UBP - Real Estate Spreads Are Out Of Whack: How To Take Advantage

2023-04-17 17:41:49 ET

Summary

- Spreads often are the source of opportunity.

- When a spread is wider or narrower than its natural state, it may be a good time to buy or sell, respectively.

- Currently, spreads are out of whack and I intend to take full advantage.

The Opportunity

Individual property cap rates are substantially below implied cap rates of the REITs resulting in a favorable ~200 basis point spread in buying certain REITs. As spreads normalize, the mispriced REITs should generate significant outperformance.

Background Information To Understand The Opportunity

With real estate, everything is valued in cap rates. There are three distinctly different categories of cap rates and understanding the subtle differences is instrumental to knowing what to buy and when. These differences facilitate taking advantage of favorable spreads and avoiding unfavorable spreads.

Let me begin with some definitions and then show how this information directly translates to actionable decisions.

3 Different Cap Rates

There are three distinctly different cap rates in the real estate world.

- Property cap rate.

- Public company cap rate.

- Development cap rate.

For an individual property, the cap rate is the net operating income (NOI) divided by the purchase price. So, if a property generates $10 per year of net income after operating expenses and is being sold for $100, that would be a 10% cap rate.

Public company cap rates work in a similar way. Adding up all the property NOI and subtracting corporate level expenses gets the total company level NOI figure, which one can divide by the enterprise value (market cap + debt - cash) to get the cap rate of the company. Public company cap rates are often referred to as "implied cap rated" or essentially the cap rate that is implied by the market price.

Finally, a construction project has a cap rate as well, but it is more of an estimate because the revenue line is not yet a known figure. Otherwise, it is the same as the individual property, just with assumptions of stabilized NOI rather than an actual number.

Great, now that the definitions are out of the way, we can get to the headline topic of this article - Spreads.

Spreads

A spread, in this instance, is the difference between cap rates. At any given time, public companies will trade at different cap rates than individual properties, which trade at different cap rates than development projects.

If the individual property cap rate is X, the natural spreads are as follows:

- Public companies trade at X minus 50 basis points.

- Developments trade at X plus 250 basis points.

I refer to this as the natural spread because it is the economically rational spread to which the market should tend to gravitate.

Public companies should trade at a slightly lower cap rate than individual properties for two reasons:

- Greater liquidity.

- Portfolio premium.

With a portfolio of assets rather than a single asset the buyer gets diversification benefits and there is also substantially less paperwork in buying a portfolio of 1000 assets rather than 1000 individual assets.

Developments should trade at a substantially higher cap rate than an individual asset for three reasons:

- Risk in actually achieving the underwritten revenue stream.

- Uncertainty of the leasing environment at the time construction completes.

- Delayed reward: Cashflows on a new development will usually not start until 1 to 4 years after capital gets invested.

One could argue about the exact number of basis point premium for developments or how much lower public company cap rates should be, but the directionality is fairly straight forward from the qualitative reasoning above.

When Spreads Get Wonky

If spreads deviate too far from their natural levels, there is a good opportunity in playing the favorable side of the spread. Perhaps an example will bring clarity.

