NNN - Realty Income: Growth Justifies A Premium

2023-05-19 06:05:57 ET

Summary

- Realty Income is a fundamentally appealing REIT with a strong business model, valuation, and continued growth.

- Despite underperforming in the past year, the company has shown positive operational performance and growth in revenue and profitability metrics.

- The company is not cheap, but it offers stability and consistent growth, making it a "buy" prospect for long-term investors who value distributions.

From a purely fundamental perspective, one of the more appealing REITs that I have come across in recent years is Realty Income ( O ). Realty Income is a rather large commercial REIT with 12,492 properties that it owns or holds interests in. 98.2% of these are single client properties and the business boasts an occupancy rate of 99%. While many investors are drawn to the company by the fact that it pays out its distribution monthly as opposed to quarterly, I just appreciate its business model, valuation, and continued growth. While the company is not the cheapest firm on the market by any means, it is reasonably priced for such a high-quality market leader. This is true on both an absolute basis and relative to similar firms. And while I don't expect the company to generate enough upside to make investors rich, I do think that, for those wanting quality and stability at a decent price, this is definitely a prospect to consider.

A disconnect

It has been almost exactly a year to the day since I last wrote about Realty Income. In that article, published May 24th of 2022, I called Realty Income 'a great REIT to consider'. Leading up to that point, the company had achieved some really attractive growth, growth that I believed was set to continue throughout at least that year. I recognized the high quality of the company's assets, but I also acknowledged that shares were not exactly cheap. At the end of the day, the quality of the operation won me over and I ended up rating the company a 'buy'. But since then, shares have sadly underperformed. While the S&P 500 is up 4.9% over that time, shares of Realty Income have seen downside of 3.6%, even with the distributions factored in.

