XYLD - Read This Before Trying To Time XYLD Or Other Covered Call Funds

Summary

- Covered call funds are popular investments in retirement circles.

- Some investors attempt to time their investment in a covered call fund, to increase their income and capital gains.

- Timing a covered call fund is difficult, and not terribly effective.

- An explanation as to why follows.

Author's note: This article was released to CEF/ETF Income Laboratory members on January 20th.

Covered call funds are incredibly popular investments in income and retirement circles, and with good reason. Covered call funds offer investors strong dividend yields and the potential for outperformance when markets are flat or drift downward, a strong combination. These same funds have significantly reduced potential capital gains, an important negative, but one that some investors are willing to put aside.

Some investors attempt to time their investment in a covered call fund, to increase their income and capital gains. Doing so is difficult, and not terribly effective.

Covered call funds have significantly reduced potential capital gains, so buying a covered call fund at rock-bottom prices does not lead to significant capital gains. Investors do see some capital gains from this, but much lower than for other funds.

Covered call fund dividends are somewhat dependent on asset values and share prices, so tend to decline when prices go down. Buying a covered call fund at rock-bottom prices means buying at rock-bottom dividends too, so investors don't see a significant increase in their yields or yield on cost from doing so. Investors do see some benefit from doing this, but lower than for other funds.

Successfully timing a covered call fund does not lead to significant capital gains or significantly increased income, so the impact on total returns is quite muted too. There is an impact, but quite a bit lower than average.

Market timing strategies are difficult to accomplish, risky and expensive to execute. Successfully timing a covered call fund brings comparatively low benefits to investors. As such, and in my opinion, attempting to time a covered call fund is a high-risk low-reward trade, and one I would refrain from attempting.

Attempting to time other funds seems like a better use of an investor's time, as would opportunistically re-investing covered call dividends in discounted CEFs and similar investments.

I'll be focusing on the Global X S&P 500 Covered Call ETF ( XYLD ) in this article, but everything here should apply to most covered call funds, including the Global X NASDAQ 100 Covered Call ETF ( QYLD ) and the Global X Russell 2000 Covered Call ETF ( RYLD ). Due to length, I won't be including an in-depth explanation as to how these funds work in this article. I have such an explanation here .

Covered Call Funds - Capital Gains Timing The Market

Covered call funds have significantly reduced potential capital gains under effectively all market scenarios. It is incredibly difficult to time a covered call fund investment so as to generate significant capital gains, because these funds are structured in such a way as to reduce the magnitude of any capital gains experienced.

Investors might be able to time their investment so as to generate some capital gains, but these would very rarely be significant , and would almost certainly be lower than average.

As an example, let's say investors successfully time the coronavirus pandemic, by buying XYLD in March 31st 2020. This is very close to the bottom, and just before one of the sharpest recoveries and bull markets in recent history.

Investing in XYLD at said date would have netted investors 21.5% in capital gains. Very good gains, but significantly lower than those of the S&P 500 index, as well as most dividend equity ETFs, including the well-known Schwab U.S. Dividend Equity ETF ( SCHD ). Capital gains were also significantly lower than those of CEFs and BDCs, two income-producing asset classes with lower potential capital gains than equities.

SeekingAlpha - Chart by Author

XYLD did see strong capital gains, but these were significantly lower than average, and were dependent on impeccable, almost prescient, timing.

Let's say you have good, not outstanding, timing, and invest in XYLD in June 30th instead, and holding until the end of the year. Doing so means buying in the middle of an incredibly strong recovery/bull market, in which equities soared double-digits in a few short months. XYLD itself would have seen capital gains of 9.2%, quite good, but significantly lower than average.

SeekingAlpha - Chart by Author

As should be clear from the above, successfully timing an investment in XYLD generates comparatively low, below-average capital gains.

In my opinion, and due to the above, investors should strongly consider not trying to time an investment in a covered call fund. Timing the market is difficulty, risky, and time consuming. Attempting to time the market might make sense when potential returns are high, but that does not seem to be the case for XYLD, nor for other covered call funds. Investors wishing to engage in market timing might be better off using their (limited) funds in other investments, including the ETFs in the table above. Better to time an investment in SPY than in XYLD, from a capital gains perspective at least.

Covered Call Funds - Dividends Timing the Market

Simple Explanation

A simpler explanation of covered call fund dividends. I have a longer, more in-depth explanation below.

Covered call fund dividends are somewhat dependent on the value of their assets. More assets means more calls can be sold, leading to higher option premiums and hence higher dividends. At the same time, more expensive assets means more expensive calls can be sold, leading to higher option premiums and hence higher dividends. Due to this, as assets per share grow, so do dividends per share. For ETFs, assets per share is basically equivalent to share price, so higher share price means higher dividends, and vice versa.

XYLD's dividends are very tightly linked to the fund's share price, as expected, although fund distribution policies smooth out a lot of volatility.

As covered call fund dividends are somewhat dependent on share prices, there is limited impact on dividend yields when share prices move. Higher share prices means higher dividends, so yields remain (roughly) the same. Same situation for lower share prices. As mentioned previously, buying a covered call fund at rock-bottom prices means buying at rock-bottom dividends too, so the impact on dividend yields and yield on costs is limited too.

