RCMT - RCM Technologies: Reaching A Tipping Point

2023-11-06 16:36:57 ET

Summary

- The global HR and recruitment industry has benefited from a tight labor market, leading to increased hiring and outsourcing of recruitment processes.

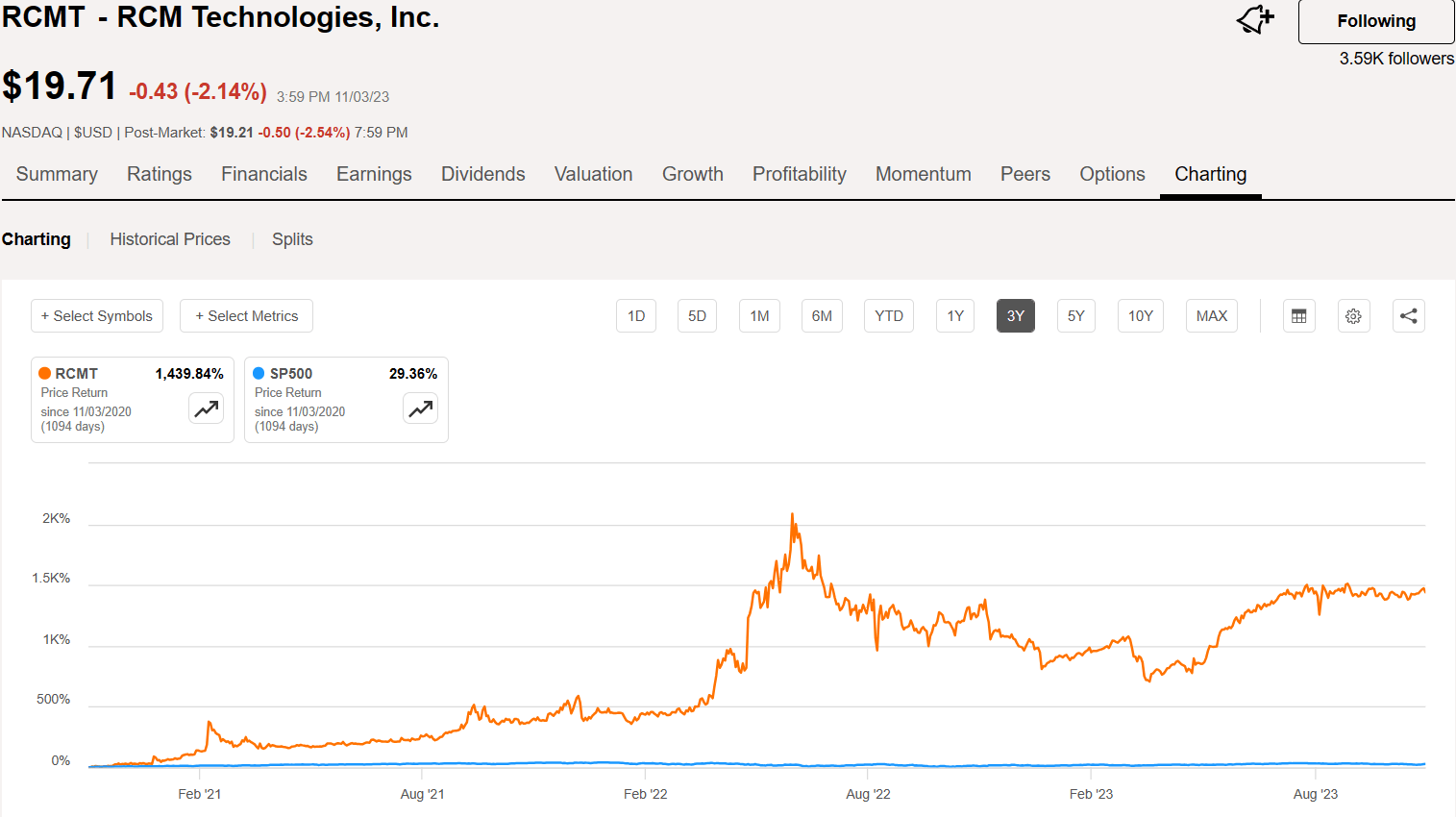

- RCM Technologies, Inc., a provider of specialty services in engineering, IT, and healthcare, has seen its stock increase by nearly 1,500% in the past 3 years.

