NNN - Real Estate In Turmoil: 3 Top-Tier High-Yielding REITs We're Buying

2023-09-11 07:00:00 ET

Summary

- Commercial real estate market is facing serious challenges, including pressure on prices and rising interest rates.

- Regional banks in the US are at risk due to their exposure to trillions of dollars in loans and investments in commercial real estate.

- Despite the market downturn, there are three stocks worth considering: Extra Space Storage, Alexandria Real Estate, and NNN REIT, all of which have strong financials and attractive dividends.

This article was coproduced with Leo Nelissen.

Commercial real estate is not in a great spot.

We're seeing some serious cracks, including pressure on prices.

In this article, we start with a breakdown of new developments, which explains why the market isn't so keen on buying real estate.

Year-to-date, the Vanguard Real Estate ETF ( VNQ ) is down 1%, which underperforms the S&P 500 by 17 points.

The goal of this article isn't to predict the next Great Financial Crisis but to highlight three stocks that we're buying.

Two of the stocks we discuss have Strong Buy ratings.

They all have top-tier balance sheets, attractive valuations, and rock-solid business models capable of taking a hit.

So, without further ado, let's dive into it - starting with the bad news.

The Commercial Real Estate Doom-Loop

A few days ago, the Wall Street Journal published an article titled Real-Estate Doom Loop Threatens America's Banks .

{kind=link}

Essentially, the article highlighted two major issues: deteriorating commercial real estate health and the risks this poses for banks.

Over the past decade, regional banks across the United States adopted a strategy of aggressively expanding their commercial real estate lending portfolios in big cities.

Unfortunately, with the commercial real estate market now experiencing a downturn due to rising interest rates and high vacancies, these banks face significant risks.

Their exposure to trillions of dollars in loans and investments could trigger a chain reaction of reduced lending, falling property prices, and more losses.

For example, Bank OZK ( OZK ), while still active in lending, has encountered early signs of market trouble.

In January, a developer defaulted on a $60 million loan from the bank due to escalating construction costs. This loan, considered safe initially, was now worth significantly less than the property it financed. This situation has left the bank in a challenging position.

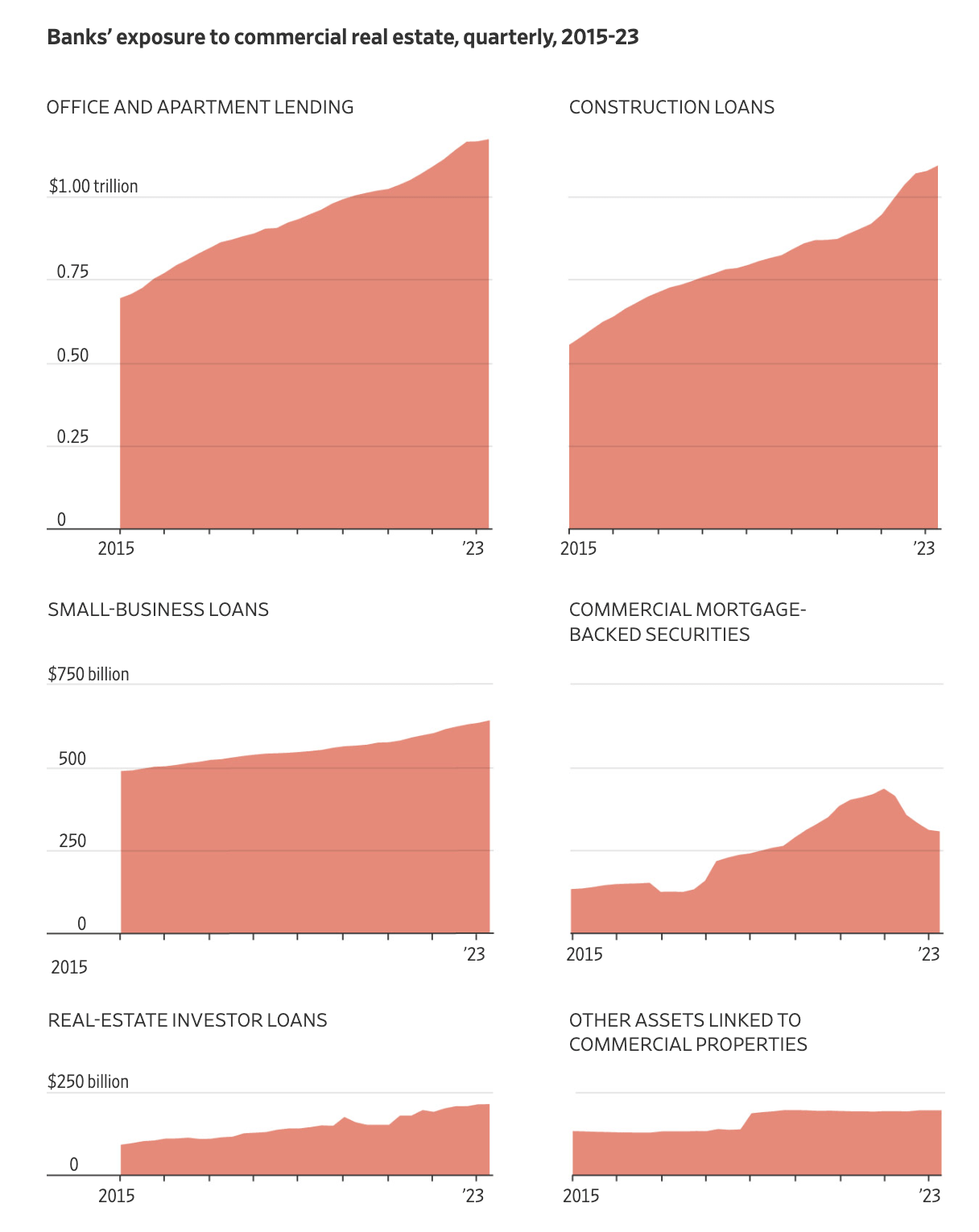

Banks' exposure to commercial real estate extends beyond their traditional lending activities. They also have indirect exposure through loans to financial companies and investments in bonds backed by commercial properties.

