RCMT - RCM Technologies: A Hidden Gem With Massive Upside Potential

2023-08-31 12:40:55 ET

Summary

- RCM Technologies has seen massively improved financial metrics and is considered a strong buy due to its promising future in the specialty healthcare segment.

- The company's revenues primarily come from healthcare services, which have increased in importance due to the pandemic and increased caution regarding future events.

- RCM Technologies has experienced significant growth in the number of schools bringing in over $300,000 in annual revenue and management predicts that this market will continue to expand.

- The company also has a massive market opportunity within the aerospace procurement spending of the US.

Investment Thesis

RCM Technologies (RCMT) popped up on my radar because of massively improved financial metrics that I deem the most important in an investment, so I wanted to take a look into the company further and see where it is going to go in the future. The company is not very well covered and according to my calculations, it is a very strong buy because of a very promising future in the specialty healthcare segment, which was helped by the emergence and subsequent decline of the pandemic, which made everyone much more cautious about such future events, leading to heavier investments in healthcare services in schools throughout the United States.

Briefly on the Company

RCMT provides technology and business solutions that are designed to enhance operational performance through the deployment of advanced IT services and engineering. The company also offers staffing services in healthcare, engineering, IT, and life sciences. The company operates through three revenue segments: Specialty Healthcare, Engineering, Life Sciences, and IT services, with more than half of revenues deriving from the Specialty healthcare segment.

Outlook

School Healthcare

A lot of the company's revenues come from the school healthcare services in the Specialty Healthcare segment. About 66% of the segment's revenue came from school-related healthcare services ( as per transcript ). The pandemic has changed how schools and other institutions approach healthcare and are much more cautious about what's going to happen next and how to prevent such events from making a huge impact like COVID-19 had on the world. This is where RCMT comes in with its expertise in identifying where an institution, like a school, lacks in terms of healthcare, whether that is the need for more behavioral health providers, therapists, or nurses. The opportunity in this segment is enormous and it has opened even more after the pandemic in ways that no one expected.

The company is doing a very good job at growing the amount of schools that bring in over $300,000 in annual revenue. According to the transcript above, in 2019, the company had less than 30 schools and only 3 bringing in over $300k a year. By the end of FY22 in December it had over 60 schools and over 15 brought in over 300k a year each. The management is also predicting that this market will 10x within 3 to 4 years and that is a very bold statement, however, I believe they're right.

