EPRT - Realty Income's Deteriorating Outlook

2023-12-14 08:05:00 ET

Summary

- Realty Income is acquiring Spirit Realty Capital.

- Most investors appear to think that this is a good move. I disagree.

- Realty Income is going down a concerning path. Here's why.

Realty Income ( O ) announced a month ago that it is going to acquire its close peer, Spirit Realty Capital ( SRC ), in a massive $9.3 billion all-stock transaction, resulting in a roughly 15% premium to SRC's latest share price.

I actually called this back in 2018 when I wrote that Realty Income should acquire SRC in an all-stock transaction as it would be immediately accretive to its FFO per share even if it paid a 10-20% premium:

{kind=link}

That's exactly what happened.

A lot of articles have already been written about this deal and they typically focus on how it is beneficial to both REITs:

- Spirit Realty Capital shareholders get a nice bump on day 1 and will be part of Realty Income going forward, which is a superior REIT in many respects. Better balance sheet, better access to capital, better track record, etc. Some investors will argue that the valuation paid for SRC was too low and if this was an all-cash deal I would agree given that they are paying a 7.7% cap rate for assets that are worth closer to a 7% cap. But keep in mind that this is an all-stock deal and so the management is simply betting that they will do better over the long run by merging with Realty Income. I think that it is a good bet because SRC's poor track record would have likely caused it to persistently trade at a discount to peers, limiting its growth prospects.

- Realty Income , on the other hand, gets to grow its FFO per share by 2.5% on day 1 on a leverage-neutral basis and without having to raise any new external capital. That is simply because O is priced at a premium relative to SRC and they are doing an all-stock deal. Moreover, over time, O may also benefit from another 1-2% of additional accretion from management cost savings and other synergies.

But this analysis is too superficial...

There's much more to this deal and this is why the market reacted negatively to it on the day it was announced:

YCHARTS

Since then, the broader REIT market ( VNQ ) has rallied and O's share price has recovered these losses.

Nonetheless, it is worth investigating this a bit more.

Why didn't the market like this deal?

I think that there are three main reasons why the market didn't like the deal:

Reason #1: Dilutive to portfolio quality

This is probably the main reason.

If you have followed SRC for a while, you will likely know that its focus has historically been on higher-yielding properties that are occupied by riskier tenants. As a result of this, the company ran into some major difficulties back in 2017 when its biggest tenant filed for bankruptcy.

Since then, SRC has spun off its troubled assets into a separate REIT and improved the average quality of its portfolio. Even then, its focus has typically been on higher-yielding properties than Realty Income because of its higher cost of capital.

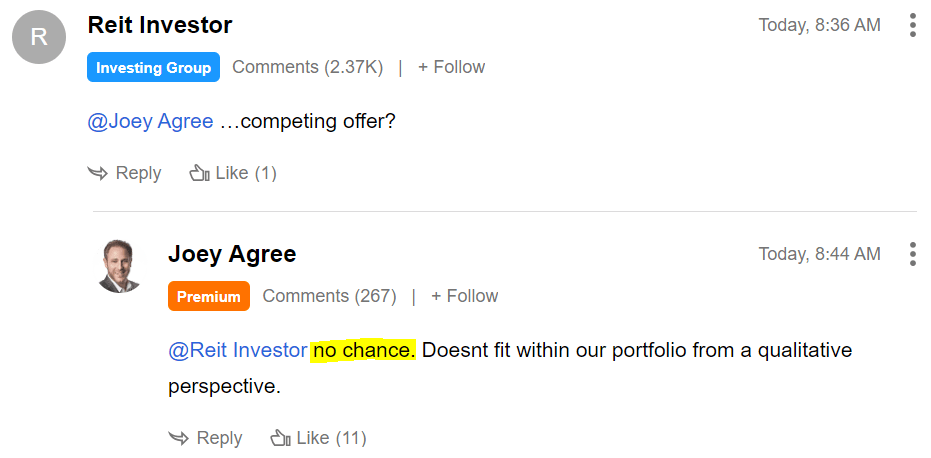

This means that Realty Income is diluting the average quality of its portfolio by acquiring Spirit Realty Capital. I was amused to see Joey Agree, the CEO of Agree Realty ( ADC ), comment that they wouldn't be interested in buying SRC because of this reason:

{kind=link}

Reason #2: Realty Income is getting too big for its own good

The second reason why the market likely didn't like the deal is because of its sheer size.

Once the merger is completed, Realty Income will have an enterprise value of approximately $63 billion, which is massive for a net lease REIT.

Realty Income claims that the large size is an advantage as it leads to economies of scale and greater diversification.

