SRC - Realty Income Snatches Up Spirit Realty Capital For A Song

2023-11-01 10:41:00 ET

Summary

- Realty Income has reached an agreement to acquire Spirit Realty Capital in an all-stock deal valued at $9.3 billion.

- The combined company will capture annualized pre-tax synergies of $50 million, resulting in cost savings and increased growth potential.

- The acquisition will allow Realty Income to diversify its portfolio and become the fourth largest REIT in the S&P 500 by enterprise value.

- The terms particularly favor Realty Income, and it's not surprising to see this game-changing purchase take place.

October 30th ended up proving to be a fascinating day for shareholders of two very sizable REITs. The firms in question are Realty Income ( O ) and Spirit Realty Capital ( SRC ). Shares of the former pulled back rather materially, closing down 5.7% for the day, while shares of the latter jumped to close up 7.9%, after news broke that Realty Income reached an agreement to acquire Spirit Realty Capital in an all stock deal that the companies said was valued at $9.3 billion. While I personally take issue with the effective purchase price, I do believe that this transaction is very appealing for the purchaser. This opinion is firmly at odds with the market's own perception. If it weren't, then shares of Realty Income would have risen in response to this development. The market seems to think that it is paying a premium of sorts for Spirit Realty Capital. But when you look at the terms of the deal, and even if you ignore potential synergies associated with it, I do believe that investors in Realty Income should consider themselves fortunate that this deal has been agreed upon.

A game-changing merger

I have a bit of a history writing about both Realty Income and Spirit Realty Capital. The last article that I wrote about the former was published in the middle of August. In that article, I lauded the company's growth and, while I recognized that shares were not cheap, I did say that they were appealing enough because of cash flows to warrant a 'buy' rating. Spirit Realty Capital, meanwhile, is a firm that I last wrote about in the middle of September. In that article, I found myself impressed by the hefty yield that units offered and by how cheap shares were. I even compared the enterprise to Realty Income, pointing out that long term investors that are focused on growth of an enterprise would prefer Realty Income over Spirit Realty Capital, but nonetheless rating Spirit Realty Capital a 'buy'. I actually concluded that article by pointing out that a purchase of Spirit Realty Capital by Realty Income might make a lot of sense, though I made the claim that betting on such a transaction was purely speculative.

{kind=link}

Fast forward to today, and it seems as though my gut feeling turned out to be accurate. According to the press release issued by Realty Income regarding the transaction, it will be acquiring Spirit Realty Capital in an all-stock deal valued at $9.3 billion on an enterprise value basis. I do take a bit of an issue with this price though. This is because the price includes an additional $200 million term loan that Spirit Realty expects to take out in December of this year. That loan has not been taken out yet and, unless the capital is distributed outside of the firm, keeping it on the books as cash would not change net debt. So based on the information that we know now, I would argue that it would be premature to count that into the purchase price. But I digress.

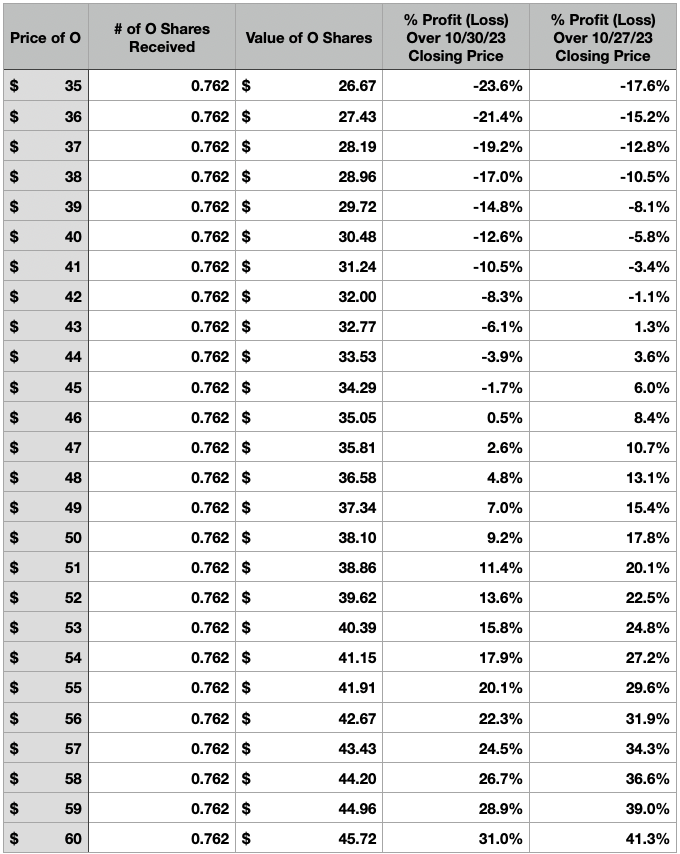

The way it will work is that, when the deal closes, shareholders of Spirit Realty Capital will receive 0.762 of a share of Realty Income for each share of Spirit Realty Capital that they own. Because Realty Income is significantly larger, its shareholders will end up with approximately 87% of the combined company, with the remainder going to investors in Spirit Realty Capital.

