ONL - Realty Income: A Bastion In The Barren REIT Landscape

2023-04-24 17:10:51 ET

Summary

- Realty Income has a strong balance sheet and is looking rather cheap these days as REITs overall take a hit.

- O has provided growing dividends that are paid monthly for 26 years, and that's firmly expected going forward.

- We also share how we've been writing puts to potentially make our position even larger at an even better price.

Written by Nick Ackerman. This was included in our options expiration recap article over the weekend, originally posted for members of Cash Builder Opportunities.

It has been a little while since we've given Realty Income ( O ) a deeper look. For the most part, it's a highly popular stock that gets covered by many different analysts and sources. Therefore, I don't generally have anything to add specifically that hasn't been written about ad nauseam. Still, we can take a quick look at the latest outlook for Realty Income and the valuation of this REIT.

We wrote to our subscribers back on March 23 and highlighted how there is "more than one way to produce 'income'" when we were recapping our previous options trades. We recommended selling puts at the time and it served as another extension of that playing out while we simultaneously remain long the position. We will elaborate on that more later.

The Current Environment For O And REITs Overall

I believe that shares of O are cheap, even at the current levels and despite the headwinds for REITs.

One of the reasons that REITs have been the worst performing sector now in the last year, by a fairly wide margin, and even over the last three years, is due to higher interest rates. They carry risks as borrowing costs rise and financing growth becomes more expensive. Some REITs carry the risk of having higher levels of floating rate debt, which means even without adding new financing, they are going to see debt costs rise.

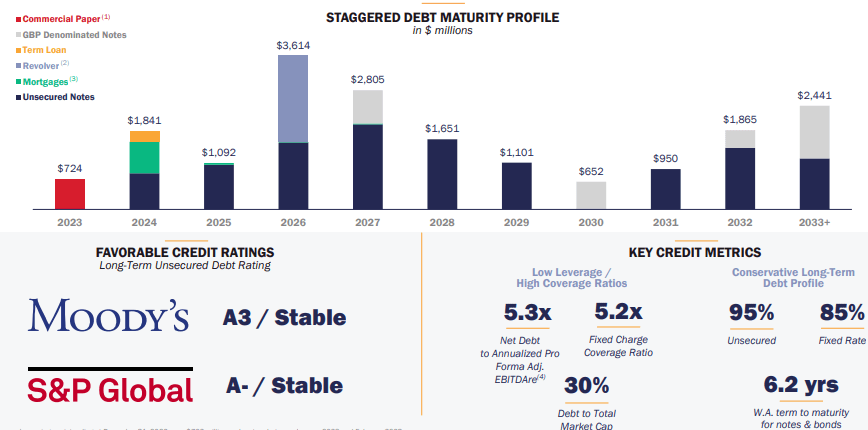

Fortunately for O, we see debt maturities that are spread out over the coming years, with no particularly heavy debt due for several years. 85% of the debt is also fixed rate, meaning only a relatively minimal portion is subject to the higher interest rates.

{kind=link}

O Debt Maturity Profile (Realty Income)

They've also continued to remain on top of the debt situation, making several moves to benefit the company over the longer term. They highlighted this in their latest earnings call .

In January, we executed a dual tranche $1.1 billion senior unsecured bond offering. The offering consisted of $500 million three year notes callable after one year and $600 million of seven-year notes. In conjunction with the three-year note, we capitalized on an attractive window to swap our interest payments from a fixed to variable rate structure, which we expect will replace a portion of our existing variable rate exposure in the capital stack.

After giving effect to the interest rate swap, we effectively locked in a variable rate spread of negative 3.5 basis points to SOFR, which represents estimated savings compared to our credit facility of over 85 basis points. It is important to note that the $500 million of variable rate exposure is expected to be in lieu of variable rate borrowings we would otherwise have outstanding on our revolver or on our commercial paper program.

