SRC - Realty Income: Catch The Falling Knife Again? You Need An Exit Plan This Time

2023-11-04 08:30:00 ET

Summary

- Realty Income Corporation stock has declined even more as investors reacted to its $9.3 billion acquisition of Spirit Realty Capital.

- The company's deal seems attractive, as its AFFO per share accretive amid a reasonable valuation and expected cost synergies. Realty Income's assets are complementary to Spirit's.

- There are valid concerns over Spirit's debt maturities from 2025, which could add to headwinds on Realty Income's 2025 AFFO estimates.

- I assessed that the steep plunge in O's valuation is justified, given the surge in long-term bond yields. I also no longer expect O's 2023 highs to be retaken soon.

- I explain the key levels that investors must watch if they plan to catch the falling knife again. While still attractive, investors must consider an exit strategy to protect gains.

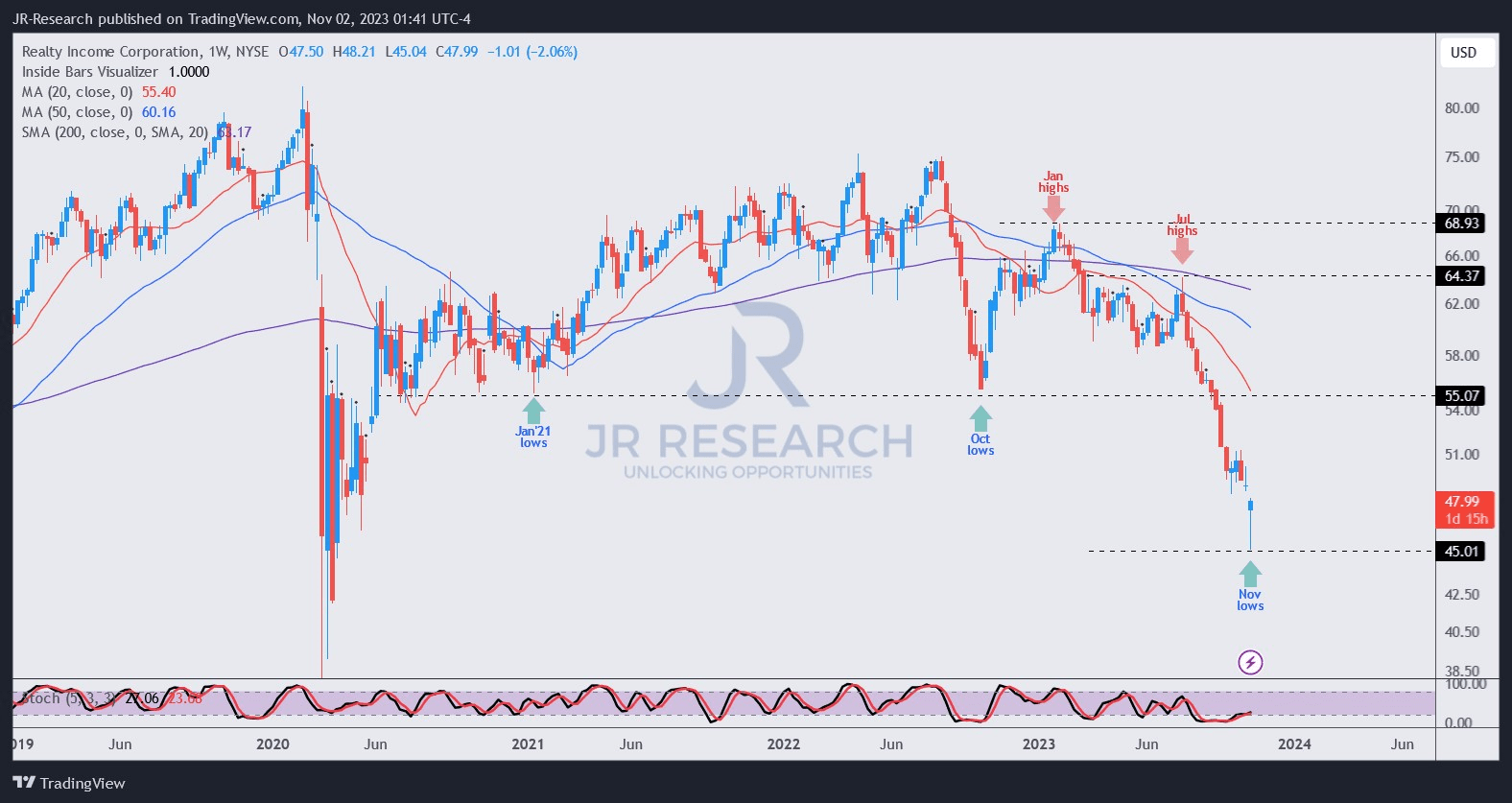

I last updated investors in Realty Income Corporation ( O ) in late August, as the leading retail REIT fell steeply, as investors priced in a higher-for-longer Fed policy. Buyers attempted to fight for O to bottom out in October but failed, as O fell further toward its lows this week.