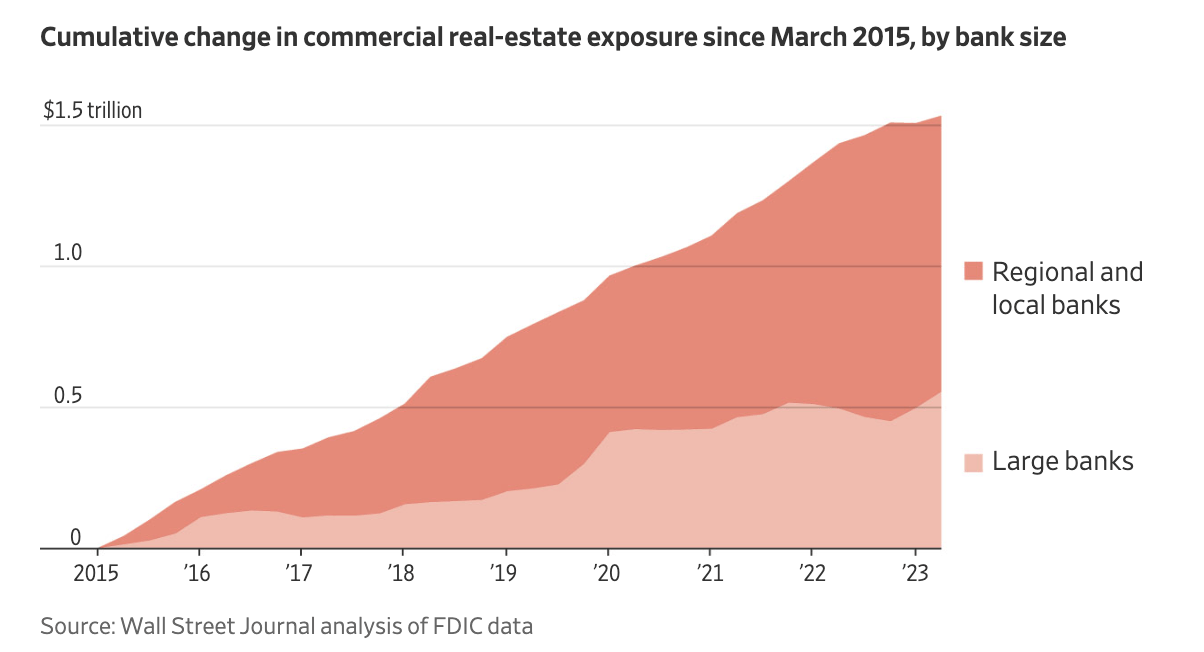

When considering these factors, the total exposure to commercial real estate reaches $3.6 trillion, equivalent to about 20% of banks' deposits.

The chart below shows that the biggest lenders are regional and local banks.

{kind=link}

According to the Wall Street Journal, regional and community banks have long dominated the commercial real estate lending market, especially after the 2008 financial crisis. Very low interest rates made real estate loans profitable, and these banks filled the gap left by larger banks that reduced their exposure to the sector.

{kind=link}

This wasn't an issue when rates were low.

After all, new debt kept the ball rolling.

Now, things have changed.

The Federal Reserve's decision to raise interest rates has added pressure on banks, as they need to offer higher rates to attract depositors. This reduces their lending capacity and ability to absorb losses from bad loans.

Earlier this year, the collapse of midsize banks led to deposit withdrawals, signaling potential systemic risks.

The downward spiral in commercial real estate can only be reversed by lower interest rates or investors stepping in to purchase distressed properties.

Wall Street firms are raising funds for this purpose, but many properties are expected to sell at significantly lower prices, potentially causing losses for owners and lenders.

Nearly $900 billion worth of real estate loans and securities need to be paid off or refinanced by the end of 2024.

Multiple sources have confirmed to me that major players are building war chests in order to aggressively buy real estate the moment elevated unemployment triggers the Fed to cut rates. At that point, they can finance new deals at attractive prices with limited competition from buyers because of the poor state of the economy!

Bloomberg confirmed these developments.

{kind=link}

According to Bloomberg, despite the potential for higher returns due to rising interest rates, new loans for commercial properties from investor-driven lenders, such as private equity and debt funds, plummeted by 60% in the second quarter compared to the previous year.

Bank-originated loans also saw a significant decline of 69%, encompassing multifamily financing.

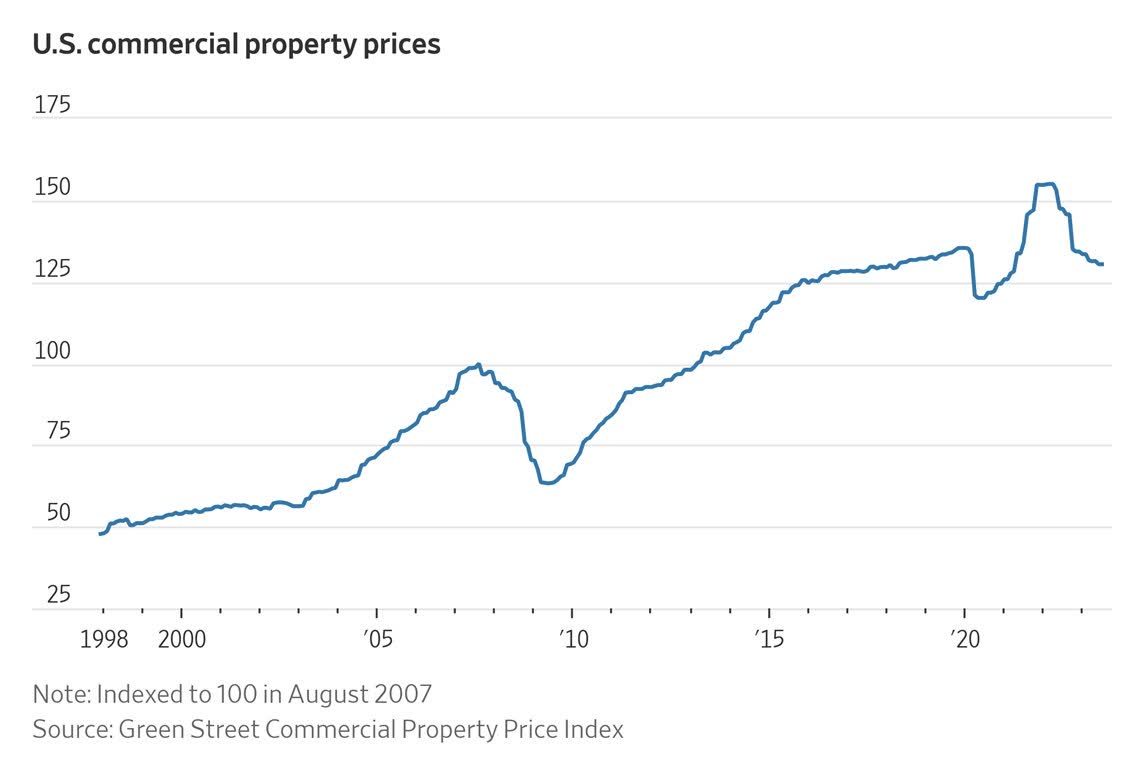

The commercial property sector has witnessed a 10% decline in prices over the year ending in June, according to MSCI Real Assets.

