SPG - Realty Income: 4.9% Dividend Yield But Valuation Is Not Favorable

2023-04-12 19:02:07 ET

Summary

- Realty Income Corporation reported dividend growth from $0.90 in FY1994 to $2.96 in FY2022, resulting in CAGR of 4.31% - and inclusion of Walgreens Boots Alliance, Inc. could help to maintain this growth.

- The company currently pays a 4.9% dividend, which exceeds the 5-year average dividend yield.

- After comparing the forward P/FFO ratio of Realty Income with the sector median of 12.53x and average industry P/FFO of 13.34x, I think the REIT is overvalued.

Investment Thesis

Realty Income Corporation ( O ) is a real estate investment trust ("REIT") that acquires and maintains standalone commercial buildings. The company has a long and consistent dividend growth record since 1994, when it went public (and since 1969 when it originated), and I believe it can sustain this growth in the coming years.

There are several growth factors that can contribute to increasing Realty Income's cash flow. And, the company's relatively high dividend yield should make it an attractive stock for risk-averse and yield-hungry investors.

About Realty Income

Realty Income Corporation is one of the top five global real estate investment trusts that acquires and maintains standalone commercial buildings that generate rental revenues through long-term net lease agreements. It owns over 12,200 properties in 84 different industries leased to over 1,240 clients. Its top seven operating regions include Texas, the United Kingdom, California, Illinois, Florida, Ohio, and Massachusetts. Each of the regions contributes 10.4%, 9.5%, 5.8%, 5.2%, 5.1%, 4.2%, and 4.2% , respectively, to the company's total portfolio annualized contractual rent.

