SRC - Realty Income's 3rd Quarter Results: The Good The Bad The Ugly

2023-11-13 08:05:00 ET

Summary

- Realty Income has made a lot of headlines recently.

- It first announced that it would acquire Spirit Realty Capital. It then announced its 3rd quarter results.

- Here's the good, the bad, and the ugly.

In a recent article , I predicted that Realty Income (O) would report strong 3rd quarter results. The reason why I felt so confident about it is that most of its net lease peers had already released their results and they had been great across the board:

- VICI Properties (VICI): Beat

- Essential Properties Realty Trust (EPRT): Beat

- Agree Realty (ADC): Beat

- EPR Properties (EPR): Beat

- NNN REIT (NNN): Beat

- NETSTREIT (NTST): Beat

Moreover, Realty Income had just announced that it would acquire Spirit Realty Capital ( SRC ) in an all-stock deal, and I doubt that SRC would agree to such a deal if Realty Income was about to negatively surprise the market. After all, it is getting paid in stock.

Well... the earnings are out and they were very good overall. It beat quarterly expectations and also increased its full-year guidance on the back of strong acquisition volumes. It acquired $2 billion worth of assets in the last quarter alone and these deals were accretive to its FFO per share, despite its now higher cost of capital.

Realty Income

But there's more to its results than meets the eye and it wasn't all positive.

Below, we highlight all the good, the bad, and the ugly that we noted from its last quarter.

The Good

We already noted that it beat expectations and hiked its guidance.

That's obviously good, but there is even better news that appears to have been missed by most investors.

Its same property revenue growth is accelerating:

{kind=link}

Historically, Realty Income has owned a lot of properties that only had 1% annual rent escalations.

But following the major portfolio acquisitions of recent years, its average rent escalations have risen closer to 2%, which is important to its future growth prospects.

Moreover, many of its legacy leases that only had 1% annual rent hikes are gradually expiring, and despite now being older properties, Realty Income has been able to resign leases with a strong 106.9% rent recapture rate, which essentially means that it has been able to bump up its rents on top of its contractual rent hikes.

This is very encouraging because historically one of the main criticisms for Realty Income has been that it enjoyed below-average rent hikes and was too heavily reliant on new acquisitions to grow. Today, its rent growth is accelerating, which makes its future growth more predictable.

The Bad

The average investment spread over the last quarter was just 100 basis points.

That's not good, but it is not bad either.

The bad news is that these relatively small spreads were achieved by raising equity at $58.58 per share.

Today, the share price is nearly 20% lower, and therefore, the 100 basis point spread is now even smaller, likely in the 0-50 basis point range.

In the US, the spreads are likely near 0 because debt is also very expensive.

But fortunately, Realty Income should still be able to make some accretive deals in Europe where debt is a bit more reasonably priced and cap rates are a bit higher as well.

Just in the last quarter, Realty Income was able to issue some senior unsecured notes with an average term of 9 years at a weighted average annual yield to maturity of around 5%.

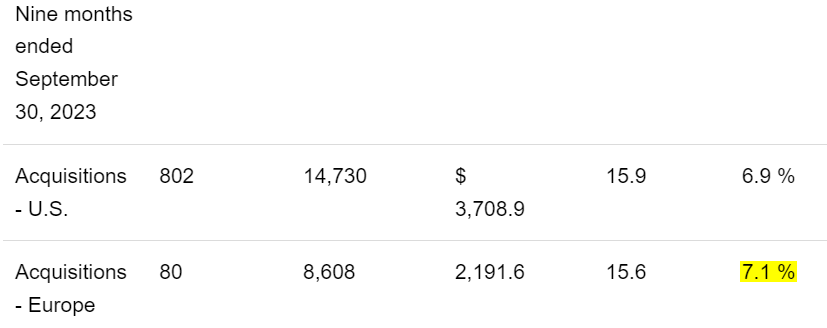

Meanwhile, it is buying properties at a 7.1% cap rate in Europe, resulting in a decent spread:

{kind=link}

Not surprisingly, Realty Income bought a lot more individual properties in Europe over the last quarter. Its purchases were about 50/50 between the US and Europe in the third quarter, but they were closer to 90/10 earlier this year.