{kind=link}

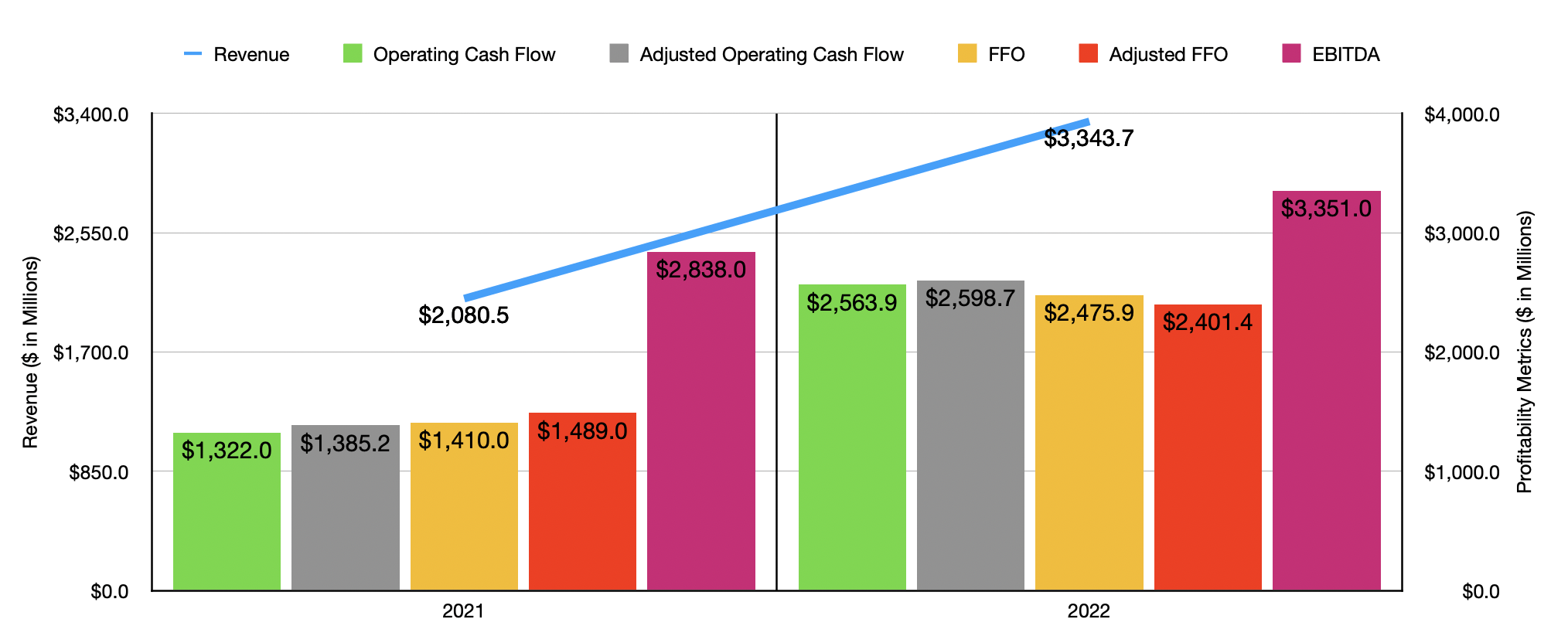

Given this relatively bad performance, you might think that there was some fundamental defect with the firm. But that's where the disconnect comes in. Operationally, Realty Income has done and continues to do quite well. Consider how the company performed during the 2022 fiscal year . During that year, revenue came in at $3.34 billion. This was up materially from the $2.08 billion in revenue the company generated one year earlier. $416 million of this sales increase came from the acquisition of 2,314 properties, totaling about 53.6 million square feet, between 2021 and 2022. The company benefited to the tune of $42.7 million from higher same store rental revenue. And, most importantly, was a deduction totaling $898.6 million in the form of rental revenue from VEREIT properties that were not included in the company's financial statements prior to November of 2021. The company did experience some weak spots, such as $154 million in lost revenue because of its Orion divestiture and $39.2 million associated with the 426 properties that it sold during and prior to 2022.

On the bottom line, the picture for the company has also been quite positive. The company went from generating $1.32 billion in operating cash flow during 2021 to $2.56 billion in 2022. If we adjust for changes in working capital, the metric would have risen from $1.39 billion to $2.60 billion. There are, of course, other profitability metrics that we should be paying attention to. FFO, or funds from operations, expanded from $1.41 billion to $2.48 billion. On an adjusted basis, it grew from $1.49 billion to $2.40 billion. And finally, EBITDA for the company increased from $2.84 billion to $3.35 billion.