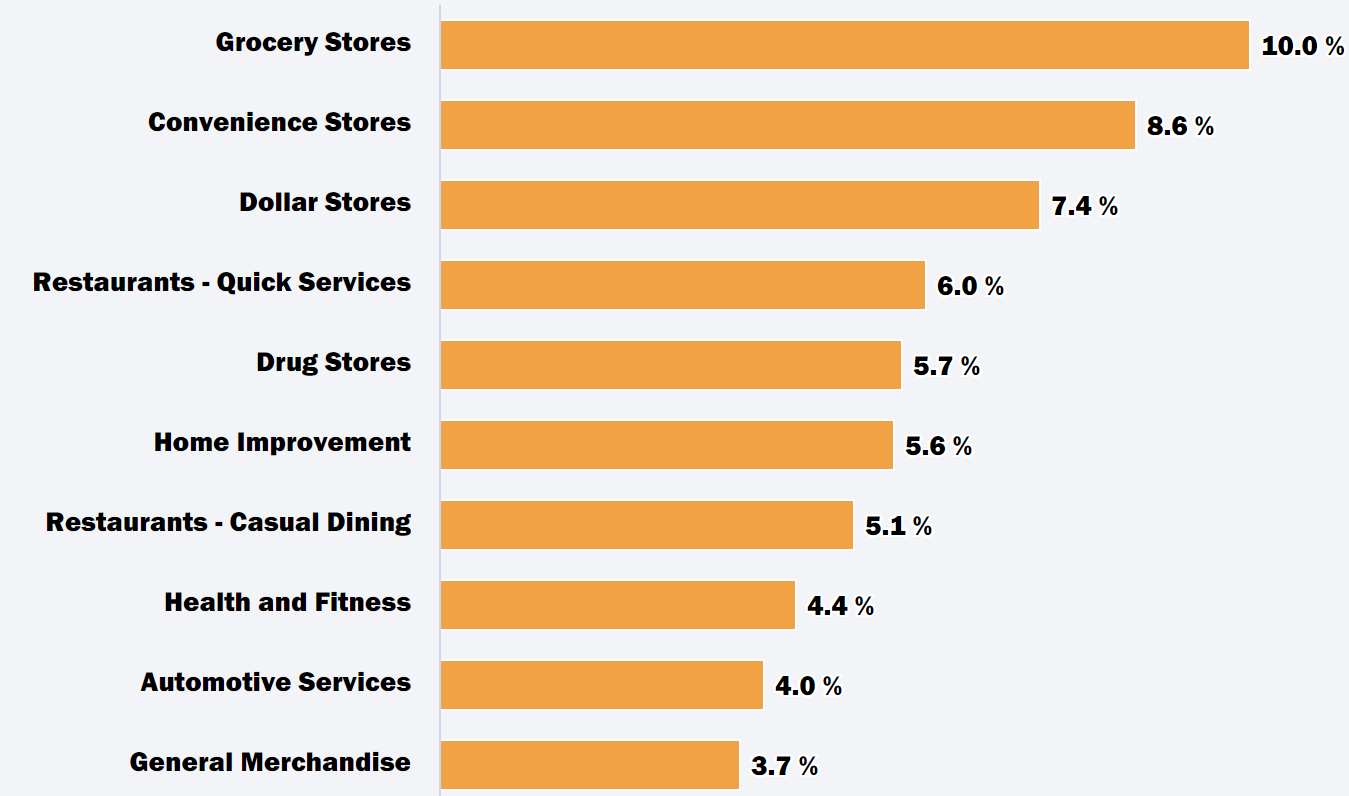

The company's property type is diversified into Industrial, Gaming, Retail, and other categories, representing 81.9%, 13.3%,2.9%, and 1.9% of its portfolio, respectively. The company mainly targets industry-leading clients from top industries and retail clients with non-discretionary or low-pricing points. It includes Drug stores, Dollar stores, Convenience stores, Grocery stores, and Quick-service Restaurants. In addition, it also focuses on other industries such as Home Improvement, Health & Fitness, Automotive services, and General Merchandise. Its client base includes well-performing industry leaders such as FedEx, Walgreens, CVS Pharmacy, Red Lobster, Dollar Tree, Sainsbury's, Walmart, Home Depot, 7-Eleven, etc.

Portfolio Classification of Realty Income (Website of Realty Income)

{kind=link}

High Growth Potential to Fuel Dividend Growth

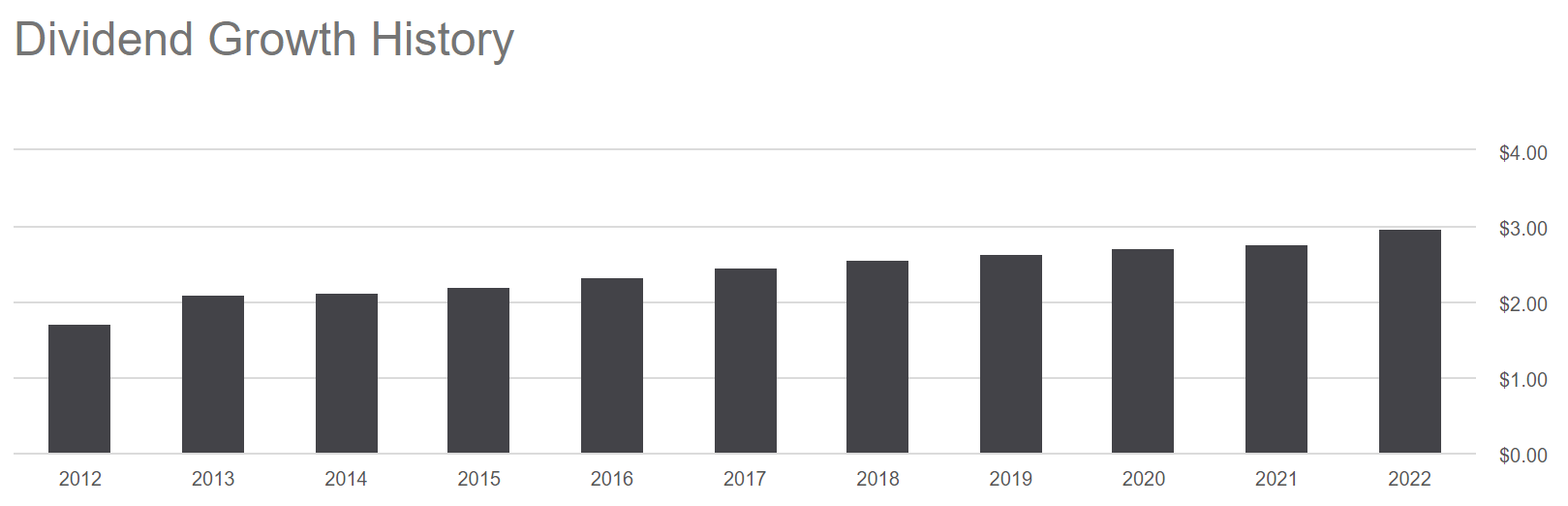

Dividend Growth History of Realty Income (Seeking Alpha)

