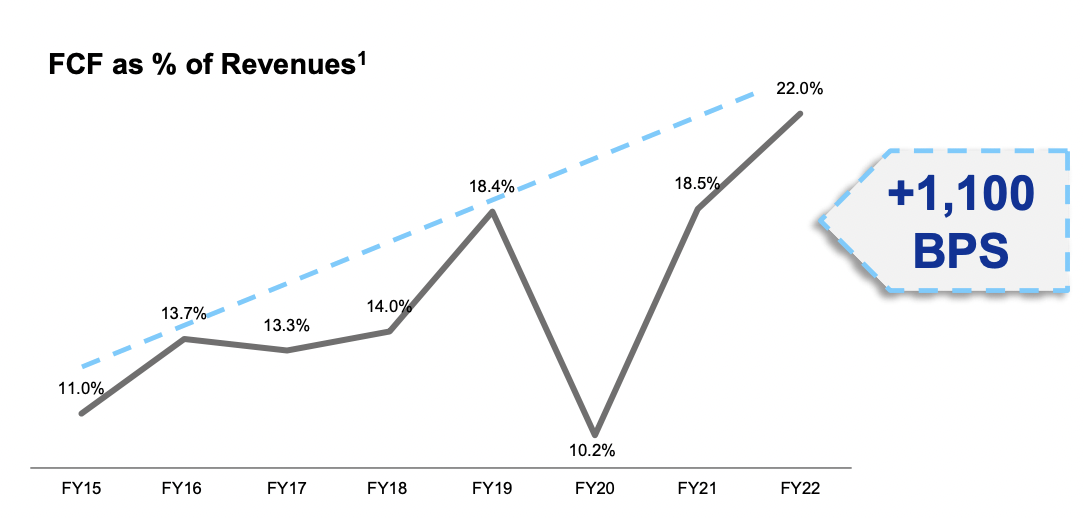

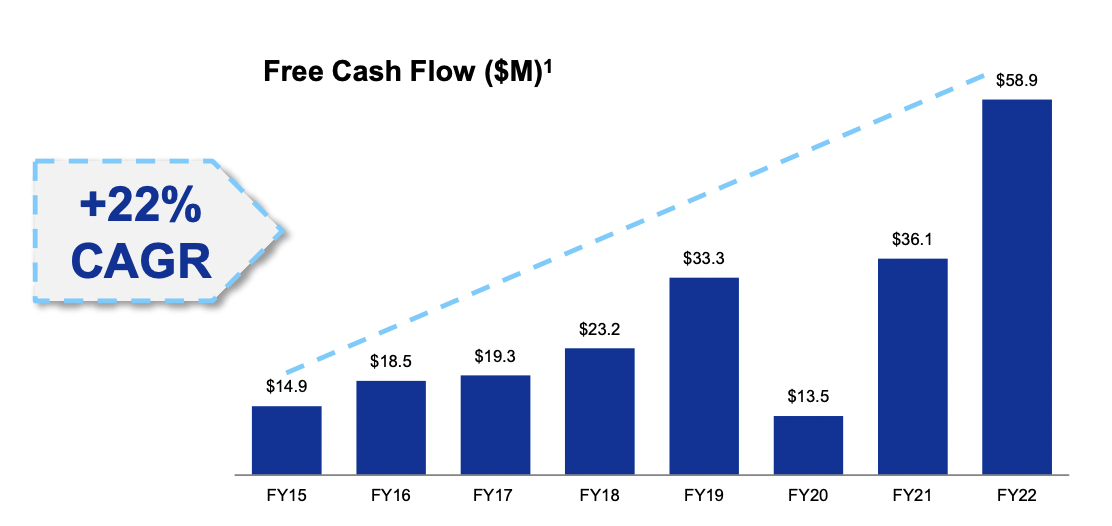

Further, with RCI's free cash flow as a per cent of revenue currently at 22%, the company could see free cash flow for 2022 come in at $71 million, up from $58.9 million in the year-ago comp. This places into view why RCI forms one of my top picks for 2023.

{kind=link}

The company is printing cash and using that to drive an ambitious program of share buybacks, which form the other method of returning cash to shareholders outside of dividends. My portfolio is heavy on dividend-paying stocks, these critically form pillars of wealth creation and I think RCI fits into this bracket. Constant share buybacks are in themselves a method of returning value to shareholders and help create the conditions for concentration, the inverse of dilution, where your ownership of the company rises each period. Hence, I see RCI as complementary to my long-term dividend-paying positions. The company has moved to define itself by the hyper-aggressive and constant buyback of its common shares which serves to increase the concentration of my holdings.

For further details see:

RCI Hospitality Should Perform Well In 2023