SRC - Realty Income: Firing On All Cylinders (Rating Upgrade)

2023-11-10 15:46:41 ET

Summary

- Realty Income Corporation reported better-than-expected Q3 earnings.

- The $9.3B acquisition of Spirit Realty Capital will diversify Realty Income's revenue streams and improve its overall diversification.

- The deal is expected to be accretive to AFFO, and Realty Income has raised its guidance for AFFO and NFFO.

- Realty Income shares are cheap at about 12X NFFO. Dividend investors get a 6.1% dividend yield here.

Realty Income Corporation ( O ) presented better-than-expected third quarter earnings this week, and the real estate investment trust ("REIT") also announced a major transaction at the end of October: Realty Income announced the acquisition of Spirit Realty Capital, Inc. ( SRC ) in a major, transformative $9.3B deal. The acquisition will help Realty Income diversify its revenue streams and generate less reliance on the retail portion of its real estate segment. Considering that: 1) The deal is expected to be accretive to adjusted funds from operations, or AFFO; 2) Shares just bounced back from their 1-year low; and 3) Realty Income raised its guidance for AFFO and normalized FFO, or NFFO, I believe the risk profile remains widely favorable for dividend investors!

Previous rating

I rated Realty Income a buy in September - "The Market Is Wrong, I Am Buying This 5.6% Yield Hand Over Fist" - because the REIT was performing well and its strong, underlying performance was not recognized by the market at the time. Since my last work on Realty Income, the REIT has announced a major $9.3B acquisition of a rival REIT, and Realty Income reported better-than-expected Q3 '23 earnings . Realty Income remains a top holding for dividend investors following the Q3 '23 report as well as the Spirit Realty Capital deal, and I am upgrading the REIT to strong buy!

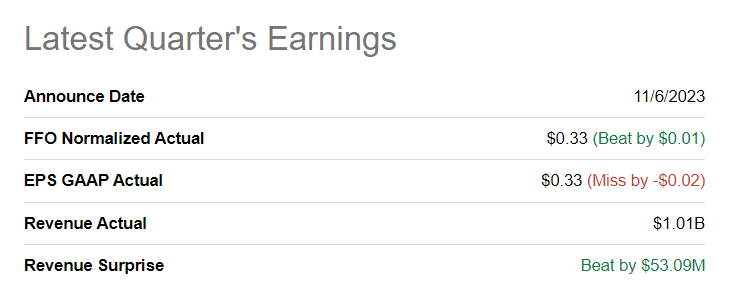

Better-than-expected Q3 earnings

Realty Income presented better-than-expected earnings for Q3 '23 with normalized FFO coming in at $0.33 per share, $0.01 above the consensus estimate.

{kind=link}

Why the Spirit Realty Capital acquisition is a big deal

In September, Spirit Realty Capital invested $950M into a transaction involving the Bellagio trophy property on the Las Vegas strip. The deal was done to strengthen Realty Income's gaming rental income streams and diversify the REIT's investment portfolio.

Realty Income's latest deal includes the acquisition of Spirit Realty Capital, a REIT that owns a large portfolio of retail and industrial properties. According to the deal terms, Spirit shareholders will receive 0.762 of a share of Realty Income, and they will own approximately 13% of the merged entity.