{kind=link}

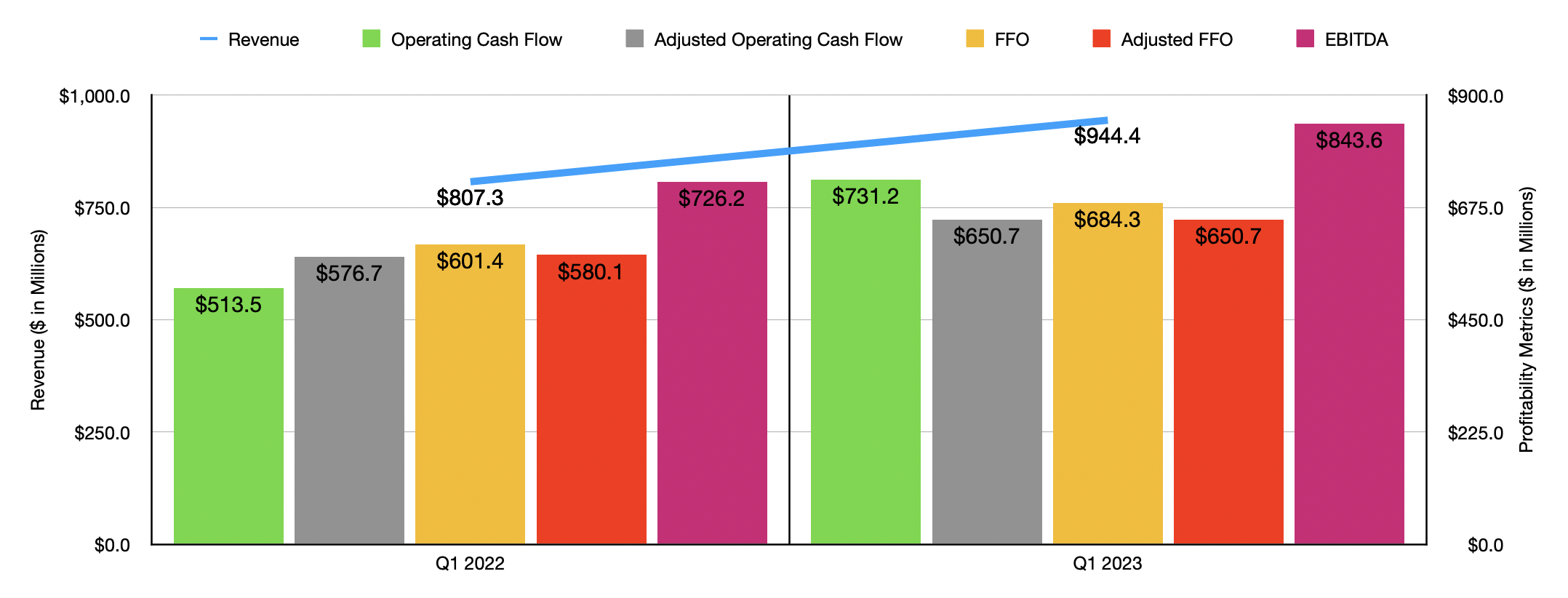

Growth for the business has continued into the current fiscal year. For the first quarter of the year, driven by the same factors that helped revenue increase in 2022, the company reported revenue of $944.4 million. That's 17% above the $807.3 million reported one year earlier. Operating cash flow jumped from $513.5 million to $731.2 million, while the adjusted figure for this expanded from $576.7 million to $650.7 million. FFO, meanwhile, went from $601.4 million to $684.3 million, while the adjusted figure for this expanded from $580.1 million to $650.7 million. And finally, EBITDA for the firm grew from $726.2 million to $843.6 million.

We don't know exactly what to expect for the 2023 fiscal year. This is not to say that management has not provided any guidance. In fact, they have. For instance, they currently think that same store rent growth will be greater than 1.25%. They also are forecasting adjusted FFO per share of between $3.94 and $4.03. At the midpoint, that would translate to a reading of $2.73 billion. The reason why I say we don't have a great deal of guidance is because we don't know the full impact on revenue associated with planned acquisitions. This year, management is forecasting over $6 billion of purchases. But given the adjusted FFO figure, we can make some assumptions about the other profitability metrics. If we assume that they would increase at the same rate, then we should anticipate adjusted operating cash flow of $2.95 billion and FFO of $2.81 billion. Meanwhile, this would translate to EBITDA of $3.81 billion.