Engineering

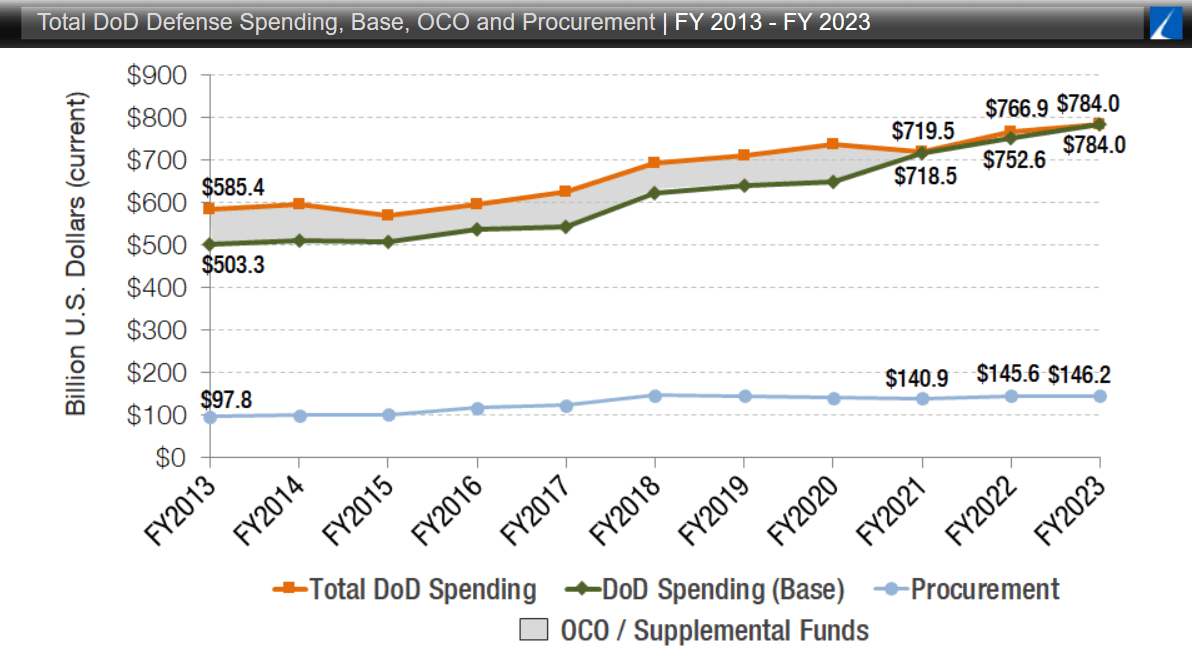

Another promising avenue of revenue is within the Engineering segment, which is Aerospace services. The company has a lot of relationships with the largest prime contractors in the US and there is a lot of opportunity for engineering services used within the aerospace division in terms of procurement and production. Total DoD spending has increased slightly over the years, however, if we look at procurement spending, it has stayed flat. Nonetheless, that is still a $146B opportunity for RCMT. The company will be able to capture some of the total spending of the DoD, not just the procurement part if it continues to gain key partnerships in the US. The company's 10K report says that the government is going to spend over $1T on procurement-related aviation expenditure over the next 3 decades, which is a lot more conservative than what the graph shows below.

{kind=link}

I believe these two segments will be the key revenue drivers going forward for the company and given it will be able to capture a decent market share in both of these if the company doesn't drop the ball right now.

Risks

The competition could soon become even more prominent seeing how the company has improved over the last couple of years and will want to take a slice of that pie. This will in turn reduce RCMT's revenues and ROI because there will be many more players in the business.

There is a chance that institutions will drop the ball on making further healthcare adjustments because of the belief that the next pandemic isn't very close since we already had one recently and start to neglect the sector once again and the company will lose a good chunk of its revenues. The sector is also affected by the seasonality of the school year, especially in Q2 to Q3 when schools close and reopen in September. Expect a lot of fluctuations in these quarters.

The company is not very well known and daily trading volume therefore is very low. Expect large fluctuations in price and because the company is so little known, may never reach the potential it has.

Financials

What I wanted to focus on in this article was how the financial position of the company has improved since FY20. Just to note, all the graphs below will be as of FY22 because I like to look at the full picture and how the company develops over the long term rather than through fluctuating quarters because of the seasonality of schools. I will include some of the latest figures for extra color if I deem them necessary.