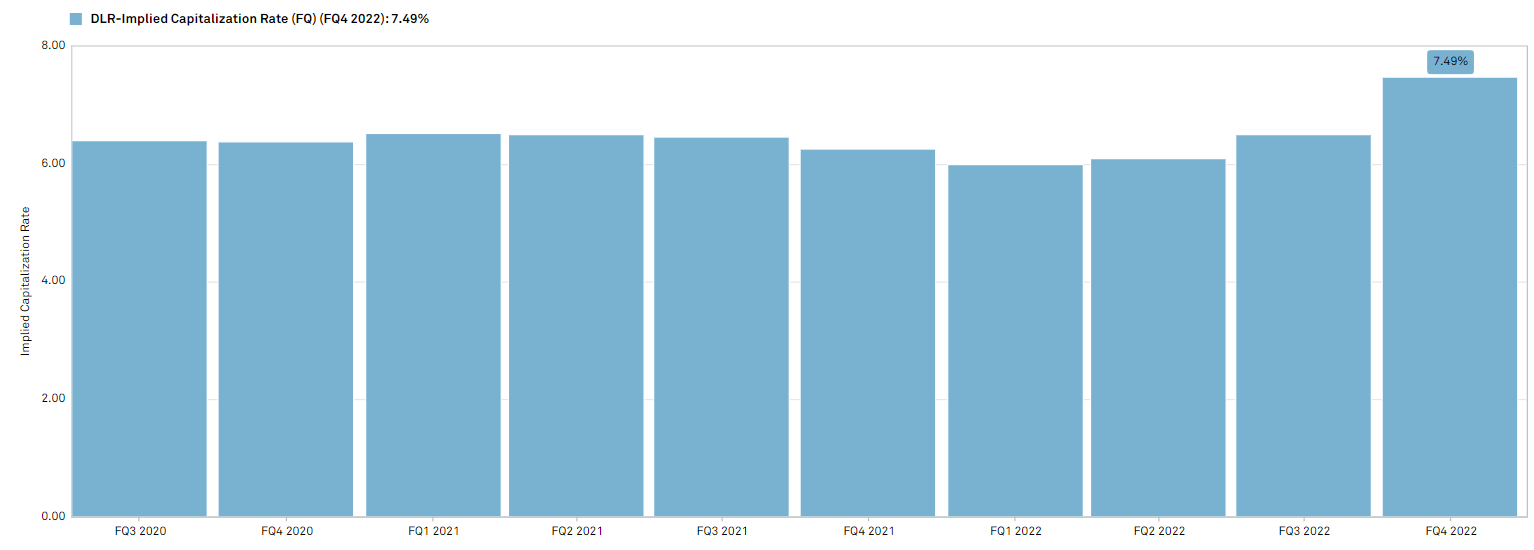

Spreads got out of line in the data center space as both private and public capital got excited about the asset type. A few years back, public market cap rates for things like Digital Realty ( DLR ) were around 6%.

{kind=link}

Individual property cap rates were somewhere in that same vicinity.

Development cap rates, however, were around 9%-11%. It was a nearly 5% spread for developers over existing properties.

With a 500 basis point spread compared to what is naturally more of a 250 basis point spread, development was extremely opportunistic. As a result, developers poured into the space. Start-ups like Switch (SWCH) developed rapidly at high cap rates and then sold the company at a low cap rate resulting in a significant gain.

Companies like Iron Mountain ( IRM ) that were not previously in the space could pour capital into data center developments and generate excellent returns.

These spreads are all relative to one another, so when one of the three types (individual property, public company, or development) gets opportunistic, the other types are probably not well positioned.

In other words, one should not buy an existing property at a 6 cap rate when that same property can be developed at an 11 cap rate.

The high development volume resulted in oversupply and rental rates for data centers have been trending down. Developers did well, existing owners suffered.

So, that is roughly the formula for taking advantage of wonky spreads - invest in the type that has the favorable spread.

Favorable Spreads Today

Spreads are once again out of whack, but this time in the opposite direction. There are opportunities across many sectors right now, but for the sake of brevity, we shall focus on retail.

Cap rates for individual triple net retail assets are around 6.05%

Boulder Group

Boulder Group's data comes from their transaction activity such as the sale below.

{kind=link}

They also frequently sell free standing fast food and convenience store locations.

These are the exact sort of properties that are in the triple net retail REITs so I would anticipate cap rates to be quite similar.

Thus, the REITs should trade at implied cap rates of about 5.50%-5.75% to account for the natural spread between portfolios and individual assets. Some of the REITs are indeed at this range.

- Agree Realty - 5.60% implied cap rate.

Agree ( ADC ) seems to be correctly priced. A couple other major retail triple net REITs are trading at slightly higher cap rates.

While I would normally see a public company at a 60 basis point favorable spread as highly opportunistic, I think there is a legitimate argument that cap rates are coming up given what the Fed has done. Thus, it is more-so that the individual property cap rate of 6.05% is too low rather than 6.65% being too high.

There are others, however, where the spread looks a bit too favorable to ignore.

