VNQ - Realty Income: A Huge Buy If The Fed Breaks The Market

Summary

- In this article, I start by assessing the health of the commercial real estate industry, which shows high resilience in the retail space.

- In light of the bigger picture, Realty Income Corporation continues what it does best: letting shareholders benefit from its tremendous stability and growth opportunities.

- Unfortunately, Realty Income's growth rates are weakening, making other investments more attractive in light of persistent inflation.

- Given the perceived risks associated with an overly aggressive Federal Reserve, I am of the opinion that Realty Income shares could present an appealing risk/reward proposition to shareholders, thereby offsetting potential risks associated with sluggish dividend growth.

Introduction

Realty Income Corporation ( O ) has garnered significant attention in the commercial real estate sector, particularly as the industry grapples with a series of economic challenges. In this article, I aim to provide an in-depth analysis of the company's performance in light of these economic woes. Specifically, we'll explore the headwinds facing the sector, including tighter lending conditions, high interest rates, and a high likelihood of Federal Reserve over-tightening. Despite these challenges, Realty Income's solid business model and strong balance sheet have allowed it to maintain its impressive performance.

Furthermore, the surprisingly strong commercial retail fundamentals in the face of these risks have also contributed to its success.

Additionally, I'll assess the company's dividend growth potential, given its recent inclusion in a number of model portfolios ( like this one ). Based on my analysis of the macroeconomic landscape and the company's specific strengths, I believe the stock represents an attractive investment opportunity, particularly during significant market corrections to improve the risk/reward.

Let's dive into the details!

Hiking Until Something Breaks

In most of my macro/market-focused articles, I mention that I expect the market to be stuck in a volatile sideways trend between the low-3,000 and mid-4,000 points range. This is based on my expectations that the Federal Reserve needs to do damage to the economy to hurt the underlying factors that keep inflation persistently high. The most prominent factor is a healthy labor market, which facilitates above-average wage growth.

Federal Reserve Bank of St. Louis

{kind=link}

So far, I have been proven right, as markets bounced off the higher end of my range. The reason was that market participants started to price in a more aggressive Fed. Why is that, you may ask? After all, we're beyond peak inflation.

The problem is that inflation is sticky. Very sticky. The Fed will have to put more pressure on the economy to get inflation to its target of 2%. Getting inflation from 8% to 6% is easy compared to getting it from 4% to 2%. Even trickier is keeping inflation at 2%. The Fed failed horribly in the 1970s, which it does not want to repeat.

Now, the market implies that there's a 70% chance that we could end this year with a Fed funds rate above 5.00%. Earlier this year, that probability was 0%.

CME Group

As if all of this isn't tricky enough, we're dealing with economic growth-slowing. While services remain somewhat strong, manufacturing sentiment has significantly weakened.

Federal Reserve Bank of Philadelphia

Hence, we're once again in a situation where the Fed is risking to break something. By breaking something, I mean hiking too much, which could trigger a bigger economic event that will eventually force the Fed to pivot.

Using Bank of America data, we see that the Fed has a track record of breaking stuff.

Bank of America

Needless to say, the aforementioned factors play a huge role in (commercial) real estate.