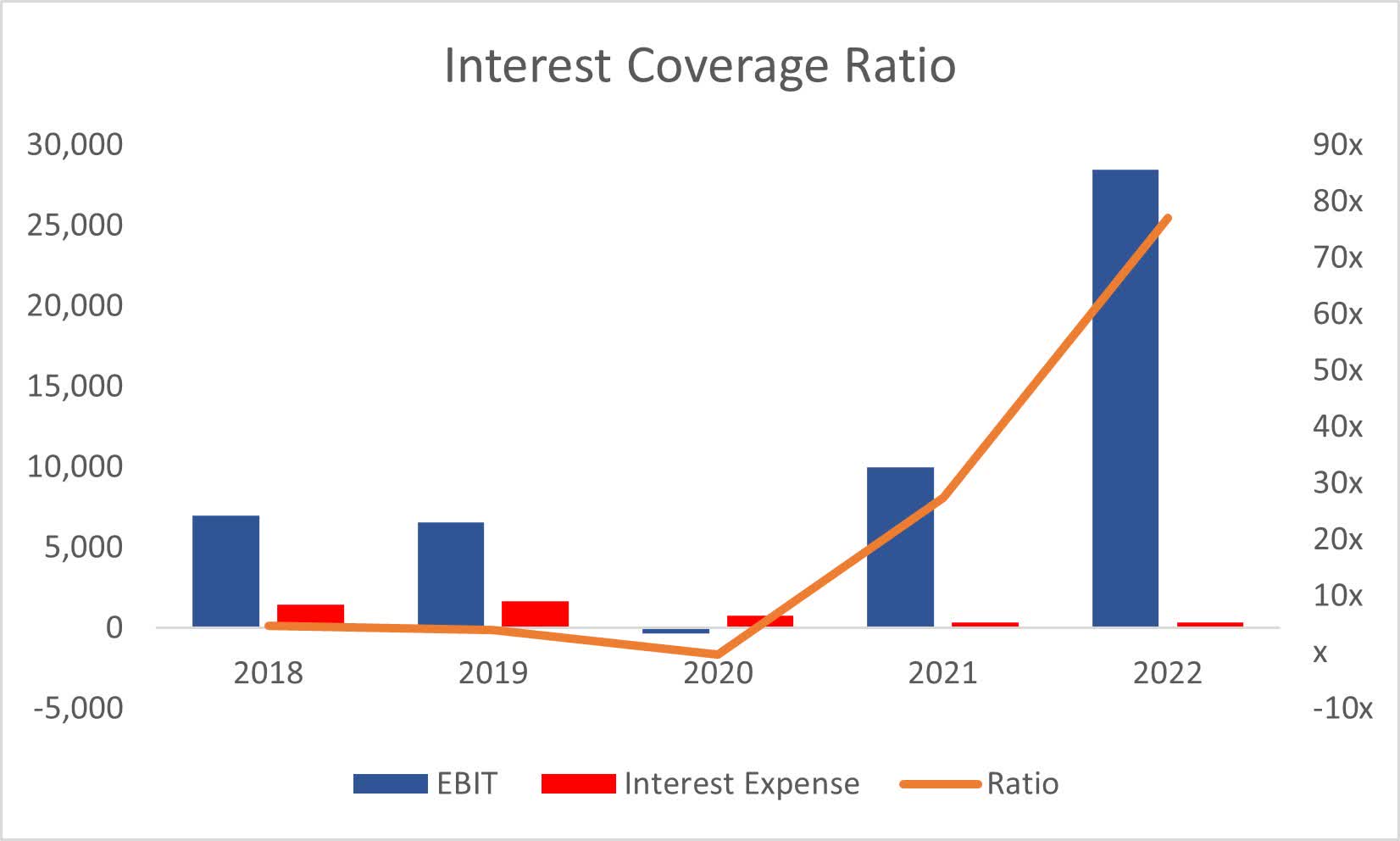

As of Q2 '23 , the company had $1.2m in cash against $14.9m in long-term borrowings under the credit facility. This doesn't look like a problem to me because the company is able to generate amazing cash from operations and EBIT, which are around $28m in FY22 while interest expense as of FY22 stood at around $370k. This means that the company's interest coverage ratio stood at a whopping 77x, meaning EBIT can cover interest expenses 77 times over. I look for companies that have a coverage ratio of at least 5x, but for reference, 2x is considered healthy. It is safe to say that RCMT has no insolvency issues.

Interest Coverage Ratio (Author)