Lastly, in January, we closed on a new $1 billion multicurrency unsecured term loan with an initial tenor of one year and with two 12-month extension options. In conjunction with closing of the term loan, we entered into a variable to fixed-rate swap resulting in an all-in effective yield of 5%.

Since O is investment-grade themselves, they can often get relatively favorable rates for their leverage. That puts them in a more favorable position than their REIT competitors.

They also just raised even more in senior unsecured notes through another dual- tranche offering in early April . In the next earnings coming up, the debt discussion will be one that we should continue to watch.

Additionally, REITs are seen as income investments. When you can get Treasuries at 4-5% now, that can make some REITs less appealing as a source for income. With fewer investors pushing up the share price of REITs, that means issuing equity also becomes less lucrative than it had been in the past.

In the chart below, we can clearly see an inverse relationship in the last year, where the 10-Year U.S. Treasury rose and sunk REITs overall. However, O has been able to keep from dropping as low as REIT peers.

Ycharts

Then a third impact of higher rates that can wreak havoc is simply the pressure on the underlying tenants. We expect rents to keep flowing in; when the economy gets tough or less than ideal, tenants, in terms of their own leverage costs, start experiencing higher interest expenses themselves. That can start eating into their tenants' cash flows. That can make some operations nonviable going forward, causing closures or bankruptcies.

While most properties can be renovated and converted to accommodate new tenants, it still adds to the uncertainty. Less business in operation also means less competition for space available. That goes back to the fundamentals of supply and demand. If there is less demand while supply stays stagnant or even grows due to new development, that could put pressure on rents in a recession.

However, this, too, is where O can shine. Their top tenants are considered investment-grade and remain relatively in demand even during a recession. The tenants listed with orange bars are investment-grade. Overall, 40.9% of the total portfolio annualized contractual rents were derived from investment-grade clients. These are also mostly large national brands, not some mom and pops that can be more sensitive to economic conditions.

O Top Tenants (Realty Income (investment-grade tenants are highlighted with an orange bar))

The industry breakdown has 10% of their portfolio in grocery stores, then another 8.6% in convenience stores. These are places that remain rather resilient in a weaker economy. Additionally, we have 7.4% in dollar stores that can actually benefit from a weaker economy as consumers look for cheaper alternatives.

O Industry Diversification (Realty Income)

This diversification amongst industries means that not every company will get hit as badly during a slow economy as others. Therefore, it's not as if the companies that are below investment grade will suddenly cease operations immediately due to a slowdown.

