RCMT - RCM Technologies: Time To Take Profits (Rating Downgrade)

2023-11-11 01:33:35 ET

Summary

- RCM Technologies' Q3 2023 financial results showed flat revenue growth and an 8.9% decrease in EBITDA.

- The specialty health care segment saw a decline in revenue due to weak demand from non-school clients.

- The company's balance sheet is a concern, with transit accounts payable soaring and the tangible book value becoming negative.

Introduction

I’ve written two articles on SA about RCM Technologies ( RCMT ), the latest of which was in June when I said that I expect EBITDA for the full year to remain above $20 million.

On November 9, RCM released its Q3 2023 financial results , and I’m surprised that the share price spiked by 14.1% on that day considering they seem somewhat underwhelming. Revenue growth was flat while EBITDA went down by 8.9% year on year to $4.7 million. While Q4 2023 is likely to be strong and I continue to think that EBITDA for the full year will surpass $20 million, the valuation is starting to look stretched, and this could be a good time to take profits. I’m cutting my rating on the stock to neutral. Let’s review.

Overview of the Q3 2023 financial results

If you aren't familiar with the company or my earlier coverage, here's a brief description of the business. RCM Technologies is involved in the provision of business and technology solutions and its business is split into three segments - engineering, life sciences and information technology, and specialty health care services. All three segments perform staff augmentation services, and the company generates revenues from permanent placement fees. The specialty health care services segment accounts for about half of revenues and specializes in the provision of long-term and short-term staffing and placement services involving health care professionals such as nurses, paraprofessionals, and physicians. Most of its clients are schools and this business got a strong boost to revenues and margins during the COVID-19 pandemic, particularly in late 2021 and the first half of 2022. The engineering segment provides engineering and design, engineering analysis, technical writing and technical support as well as EPC services and it has a retention rate of about 95%, with over 20 Fortune 500 companies among its customers. Life sciences and information technology, in turn, specializes in enterprise business, application, infrastructure, and life sciences solutions.

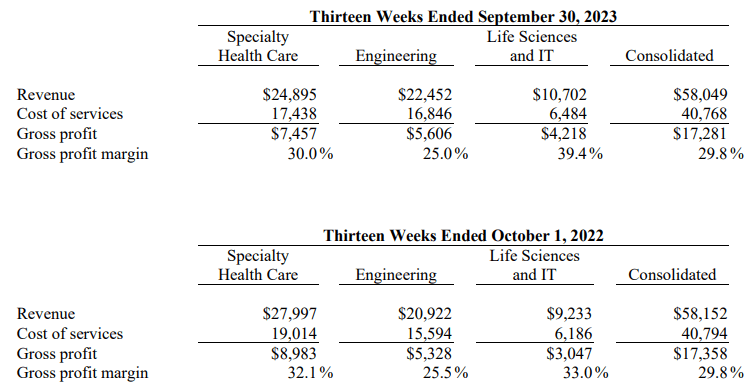

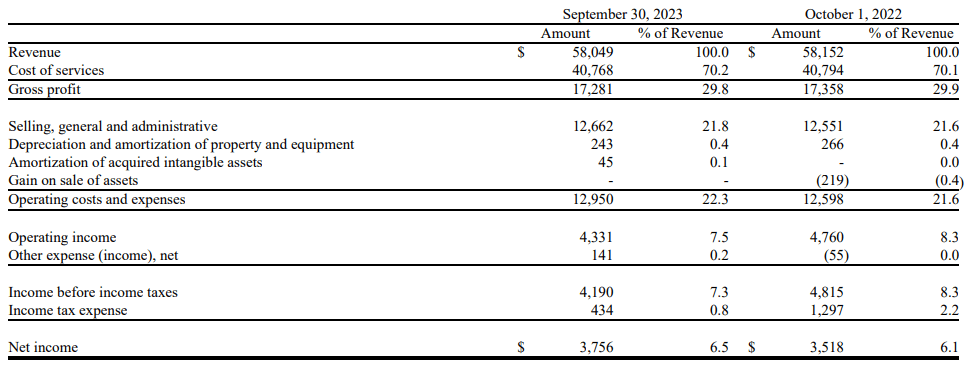

Looking at the Q3 2023 financial results, we can see that revenue inched down by 0.2% year on year to $58 million while the gross profit margin stayed unchanged. The revenue of the specialty health care segment declined by $3.1 million due to weak demand from non-school clients as revenues from those slumped to $7.6 million from $11.4 million a year earlier (see page 35 here ). The company is just not getting a boost from COVID-19 lockdowns anymore and I expect the growth of this segment to remain in negative territory for one or two more quarters. The revenue of the engineering segment rose by 7.3% as a $3.1 million improvement in energy services revenue was partly offset by $1.4 million and $0.2 million decreases in aerospace and industrial processing revenue, respectively. Aerospace revenue was lower mainly due to a contract reduction with a major client (see page 36 here ). Turning to the life sciences and information technology segment, I think it’s encouraging to see revenue growing by double digit percentages as this year has been challenging for the IT industry. RCM explained during its Q3 2023 earnings call that the increase was driven by focusing investments on market segments with secular growth. In my view, the revenue growth of this segment is likely to remain high over the next few quarters as the company expanded its life sciences practice in regulatory compliance, ERP design and implementation during Q3 2023.