{kind=link}

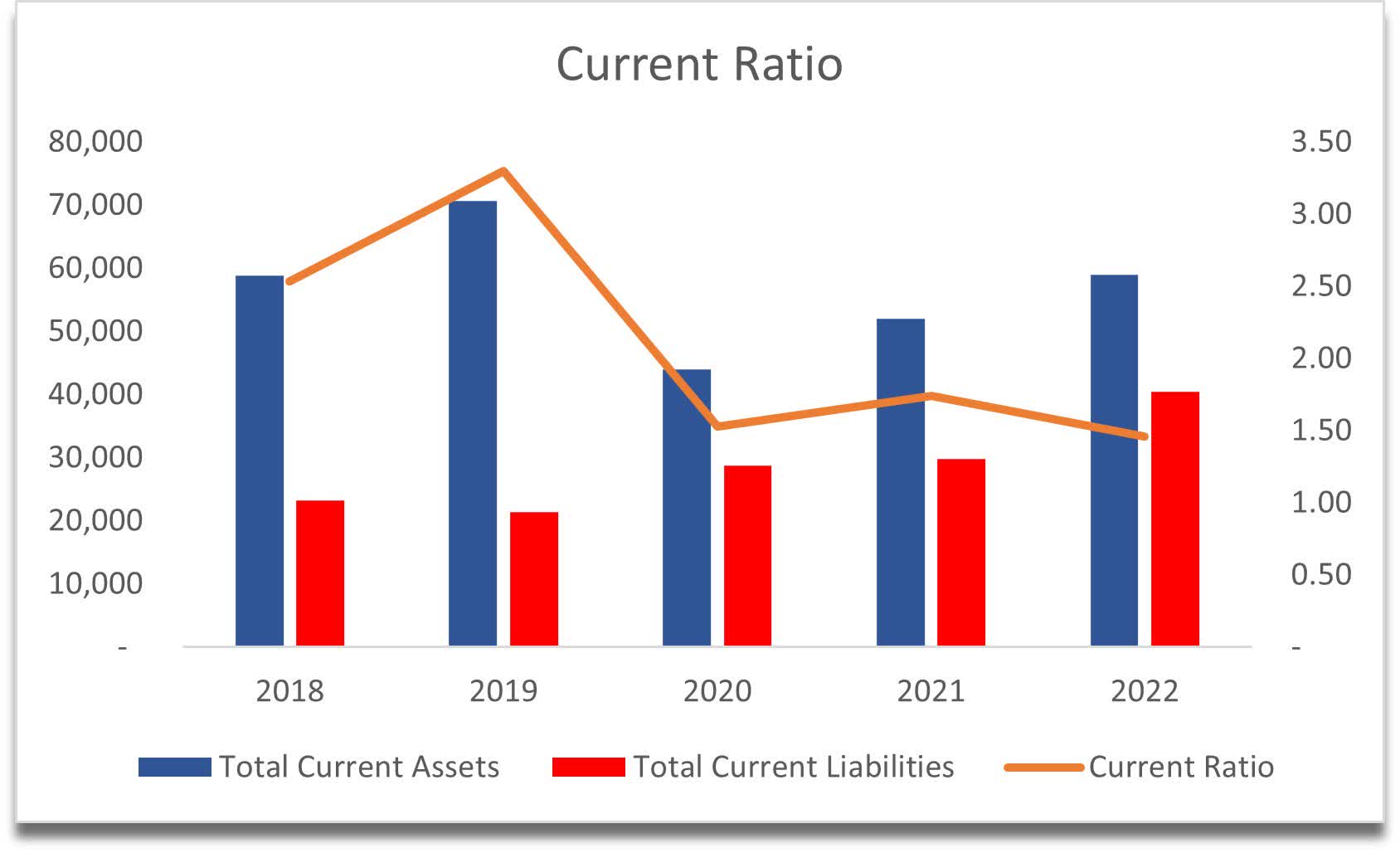

Looking at the company's current ratio, we can see that it stood at around 1.5 at the end of the year, which is right at the number that I like to see companies achieve. This tells me that the company is using its assets efficiently, i.e., not hoarding cash that can be used for further expansion and is still able to cover its short-term obligations.