But the market is smart enough to recognize that past a certain size, there are also diseconomies of scale as it becomes a lot harder to grow.

The larger you are, the smaller the impact each new acquisition will have, and there are only so many properties for sale at any given time.

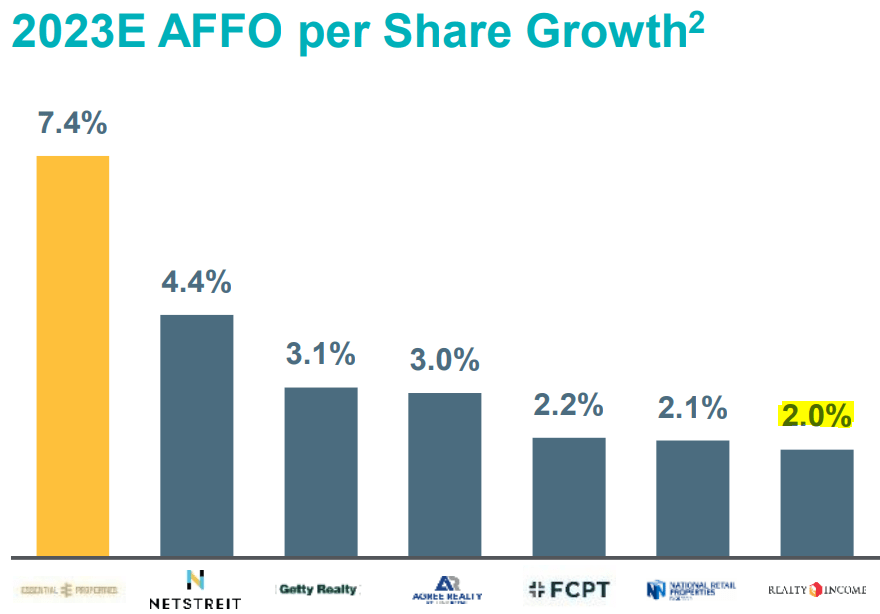

This is the main reason why many of Realty Income's close peers have been growing faster even before this merger:

Essential Properties Realty Trust

{kind=link}

Following this merger, Realty Income will be another $10 billion larger, which in itself is the size of a big REIT.

The 2.5% FFO per share accretion is a win in the near term, but if it hurts the company's long-term growth rate, then it could warrant a lower valuation multiple, despite the near-term accretion.

Reason #3: Too little accretion

Finally, you need to ask yourself if this is all worth it.

Realty Income is diluting the average quality of its portfolio and potentially hurting its long-term growth rate to gain 2.5% of FFO today.

The market appears to think that the upside isn't worth the downside and this is why Realty Income's share price dropped by 5.7% when the deal was announced.

So should you buy, hold, or sell?

I still give it a Buy rating.

Investors tend to forget that each investment has pros and cons and Realty Income is no exception.

Its pros are that:

- It still owns one of the best net lease portfolios in the market.

- It generates highly consistent and predictable cash flow that's set to grow, albeit at a slightly lower growth rate than some peers.

- It has a sector-leading A-rated balance sheet.

- It has one of the best track records of all REITs.

- The management is laser-focused on growing its monthly dividend.

The main cons are that:

- Its large size is forcing it to do more portfolio deals, which risks diluting the quality of the portfolio over time.

- Its growth will likely underperform some of its peers over time.

But that's more than reflected in the company's valuation in my opinion.

It is today priced at a historically low valuation and high yield:

| Typical |

| Today |

| FFO Multiple |

| ~20-25x |

| 13.2x |

| Dividend Yield |

| ~4% |

| 5.7% |

And it is also priced at a discount relative to its peers. This is the first time in a long time that Realty Income is the cheaper option in the net lease sector:

| FFO Multiple |

| FFO Multiple |

| Dividend Yield |

| Realty Income ( O ) |

| 13.2x |

| 5.7% |

| VICI Properties ( VICI ) |

| 13.4x |

| 5.4% |

| Agree Realty ( ADC ) |

| 14.5x |

| 5.0% |

| Essential Properties Realty Trust ( EPRT ) |

| 13.8x |

| 4.6% |

I think that the entire sector is undervalued and each of these REITs has unique pros and cons depending on what you are looking for.

O may not be the best pick if you are seeking to maximize total returns because its large size will limit growth prospects.

But if you are a conservative income investor and your goal is to maximize safe income, then Realty Income is arguably the best pick right now and that is why it makes sense for our Retirement Portfolio.

For further details see:

Realty Income's Deteriorating Outlook