- RCMT offers growth-oriented investors an opportunity to take advantage of underpriced shares with a strong business model, outstanding management, and long-term growth prospects.

The job market and employment trends around the globe have been shifting and adjusting over the past three years since the onslaught of the Covid pandemic, which changed how the world works. Massive layoffs during the pandemic, and uncertainty around re-hiring once businesses started to rebound led to an increase in outsourced employees and part-time or temporary job listings.

According to IBIS World , statistics and trends in the global HR and Recruitment industry indicate that a tight labor market has been good for the recruiting and placement firms in 2023 that provide services to companies as they increase hiring because they often turn to those companies first.

HR and recruitment companies rely on a businesses' desire to outsource their recruitment process and human resource management activities. Their performance depends on their major market's economies and the impact these conditions have on labor. Regulation, especially for temporary employees, can hamstring providers, as this makes it more difficult to operate. More liberal labor laws in developed nations have been essential to HR and recruitment companies' growth. Large companies are now focusing on emerging markets that will undergo the same process in the future. COVID-19 put a halt to positive momentum in recent years, as businesses seeking to cut costs were unwilling to hire and minimized their HR programs. Revenue increased at a CAGR of 0.1% to $761.6 billion through the end of 2023. This includes a 1.4% expansion in 2023 alone, as the economy continues to normalize following the pandemic and labor markets are strengthening, which will benefit HR and recruitment companies.

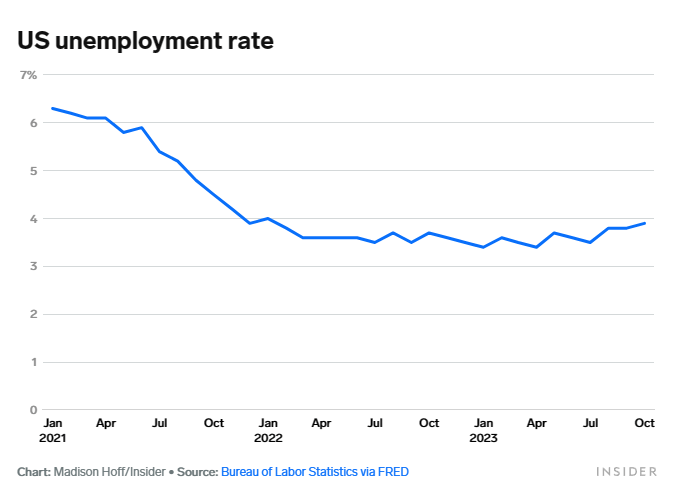

Despite soaring inflation and ongoing fears of a looming recession in the US, the labor market remains tight. Although job growth has been slowing in 2023, unemployment remains below 4% and increased only slightly in October from 3.8% to 3.9% as wage growth slowed, as discussed in this recent report from Business Insider.

{kind=link}

That is all good news for one small company that offers recruiting and contract placement services, targeted specifically at companies needing specialized employment help. That company is RCM Technologies, Inc. (RCMT), a provider of specialty services in advanced engineering, information technology, and healthcare. From the company’s website:

RCM has been an innovative leader in the design, development and delivery of these services to commercial and government sectors for over 35 years. Over the years, the company has developed and assembled an attractive, diverse and extensive portfolio of capabilities, service offerings and delivery options, established a proven record of performance and credibility, and built an efficient pricing structure. This combination offers clients a compelling value proposition with the potential to substantially accelerate the successful attainment of their business objectives.