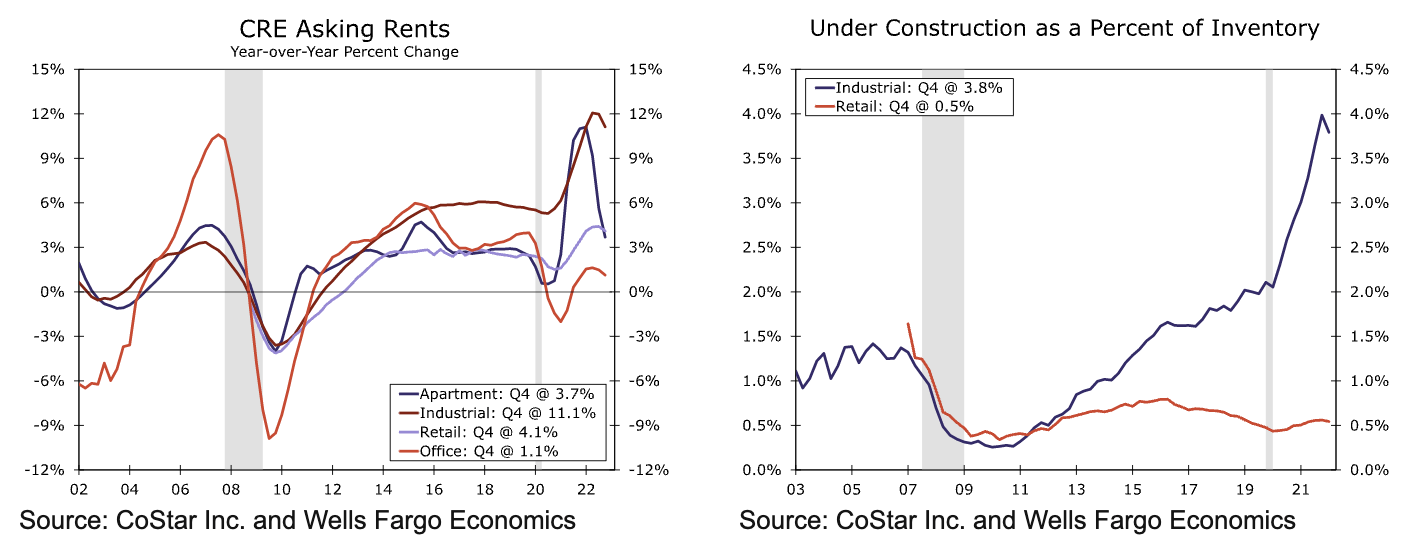

Commercial Real Estate Is Weakening

However, retail remains strong

Before I started writing this article, Wells Fargo & Company ( WFC ) came out with a report mentioning that the probability of a soft landing is increasing as a result of a robust labor market.

However, the bank also noted that pressure is starting to weigh on CRE (commercial real estate) activity. The good news is that weakness, so far, is limited and mainly visible in two areas:

- Apartments

- Offices.

Office vacancy rates have been an issue for a very long time. This problem started decades ago when offices were very tax-friendly investments. Also, nobody was betting on the big impact technology could have on remote work. Vacancy rates are now above 12%. Meanwhile, apartment vacancy rates are normalizing after falling off a cliff after the pandemic.

Wells Fargo

The good news is that retail is still doing well. Retail vacancy rates are dropping as demand is outpacing supply. The net absorption rate increased to 33.8 million square feet in the second half of 2022. Total completions came in at 15.2 million square feet.

Wells Fargo

Moreover, the vacancy rate of 4.2% in 4Q22 is the lowest on record (going back to 2007).

Rents improved by 4.1% in 4Q22, the second-best performance among major property types behind industrial.

According to Wells Fargo :

The low levels of new retail construction mean, even with a cooldown in rental demand from reduced consumer spending, retail vacancy rates are likely to remain low and support rent growth in the retail space over the next few years.

{kind=link}

So far, this is terrific news for retail, as it seems to withstand mounting headwinds.