{kind=link}

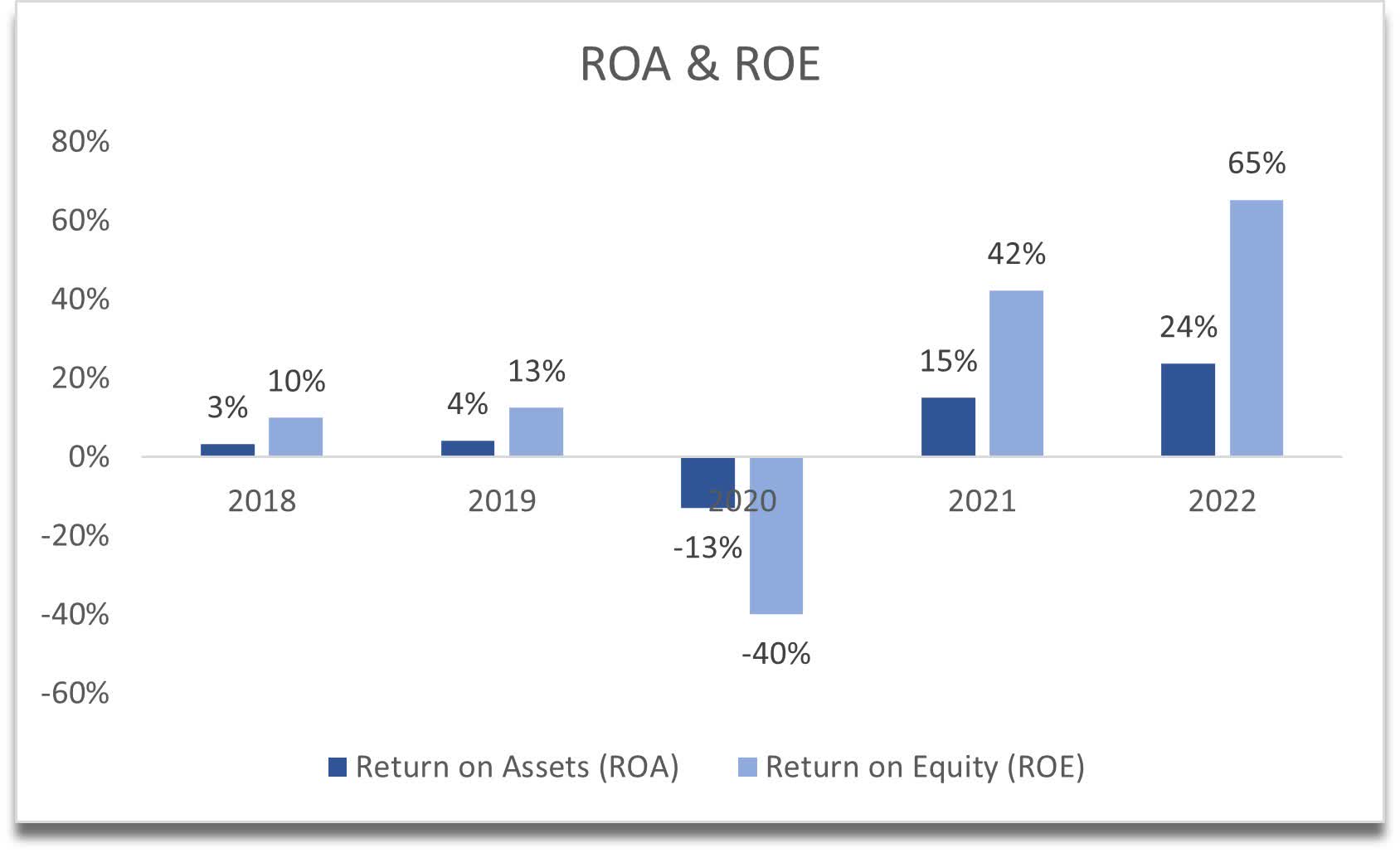

In terms of efficiency and profitability, the company's ROA and ROE have exploded in the last two years because of exactly what I said above. Institutions are taking healthcare services a lot more seriously and the demand for the company's services has exploded. These are well above my minimums of 5% for ROA and 10% for ROE. We can see how everything shifted after the pandemic.