Additionally, the rate of commercial mortgage-backed securities delinquencies, or workouts with special servicers, increased to 6.44% in July, up from 6.07% in the previous month, as reported by the Kroll Bond Rating Agency.

{kind=link}

On top of this, banks are being pressured into reducing commercial real estate exposure after the aforementioned bank failures earlier this year.

Again, we're not predicting the next Great Financial Crisis.

However, unless the Fed lowers rates soon, we could be looking at a doom loop. Prices are falling, and nobody is buying and selling. No new debt is fueling a debt-fueled boom.

This could end in much lower prices before buyers return.

With this in mind, investors can sell everything and run for the hills. However, they can also buy 5% yielding short-term government bonds.

Or they buy bulletproof REITs with high yields, consistent dividend growth, and healthy balance sheets. These stocks may suffer in the mid-term. However, at fair prices, they offer enticing opportunities to build long-term wealth.

Extra Space Storage - 5.1% Yield, BBB+ Credit Rating

The first REIT is my favorite: Extra Space Storage ( EXR ).

It is a core holding of my portfolio and also one of my worst-performing investments at the moment. Needless to say, this comes with opportunities.

Extra Space Storage is somewhere caught in the middle.

The company is in fantastic financial shape. It got a credit rating upgrade to BBB+ after it finished the acquisition of Life Storage (formerly trading under the LSI ticker). Rating agencies really liked that the two strongest self-storage operators joined forces.

The combined company has $12 billion in net debt. Its net leverage ratio is 5.0x EBITDA. Only 16% of its debt is secured. Just 11% of its debt matures before 2025.

Furthermore, both EXR and LSI have dominated the self-storage space since the Great Financial Crisis when it comes to same-store revenue growth and core FFO (funds from operations) growth.

Extra Space Storage

Unfortunately, EXR shares are 45% below their all-time high, caused by general real estate headwinds and the fact that the same storage segment is cyclical.

An industry that benefits from consumers buying more stuff than they need isn't in high demand the moment consumer confidence falls off a cliff.

However, there's good news. For example, EXR has a >94% occupancy rate, high exposure to growth markets in the Sunbelt, and long-term secular growth tailwinds like mini-warehouses and last-mile logistics. LSI especially has been working on these growth measures.

Extra Space Storage

EXR also benefits from supply constraints, which helps pricing.

On a full-year basis, the company expects to grow same-store revenues by at least 2.5%. Net operating income is expected to grow by at least 2.0%. These numbers were revised down from 3.75% and 3.0%, respectively. They still show EXR's resilience in this market.

With regard to its dividend, EXR shares yield 5.1% with a 78% core FFO payout ratio.

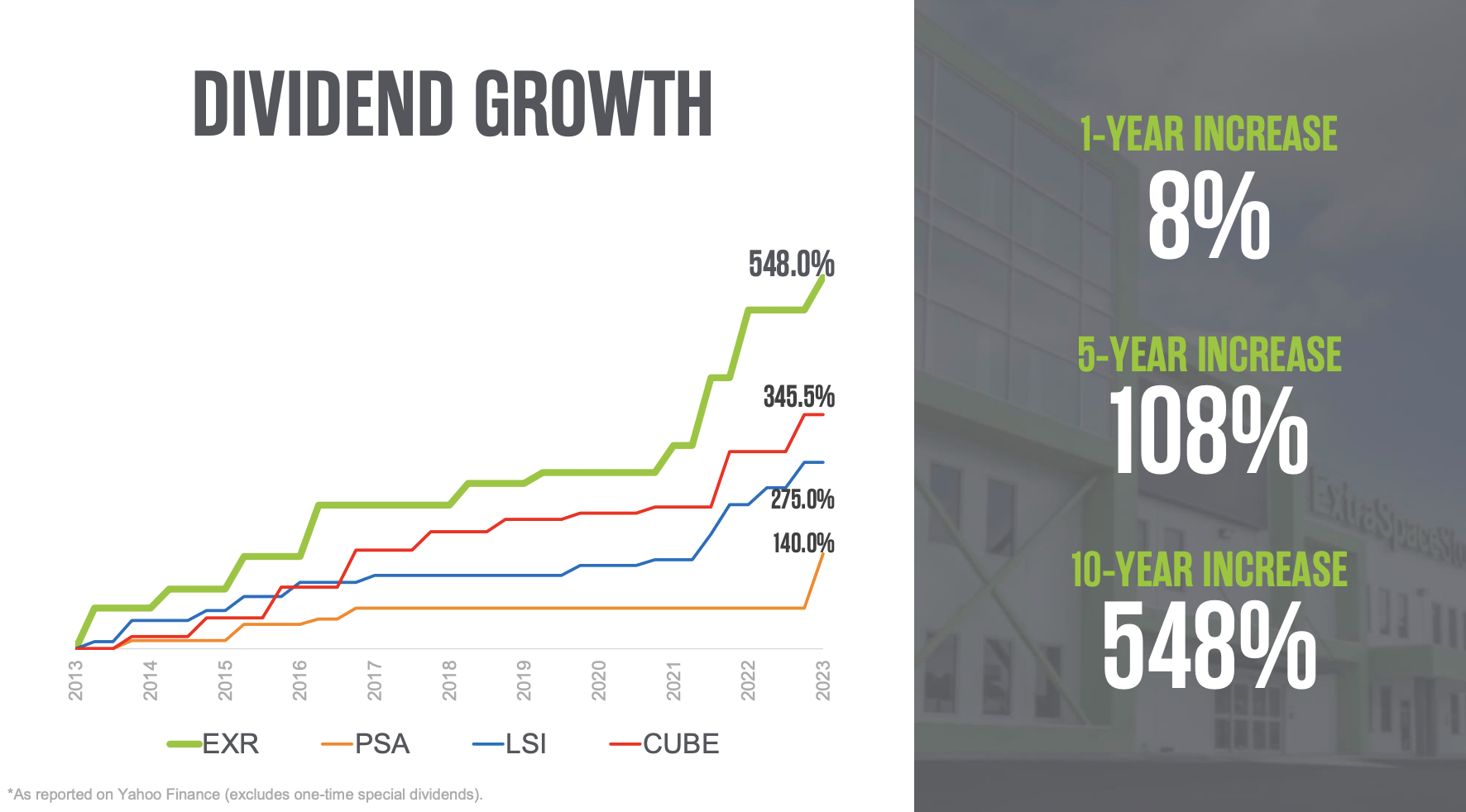

Over the past ten years, EXR's dividend has grown by almost 550%.