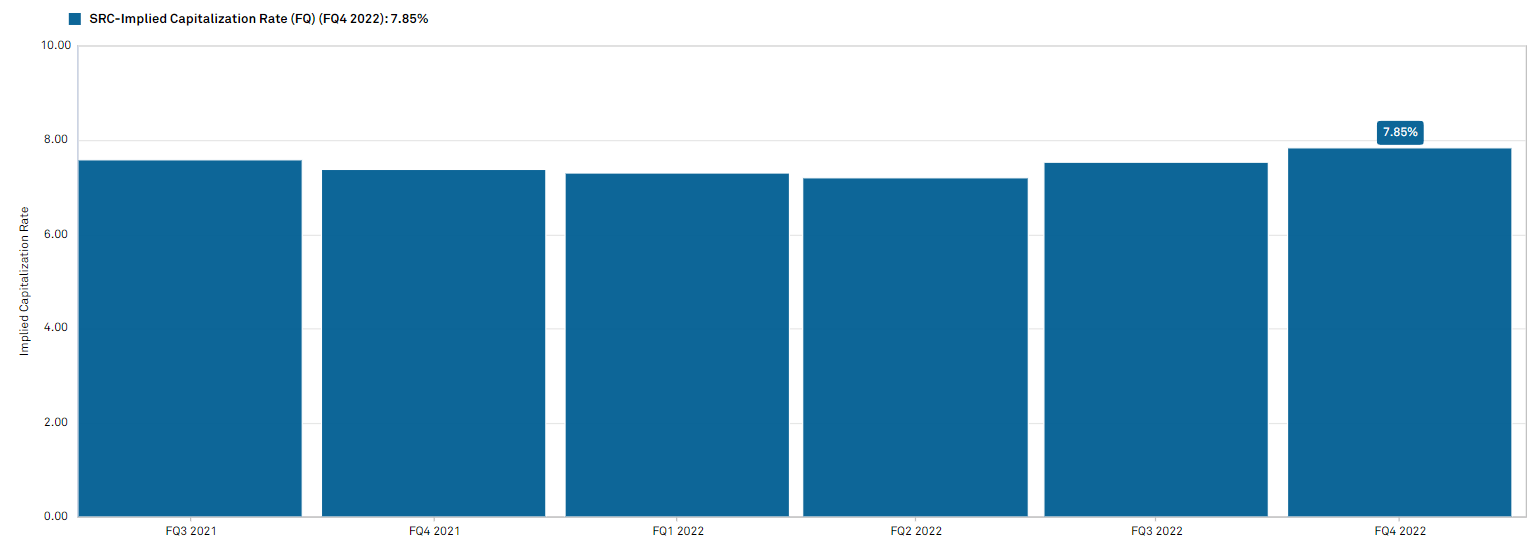

- Spirit Realty ( SRC ) - 7.85% implied cap rate

{kind=link}

SRC's assets are nearly identical to the ones Boulder Group is selling today at around 6.05% cap rates.

Either Boulder Group is the world's best-selling agent or SRC is opportunistic. Buying SRC nets one $120 of real estate for each $100 invested. The portfolio could be liquidated as individual properties and net shareholders a roughly 20% return.

Even Greater Opportunity In Grocery

Grocery anchored shopping centers are slightly different assets, but the individual property cap rate is in that same roughly 6% ballpark.

Fundamentally, I prefer this asset type as the grocery anchors are a seemingly permanent source of foot traffic that is driving strong rental rate growth. So, while triple net retail is getting around 2% annual lease rate growth, shopping centers are closer to 5% annual growth.

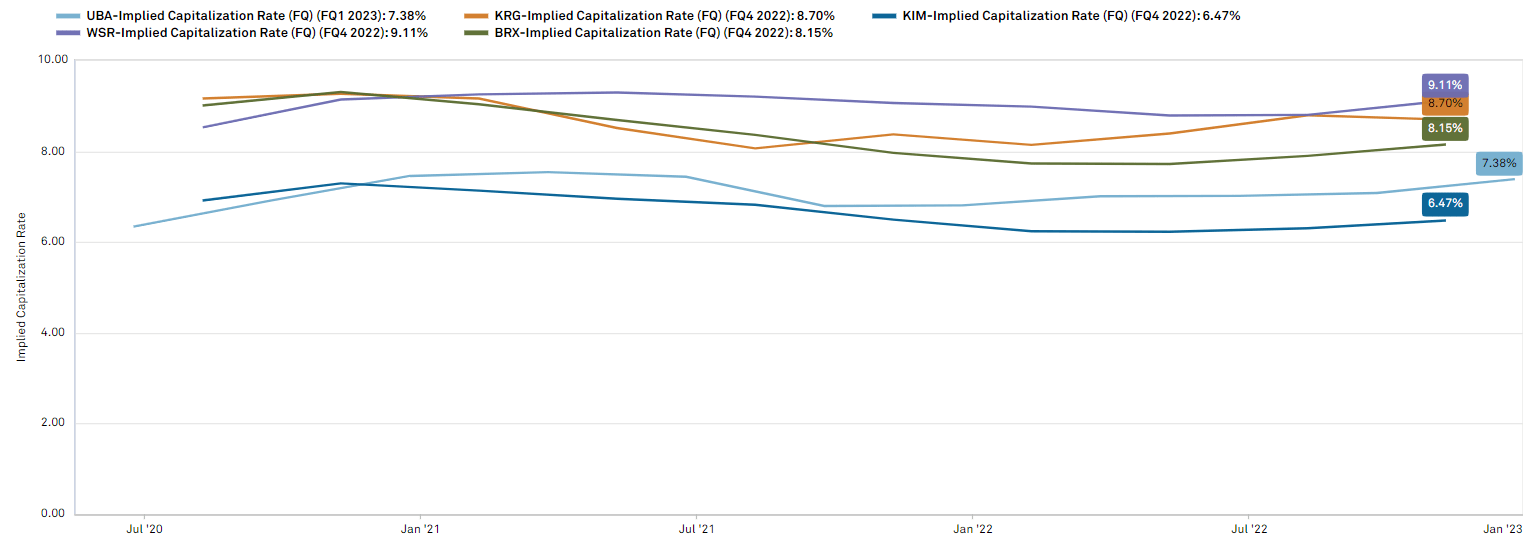

In this area, there is also a dispersion of valuation. Kimco ( KIM ) is trading at a 6.5% implied cap rate making it perhaps slightly cheap, but about right. Some of the others, however, are outrageously cheap.