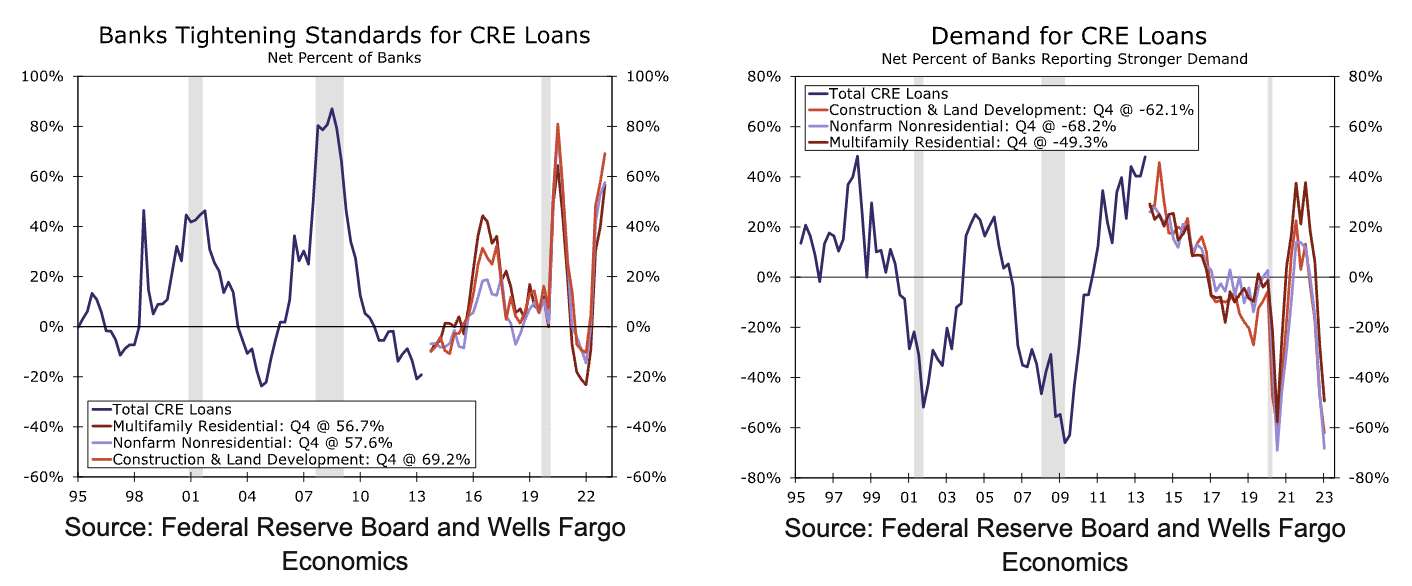

That said, I'm watching credit. One of the reasons why new supply growth is subdued is the fact that lending standards have been tightened at a pace similar to the Great Financial Crisis and pandemic peaks.

As a result, demand for new CRE loans has imploded.

{kind=link}

The good news is that these conditions will prevent new supply growth from accelerating. However, I do see risks in the poor health of the consumer. I believe that CRE risks for retail should not be underestimated - especially not if the Fed hikes higher for longer.

With that said, let's look into Realty Income, the star of this article.

Realty Income Means Safety & Reliable Income

On February 21, Realty Income reported its quarterly results . The company reported FFO (funds from operations) of $1.00 in its 4Q22 quarter. This beat estimates by a penny. Normalized FFO increased by 18.0% to $1.05. Total revenue in that period came in at $888.7 million, an improvement of 29.7% versus 4Q21. That number beat by $48.1 billion.

{kind=link}

Moreover, the company's guidance was strong. The company expects full-year FFO per share to be in the $4.01 to $4.13 range. The average analyst estimate was $4.09. Same-store rent is expected to grow by over 1.25%. The occupancy target is 98%.

The company ended the year with an occupancy rate of 99%, the highest occupancy rate at the end of a reporting period in more than 20 years!

This is part of the stability Realty Income brings to the table. According to Sumit Roy , President, and Chief Economic Officer:

At Realty Income, we strive to provide stability and sustainable growth on behalf of our investors. And during periods of economic uncertainty like we find ourselves in today, the resilience demonstrated by our business model is important to highlight. During our 28-year history as a public company, our combined total return consisting of AFFO per share growth and dividend payments generated by our operations has not experienced a single year of downside volatility in the form of negative total returns.