{kind=link}

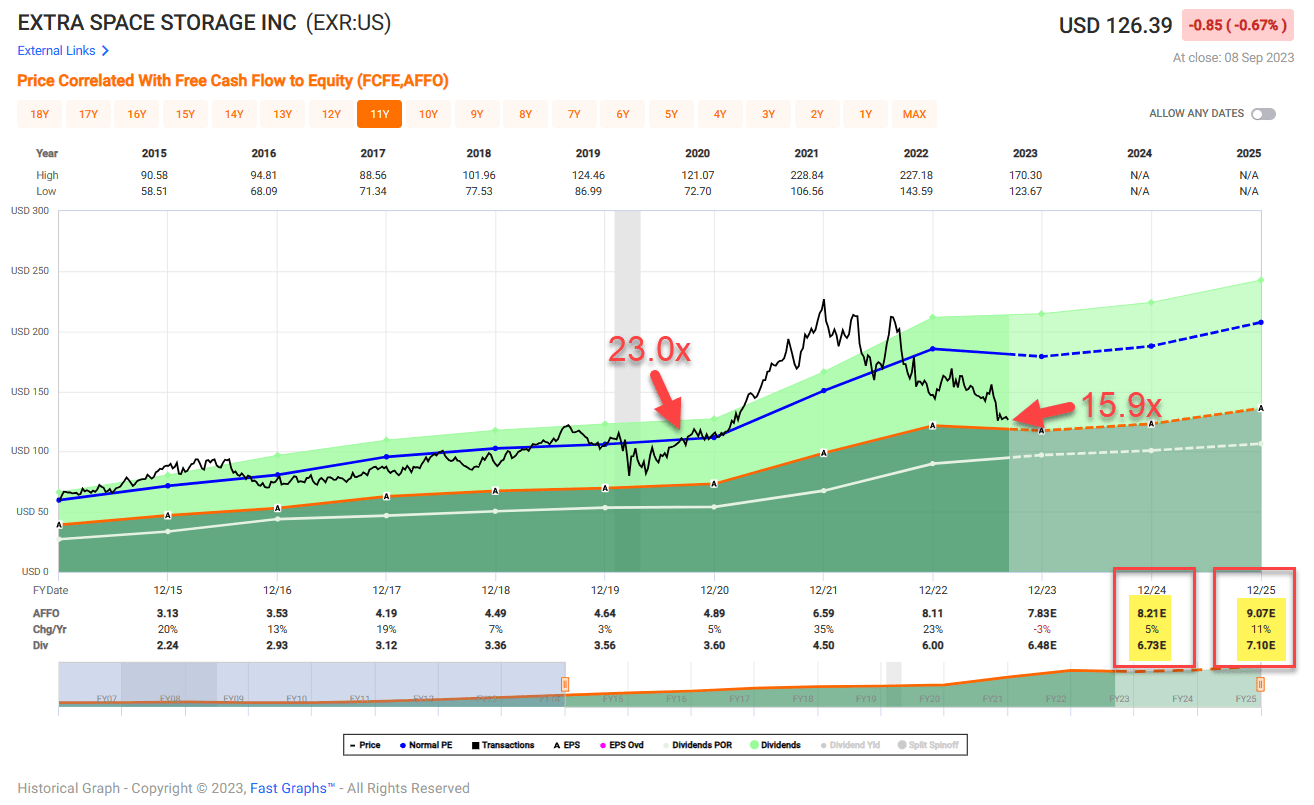

The company is trading at 15.6x core FFO.

This valuation multiple is close to the lower bound of its long-term valuation range. The median sector multiple is 12.6x, which gives EXR a slight premium.

However, over the past five years, EXR has grown its FFO by 14% per year. The sector median compounding growth rate was just 2%.

iREIT® has given EXR a Strong Buy rating.

While the stock is one of the victims of this environment, a lot has been priced in. The company has a top-tier balance sheet (with a recent upgrade), ongoing secular tailwinds, and a very juicy dividend.

{kind=link}

Alexandria Real Estate - 4.3% Yield, BBB+ Credit Rating

Like Extra Space Storage, Alexandria Real Estate ( ARE ) is also suffering. Shares are roughly 48% below their all-time high. Even worse than the consumer-focused exposure of EXR, ARE is dealing with office real estate!

However, it's not as bad as traditional real estate for one major reason: ARE leases to high-tech firms in the healthcare business.

ARE, which also has a BBB+ credit rating and a 95.1% 2023E occupancy guidance, benefits from the fact that 90% of its revenues come from investment-grade or publicly traded large-cap tenants.

ARE IR

The majority of its tenants are healthcare-related companies like biotechnology and life science giants. These companies require high-tech offices. While a full-blown office real estate implosion won't do ARE any favors, it does not compete with your average office REIT.

Its tenants also benefit from anti-cyclical demand.

The industry's market value is estimated to be worth over $5 trillion, with approximately $450 billion allocated for R&D funding in 2023. Alexandria's lab space infrastructure is essential in meeting the demand for this expanding industry.

The demand for lab space remains strong, largely due to scientific, clinical, and commercial achievements rather than market cyclicality or macro trends affecting other sectors. This is a crucial factor to consider.

Even better, Alexandria believes we're seeing a new golden age of biology, with significant FDA drug approvals and record-high innovation.

In the second quarter of 2023, tenant rent collections were nearly perfect at 99.9%, with July rent collection exceeding 99.7%.

Having said that, the company has a 4.3% dividend yield, protected by a safe 62% payout ratio. The five-year dividend CAGR is 6.2%. Over the past ten years, that number has been 7.5%.

With regard to its aforementioned credit rating, this is what the company said during its 2Q23 earnings call:

"We're very proud of the stellar balance sheet we built since the days of the great financial crisis when we were a small and unrated REIT. Upon the closing of our $1 billion line of credit accordion add-on, one of the banks said of Alexandria, Congratulations on the successful expansion of your credit facility to $5 billion. This is a significant accomplishment in any environment where many real estate owners are struggling to source debt capital." - ARE 2Q23 Earnings Call

The company has no maturities before 2025 and 99.2% fixed-rate debt.