Attractive Valuation

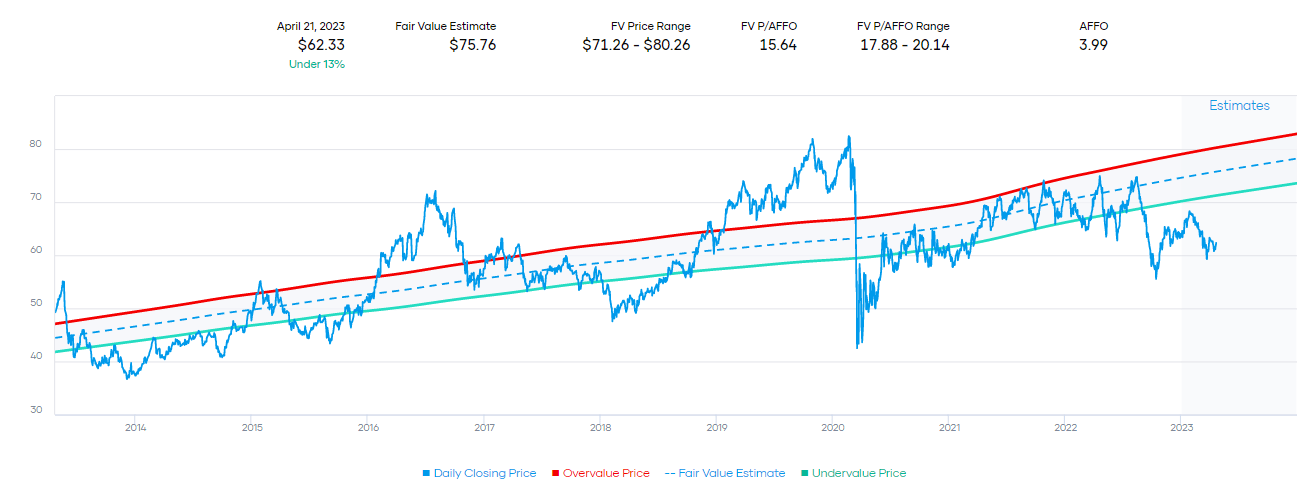

Looking at the fair value estimate based on the historical P/AFFO of the last decade, we can see that O is incredibly cheap.

{kind=link}

O Fair Value Estimate Based on Ten Year Range (Portfolio Insight)

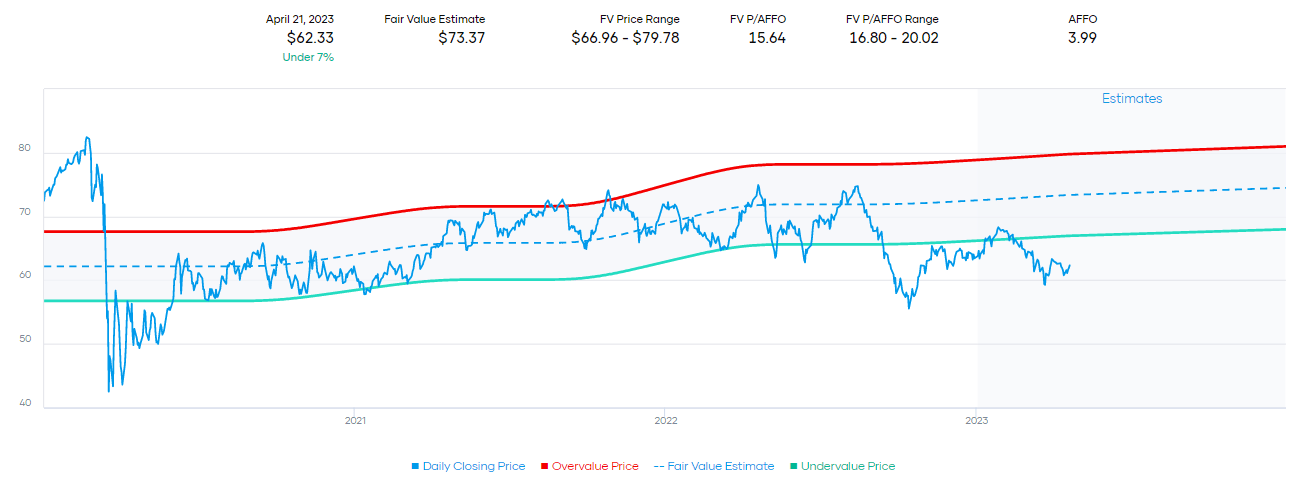

However, some of this is to be expected due to the factors laid out above and the pressures of higher interest rates. While the low $70s to $80s were previously probably an acceptable range based on its historical valuation in the last decade, in more recent years, this would have come down. The chart below shows the fair value range for the last three years, which could still be slightly elevated due to strength in 2021 when rates were at 0%.

{kind=link}

O Fair Value Estimate Based on Last Three Year Range (Portfolio Insight)