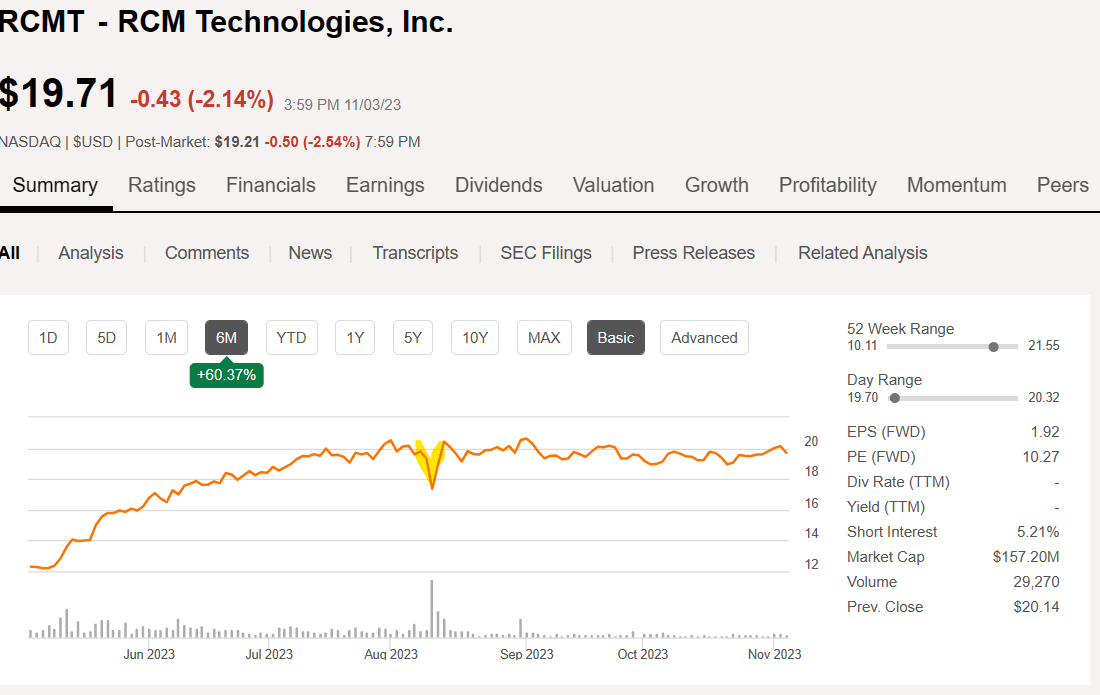

In just the past 3 years, RCMT stock has increased by nearly 1,500% and remains a Buy ahead of Q3 earnings, which are due to be reported on November 9.

{kind=link}

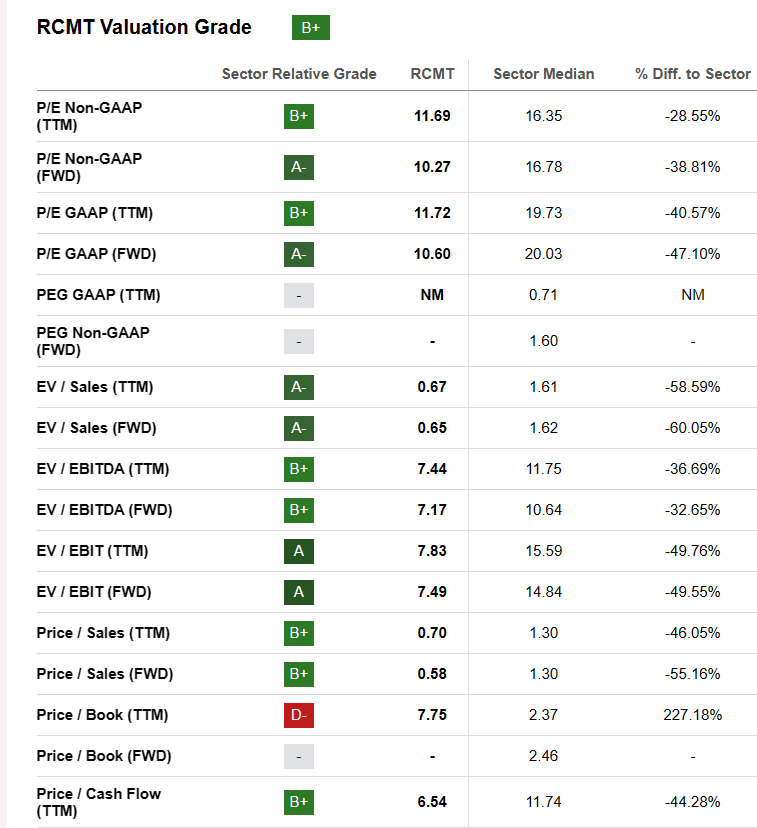

RCMT is a mostly underfollowed stock with just two Wall Street analysts, and less than 4,000 followers on Seeking Alpha. The stock offers growth-oriented investors a unique opportunity to take advantage of the underpriced shares of this small cap company that has an average price target of $25 and trades at a forward P/E of 10.27.