{kind=link}

There are multiple reasons why this purchase makes a great deal of sense to me. For starters, the management teams at the firms believe that the combined enterprise will be able to capture annualized pre-tax synergies of $50 million, with $20 million of that in the form of stock-based compensation and the rest in the form of other general and administrative savings. These savings will be the result of trimming the fat when it comes to overhead that would be redundant for one firm that wouldn't be for two separate firms. It's likely that other corporate costs will also be involved, though we don't know to what extent that may be the case.

{kind=link}

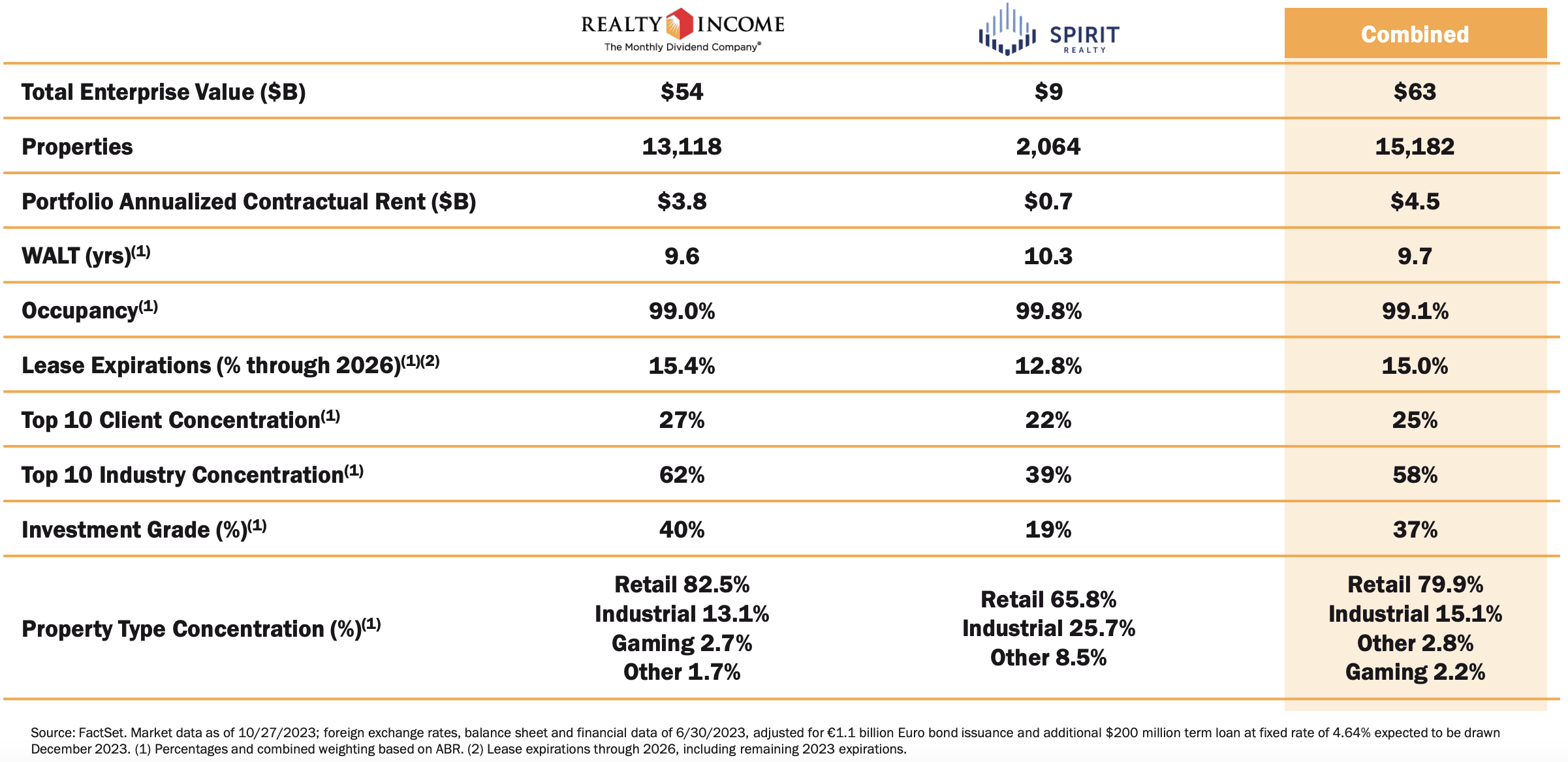

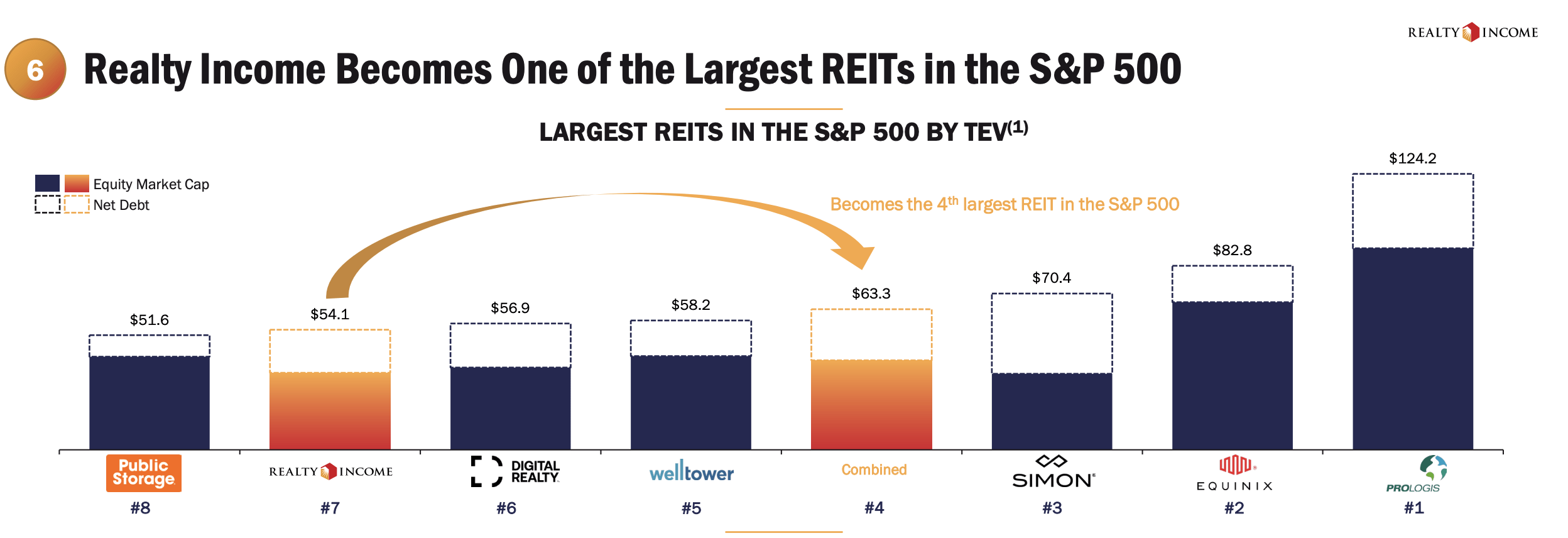

A second reason for this transaction involves the size of the two companies. The fact of the matter is that Realty Income is a behemoth in the REIT space. The company has 13,118 commercial real estate properties in its portfolio that collectively generate annualized base rent of around $3.8 billion. The company has made it a point to pay out distributions each month, as opposed to the more regular quarterly payments, which is a testament to the stability of its business model. But there's always room for additional growth. Spirit Realty Capital has 2,064 properties in its portfolio that total 61 million square feet of space. Annualized base rent is around $695 million. Upon completion of the transaction, Realty Income will go from being the 7th largest REIT in the S&P 500 by enterprise value to being the 4th largest. With that size comes certain advantages such as the ability to get better terms on deals and to generate enough capital to grow rapidly.