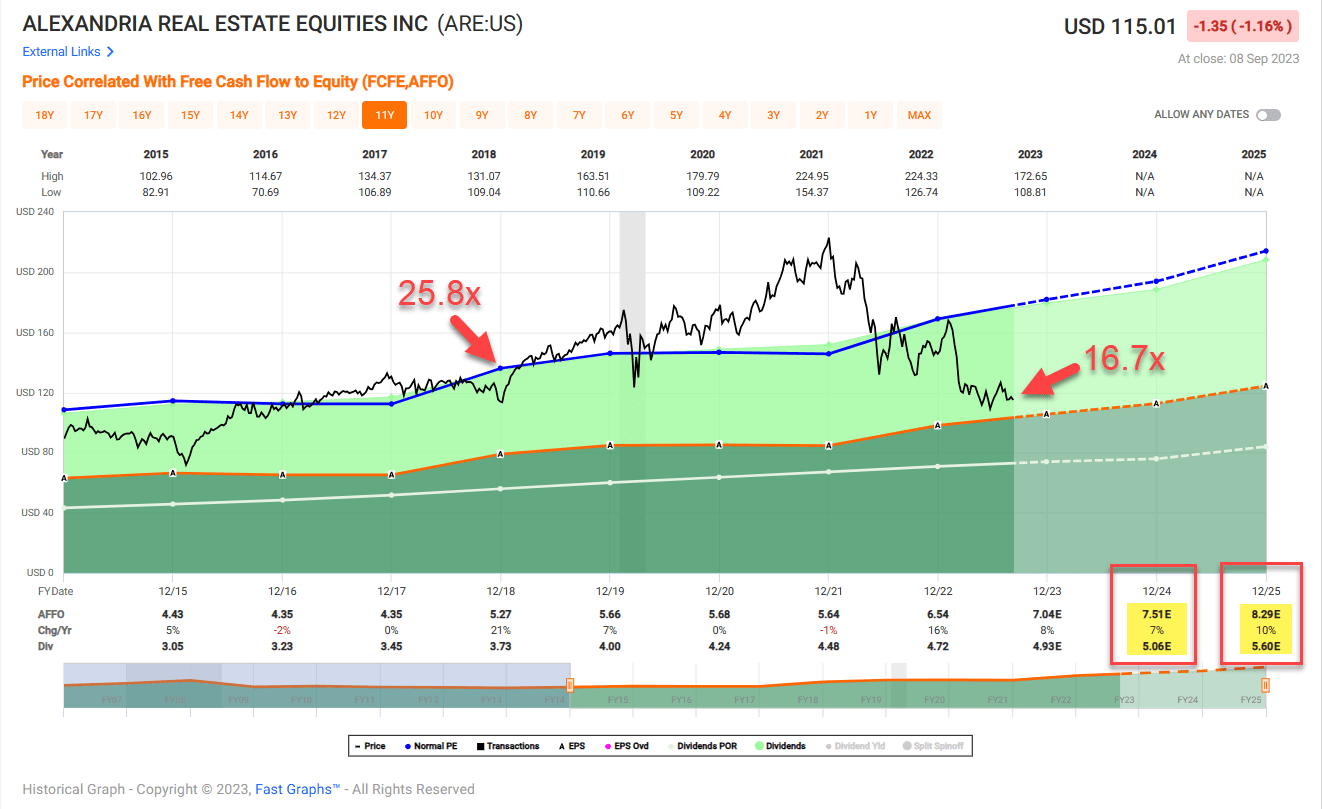

Valuation-wise, the company is trading at 14.5x FFO, below its ten-year median of roughly 16x FFO.

iREIT® has a Strong Buy rating on this company.

{kind=link}

NNN REIT - 5.9% Yield, BBB+ Credit Rating

Like its net lease peer Realty Income ( O ), NNN REIT ( NNN ), formerly known as National Retail Properties, stands out as a source of both safety and income.

With a BBB+ credit rating, 100% unsecured debt, and an average weighted maturity on its debt of 12.3 years, the company is one of the safest players in its industry.

The weighted average effective interest rate on its debt is just 3.8%!