Ahead of the Q3 earnings call, I would like to outline some reasons for my buy rating based on the company’s high quality business model, strong leadership, and long-term growth opportunities. The end of the Covid pandemic has created a unique short-term opportunity, but the company has been spending most of the past 5 years since the appointment of Executive Chairman, Brad Vizi, getting into position to take advantage of the opportunities that lie ahead.

High Quality Business Model

The RCM Healthcare segment has been providing school nurses and other healthcare professionals including travelling nurses since 1975. Recent trends, especially post-Covid, in behavioral health and mental health challenges have provided opportunities for RCM to expand services in those areas. The Executive Chairman, Brad Vizi, explained some of those recent changes during the Q2 earnings call:

Moreover, our effort to expand our school and healthcare facility clients have not only broadened our reach, but also strengthened our ties with local communities and providers. These initiatives have bolstered client penetration and allowed us to serve more students and patients in need, making a sustainable impact. We have also invested significantly in technology to enhance the applicant user experience and optimize operational efficiency.

The RCM Life Sciences and IT division has been expanding and seizing new opportunities. According to CEO Vizi, that segment delivered only about 5% of revenues 30 months ago and expanded to 33% of revenues in Q1 and up to 43% of revenues in Q2. With more than 160 current customers and 95% repeat engagements, that division has strong growth potential going forward as well. As Executive Chairman Vizi stated on the earnings call:

On the Life Sciences and IT front, we believe that division has reached a tipping point as we continue to grow our project and managed solutions business.

The RCM Engineering division has also been performing well and is poised to continue its solid growth well into the future. The global energy transition has opened up new opportunities for RCM including the recently opened Thermal Kinetics Test Center . The Energy services group announced a major new win for a new substation project in the northeastern US. The group has also been expanding its European footprint. The aerospace and defense team has already added 8 new clients in 2023 and expects to expand to 12 by the end of the year. The future for the engineering division looks promising as well as explained by Executive Chairman Vizi on the Q2 earnings call:

The expansion of existing clients and new clients with our core expertise, and new arenas provides much desired depth and breadth to the organization and strongly positions us for 2024. We have also begun to see traction on one of our largest awards from our strongest OEM clients across the entire spectrum of engineering resources with potential opportunity spanning into 2026.

Strong Leadership

The Executive Chairman and President, Brad Vizi has been in that role since June 2018. Prior to that he was Chairman of the Board since 2015 and was a Board member starting in 2013. He has also served on the board of L.B. Foster ( FSTR ) since 2016. He has significant public company experience in the areas of capital allocation, corporate strategy, compensation planning, and marketing to the investment community. According to the company website , his prior experience in investing and asset management is also extensive and impressive.

The CFO, Kevin Miller, also has an impressive track record with the company, serving as CFO, Treasurer, and Secretary since October 2008. From 1997 to September 2008, he was Senior Vice President of RCM. On the Q2 earnings call, he summarized the results for the first half of 2023 and what they expect to see going forward:

For fiscal 2023 we expect at least 75 school clients with 30 over 100k in revenue. We saw a nice sequential uptick in engineering revenue in Q2 '23 driven mainly by the increase in energy services contract wins. We expect our engineering group to sequence sequential increases throughout the rest of 2023. As Brad discussed, our Life Sciences and Information Technology segment had a nice sequential increase as our managed service offerings continue to drive our growth.