- Urstadt Biddle ( UBA ) has a 7.38% implied cap rate

- Brixmor ( BRX ) has an 8.15% implied cap rate

- Kite Realty ( KRG ) trades at a 8.7% implied cap rate

- Whitestone ( WSR ) trades at a whopping 9.11% implied cap rate

{kind=link}

These spreads are completely backward to the natural levels, which creates an excellent opportunity to invest.

How Spreads Got Out Of Whack

The cap rates of the three different types of property pools respond to different market forces.

Development cap rates are driven by two things:

- NOI.

- Construction costs.

For retail, NOI has been fairly stagnant to slightly up over the past decade while construction costs have soared. As a result, construction has not been all that viable and there has been minimal new builds.

Individual property cap rates are driven by two things:

- NOI.

- The price private capital is willing to pay.

NOI has again, been fairly stable to slightly up while the price private investors are willing to pay has fluctuated with macro and fundamentals. Cap rates got down to the 5s during the low interest rate environment and then moved back up to around 6% as interest rates rose. In my estimation, the private market pricing has been largely correct.

Public REIT implied cap rates are driven by three things:

- NOI.

- Macro and fundamentals.

- Fear and greed.

The first two should have caused public REIT implied cap rates to move in parallel with individual asset cap rates with the REITs sitting around 0 to 50 basis points south of individual properties.

That largely happens through market history until periods of time in which fear or greed take over. Right now, it is a fear bonanza. Even as the retail REITs report 20% positive roll-ups on lease renewal the market is fleeing the sector.

It is not rational, but it does create opportunity.

In buying something like Brixmor, Whitestone, or Kite Realty at a roughly 8%-9% cap rate while the assets in their portfolio could be sold today for 6% cap rates investors are heavily advantaged. Buying properties at 70 cents on the dollar results in more NOI, higher dividends, and eventually a big capital gain when the company is either sold or trades back toward fair value.

The REITs Are Aware Of The Situation

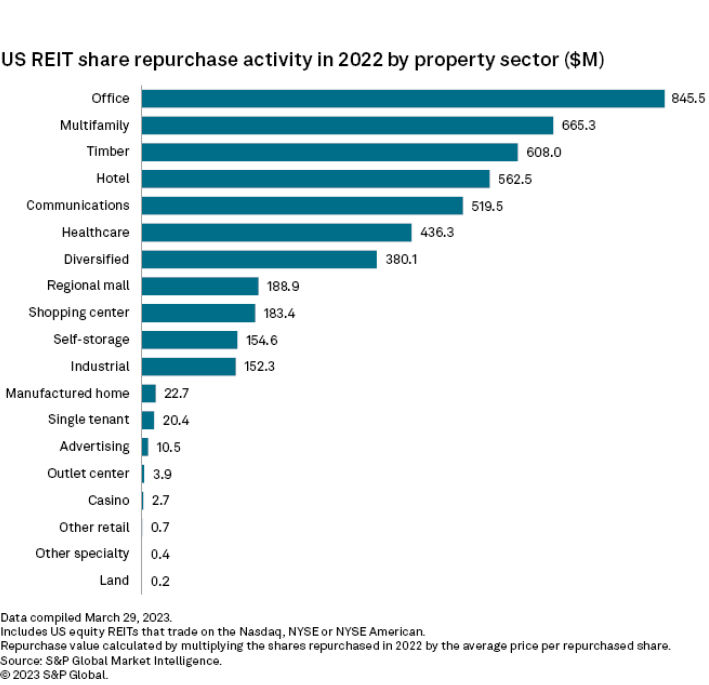

When a REIT is trading below fair value, it doesn't make sense to issue equity and buy properties. REITs are going the other way to take advantage of the mismatched pricing. They are selling properties at fair value and using the proceeds to buy back stock at below fair value.

Share buybacks among REITs are way up and the repurchase activity is greatest in areas where there is the largest disconnect between public REIT valuations and individual asset valuations.

{kind=link}

REITs tend to know the value of their own properties. When a sector known for perpetually issuing equity stops issuing equity and instead buys back shares, it might just be a clear opportunity.

For further details see:

Real Estate Spreads Are Out Of Whack: How To Take Advantage