As an example, compare XYLD's historical yield on cost:

{kind=link}

With that of PCEF / the average CEF:

{kind=link}

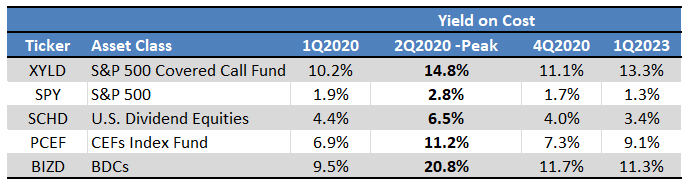

As can be seen above, XYLD's yield on cost is somewhat more stable than that of PCEF. This is particularly notable in early 2020, the big spike in between the 2Y and 4Y mark at the bottom. PCEF's yield on cost spiked in early 2020, almost doubling at its peak. XYLD's yield on cost also increased, but the impact was much more muted, peaking at +40%. An important portion of said increase was due to increased volatility , which led to higher option prices as the pandemic hit. Lower share prices themselves were responsible for a large chunk, perhaps most, of that 40% dividend increase, but not all.

In any case, successfully timing an investment in XYLD does result in a higher yield on cost for investors, but the impact is somewhat more muted relative to PCEF which represents the average CEF. The same is true relative to most other funds and income-producing asset classes as well.

{kind=link}

As can be seen above, XYLD's yield on cost increased by 3.6% during the depths of the pandemic, but other funds saw higher increases too. PCEF's yield on cost increased by 4.3%, and from a much lower base. BIZD's yield increased by a whopping 11.3% , from a comparable base to XYLD.

In my opinion, and due to the above, income investors should strongly consider not trying to time an investment in a covered call fund. For income investors, it seems much better to try and time an investment in BIZD and some CEFs, than in XYLD.

In-Depth Explanation

Let's start by looking at how timing an investment for increased income works for a normal equity, let's say Altria ( MO ).

Altria's stock trades at a specific, but variable, price. Altria's shares currently trade at $45.60 per share. Altria's shares might trade at a different price in the future, lower or higher.

Altria pays a specific, but variable, dividend to shareholders at regular intervals. Altria currently pays investors $0.94 in dividends per share every quarter. Altria's dividends might be different, lower or higher, in the future.

Altria's share price and dividend are different metrics, and might not necessarily move in the same direction. As an example, Altria's dividends increased in 2022, but its share price decreased instead.

Investing in Altria when share prices are low allows investors to buy more shares with the same amount of cash, maximizing their income (more shares = more dividends).

The situation is a bit different for covered call funds.

Covered call funds invest in securities.

XYLD invests in the underlying components of the S&P 500 index. For simplicity's sake, let's assume XYLD directly invests in the S&P 500 index instead.

Although SPY's share price and the price of its options are two different metrics, both tend to move in the same direction. Higher SPY share prices means higher SPY option prices, and vice versa.

Conceptually, this is because potential option profits are at least partly dependent on the price of the underlying security.

For the buyer of these options, profits are basically equivalent to next month SPY capital gains minus option premiums. Let's say the buyer is a bull, and expects SPY to go up by 2.0% next month. Said buyer would be willing to pay 2.0% max for these options, as at this price profits are zero (in practice, other factors would affect the price of these options, but I digress). If SPY trades at $1000 per share, they would be willing to pay $20. If SPY trades at $100 per share, they would be willing to pay $2. SPY currently trades at $410, so they would be willing to pay $8.20, not too far off from current option prices . Do note that the situation is very different to that of most investments or equities. Altria's dividends are not dependent on the company's share price at all, at least not this directly.

As is hopefully clear from the above, option prices are directly impacted by the price of their underlying security. Most option pricing formulas explicitly indicate this as well.

Investopedia

Due to the above, buying covered call funds when share prices are low has limited or reduced impact on the dividend yields and yield on costs received by investors.

Covered Call Funds - Total Returns

Successfully timing an investment in a covered call fund results in comparatively meager capital gains and increased income. Total returns should be comparatively low as well. This was the case if investors bought XYLD in 2Q2020, close to the market bottom of that year, as expected.

Although successfully timing an investment in the covered call fund did lead to positive capital gains, income, and total returns for shareholders, the impact was comparatively low in all three metrics.

Covered call funds are ineffective investment vehicles for market timing strategies, so investors attempting to implement these should consider alternative funds and investments when doing so. In my opinion, at least.

Covered Call Funds - Other Considerations

Successfully timing the market with a covered call fund leads to relatively meager capital gains, income, and total returns. Corollary to this is that unsuccessfully timing the market leads to relatively meager capital losses, reduced income, and (negative) total returns. As an example, XYLD has outperformed the S&P 500 by 4.3% since January 2022, close to the market top. XYLD has suffered some losses, but moderately lower than average.

From the above, it seems that timing is less important for covered call funds than average, an important benefit for these funds and their investors.

Covered call funds provide investors with very strong dividends, which can be re-invested in other funds or investments at more opportune times. Investors attempting to time the market could use XYLD's dividends to do so, even if they don't use the fund itself. Doing so is a much more worthwhile strategy than trying to time an investment in XYLD itself, in my opinion at least.

Conclusion

Successfully timing an investment in a covered call fund leads to comparatively meager capital gains, less increased income, and total returns. Successfully timing the market is difficult, risky, and somewhat expensive. In my opinion, attempting to time a covered call fund is a high-risk low-reward trade, and one I would refrain from attempting.

For further details see:

Read This Before Trying To Time XYLD Or Other Covered Call Funds