{kind=link}

The company has an impressive and long track record of consistent dividend growth . As we can see in the above chart, the dividend payment of the company has increased steadily in the past. It has managed to maintain its dividend growth for 28 consecutive years and 101 quarters as a member of the S&P Dividends Aristocrats Index. The company has reported dividend growth from $0.90 in FY1994 to $2.96 in FY2022, resulting in a CAGR of 4.31%. In the previous year, the company distributed a total annual cash dividend of $2.96, representing a dividend yield of 4.77% compared to the current share price. In the current year, it distributed monthly dividends of $0.2485, $0.2545, and $0.2550 in January, February, and March, respectively, raising the dividend slightly as it often does.

I believe the company has the potential to sustain its dividend growth in the coming times, as there are several growth factors and competitive advantages which can improve its financial performance. It has a highly diversified portfolio in terms of regions, clients, and property type, ensuring the resiliency of its 92% rent from economic downturns. Its focuses on targeting Fortune 1000 investment-grade companies, which helps it to maintain its consistent growth. In addition, the company is highly dedicated to its expansion plans, which has significantly increased its acquisition volume to $9 billion in FY2022. The company has successfully leveraged its bulk buying capacity at wholesale rates, giving it a competitive edge over its peer companies. That was all about its competitive advantages, which can be considered to estimate its future growth.

Now, moving on to the external factors. Even though the company's portfolio is highly diversified, increasing operations in the Drug store sector can be a primary catalyst to boost its growth. The company has included Walgreens Boots Alliance, Inc. (WBA) in its client base, which covers approximately 50% of the retail prescription market share. Currently, Walgreen is planning to start nearly 1000 full-service doctor offices in the next four years, which can increase the company's occupancy level and further expand its profit margins.

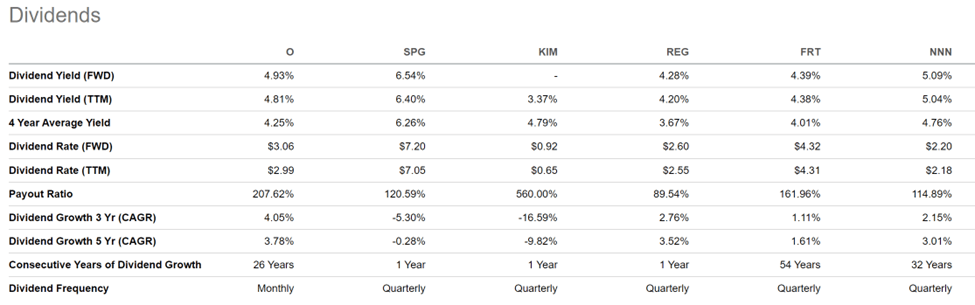

Peers Dividend Payment Details (Seeking Alpha)

{kind=link}

As per my analysis, these factors can significantly improve the company's cash flows and increase its dividend in the coming quarters. As shown on Seeking Alpha, the company's annual dividend payment will be $3.06, which represents 4.9% compared to the current share price. Realty income's 5-year average dividend yield is 4.33%. According to Seeking Alpha's estimates, the company can exceed its 5-year average dividend yield in FY2023.

Now, let's compare the estimated dividend yield with the industry average. The average industry dividend yield is 4.77%. After comparing the Seeking Alpha estimates with the industry average dividend yield, I think Realty Income Corporation can pay a higher dividend yield than its industry average.

