STWD - Ready Capital: Why Decreased Distributable Earnings Are Not Frightening

2023-06-28 17:13:37 ET

Summary

- I expect Ready Capital's distributable earnings in 2Q and 3Q 2023 to be lower than the current quarterly dividend of $0.40 per share.

- Thus, one might argue that there could be a dividend cut in 2H 2023. However, the company can maintain the current quarterly dividend even with distributable earnings of $0.30 per share.

- Ready Capital's recent merger with Broadmark Realty Capital has provided the company with higher unrestricted cash, better debt-to-equity ratios, and expanded operations. The merger is expected to increase Ready Capital's distributable earnings.

- In case of a dividend cut, in my worst-case scenario, RC's dividend yield may remain higher than 10% at its current prices.

As Ready Capital ( RC ) reported its 1Q 2023 quarterly results, due to significantly lower distributable earnings compared with the previous quarter, I believe the probability of a dividend cut for the second quarter increased. However, for the second quarter of 2023, RC’s Board of Directors announced two dividends to common stockholders and operating partnership unitholders totaling $0.40 (in the first quarter of 2023, RC paid a dividend of $0.40 per share). As RC’s distributable earnings may not cover its quarterly dividends of $0.40 per share in 3Q and 4Q 2023, and as interest rates are expected to remain high for now, one might argue that there might be a dividend cut. However, we cannot be sure about that, and the company's Board of Directors might decide to maintain its current quarterly dividends in 3Q and 4Q of 2023.

Ready Capital has a strong balance sheet, and its significant high small to medium balance commercial ((SBC)) originations in 2021 and 2022 can help keep the company's balance sheet in a good position. Also, RC's small business administration ((SBA)) originations in 2021 and 2022, which were about 120% more than in 2020, can bring a considerable amount of cash to the company in the following years. Also, the merger with Broadmark has been completed, and now, providing significant growth capital for investment. Thus, even with distributable earnings of lower than $0.40, the company's Board of Directors might be able to maintain the current quarterly dividends. However, it is wise to be ready for the worst. In case of a dividend cut (if it happens), I estimate how much would it be. I estimate Ready Capital's distributable earnings in 3Q and 4Q 2023 to be about $0.30 per share. Thus, in my worst-case scenario, RC's Board of Directors can approve 3Q and 4Q 2023 quarterly dividends of $0.30 per share. In another world, in case of a dividend cut, RC's quarterly dividend would decrease from $0.40 to $0.30 per share. It is just an assumption based on my estimation of RC's earnings in 3Q and 4Q 2023, and I am not saying that there is going to be a dividend cut for sure. However, be mindful that even assuming quarterly dividends of $0.30 per share, RC's 1-year forward dividend yield would be more than 10% at its current prices, which makes RC a buy for me.

The merger

On 31 May 2023, Ready Capital announced the completion of the merger with Broadmark Realty Capital, a real estate finance company that specializes in originating and servicing residential and commercial construction loans. As a result of the merger, each outstanding share of common stock of Broadmark converted into the right to receive 0.47233 shares of Ready Capital's common stock. Due to the Merger with Broadmark Realty Capital, Ready Capital now has access to higher unrestricted cash, has higher unencumbered assets, has a better recourse debt-to-equity ratio, and has a better total debt-to-equity ratio. Also, due to the merger, Ready Capital is now operating in more locations. It is important to know that since 2016, Ready Capital has completed seven transactions, including one reverse merger, two acquisitions, and four mergers. Thus, its recent merger is not a new thing to the management, and, the company has enough experience to handle potential challenges.

Distributable earnings and dividend yield

RC’s net income jumped from $14 million in 4Q 2022 to $37 million in 1Q 2023. However, RC’s better net income in 1Q 2023 compared with 4Q 2022, shouldn’t mislead you about its ability to pay dividends. Because, taking into account the impact of CECL on accrual loans, and other reconciling items, RC’s distributable earnings attributable to common shareholders in 1Q 2023 was $33 million, or $0.31 per share, compared with $47 million, or $0.42 per share in 4Q 2022.