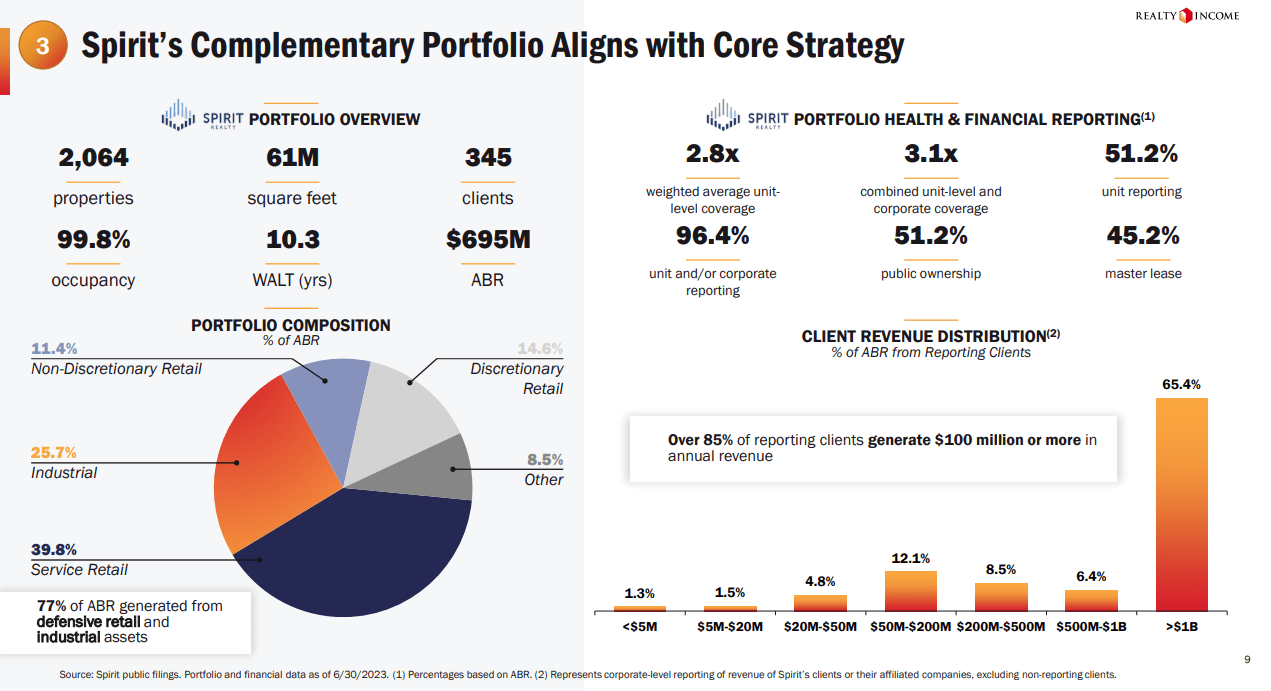

Spirit Realty Capital had 2,064 properties in its portfolio in the last quarter, the majority of which fell into the Service Retail and Industrial categories. In fact, more than three-quarters of Spirit Realty Capital's ABR (its annualized rental income) falls into defensive (recession-resistant) retail and industrial.

The lease metrics of Spirit Realty Capital also look very attractive, as the REIT had a 99.8% occupancy rate and a 10.3 weighted average lease term/WALT… which is higher than Realty Income's 9.6 weighted average lease term. Long lease terms are favorable, as they generate a high degree of cash flow visibility for landlords.

{kind=link}

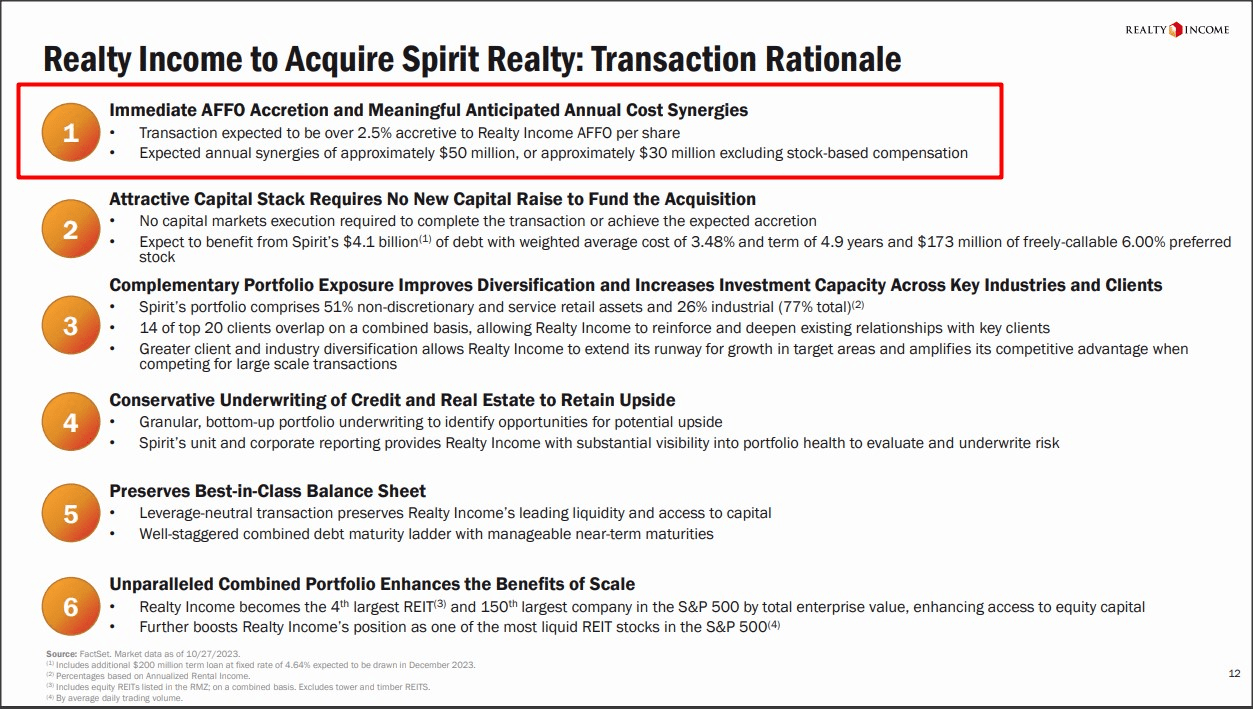

For Realty Income, the deal has a number of benefits, including improved diversification (the deal will increase Realty Income's industrial representation) and result in AFFO accretion. According to Realty Income, the combined portfolio will include 79.9% retail, 15.1% industrial, 2.2% gaming, and 2.8% other. The acquisition will boost Realty Income's industrial share, but lower the retail share, improving the REIT's total diversification.