Acquisition Volume (Investor Presentation: Slide No: 21)

Inflation and Rising Long-Term Debt

The company has reported 59.8% YoY rental income growth driven by rising inflation and the acquisition of 1300 properties in 2022. However, the rising inflation has also led to the significant growth of interest rates as central banks increase interest rates in an inflationary environment. In FY2022, the company reported an interest expense of $465.2 million, which is 43.7% YoY growth compared to the $323.6 million in FY2021. The company currently has $17.4 billion in long-term debt on its balance sheet , which is 42.3% of the current market capitalization.

As we know, the Federal Reserve is continuously increasing the interest rates to counter rising inflation. Currently, the Fed rates have increased to the levels of 4.75%-5% . Still, the inflation rose 6% in February. That is why I believe the interest rates might continue to increase in the coming months, as inflation is still very high compared to the average inflation rate of 3.8% .

Currently, the weighted-average rate of interest of Realty Income is 3.15% . I believe Realty Income's weighted-average rate of interest might grow in the coming months as the Fed continues to increase the interest rates. If inflation and interest continue to rise in the coming times, this could increase the financial cost to Realty Income and contract its margins.

Valuation

The company has various growth dynamics, which can significantly improve its financial performance and increase its cash flows. I believe Realty Income's diversified portfolio and inclusion of Walgreen in its client base can help the company to maintain its dividend growth and increase its funds from operations ("FFO"), as Walgreen is planning to start nearly 1000 full-service doctor offices in the next four years . According to Seeking Alpha, the company's FFO per share for FY2023 might be $4.00-$4.21, which is a growth of -0.1%-4.21%. After considering all the growth factors, I think that the growth of 4.21% is accurate. That is why I am estimating FFO per share of $4.21 for FY2023, which gives the forward P/FFO per share ratio of 14.75x. After comparing the forward P/FFO ratio of 14.75x with the sector median of 12.53x, I think the company is overvalued at current price levels as per the P/FFO valuation method.

I am selecting Simon Property Group ( SPG ), Kimco Realty Corporation ( KIM ), Regency Centers Corporation ( REG ), Federal Realty Investment Trust ( FRT ), and National Retail Properties ( NNN ) for a peer comparison as all of them have more than 40% long-term debt-to-capital ratio and low volatility. Due to similar long-term debt-to-capital ratios and low volatility, all of them might experience similar impacts of rising inflation and interest rates.

Currently, SPG, KIM, REG, FRT, and NNN are trading at forward P/FFO ratios of 9.23x, 12.32x, 14.98x, 15.21x, and 13.56x, while Realty Income is currently trading at a forward P/FFO ratio of 14.75x. This shows that the company is trading 10.6% above its average industry P/FFO ratio of 13.34x. However, Realty Income's 3-Year average P/FFO ratio is 18.88x, which indicates that the company is trading 21% below its 3-year average P/FFO ratio. But, I believe that the company might fail to gain momentum in the coming period due to rising inflation and interest rate and keep trading below its 3-year average P/FFO ratio, as the rising inflation and interest rates can increase the operating and financial cost of the company.

Every piece of negative news of inflation and interest rates can put negative pressure on the share price, and I believe the interest rates might keep increasing as the inflation is still high compared to historical levels. That's why we can conclude that Realty Income Corporation is overvalued as per the P/FFO valuation method.

Conclusion

Realty Income Corporation is an S&P 500 (SP500) company mainly known for monthly dividend payments. The company has a long track of consistent dividend pay-outs, which I believe it can sustain for a longer period as it has several competitive advantages and there are favorable industry dynamics that can fuel its financial performance. The company will pay investors a tasty dividend yield of 4.9% compared to the current share price.

However, rising inflation and interest rates could adversely affect Realty Income Corporation profit margins. The company is currently trading above its sector median and average industry P/FFO ratio. However, Realty Income is trading 21% below its 3-year average P/FFO ratio. But, I believe that the company might fail to gain momentum in the coming period due to rising inflation and interest rate and keep trading below its 3-year average P/FFO ratio.

Therefore, as per my analysis, Realty Income Corporation is overvalued according to the P/FFO valuation method. I think the relatively high dividend yield cannot justify the overvalued share price for new investors. Therefore, after considering all these factors, I assign a sell rating for Realty Income Corporation.

For further details see:

Realty Income: 4.9% Dividend Yield But Valuation Is Not Favorable