{kind=link}

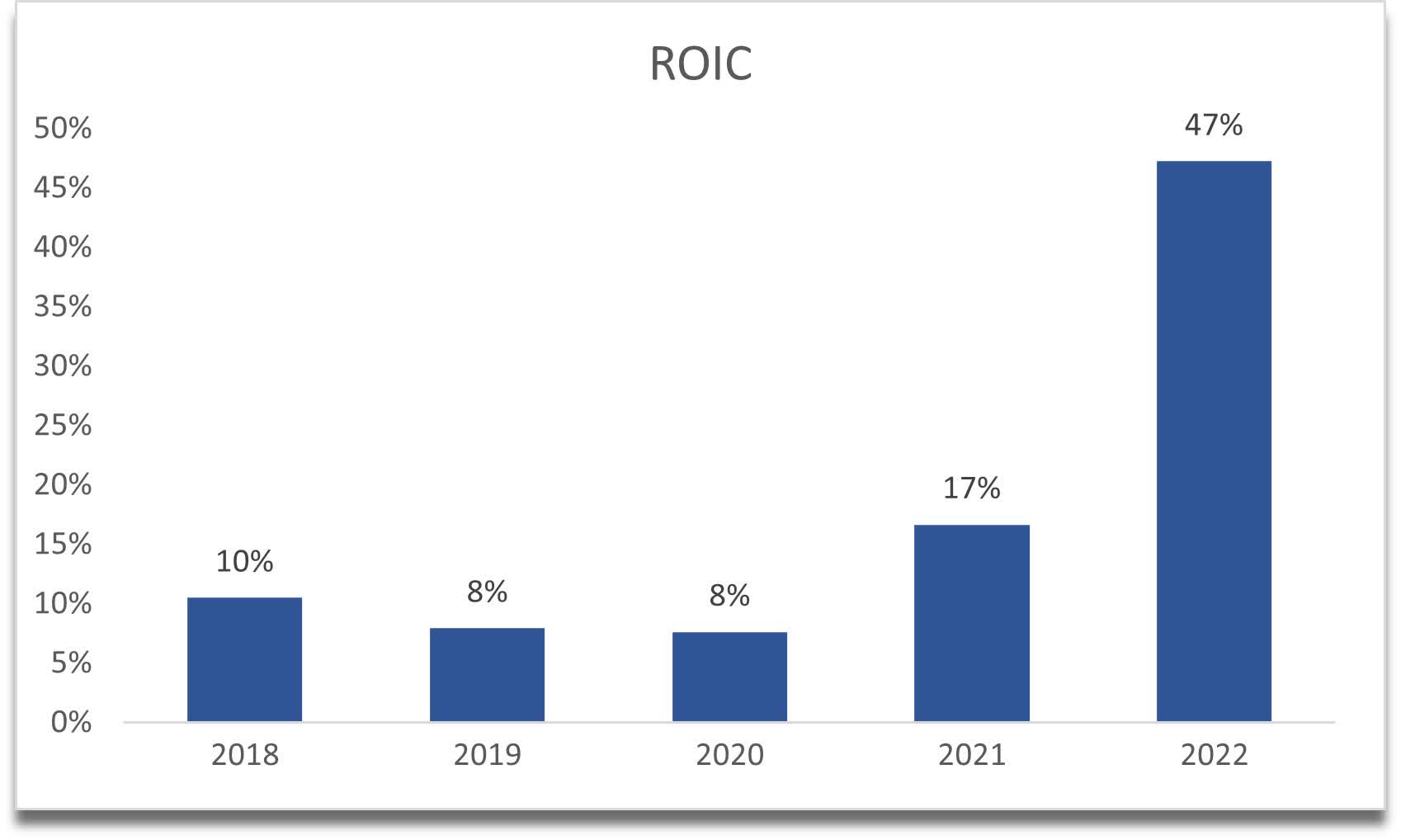

The same story can be said about the company's return on invested capital, which also exploded last year to a whopping 47%. This tells us that the company has a really strong competitive advantage and a strong moat. This metric, coupled with ROA and ROE deserve a premium on the share price because of how efficient and profitable the company became after the pandemic.