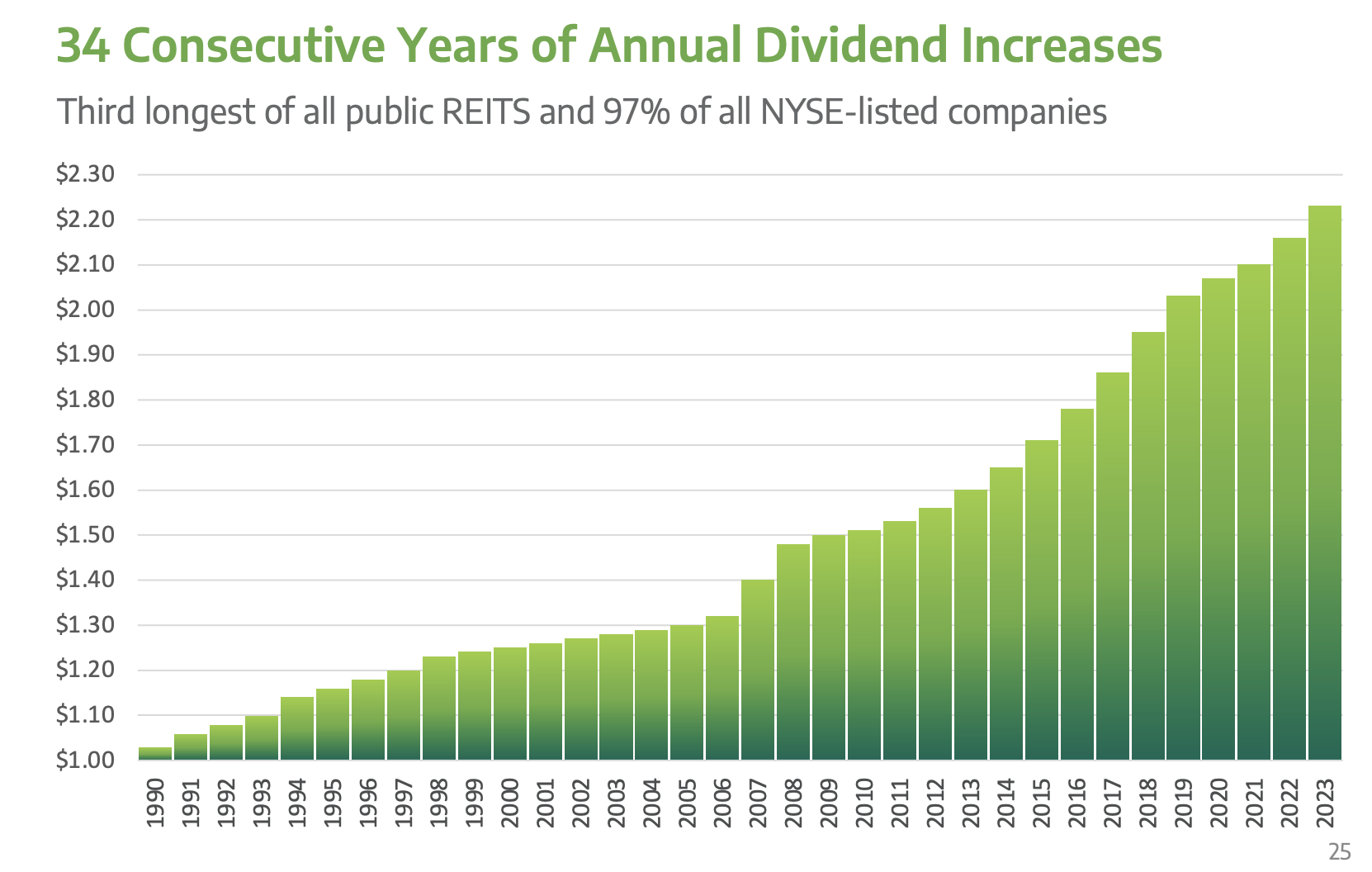

Even during the Great Financial Crisis, the company hiked its dividend. It now has a track record of 34 consecutive years of annual dividend increases. This is the third-longest in the REIT space, and it beats 97% of its NYSE peers.

This dividend is protected by a 68% AFFO payout ratio and its solid balance sheet.

{kind=link}

Over the past five years, the average annual dividend growth rate was 2.9%. That's not a lot. However, it beats the Fed's inflation target, it's consistent, and having a yield close to 6% as a basis is a big deal.

Although it can be said that the retail space is cyclical, the company has top-tier tenants. As of June 30, it had a 99.4% occupancy rate.

It also helps that just 3.3% of leases expire through 2024. The weighted average remaining lease term is 10.2 years. Close to 60% of leases expire AFTER 2031.

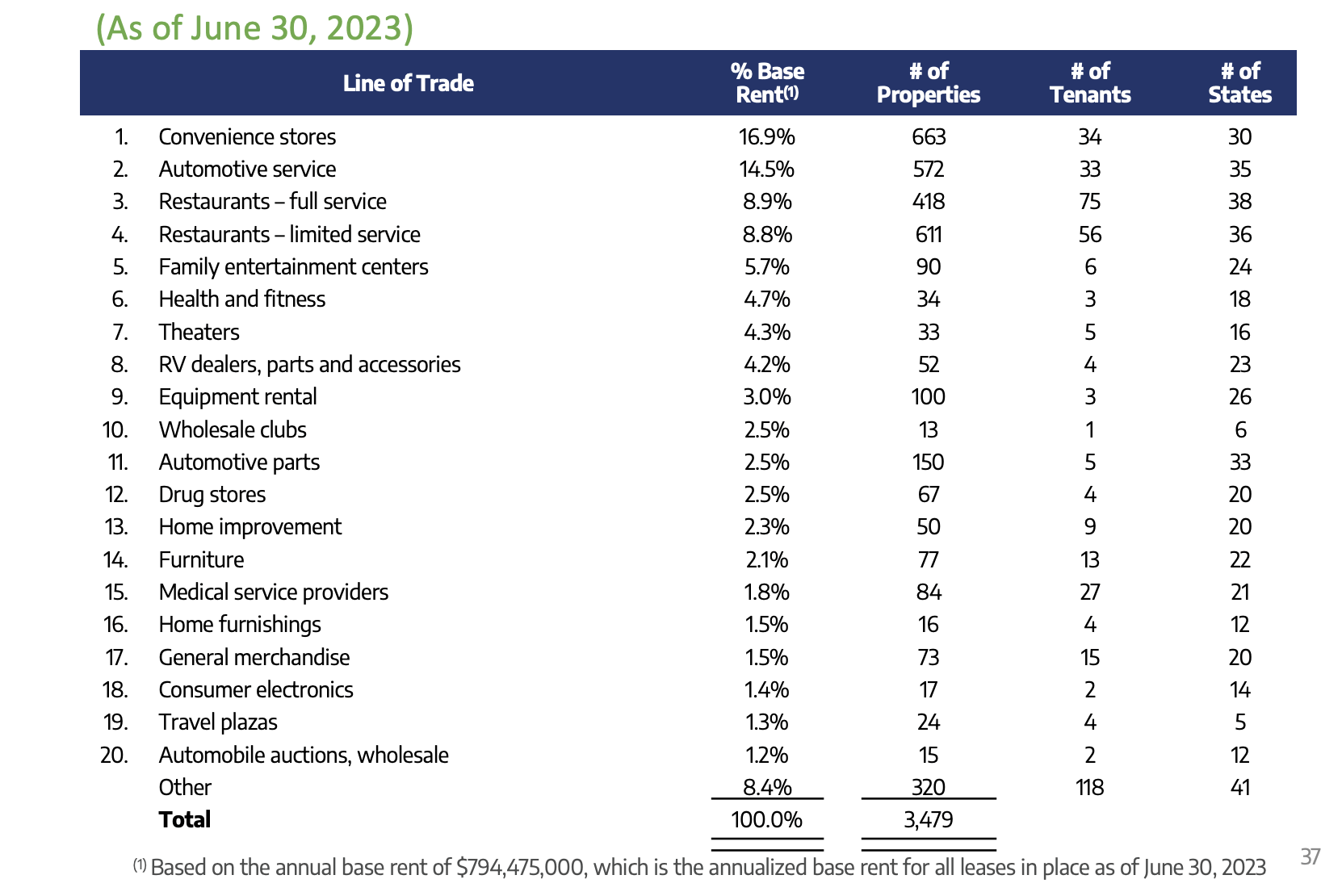

Looking at the overview below, the company has close to 3,500 properties. 17% of its base rent comes from convenience stores. 15% of its rent is generated through properties leased to automotive service companies. Restaurants account for close to 18% (combining limited and full-service restaurants).