{kind=link}

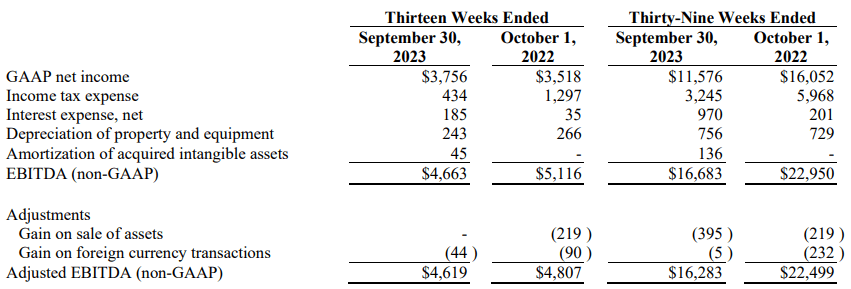

Yet, EBITDA for the quarter decreased by 8.9% despite the revenue and gross margin remaining at the same levels and the main reasons for this included a lack of capital gains as well as slightly higher selling, general and administrative (SG&A) expenses.

{kind=link}

{kind=link}

Looking at the balance sheet, I’m concerned that transit accounts payable has soared to $38.4 million while the transit accounts receivable was just $9.5 million as of September. While the absolute amounts and spreads fluctuate significantly from quarter to quarter, it’s unusual to see the spread that high and this $22.4 million increase accounted for the majority of the $27.1 million free cash flow for the first nine months of 2023. RCM spent a total of $24.4 million on share buybacks during the period , including $3.4 million in Q3 2023. As a result, the tangible book value is now negative.

RCM Technologies

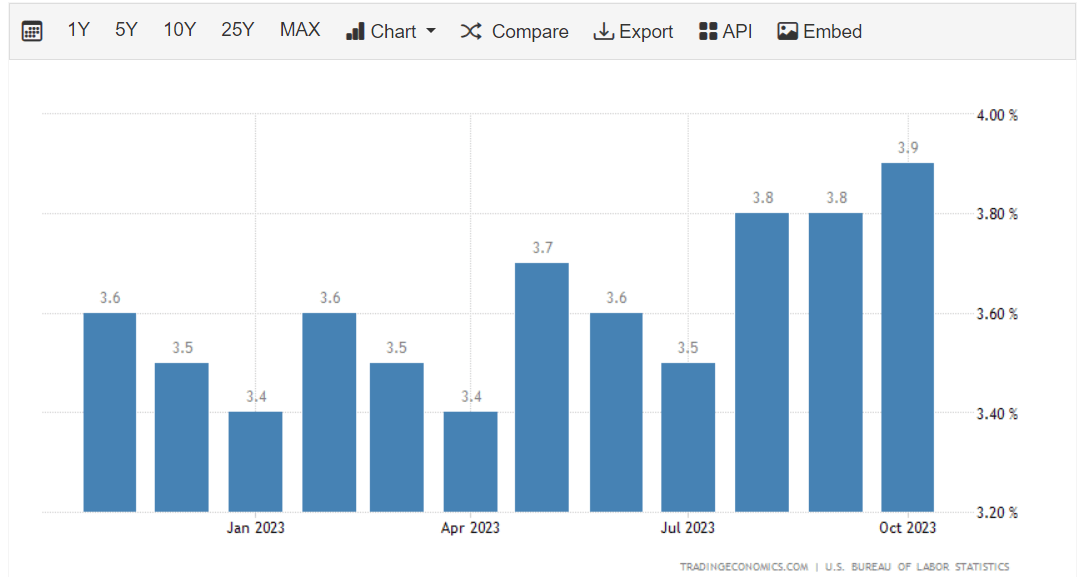

Looking at what to expect for the future, RCM said during its Q3 2023 earnings call that it expects Q4 to be its strongest quarter for the year with EBITDA returning to growth and that the outlook for 2024 and beyond being bright. I find this encouraging considering EBITDA for Q4 2022 came in at $6.9 million, which means that EBITDA for 2023 should surpass $23 million ($6.9 million in Q4 2022 plus $16.7 million for the first nine months of 2023). Yet, I think RCM could be overly optimistic for 2024 considering the unemployment rate in the USA has started to inch up as interest rates remain high. In my view, this is likely to dampen demand for the staffing services sector in 2024.

{kind=link}

Looking at the valuation, RCM Technologies has an enterprise value of $180.2 million as of the time of writing and is trading at an EV/EBITDA ratio of 7.6x on a TTM basis. In my view, RCM is unlikely to grow much in 2024 as the US labor market cools off and I’m concerned that the strength of the balance sheet has deteriorated since the start of 2023 as the tangible book value is now negative. I think that the company should be trading at about 8x EV/EBITDA, which leaves a small margin of safety here and I think that investors should start thinking about taking profits here.

Investor takeaway

RCM’s EBITDA shrank in Q3 2023, but the company is optimistic that it will be back to growth in Q4. However, I’m concerned that the tangible book value has slipped into negative territory due to the aggressive share buybacks and I think that 2024 could be a tough year as the unemployment rate in the USA has started to increase once again. I think this could be a good time for investors to trim or close their positions here.

For further details see:

RCM Technologies: Time To Take Profits (Rating Downgrade)