We expect the fourth quarter to be our best quarter for 2023. With so many recently awarded school contracts, we're very excited to see the results. We expect both our Engineering and Life Sciences and Information Technology segments to see sequential increases in the third and fourth quarters. While there is always the risk of large projects sliding to the right, we expect a substantial uptick in the fourth quarter for all three of our engineering groups.

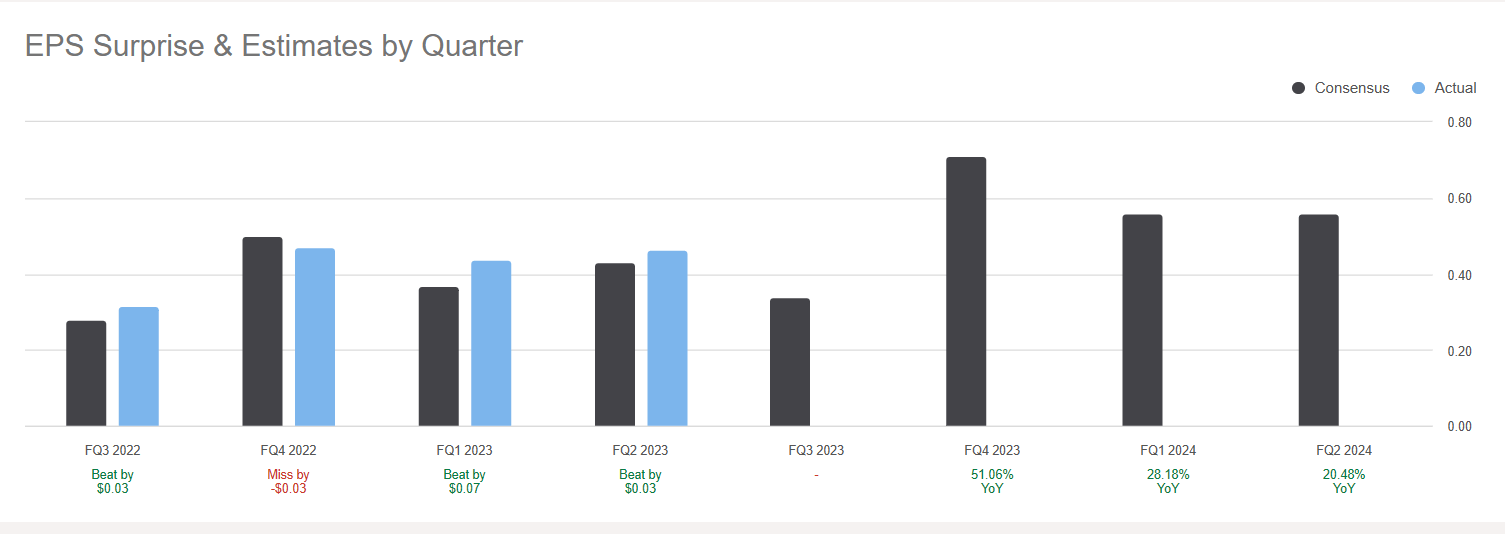

This expectation for a seasonally weaker Q3 followed by a big spike in Q4 earnings is consistent with previous years and is illustrated by the Earnings Summary page for RCMT. The Q3 earnings are expected to be somewhat subdued as a result of schools being closed through August or early September, so those revenues will likely jump in Q4 once that demand picks up again and with the recent additional wins in the healthcare segment for school clients, as explained by CFO Miller:

We're incredibly excited about this upcoming school year. I want to give some limited information on our non-COVID related school business. In fiscal 2022, we had about 60 active school clients with 22 exceeding 100k in revenue. That compares to fiscal 2019 when we had only six clients over 100k in revenue. For fiscal 2023 we expect at least 75 school clients with 30 over 100k in revenue.

{kind=link}

M&A Activity Fuels Long-Term Growth

In October 2022, RCM acquired TalentHerder, a talent acquisition services company, bolstering their existing capabilities in recruitment and outsourcing. In May of this year, RCM Energy announced the opening of its new operation center in Germany, further expanding their European footprint.