{kind=link}

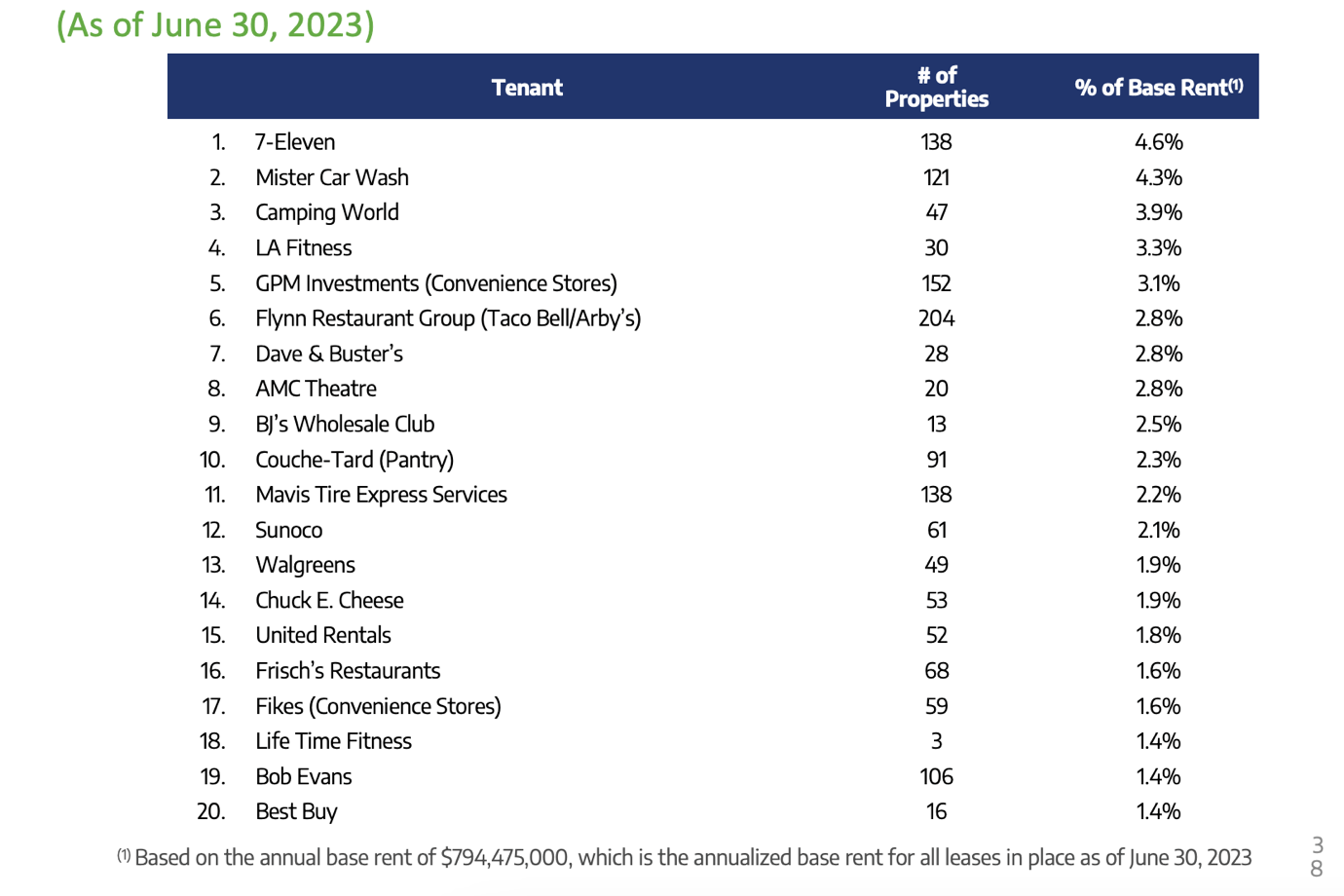

The company's top tenants include 7-Eleven, Mister Car Wash, Camping World, LA Fitness, investment groups owning convenience stores and fast-service restaurants, Dave & Buster's, and AMC Theatres. None of its tenants account for more than 4.6% of the annual base rent.