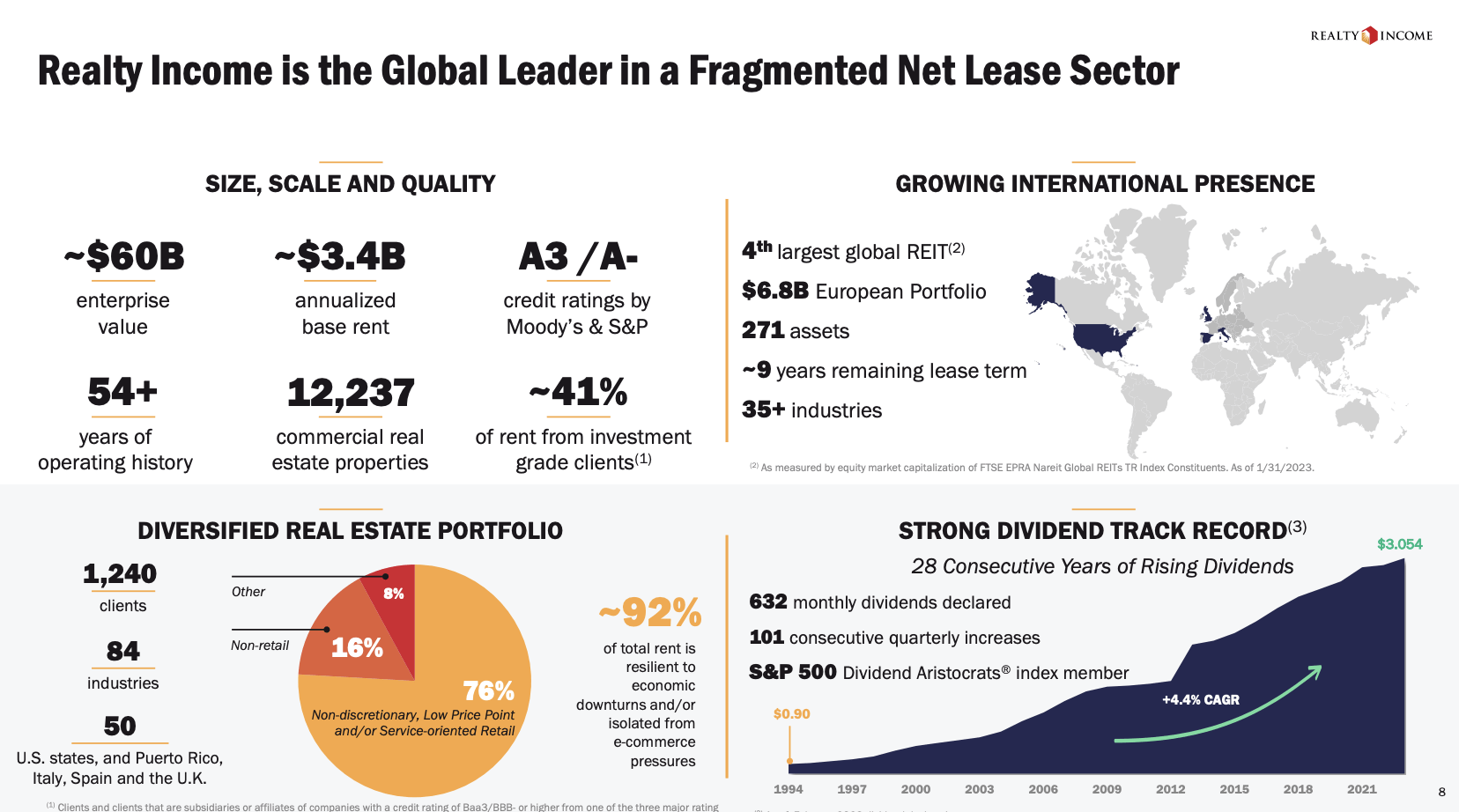

The company's stability is one of the core attributes investors have focused on for more than a decade. The company is one of the few real estate investment trusts ("REITs") with an A-rated balance sheet, has been in business for more than 54 years, owns more than 12,000 commercial properties, and has 28 consecutive years of rising dividends, making the stock a dividend aristocrat.

{kind=link}

Since going public in 1994, the company has returned 14.6% per year with a beta of 0.5 versus the S&P 500. In 26 of 27 years, the company has reported positive earnings per share growth.

The only issue the company is dealing with is the (pending) bankruptcy of Cineworld, which represents 1.4% of Realty Income's portfolio. Realty Income has collected 100% of contractual rent from Cineworld properties since October 2022. However, in an abundance of caution, the company recorded $13.7 million of additional reserves associated with nine Cineworld properties previously on accrual accounting in the fourth quarter.

Despite the bankruptcy, Realty Income believes that its portfolio of Cineworld assets generally outperformed the operator's portfolio and will provide an update on the outcome of negotiations when appropriate.

With that said, the company is investing in growth. The investment pipeline remains active, and they plan to invest over $5 billion in 2023.

Here are some areas the company is focused on:

- The company is looking to penetrate the healthcare REIT market. This market benefits from 7.2% annual (expected) growth in Medicare until at least 2030. This $2 trillion market also benefits from massive healthcare spending. Per-capita spending on healthcare is $13K per year in the US. That's twice the OECD average.

- The company agreed to fund up to $1 billion in development opportunities in vertical farming . This will be done through an alliance with vertical farming company Plenty Unlimited. Properties will be leased to Plenty under long-term lease agreements.

- The company is expanding in Europe . For example, the company now owns seven wholesale properties operated by the Metro Group for close to $170 million. As a European, I am familiar with Metro and believe the company is dealing with a terrific long-term tenant that brings both growth potential and stability.

- The fourth point is closely tied to the preceding ones and highlights the significant advantage that Realty Income enjoys from its sale-leaseback ("SLB") operations. Under this arrangement, companies in need of funding sell the properties they own, generating cash, and subsequently lease them back from Realty Income. This not only provides a steady stream of income for the company but also reduces the tenant's risk profile. In fact, tenants are more likely to improve their business with the proceeds from the real estate sale, making them less likely to default on their lease payments. Realty Income's healthy balance sheet provides it with the opportunity to offer attractive rates to potential SLB tenants, which makes it easier to grow in that area. After all, a company with bad credit would not be able to offer conditions to a potential SLB customer that beat finding funding via banks or other ways.