In the aerospace and defense segments, the company tripled the number of new hires across their client base in Q2 as compared to Q1. The space segment is also expanding, and a major new win is helping to propel that business forward, as explained by Brad Vizi on the Q2 call:

In addition, we have been awarded a sole source contract for one of our space clients, where we are providing support from conceptual design through aftermarket services in hybrid and flexible scenarios. We now have a proven track record with our digital conversion expertise and methodology with an aftermarket, as well as our model-based definition prowess, which now expands across multiple clients throughout the United States.

Additional backlog was added during the first half of 2023 in the Engineering division including the critical development of elements related to an ethanol aviation fuel facility and the RCM Thermal Kinetics unit startup.

The IT and Life Sciences division has also benefited from recent acquisitions and a growing pool of qualified applicants ready to deploy on project assignments, as indicated on their website.

{kind=link}

Valuation and Capital Allocation

As of the end of Q2 the company had repurchased nearly 1.6 million shares of company stock. After a seasonally weak Q3 the fourth quarter is on track to see a double digit increase in earnings growth, consistent with the company’s long-term objectives.

Overall gross margin in Q2 was flat QOQ at 28% although the IT and Life Sciences segment saw outstanding margin performance at 39.4%. Engineering gross margin saw a small uptick but is expected to be even better going forward, in the mid-twenties. Healthcare margins should improve by Q4 with the new school business increasing its share.

The CFO, Kevin Miller stated that Q3 2023 EBITDA should be in line with Q3 2022, with Q4 lining up to have a nice run rate heading into 2024. The expectation for 2024 is to see double digit EBTDA growth compared to 2023.

The SA Quant factor grades for RCMT are all quite positive as well. RCMT is ranked 4 out of 36 in the Research and Consulting Services industry, right behind Willdan Group (WLDN).

Seeking Alpha

Willdan also provides engineering and consulting services and is another small company that could be considered a peer to RCMT. Willdan just reported Q3 results on November 2 and expects to see 2023 net revenue growth of between 10% to 12%.

In terms of valuation, the only negative seen on the Quant factor grades for RCMT is the Price to Book value. All other metrics compare quite favorably to peers in its sector.

{kind=link}

Ratings from Analysts

A recent excerpt from a letter written in July by hedge fund Deep Sail Capital Partners explains why they are bullish on the stock for reasons similar to what I have outlined above. Several other analysts on Seeking Alpha have also given the stock Strong Buy ratings this year. My current rating is just a Buy rather than Strong Buy only because I believe that the Q3 earnings report could disappoint based on comments from the leadership team on seasonal impacts to the bottom line. For investors willing to hold for the long-term, I believe that RCMT will not disappoint over the next 5 years even if they have one bad quarter.

Seeking Alpha

Conclusion

As I stated in the beginning of this article, RCMT is poised to take advantage of a growing contract, specialized recruitment, and outsourced employment trend as companies struggle to hire qualified specialists in the fields of IT, Engineering, and Healthcare. With existing clients in schools, engineering firms, aerospace and defense industries, and Life Sciences looking to expand and/or request repeat business, RCMT is positioning itself for long-term growth.

The outstanding management team has executed well on the company strategy and vision and is capitalizing on its existing client relationships while expanding into new areas of expertise as well as new geographies including Europe.

While the Q3 results may not exceed expectations the market could decide to punish the stock in the short term. The long-term growth expectations and current low valuation make for a buying opportunity should the price suffer after reporting Q3 earnings on November 9. I would be cautiously optimistic about buying shares under $20 with a near-term price target of $25, but because the company has a very small market cap of about $150M, the possibility of some price volatility should be anticipated. Even after reporting strong results in Q2, the price dropped considerably in the days following the August 9 report before recovering and advancing higher as seen in the yellow highlight on the price chart.

{kind=link}

It would not be unusual for the price to drop 10% to 20% in the next few days, depending on what happens with the broader market and based on the Q3 report. If the company misses expectations (currently EPS of $0.34 expected) then it would be quite possible to see the price drop by 10% or more.

I rate the stock a Buy at the current price of just below $20 but I would raise my rating to a Strong Buy if the price should drop below $16.

For further details see:

RCM Technologies: Reaching A Tipping Point