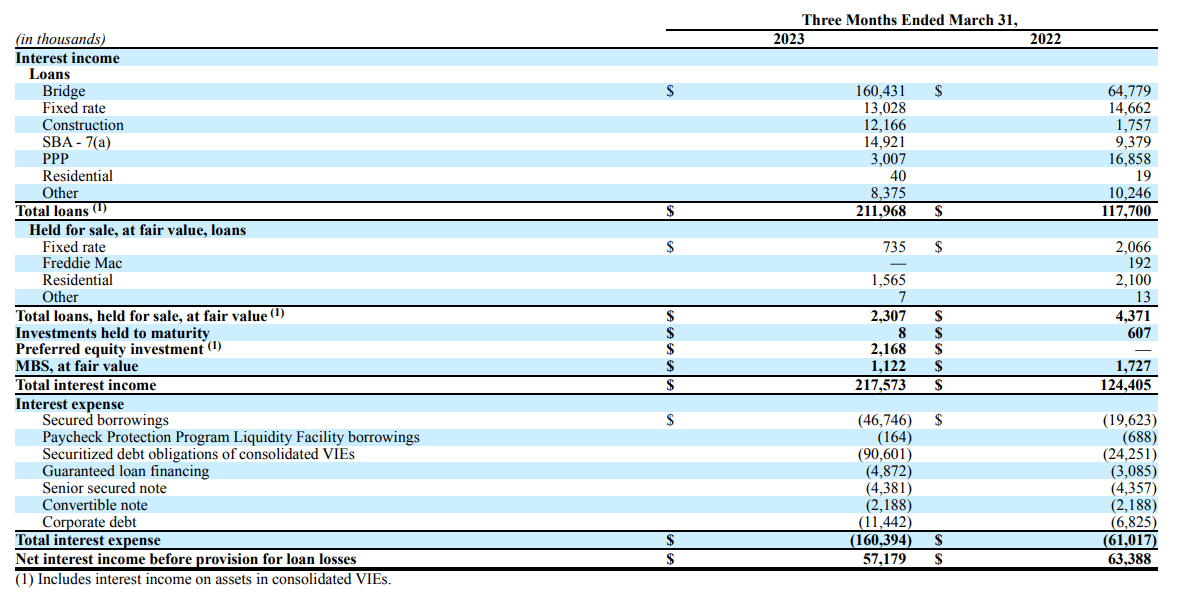

As of 31 March 2023, RC had net total loans of $3128 million, compared with $3576 million on 31 December 2022, as its bridge loans dropped. On the other hand, the company’s net total loans in consolidated VIEs increased from $6312 million on 31 December 2022 to $6782 million on 31 March 2023, as its bridge loans in consolidated VIEs increased by $523 million. In the first quarter of 2023, RC’s interest income from bridge loans was $160 million, compared with $65 million in 1Q 2022. On the other hand, as its secured borrowing and securitized debt obligations of consolidated VIEs jumped in 1Q 2023, RC’s interest expense in 1Q 2023 was $100 million higher than in 1Q 2022 (see Figure 1). As the company is exposed to changing interest rates and market conditions, its cash flows associated with borrowings have been negatively affected due to higher interest rates. Interest rates in 2Q 2023 are higher than in 1Q 2022, and there might be further interest rate hikes by the end of the year. Thus, excluding the effect of the merger with Broadmark, RC’s net interest income in 2Q 2023, 3Q 2023, and 4Q 2023 may be lower than in 1Q 2023. However, it is important to know that RC’s provision for loan losses of $34 million in 4Q 2022, turned into a recovery for loan losses of $7 million in 1Q 2023, implying that the company is now at a lower risk of loan defaults. The company’s distributable earnings in 2Q 2023 (excluding the effect of the merger with Broadmark), were flat QoQ.

Figure 1 – RC's interest income and interest expense

{kind=link}

In the first quarter of 2023, Broadmark reported distributable earnings of $12 million, or $0.10 per share, flat QoQ. In the first quarter of 2023, Broadmark had a net interest income of $17 million, compared with a net interest income of $14 million in 4Q 2022, and a net interest income of $22 million in 1Q 2022. Overall, higher interest rates hurt Broadmark financial results. But, the company’s 1Q 2023 results were better than in 4Q 2022. Before the merger, Broadmark had a monthly cash dividend of $0.035 per share ($0.105 per share on a quarterly basis). As Broadmark’s distributable earnings in 1Q 2023 was $13 million, I expect Ready Capital’s distributable earnings from the merger with Broadmark to increase between $10 to $15 million. Ready Capital’s distributable earnings in the second quarter of 2023 might be between $45 to $55 million. As Ready Capital had 111 million shares in 1Q 2023, and Broadmark had 132 million shares in 1Q 2023, due to the merger, and with a one to 0.47233 conversion rate, Ready Capital’s number of shares of common stock outstanding in 2Q 2022 is calculated to be 173 million. Thus, I estimate Ready Capital’s distributable earnings in 2Q 2023 to be between $0.26 to $0.32 per share. RC's board of Directors has already declared a 2Q 2023 dividend of $0.40 per share, meaning that the company could also potentially declare quarterly dividends of more than its distributable earnings in 3Q and 4Q 2023 too.

But, be mindful that it is not normal for RC to pay a quarterly dividend more than its distributable earnings. From 1Q 2022 to 4Q 2022, RC's distributable earnings fully covered its quarterly dividends. Due to higher interest rates, the company's net interest income (before provision for or recovery of loan losses) was the lowest in the past five quarters. The Federal Reserve might start decreasing interest rates soon, and even before then, there might be further rate hikes. Thus, in 3Q and 4Q 2023, RC's distributable earnings might be about $0.30 per share. Based on this estimation, I estimate RC's dividend cut, if it happens. Please be aware that I am not saying that RC's Board of Directors will cut the quarterly dividend. Also, I am not saying that RC's Board of Directors should cut its quarterly dividend. I am just estimating (based on my calculations for RC's distributable earnings in 2Q and 3Q 2023 after the merger) that in case of a dividend cut (which is hypothetical), how much of a quarterly dividend you can expect in 3Q and 4Q 2023.