{kind=link}

With that said, dividend growth continued as well.

The company recently increased its monthly dividend by 2.4%, representing a 3.2% growth rate over the previous year.

Realty Income currently pays a $0.2545 dividend per share per month. This translates to a yield of 4.7%, which is very decent. The company is consistently yielding higher than the Vanguard Real Estate ETF ( VNQ ). Please note that the yield in the chart below has NOT been updated. The yield premium is roughly 100 basis points.

Moreover, the company has consistently outperformed this benchmark on a total return basis.

The company is truly the perfect mix of:

- A fantastic bullet-proof business model/portfolio.

- A healthy balance sheet with plenty of room to accelerate growth when others fight unfavorable financing conditions.

- An above-average dividend yield with slow but steady dividend growth.

- A decent outlook at a time when real estate markets are weakening.

- Long-term outperformance, which I expect to last.

One Problem, My Personal Opinion & Timing

With that said, there's one issue. Due to its maturity, the company's growth rates are slow. As fellow contributor Jussi Askola wrote earlier this week:

Realty Income's growth has slowed down even as inflation has shot up and as a result, it doesn't provide adequate protection against inflation anymore.

[...] Realty Income's contractual rent hikes are materially smaller than those of its high-quality peers. Moreover, its leases are also shorter, which increases the risk of vacancy and the need for capex. It also doesn't have periodic CPI adjustments in its leases, unlike WPC and VICI, and finally, it seems that it has more leases with some capex responsibility than its peers. Most of its leases are "triple net" with no capex responsibility, but it also has some "double nets", which typically put the responsibility of the roof/structure and/or the parking on the landlord.

Especially for income-focused investors, buying a stock that is unlikely to beat (expected) inflation with its dividend hikes is somewhat of a red flag.

The company's cash payout ratio is 66%. The sector median is 57%.

However, my opinion is that Realty Income is a much better investment than a lot of higher-yielding alternatives.

So, I believe there are two solutions.

- Buying REITs with faster growth rates. For example, I am focused on self-storage real estate. I have large positions in both Public Storage ( PSA ) and Extra Space Storage Inc. ( EXR ), which I am going to expand in the months ahead. These REITs are more volatile than O, yet they have higher dividend growth rates. They also outperform O on a long-term basis.

- Solution number two is what I often do when I like a company but not the risk/reward it currently presents: waiting for a better entry. Realty Income is currently trading at 15.7x 2023 FFO (I'm using the upper bound of its guidance here!). That is fair and in line with its net-lease peer group. It's a fair valuation. However, given my view on the Fed and the high likelihood that something breaks in the quarters ahead, I believe that we might be able to buy Realty Income at a better valuation.

If Realty Income were to offer a yield of more than 5.2%, I believe it would be a good investment, despite slow growth rates.

Even better, on weakness, I believe that O is one of the best investments in real estate.

Takeaway

In this article, we have explored one of the largest and most iconic real estate companies in the world, Realty Income. Despite facing economic challenges such as higher interest rates and poor consumer health in 2022, the company has managed to expand its business impressively. Furthermore, Realty Income is exploring new avenues for growth outside of traditional retail real estate.

Moreover, the retail real estate sector is performing well, with demand growth surpassing new supply, vacancy rates declining, and pricing opportunities remaining robust.

However, Realty Income Corporation's business model does not offer high growth potential. Income-oriented investors may face challenges as inflation is expected to outpace dividend growth.

Considering this, there are two alternatives available. One is investing in fast-growing REITs with decent yields, which could lead to higher volatility. Alternatively, I suggest another option based on my view that the Fed is in a precarious position. Given the macroeconomic conditions, it is likely that the Fed will continue to hike into economic weakness, potentially leading to severe economic consequences. Even Realty Income's stock, with its resilient business model and strong balance sheet, could be affected. If this happens, I would consider buying the stock during a dip, potentially resulting in an even better yield.

In conclusion, despite the challenges, I remain optimistic about Realty Income's future and consider it to be one of the best REITs available in the market.

For further details see:

Realty Income: A Huge Buy If The Fed Breaks The Market