{kind=link}

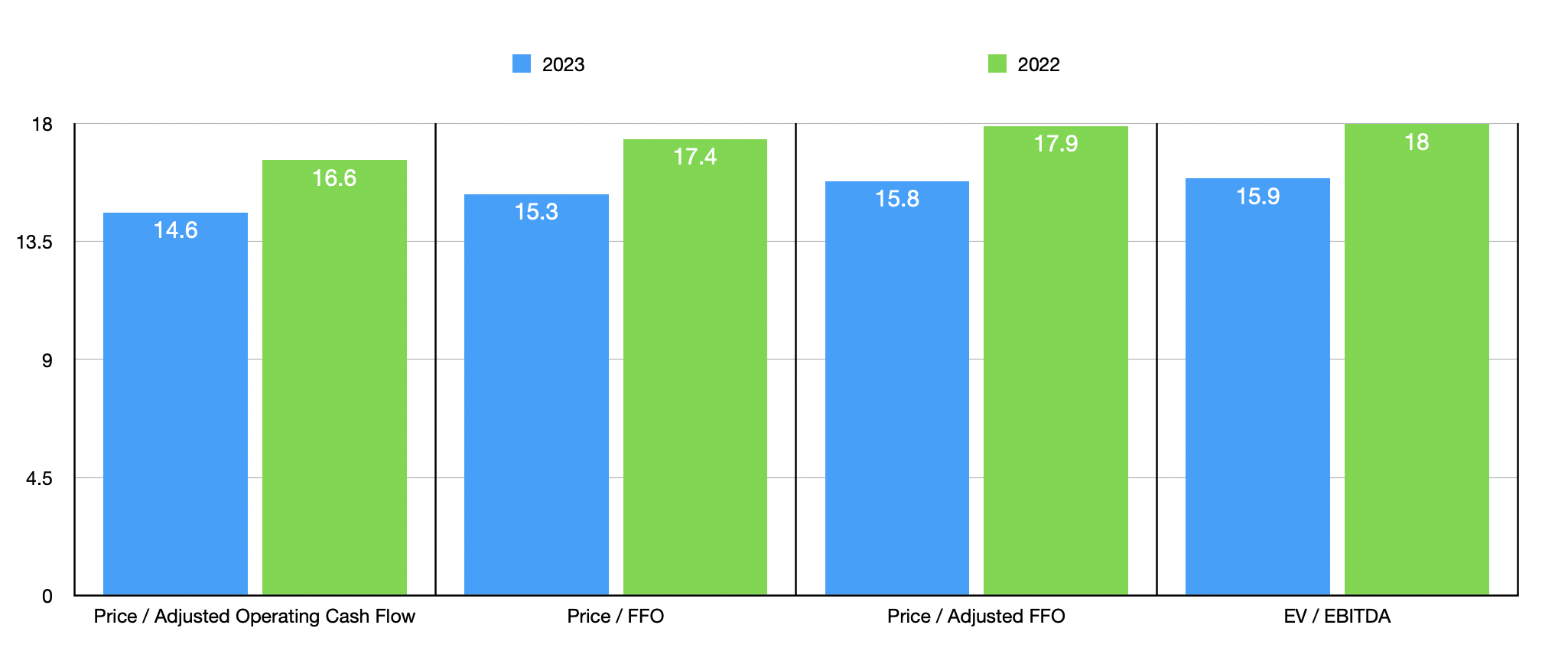

Based on these figures, it's fairly easy to value the company. In the chart above, you can see how shares are priced using both data from 2022 and forward estimates for 2023. The metrics all come in it rather similar levels. On the whole, I wouldn't say that this pricing is cheap. But it's also not at a level that would scare me. If this was not a REIT but was, instead, a company with more volatile results and less certainty when it comes to growth, I would be more neutral on the business. But high-quality companies that offer stability and consistent growth deserve something of a premium. Relative to similar firms, shares don't look unreasonably priced. In the table below, you can see how they are priced compared to five similar entities using two of the different metrics. From the price to operating cash flow approach, four of the five companies ended up being cheaper than our prospect. But when it comes to the EV to EBITDA approach, only two were.

| Company |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Realty Income |

| 14.6 |

| 15.9 |

| Simon Property Group ( SPG ) |

| 9.2 |

| 13.0 |

| Kimco Realty Corporation ( KIM ) |

| 11.2 |

| 20.6 |

| Regency Centers Corporation ( REG ) |

| 14.9 |

| 16.0 |

| Federal Realty Investment Trust ( FRT ) |

| 13.3 |

| 14.3 |

| NNN REIT ( NNN ) |

| 13.2 |

| 16.6 |

Takeaway

From all that I can see when it comes to Realty Income, the company is a quality operator that continues to grow at a respectable clip. While shares of the company are definitely not cheap, they do look priced at levels that are reasonable. And for those focused on the long haul and who value distributions, this is a good opportunity to keep in mind. In all, I still do believe that the company makes for a 'buy' prospect, so I have decided to keep it rated that for now.

For further details see:

Realty Income: Growth Justifies A Premium