{kind=link}

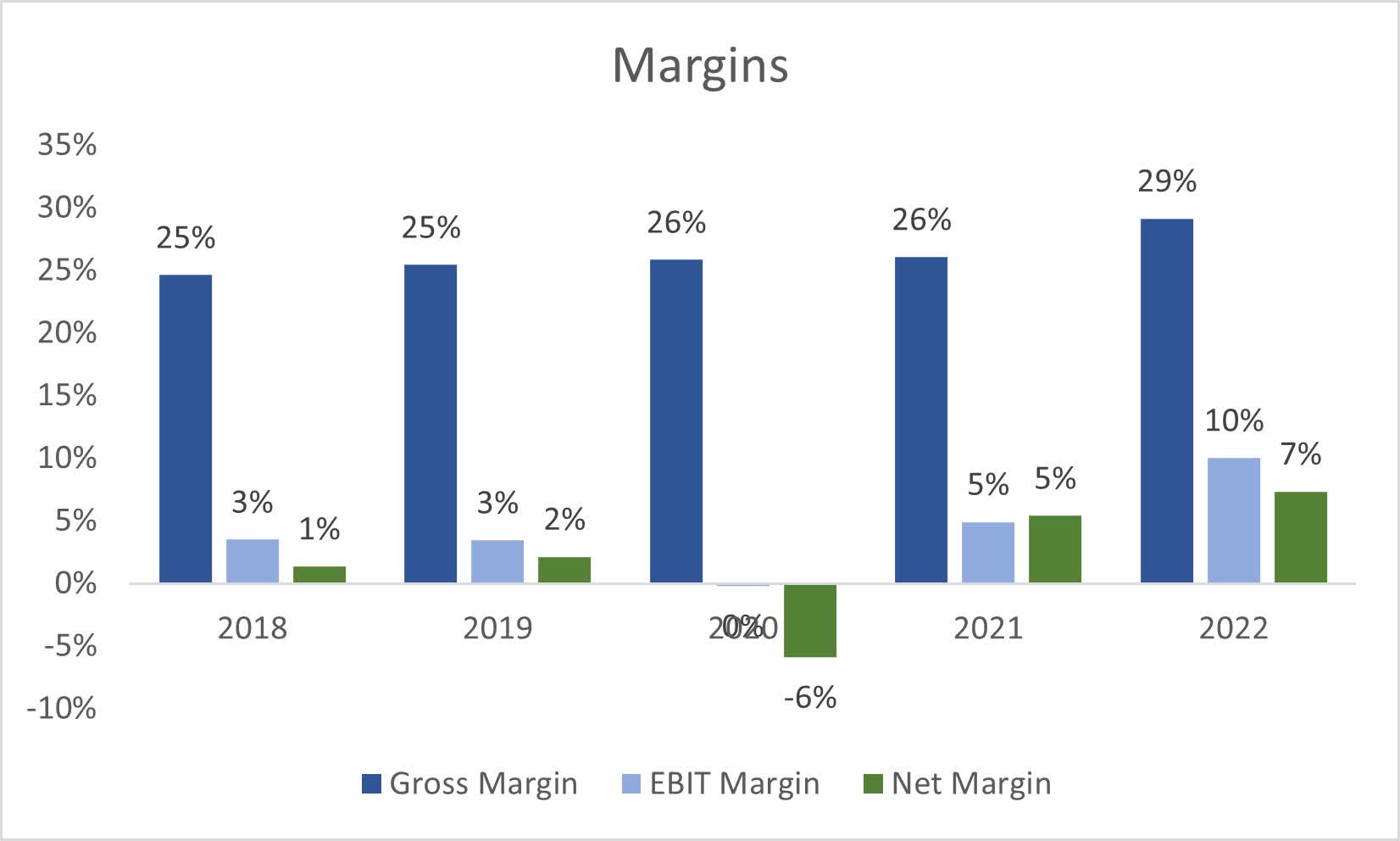

During this time, margins have also expanded quite considerably compared to the pre-pandemic levels. Only time will tell if all the above metrics and margins will stabilize around these numbers or if will we see some dips in the future. Even with some dips in ROIC, ROA, and ROE, the company will still be very profitable and efficient.

