ETD - Real Estate: A Clear And Growing Drag To The Economy And Potentially The Banking System

2023-10-16 17:58:59 ET

Summary

- Higher interest rates are significantly impacting housing affordability as well as existing home sales, creating a drag on the overall economy.

- However, it is the accelerating deterioration in the commercial real estate sector that should most concern investors.

- Delinquency rates for commercial real estate loans are far higher than in 2022 and continue to move higher at a concerning pace.

- These problems could eventually cause significant problems for the financial system, particularly at regional banks, which are already under considerable pressure.

- Investors should keep a focused eye on these mounting problems as they could easily help trigger the next recession and bear market.

Handling a downturn in fortunes is an uphill task .”? Haresh Sippy.

After falling continuously from a 9.1% reading in June of 2022 to 3.0% in June of this year, the monthly CPI report has started to back up with a print of 3.2% in July and two identical readings of 3.7% in both August and now September.

This means that interest rates are likely to remain " higher for longer ." Unfortunately, higher rates have a myriad of negative impacts across the economy, but one area particularly affected is the real estate sector.

Freddie Mac

The residential real estate market is facing substantial headwinds. Things continue to deteriorate on the mortgage front, as can be seen in last week's weekly mortgage rate update. The 30-year fixed-rate mortgages averaged 7.57% as of Oct. 12, up from last week, when they averaged 7.49% and 6.92% in the year-ago week.

Housing affordability just hit yet another new low last week, according to a report on Bloomberg.

National Association of Realtors

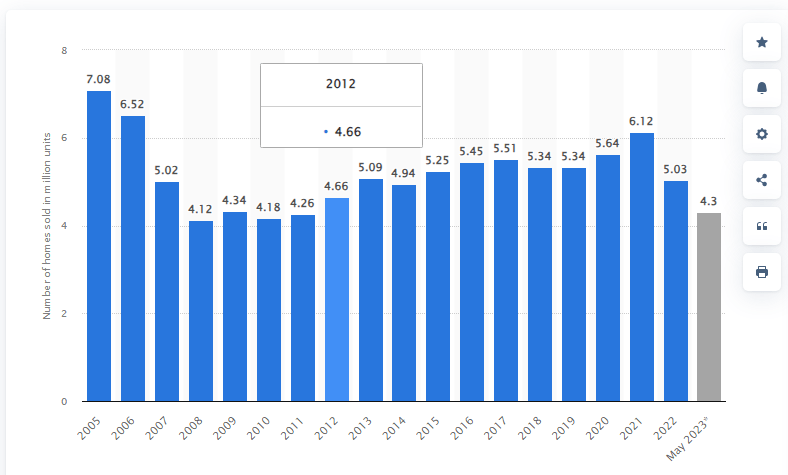

Existing home sales are significantly under their levels of 2020 and 2021.

{kind=link}

This is likely to continue to be the case until either mortgage rates fall significantly; median income rises substantially (unlikely given the probable recession ahead) or average home prices come down dramatically.

Atlanta Federal Reserve

Home prices have held up better than one would think, but that is largely due to the lack of inventory on the market. This is partially due to new home builds being lower than historical trends but primarily due to so many homeowners having " golden handcuffs" in place via having existing mortgage rates under four percent.

Reduced housing activity is likely to remain an economic drag to GDP growth until affordability improves dramatically. Something that is very unlikely to happen over the next year. This also should have impacts to ancillary industries that rely on new home ownership. Headwinds for retailers that serve this space like The Home Depot ( HD ), Williams-Sonoma ( WSM ) , Ethan Allen Interiors Inc. ( ETD ) and Lowe's ( LOW ) are likely to persist if not increase in the quarters ahead. This is another reason I am very underweight the entire retail sector within my portfolio at the moment.

The good news is that tough times in the housing sector are very unlikely to impact the financial system in any significant way, unlike the Great Financial Crisis. After that debacle, " Liar Loans ," mortgages with no income verification or zero/low down payments, went the way of the Dodo bird. A large percentage of current home purchases are being transacted via all-cash deals or through mortgages with very large down payments. Default rates are likely to remain low in this part of the real estate market.

Unfortunately, one cannot say the same thing about the commercial real estate, or CRE, market. While the residential housing market will a negative for economic growth over the near term, growing problems in the CRE space could easily spill over into the larger economy and banking system.