Realty Income

The AFFO accretion, in my opinion, is possibly the biggest benefit of the Spirit Realty Capital acquisition, but there are others as well, including Realty Income being able to lower its expenses and gaining access to Spirit Realty Capital's low-cost debt:

{kind=link}

The dividend is well-supported by AFFO

While the Spirit Realty Capital deal gained a lot of attention, the commercial REIT performed just as well on a standalone basis. In the first nine months of FY 2023, Realty Income reported $2.99 per share in AFFO, showing 2.4% growth compared to the year-earlier period. In total, Realty Income distributed 76.4% of its AFFO to shareholders, which is about on the same level as the distribution percentage in the year-earlier period.

Realty Income

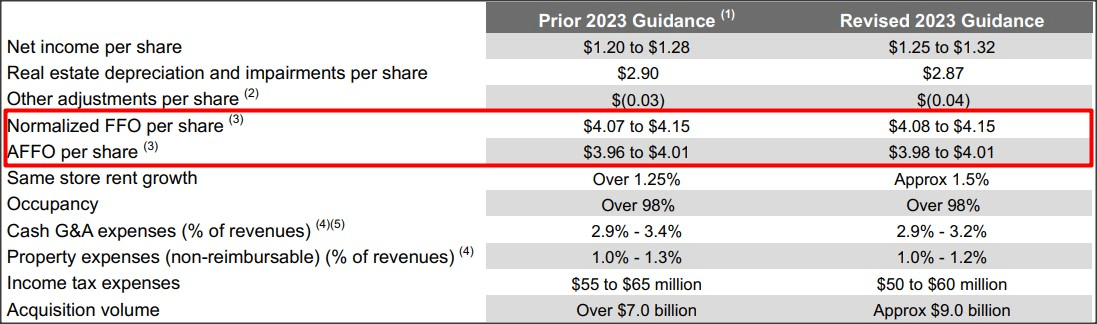

Raised NFFO/AFFO guidance, Realty Income's valuation

Due to strong rental revenues, Realty Income raised its NFFO guidance by $0.01 to a new range of $4.08-4.15 per share and its AFFO guidance by $0.02 to $3.98-4.01 per share.

{kind=link}

Realty Income no longer trades at 1-year lows, but dividend investors are still getting a bargain here, in my opinion: shares are trading at $50.22, which implies, given the new guidance, a NFFO multiplier factor of 12.2X, based off of the mid-point of guidance. This multiplier factor also implies a solid 8.2% NFFO yield.

At the beginning of 2023, Realty Income traded at $65, which reflected a 15.8X multiplier factor. I believe, given the consistency of Realty Income's results, low AFFO-based payout, and AFFO accretion related to the Spirit Realty Capital deal that the REIT is fairly valued at about ~16X NFFO... which is more in line with the REIT's historical average. A 16X NFFO multiplier would give Realty Income a fair value of ~$66 and about 31% upside potential.

Risks with Realty Income

As I said last time, Realty Income has a low amount of operational risk given its strong metrics regarding payout ratios and diversification, but the REIT does have a lot of valuation risk… as do all companies whose shares trade on the stock exchange. The biggest commercial risk for Realty Income, as I see it, relates to the current high-interest market, which makes capital more expensive. Another risk more unique to Realty Income is that the REIT has become so big that it can only meaningfully grow through acquisitions… which may result in Realty Income overpaying for acquisitions.

Final thoughts

Realty Income is firing on all cylinders, outperforming earnings expectations and adding new FFO through accretive business deals. However, the market is currently not very interested, it seems, in recognizing Realty Income's core value proposition (consistent FFO growth and a growing monthly dividend).

For contrarian investors, a buying opportunity still exists here as Realty Income Corporation shares trade well below my fair value estimate. The Spirit Realty Capital deal also seems to be highly favorable as the acquisition is set to boost Realty Income's funds from operations potential, especially in the industrial category, and improve its diversification metrics as well!

For further details see:

Realty Income: Firing On All Cylinders (Rating Upgrade)