{kind=link}

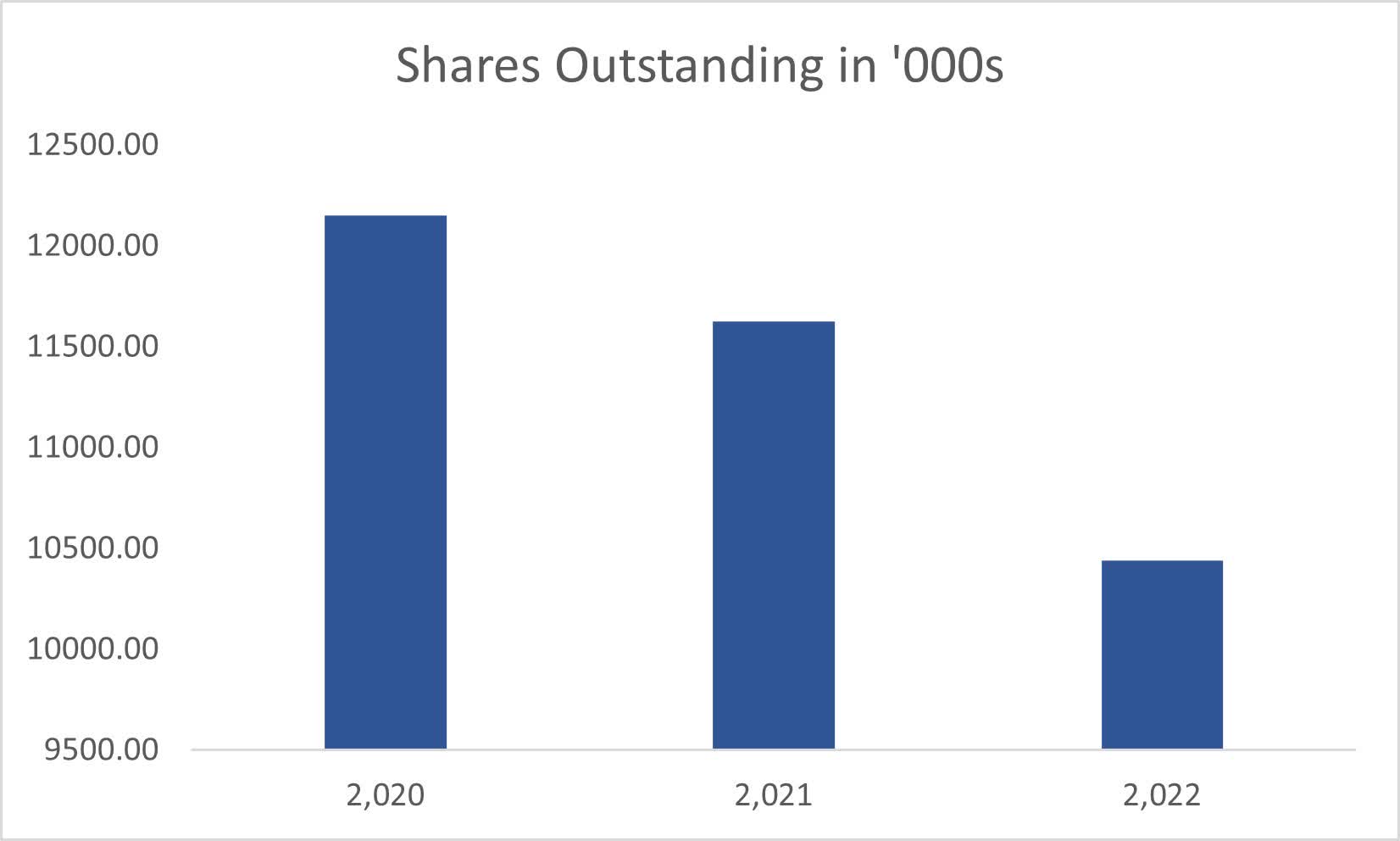

The company has also started to buy back its shares at a reasonable pace. This is good if the share price is below or at fair value, which we will see in the next section if it is.

{kind=link}

Overall, we can see that the company benefited quite a lot from the disaster of 2020. It opened new opportunities to help the health system of schools and other institutions that started to take healthcare a lot more seriously than it did up until 2019. I believe that this is just the beginning and there is a lot more growth going forward for the company. Maybe not at the same explosive pace but I don't see this reverting to the '19 numbers.

Valuation

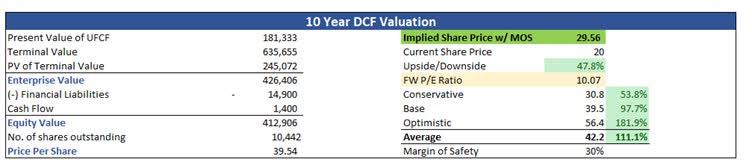

In the last 2 years, the company saw revenues grow at a pace of 36% and 40%, which are much higher than pre-pandemic levels. I could see the company continuing strong growth going forward, however, I will be more conservative, and for my base case, I will grow revenues by around 6% CAGR for the next decade. For the optimistic case, I went with a 10% CAGR, while for the conservative case, I went with a 4.2% CAGR over the next decade.

In terms of margins, I decided to improve gross margins by around 300bps from FY22 margins over the next decade, which I think is still rather conservative. I also decided to keep operating margins where they were at the end of FY22. This will bring net margins from around 7% in '22 to around 10% by FY32.

And because the company is quite small, which tends to fluctuate a lot more than more established companies, I will add a 30% margin of safety on top of these assumptions. With that said, RCMT's intrinsic value is $29.9 a share, implying a heavy discount to fair value currently.

{kind=link}

Closing Comments

I have been very conservative in the company's valuation and potential here, however, even with such assumptions, the company is heavily undervalued in my opinion, and offers a very good risk/reward right now. For that reason, I rate the company a Strong Buy.

I also believe that the company has a lot of prospects in all its revenue segments, not just the healthcare side of things, however, in my opinion, even if those other segments aren't growing much, the healthcare segment will continue to outperform.

Investors do need to be a bit more cautious because the company is still quite small and may experience a lot of fluctuations in price due to liquidity, however, if you can stomach these, then in the long run, I believe the company will reward shareholders handsomely.

It looks like the company is a hidden gem, with only 1 analyst covering the stock, and not many followers in general. I will be looking to start a small position very soon and see how it fares over time.

For further details see:

RCM Technologies: A Hidden Gem With Massive Upside Potential