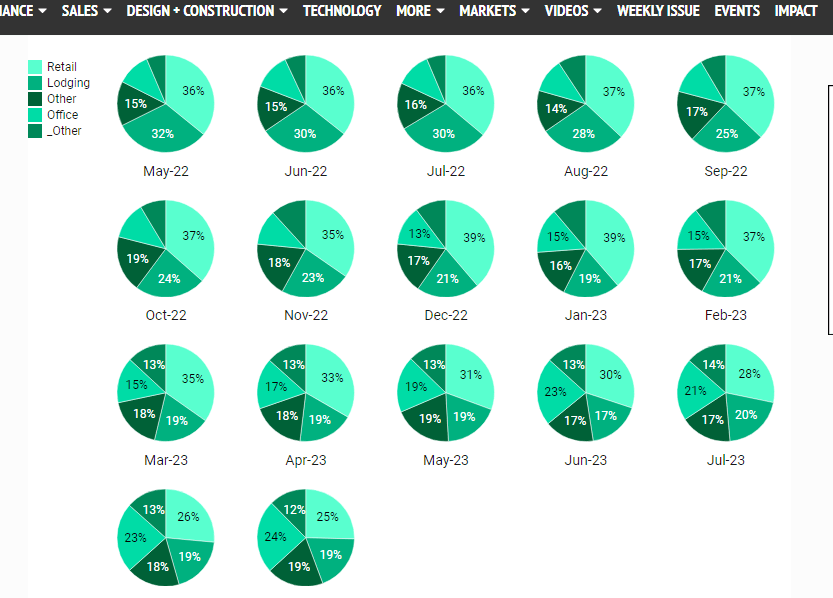

According to the latest report from Trepp for September, 5.19% of all commercial mortgage-backed securities or CMBS are now delinquent. This is up 12bps from August and up sharply from under two percent at the end of 2022. CMBS loans either delinquent or in special servicing rose to 6.83% from 6.73% in August. Most importantly,

The combined special servicing and delinquency rates marked a 7.43 percent overall distressed rate of CMBS loans, which was an increase of 26 basis points (3.6 percent) from August ."

{kind=link}

Delinquency rates were primarily driven higher by the office sector, where they jumped a concerning 139 basis points from August and now stand at 10.75%. While the office space remains under the most distress part of the CRE space due to falling asset values and the impacts from the implosion of the virtual workforce since the pandemic, it is hardly the only part of the CRE complex undergoing mounting stress, as can be seen from the chart above.

Trepp, Morgan Stanley Research

Unfortunately, this situation is likely to get much worse before it gets better. This is due to some $2.5 trillion of CRE debt that needs to be refinanced at much higher interest rates over the next five years. Obviously, this could have impacts on the financial system as delinquencies and write-offs continue to increase.

Most impacted will be the regional banks, given this part of the banking system provides 70% of the loan origination to the CRE sector and holds approximately 30% of outstanding CRE debt. Regional banks also are struggling with higher interest rates, causing large " unrealized losses" on their bond portfolios. This is what helped triggered the crisis and eventual insolvency of three large regional banks like Silicon Valley Bank earlier this year. Given the yield on the 10-Year Treasury (US10Y) rose by three quarters of one percent in the third quarter, that challenge has only increased in recent months.

MarketWatch

It is also hard to de-risk in this area, as even the large banks like JPMorgan Chase & Co. ( JPM ) and Goldman Sachs ( GS ) are having problems unloading some of their commercial real estate loans.

Given this, it is hard to see how the regional banks don't see escalating losses from their CRE loan portfolios. This is one reason I have built up a decent position in long-dated, out of the money bear put spreads against SPDR® S&P Regional Banking ETF ( KRE ), despite most regional banks like Regions Financial Corporation ( RF ) being currently cheap on a P/E basis and sporting more than healthy dividend yields. Rising losses on their CRE loan portfolios are likely going to mean healthy. Downward earnings revisions in the months and quarters ahead.

More concerning for the economy, mounting CRE losses also means regional banks will have to pull bank on lending. This will have impacts on the larger economy, especially on small businesses, which are a key client of regional banks.

Deterioration on both sides of the real estate coin is yet another reason I think the most likely scenario for 2024 is recession. However, I believe it is likely to be a mild economic contraction, unless mounting CRE loan losses result in additional regional bank failures and significant impacts to the financial system, then all bets are off.

We cannot have, but can lose, everything .”? Mokokoma Mokhonoana.

For further details see:

Real Estate: A Clear And Growing Drag To The Economy, And Potentially, The Banking System