{kind=link}

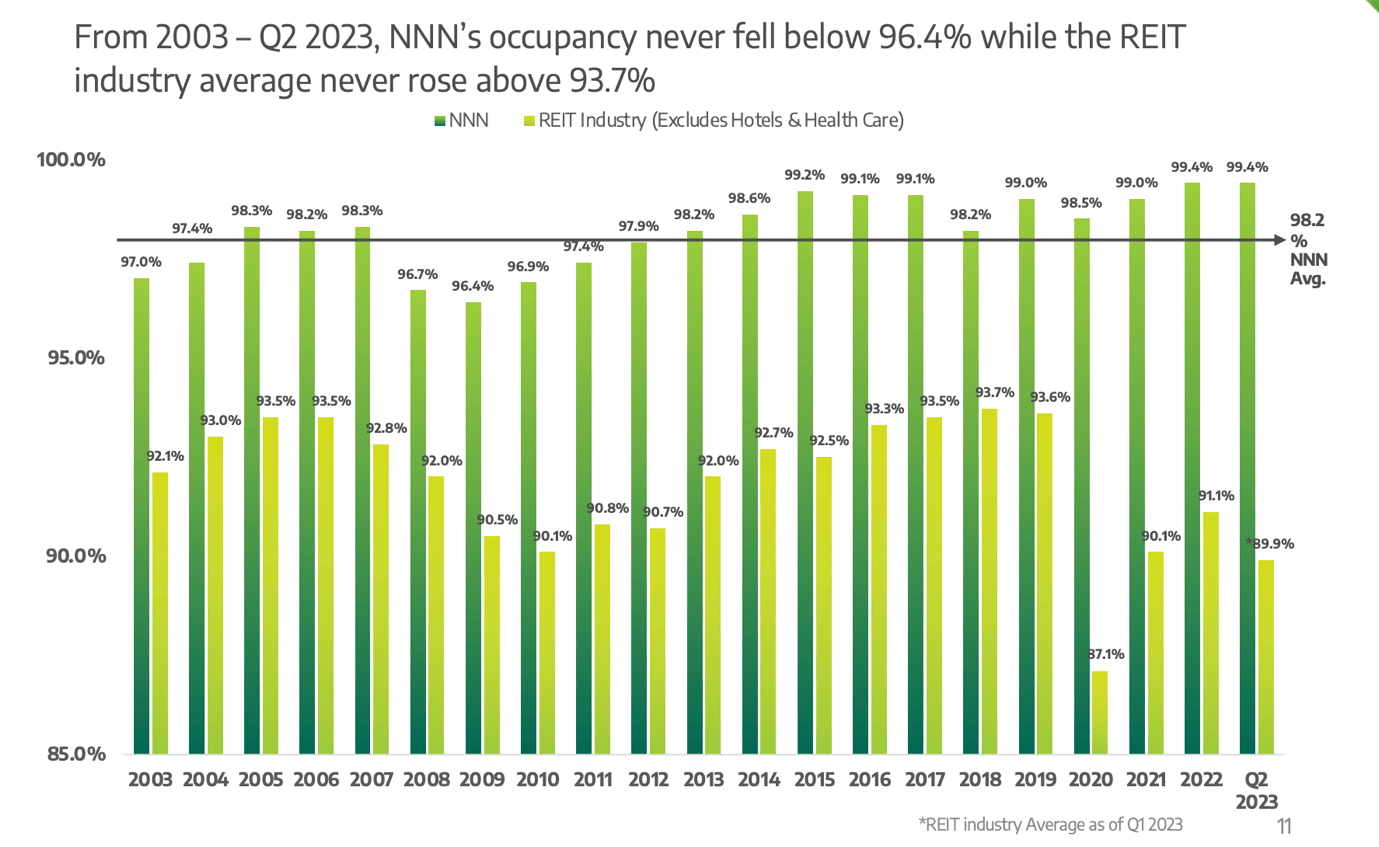

Thanks to its conservative profile, the company has consistently beaten the (adjusted) average REIT occupancy rates, and it did not even see a sub-96% occupancy rate during the Great Financial Crisis. The adjusted average REIT occupancy rate during that recession was 90.1%.

{kind=link}

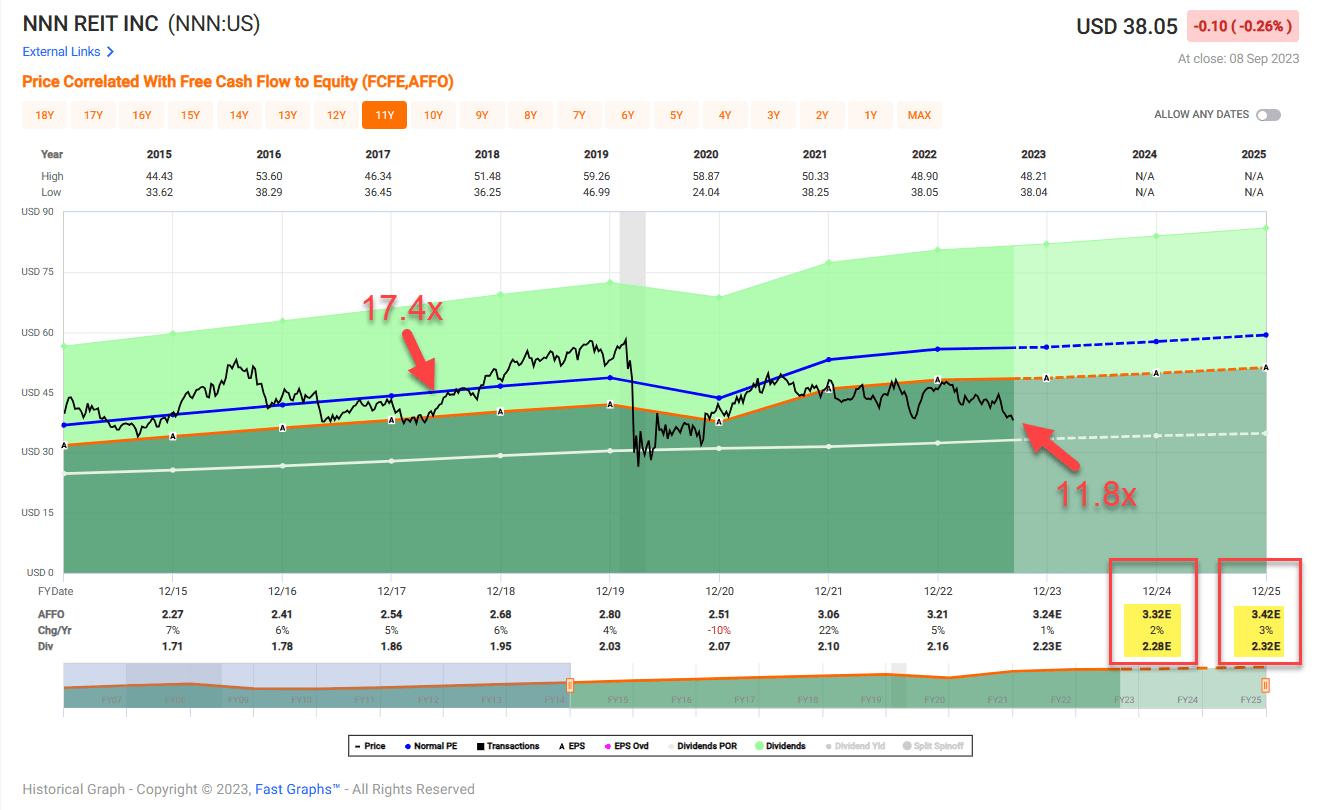

With regard to its valuation, NNN shares are down 17% year-to-date, as even the strongest players are getting punished.

The good news - and the reason we write articles like this one - is that this offers opportunities.

Not only is NNN yielding 6%, but it also trades at just 11.8x forward AFFO. The sector median is 14.2x.

It's not uncommon to encounter unreasonable valuations during unusual economic times. However, this valuation won't make sense on a long-term basis and makes NNN an attractive buy.

The current consensus price target is $46, which is 21% above the current price.

iREIT® has a Buy rating on NNN.

Again, none of these companies are immune against steep recessions. However, they offer attractive long-term value, are financially healthy, are unlikely to cut their dividend, and are likely to maintain long-term dividend growth.

{kind=link}

Takeaway

In a turbulent real estate market, it's essential to focus on opportunities amid the chaos. While the commercial real estate sector faces challenges and uncertainty, three stocks stand out as promising investments.

- E x tra Space Storage is a top choice, with strong financials and a 5.1% yield. Despite recent headwinds, it boasts high occupancy rates and exposure to growth ma rkets, making it a resilient pick.

- Alexandria Real Estate operates in the office real estate sector but benefits from leasing to high-tech healthcare firms, offering stability in uncertain times. Its 4.3% yield and solid occupancy guidance make it an appealing option.

- NNN REIT provides safety and income with a 5.9% yield, a BBB+ credit rating, and an impressive dividend track record. Its conservative profile and attractive valuation make it an intriguing investment.

In these challenging times, these stocks offer potential for long-term value and consistent dividends. While no investment is immune to recessions, these choices are financially healthy and poised for growth.

Note: Brad Thomas is a Wall Street writer, which means he's not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: Written and distributed only to assist in research while providing a forum for second-level thinking.

For further details see:

Real Estate In Turmoil: 3 Top-Tier, High-Yielding REITs We're Buying