Investors have correctly priced in higher bond yields, as the 10Y yield ( US10Y ) broke decisively above its August resistance levels, reaching above the 5% level two weeks ago. Last week's selloff culminated with Realty Income's mega $9.3B acquisition of smaller peer Spirit Realty Capital, Inc. ( SRC ). Realty Income expects the deal to close in the first quarter of 2024 and is expected to be accretive to AFFO per share with an increase of 2.5%.

As such, investors have been battling it out as dip-buyers returned this week, assessing the deal's benefits and contemplating the risks. I believe the growth risks to Realty Income's $9.3B deal are clear, as it needs to continue consummating external growth opportunities as organic growth slows. The deal's 2.5% expected accretion is considered conservative. Management highlighted that they telegraphed more prudent estimates, given the macroeconomic uncertainties.

Revised analysts' estimates suggest an AFFO per share growth of 3.7% in FY24, lifting its previous growth outlook of above 1%. As such, analysts remain cautiously optimistic, although questions persist over the momentum from 2025. Despite that, analysts' FY25 AFFO growth estimates of 3.1% suggest confidence in the deal's medium-term prospects, even as the interest rate environment could remain harsh.

I believe Realty Income's timing on the acquisitions seems to be the right one, given SRC's current valuation. While the market has tried to price in the implied takeover premium as SRC surged above $37 this week, its forward AFFO multiple of 9.9x remains below O's forward AFFO per share multiple of 11.7x. Management indicated that its estimated 2.5% AFFO per share accretion has accounted for the "differential" in their relative AFFO per share multiples.

As such, Realty Income seems to have bolstered its scale and market leadership in complementary assets with Spirit Realty Capital at a pretty reasonable valuation. Its ability to leverage its premium multiple in the all-stock offering should provide confidence to investors about its ability to maintain its leverage.

Despite that, there were some notable concerns raised by analysts on the call that behoove caution over Spirit Realty Capital's debt. Realty Income will take over $4.1B in debt with a weighted average cost of about 3.48% and an average term of 4.9 years. However, there are valid concerns over about $800M in maturity in 2025, adding to Realty Income's original $1.09B. In total, it represents about 7.6% of the company's consolidated debt base.

Management's commentary suggests the company isn't unduly concerned as there are no near-term maturities in Spirit's debt to deal with, "providing a favorable outlook for the next 12 months."

However, I believe the market needs to reflect medium-term refinancing risks on Spirit's long-term debt, as Realty Income's bond yields reached "mid-to-high 6%" recently. As such, unless we expect a structural downshift in interest rates over the next two years, I believe it's critical to assess increased refinancing risks, putting pressure on Realty Income's FY25 AFFO outlook. Also, while the Fed paused its rate hikes at the recent FOMC meeting, the committee remains open to further hikes if necessary.

Also, investors must reflect on increased execution risks as Realty Income integrates Spirit's business model into its underwriting process. Management indicated that "it is too early to determine whether Realty Income will incorporate practices from Spirit Realty's underwriting process." While Realty Income has substantial experience in this aspect and the assets' complementary profile, the hostile macro environment has reduced the teams' margin for error.

{kind=link}

There's little doubt that the steep decline in O since its July 2023 highs has spooked holders into fleeing, as it capitulated toward this week's lows ($45 level). The steep decline has opened up a mean-reversion opportunity for high-conviction investors believing in the earnings accretive profile of the Spirit deal.

I also assessed dip buyers have returned, although O has no bear trap (false downside breakdown) that could bolster its current levels. The failure by buyers to hold O's $55 level was consequential, as it led to a massive wave of technical selling over the past two months.

As such, my conviction of O recovering its 2023 highs in the near- to medium-term has significantly lowered. Despite that, I assessed the mean-reversion opportunity remains valid, but I suggest taking profits below the $55 zone. As such, the 20% potential upside is still reasonable if O can hold its current levels. Coupled with a dividend yield of 6.6%, the risk/reward profile remains attractive.

Rating: Maintain Buy.

Important note: Investors are reminded to do their due diligence and not rely on the information provided as financial advice. Please always apply independent thinking and note that the rating is not intended to time a specific entry/exit at the point of writing unless otherwise specified.

We Want To Hear From You

Have constructive commentary to improve our thesis? Spotted a critical gap in our view? Saw something important that we didn't? Agree or disagree? Comment below with the aim of helping everyone in the community to learn better!

For further details see:

Realty Income: Catch The Falling Knife Again? You Need An Exit Plan This Time