{kind=link}

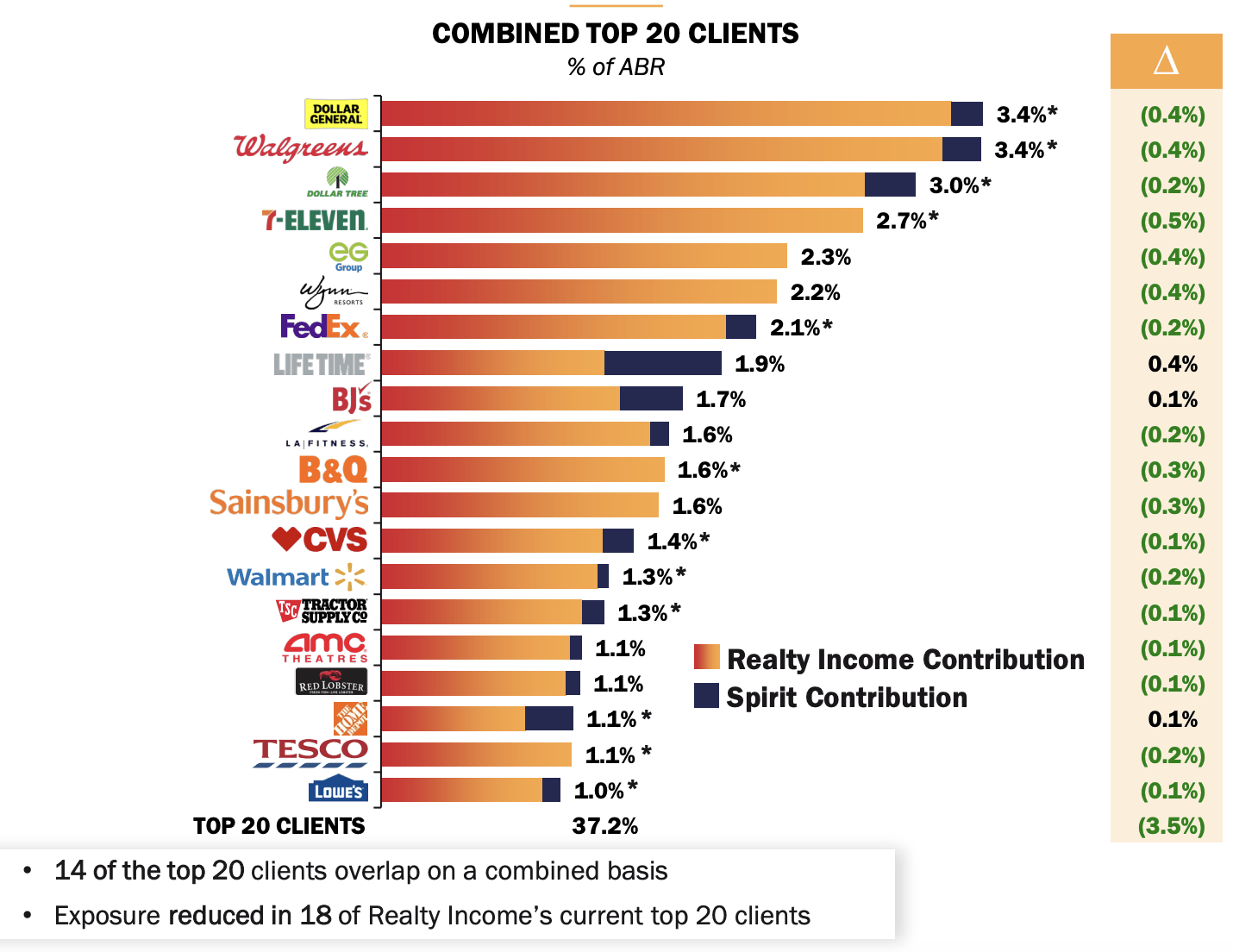

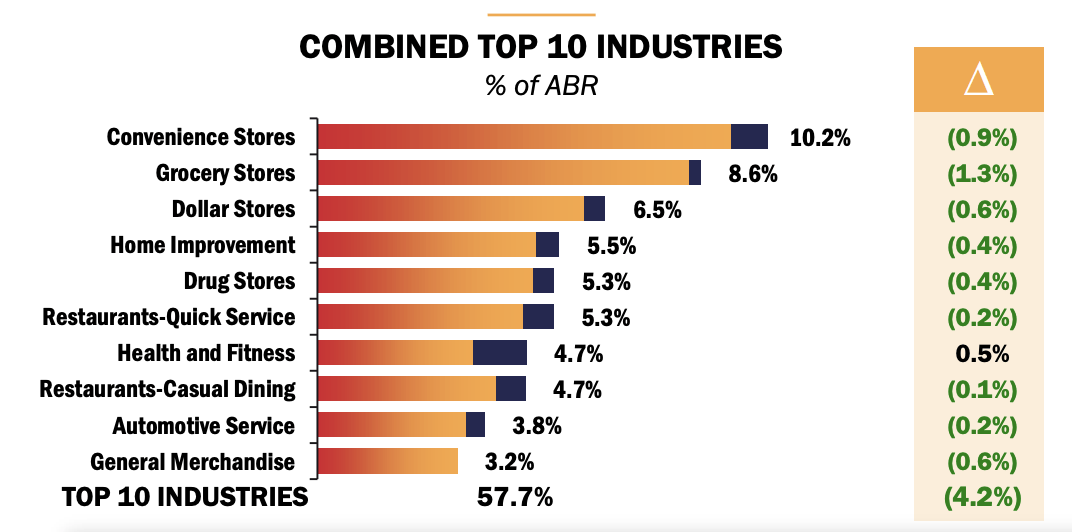

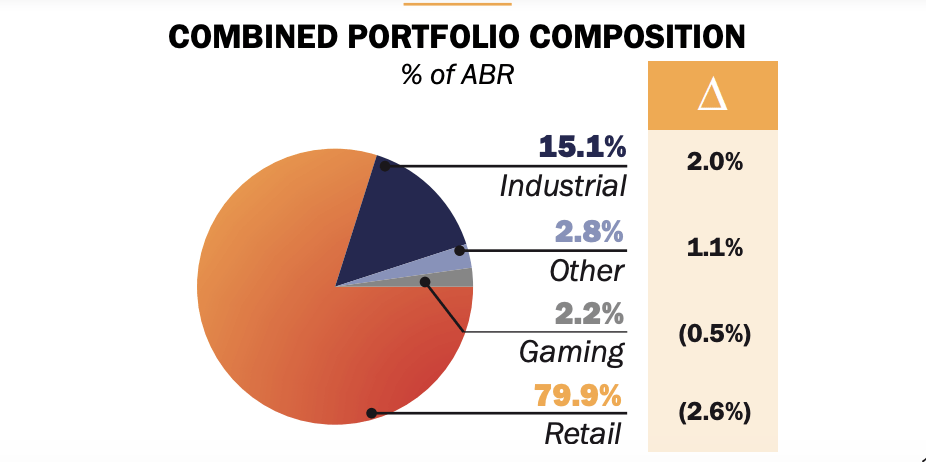

The transaction we also have another benefit. And that's that it will allow further diversification for shareholders of Realty Income. As you can see in the image above, exposure to the majority of the 20 largest clients for Realty Income will decrease, as will its exposure, as shown below, to the 10 largest industries that it caters to. The company will also see a change in exposure in some other ways. For instance, as of this writing, Realty Income generates 76% of its annualized base rent from retail. That number is expected to climb to 79.9% following the completion of this transaction. Exposure to industrial properties, meanwhile, will grow from 13% to 15.1%.