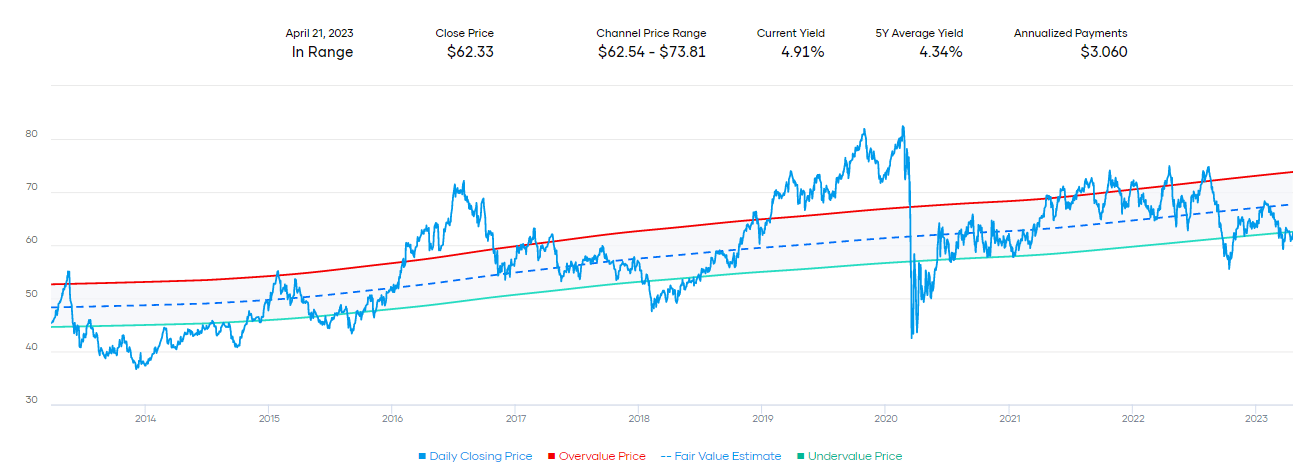

Therefore, while I believe that O is cheap, the fair value could be closer to around the $65 to $70 range. That is quite close to the fair value range provided when looking at O's dividend yield.

{kind=link}

O Fair Value Based on Yield (Portfolio Insight)

Fortunately, for a longer-term investor trying to get the absolute low here isn't necessary to provide longer-term results. O is still expected to grow in the coming years, slowly but surely.

{kind=link}

O AFFO History and Forward Estimates (Portfolio Insight)

However, with minimal growth going forward compared to the past, we could also expect the dividend growth to slow. O has never really been one to grow incredibly fast in terms of its dividend, but more steady and long-term growth.

Where that can change is if they make some large acquisitions that are accretive to earnings. Around the time they closed on their VEREIT acquisition , we actually saw a slightly larger than usual increase in the dividend after that. That was even after they spun off the office portion into Orion Office REIT ( ONL ).

{kind=link}

O Dividend History (Seeking Alpha)

You Have 'Options'

O has been treating us very well, too, in terms of writing puts to make our position larger at an even better price potentially. We've had several trades expire worthless while also keeping a long position. This latest trade was entered into on March 23, 2023.

We went with the $57.50 strike price while shares hovered near $60 at the time. I think that O under $60 is really attractive, so this is a case where I was actually being even more conservative. Had we been assigned, the breakeven due to the premium collected would have been $56.86.

Shortly after entering our trade, shares rose along with the rest of the market once the banking crisis started to wind down. While the dust might not have been completely settled, it at least started to become clear that public and private entities were stepping in to put a stop to collapsing banks.

Ycharts

Following that initial surge, shares sort of just languished and limped along. But, for selling puts, that doesn't matter. It only matters whether the share price is above or below the strike price come expiration. In this case, we netted the entire $0.64 in premium over the course of 29 days for a PAR of 14.01%. That works out to roughly 2.5x the monthly dividend.

Conclusion

O remains a long-term REIT that an investor can rely on for income going forward. They're positioned with a strong balance sheet, and an investment-grade rating allows them greater flexibility than some peers. While it isn't the most exciting investment available, that's part of its charm. To liven it up a bit, one can go to options writing in puts or covered calls to help potentially boost results.

REITs have been slammed with higher interest rates. However, Realty Income's rock-solid balance sheet, smart management and investment-grade credit rating remain a bastion to rely upon in this otherwise barren REIT landscape.

For further details see:

Realty Income: A Bastion In The Barren REIT Landscape