We will likely see more of the same going forward because there simply isn't any spread in the US anymore. This is also likely why Realty Income pushed for this deal with SRC as it allowed it to secure another year of accretive external growth in an environment that otherwise isn't offering them many opportunities. Viewed from this angle, the SRC deal is clearly beneficial to Realty Income.

The Ugly

Have we overestimated Realty Income's average portfolio quality?

It just came to a resolution with Cineworld, which operates its Regal theaters and had filed for bankruptcy protection earlier this year.

And it seems like Realty Income's outcome is worse than that of EPR Properties (EPR), which also had to renegotiate its leases with Regal.

EPR was far faster to come to a resolution. It announced its resolution back in June, which in itself shows you that Regal was in more urgency to secure these specific properties. Its deal with EPR led to a rent recapture rate of 96% in year one, and growing thereafter as the box office continues its recovery. Moreover, it established a new master lease with a 13-average lease term.

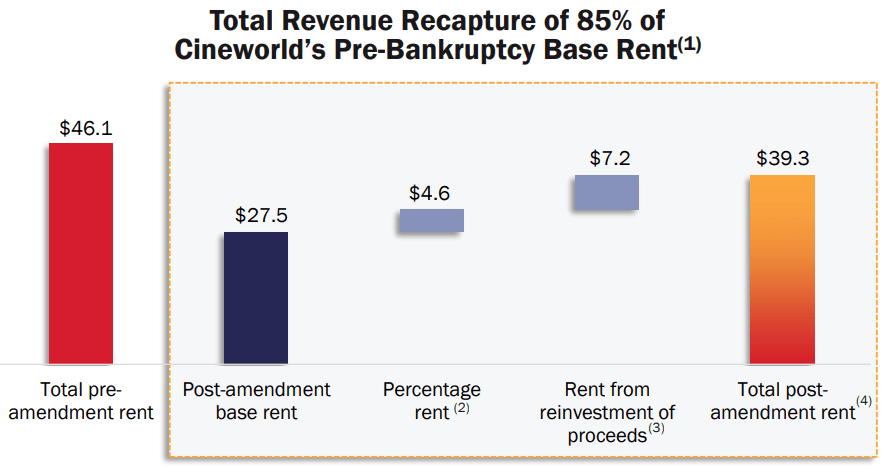

Realty Income, on the other hand, took 5 months longer to come to a resolution and it only got an 85% rent recapture rate. Cineworld also only signed a new 10-year lease:

{kind=link}

These properties only represent 1.1% of Realty Income's revenue so it is not a big deal in the grand scheme of things, but if this deal means that Realty Income's overall portfolio quality has been overestimated, then it would be quite disappointing.

The market today perceives EPR as a "lower quality" REIT and it is priced at a significant discount relative to Realty Income.

| EPR Properties |

| Realty Income |

| FFO Multiple |

| 8.8x |

| 12x |

But as we saw here, this is not necessarily the case.

So keep a close eye on the occupancy rates and the future rent recapture rates of Realty Income's properties vs. that of its close peers. If we see more underperformance coming from Realty Income, it may confirm that the market may have overestimated Realty Income's portfolio quality.

Bottom Line

We bought more shares of Realty Income after it dropped to $46 following the announcement of its deal with Spirit Realty Capital:

{kind=link}

At that price, we thought that buying Realty Income was a no-brainer, especially ahead of what we thought would be strong earnings.

But even today at a 10% higher share price, we continue to think that Realty Income is a great pick for conservative income-oriented investors who are seeking to maximize safe income and that is why we hold it in our Retirement Portfolio.

I think that there are better options for REIT investors who are seeking to maximize total returns, but priced at a 6% dividend yield and just 12x FFO, Realty Income offers great risk-to-reward for conservative income-oriented investors

For further details see:

Realty Income's 3rd Quarter Results: The Good, The Bad, The Ugly