{kind=link}

{kind=link}

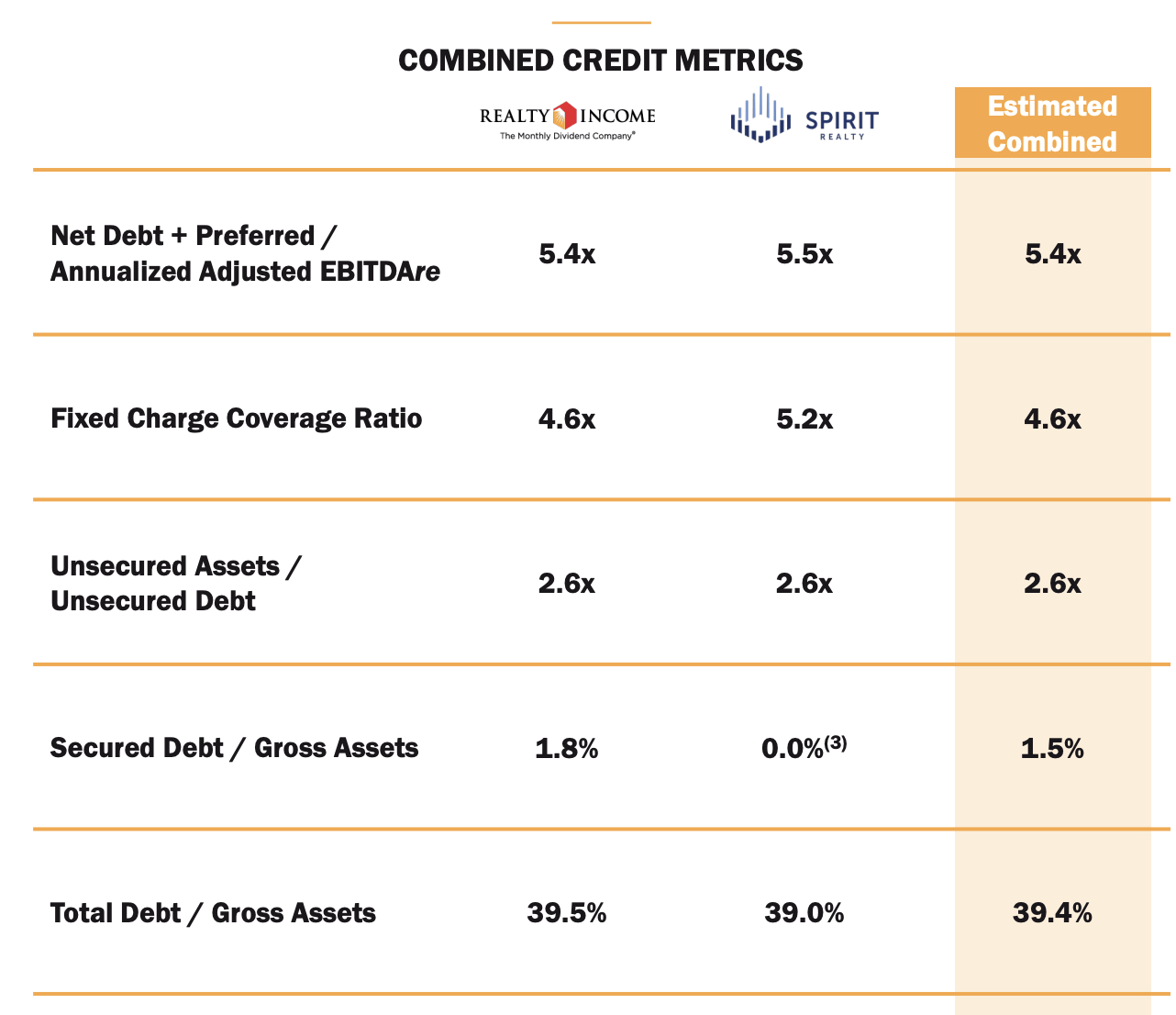

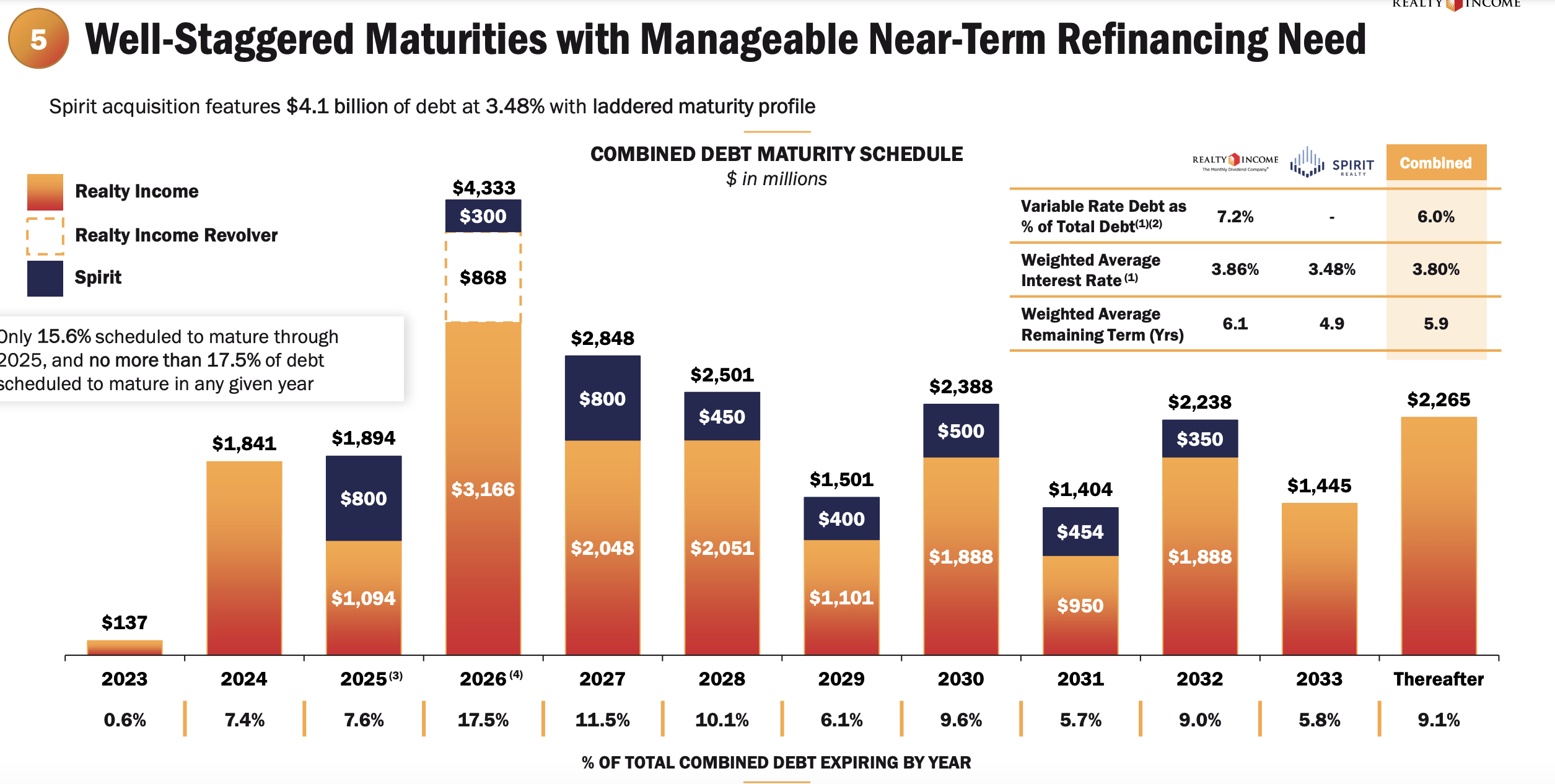

Some investors might be worried about leverage. This is a natural consideration. It's all too common for companies in the market to take on other firms that already have a lot of leverage. That can cause issues down the road. The good news is that the two companies are similar in this regard. The net leverage ratio of Realty Income currently stands at 5.4, while for Spirit Realty Capital we get a reading of 5.5. The combined company will still have a net leverage ratio of 5.4. But this doesn't mean that all the debt changes are positive.

{kind=link}

The weighted average remaining term of debt for Realty Income is 6.1 years, while for Spirit Realty Income it is 4.9 years. Put another way, Realty Income we'll go from having 39.9% of its debt coming due between now and 2027 to having 41.1% due over that same window of time. Most of this is because of $800 million of debt owed by Spirit Realty Capital that comes due in 2025 and another $800 million that comes due in 2027. The good news is that all of the debt on Spirit Realty Capital's balance sheet is fixed and the weighted average interest rate of that debt is 3.48%. That's a bit below the 3.86% per annum that we get for Realty Income.