As the normal situation is that the company's distributable earnings fully cover its dividends, in case of a dividend cut (hypothetical), and in my worst-case scenario, you still can expect RC's Board of Directors to approve a quarterly dividend of $0.30 per share in 3Q and 4Q 2023 in my view. With a quarterly dividend of $0.40 per share, RC has a 1-year forward dividend yield of 14.3%, which is higher than its peers. Assuming a quarterly dividend of $0.30 per share, RC's dividend yield would be 10.8% at its current prices.

Comparison to the peers

Compared to its peers (based on dividend yield), RC might be as good as Starwood Property ( STWD ), but not as good as Arbor Realty ( ABR ) and Blackstone Mortgage Trust ( BXMT ). In my article on Starwood Property, I explained that there might be a dividend cut in the upcoming quarters. Without a dividend cut, STWD has a 1-year forward dividend yield of 10.0%, which is lower than my estimation for RC’s 1-year forward dividend regarding a dividend cut of $0.10 per share. In my article on Arbor Realty, I explained that its distributable earnings can be high enough to cover quarterly dividends of between $0.40 to $0.42. ABR has a 1-year forward dividend yield of 11.5%. Finally, in my article on BXMT, I explained that its Board of Directors may not face serious challenges to maintain the quarterly dividend of $0.62 per common share. BXMT has a 1-year forward dividend yield of 12.0%. Be mindful that without a dividend cut, RC's 1-year forward dividend yield is 14.5%, which is significantly higher than its peers. We don't know if there is going to be a dividend cut, or if RC's Board of Directors continue approving the quarterly dividend of $0.40 per share. I just want to be ready for the worst.

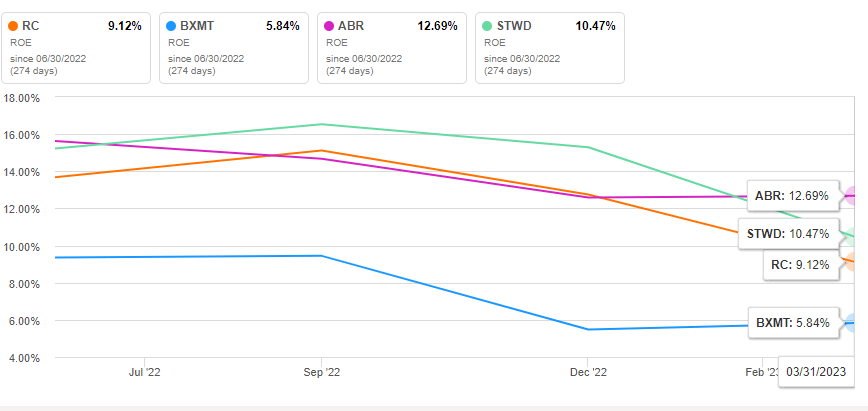

RC's high dividend yield (both in the case of a quarterly dividend of $0.40 or a quarterly dividend of $0.30) is not the only thing that makes the stock a buy. Figure 2 shows that RC has a lower price-to-book value compared to STWD, ABR, and BXMT. While RC has a P/B of 0.74, ABR has a P/B of 1.1, STWD has a P/B of 0.94, and BXMT has a P/B of 0.78. Also, Figure 3 shows RC's ROE compared to its peers. We can see that while RC's return on equity is higher than BXMT's ROE, ABR and STWD have higher ROEs. Overall, based on dividend yield, price-to-book value, and return on equity RC is in a good position in comparison to its peers.

Figure 2 - RC's P/B vs. peers

SA

Figure 3 - RC's ROE vs. peers

{kind=link}

Risks

RC's total investment in some companies is significant. Thus, if a significant investment in one or more companies fails to perform as expected, RC's financial results could be materially affected in a negative way (the magnitude of a loss could be more significant if the company had smaller investments in more companies). As of 31 March 2023, RC's investment in six companies each accounted for more than 5.0% of its net assets (see Figure 4). If any of these companies face financial difficulties and fail to repay their obligations or perform as expected, RC's net interest income may decrease considerably. Furthermore, as interest rates are expected to remain high, investor concerns regarding the U.S. or international financial systems may cause less favorable commercial financing terms. Thus, RC may face a more difficult condition to acquire financing on acceptable terms, and revise its loan generation strategies.

Figure 4 - The fair value of the totals of investments held in portfolio companies as of 31 March 2023 that each represent greater than 5% of RC's net assets

{kind=link}

End note

After the merger with Broadmark, I estimate Ready Capital’s distributable earnings to be $0.26 to $0.32 per share in 2Q 2022. For 3Q and 4Q 2022, I estimate RC's distributable earnings to be about $0.30 per share. Thus, I believe there could potentially be a dividend cut in 3Q and 4Q 2023. However, the company's Board of Directors may also maintain the current quarterly dividends. The point is that you should know what you are dealing with if a dividend cut happens. Even with a quarterly dividend of $0.30 per share, RC’s dividend yield can remain higher than some of its biggest competitors. The stock is still a buy in my opinion.

For further details see:

Ready Capital: Why Decreased Distributable Earnings Are Not Frightening