{kind=link}

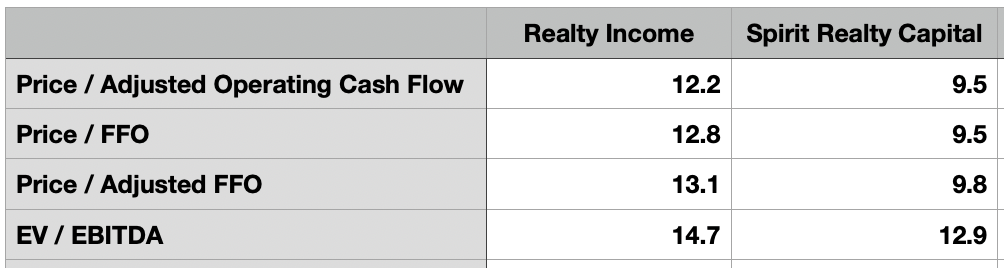

Judging by how shares of both companies responded to this development, it's clear that market participants are not terribly happy with Realty Income. In some respects, I understand this. As I mentioned in the aforementioned article about Spirit Realty Capital, Realty Income is the superior firm. Having said that, it's also clear to me that Realty Income is getting the company at a really good price. As I mentioned earlier, Realty Income's investors we'll end up with 87% of the combined company. However, using estimates for the 2023 fiscal year, Realty Income is only bringing 84.7% of the adjusted operating cash flow and 84.3% of the EBITDA to the transaction. A disparity could make sense if leverage was different, but I have already explained how that's not the case. Another way to look with this is shown in the chart below. That chart shows the pricing of the deals at the implied price as agreed upon in the merger announcement. By every metric, Realty Income is more expensive than Spirit Realty Capital. And the fact that the transaction is all stock means that Realty Income is essentially using expensive currency to pay for the enterprise its acquiring.

{kind=link}

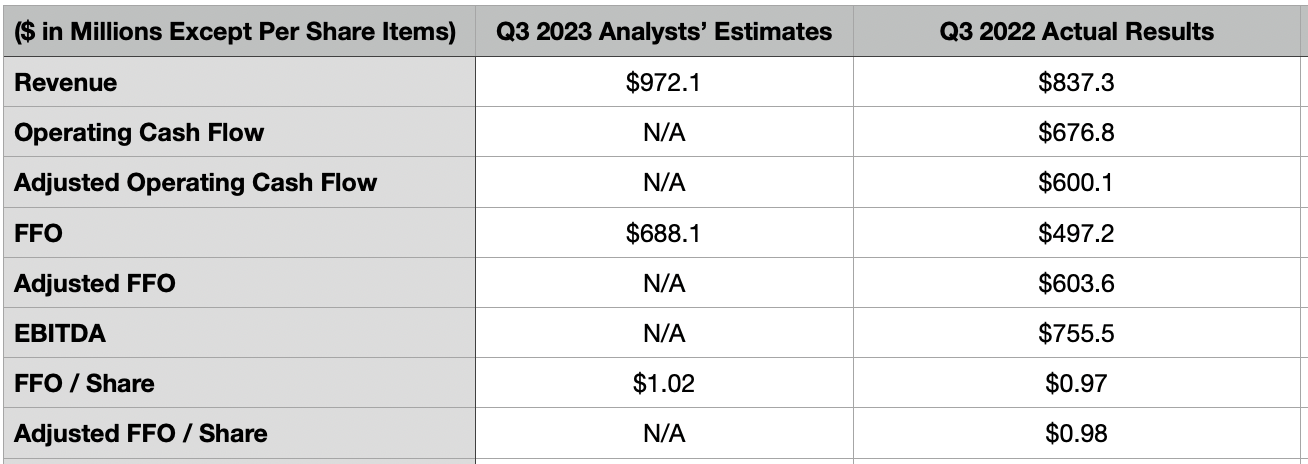

It will be interesting to see what this all means when Realty Income reports earnings in the coming days. After the market closes on November 6th, the management team at the firm will announce financial results covering the third quarter of the company's 2023 fiscal year. At present, analysts are forecasting revenue of $972 million. This will be materially higher than the $837.3 million the company generated the same time last year. And much of that growth should be attributable to the $7 billion that management is allocating toward capital expenditures this year. FFO per share is forecasted to be $1.02. If this turns out to be accurate, it would represent an increase over the $0.97 per share generated one year earlier. Put another way, this should take FFO up from $597.2 million to $688.1 million.

{kind=link}

Investors should pay attention to these metrics, but they should also be paying attention to other important metrics as well. For context, in the third quarter of last year, operating cash flow was $676.8 million, while adjusted operating cash flow totaled $600.1 million. Adjusted FFO came in at $603.6 million, while EBITDA totaled $755.5 million. In all likelihood, these will also each increase year over year. To be honest, I don't believe that anything management reports that involves this merger will impact financial results for the quarter. But investors should pay attention for significant changes in spending guidance given that this is a large transaction. It is entirely possible that management may lower guidance on spending for the year because of the size of this transaction. But I don't think there's a high probability since this is an all-stock deal as opposed to all cash or cash and stock. But then again, when you add on top of this the earlier announcement that the company acquired a minority stake in Bellagio Las Vegas in exchange for $950 million, I wouldn't be terribly shocked at some sort of scaling back.

Takeaway

Based on the data provided, I will say that I view this purchase of Spirit Realty Capital by Realty Income as a net positive for the latter. Shareholders of the former do get a bit of upside in the short run. They also get to be part of a larger and, frankly, superior company. But at the end of the day, I do think they got the less appealing side of this transaction. If synergies come through, the picture looks even more appealing. But investors should never bank on that and they should also pay attention to what is reported in the coming days for earnings to see to what extent guidance might change and the impact that might have, if any, on the thesis for either firm.

For further details see:

Realty Income Snatches Up Spirit Realty Capital For A Song