SRC - Realty Income Stock: Future Growth Opportunities In SLBs

2023-11-09 08:30:46 ET

Summary

- Realty Income Q3 earnings came in better than expected for revenue and FFO/share.

- Realty Income dividend is at a decade high for this aristocrat when discounting the Covid "flash crash".

- Realty Income Q3 earnings presentation clearly outlines excess liquidity and its upcoming opportunities for SLB transactions amongst operators in a pinch.

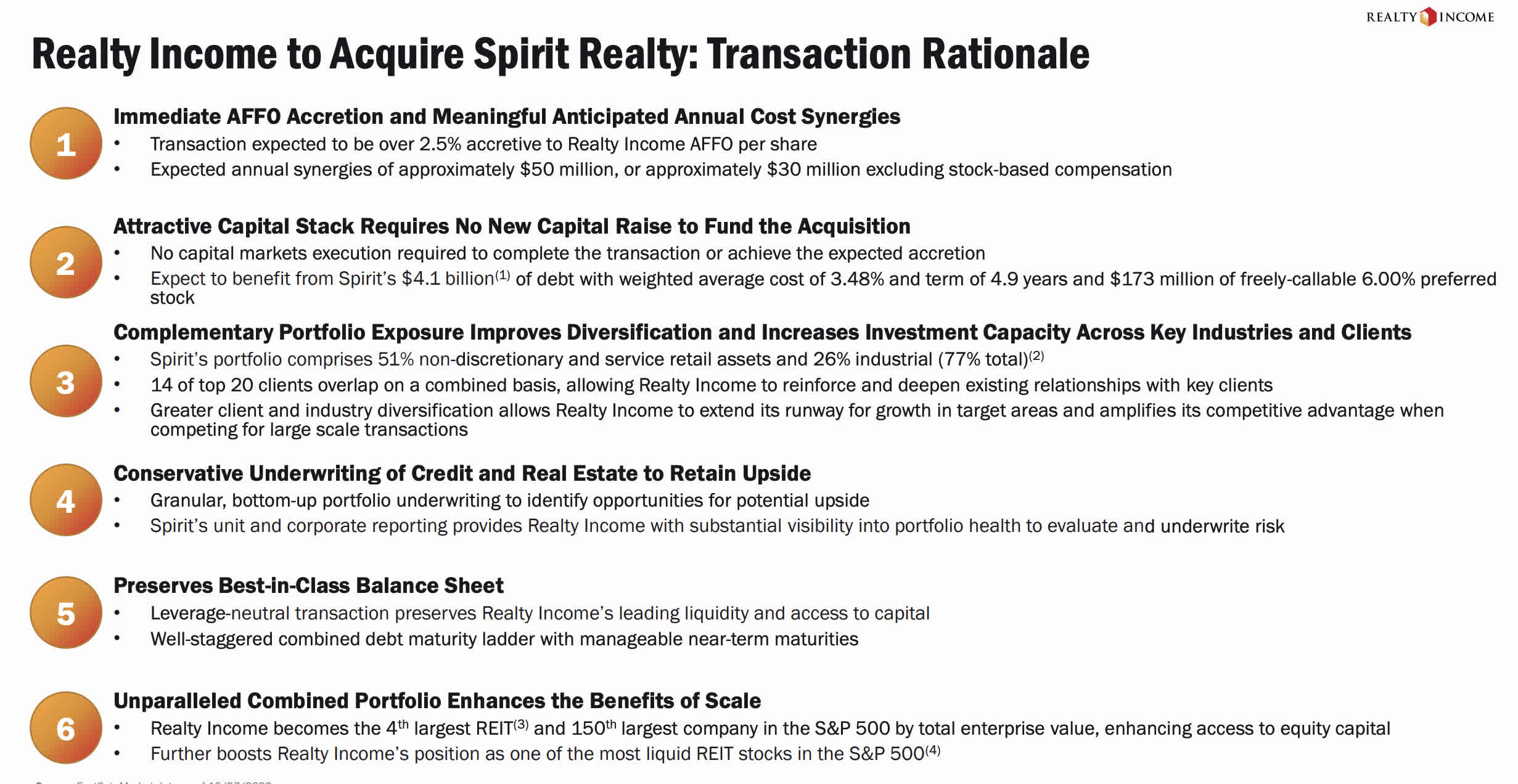

- This article lays out the accretive nature of the Spirit Realty Capital deal and addresses the acquisition of debt.

- Realty Income's price appreciation trends have, in a rarity, disconnected from increases in EBITDA growth. Indicative of value.

Quick look at the merger

One of my favorite authors who is not often spoken about on Seeking Alpha is Ken Fisher. His books do an excellent job of teaching us to first convert any ratios to percentages to easily evaluate the feasibility of any deal. Invert the earnings ratios and you get a yield. Divide the interest rates by total debt, and you can see the near-term cost of debt. Comparing the two, you can come up with a decision on whether it's better to sell equity or sell debt to expand a business if additional capital is needed. It also better helps to evaluate your own personal stock buying decisions, in my opinion.

Realty Income Corporation (O) had a quick snap back into the $40s after the acquisition announcement of Spirit Realty Capital (SRC). I bought as much as I could as the yield approached 7% for a brief moment. The more I did some Ken Fisher-esque back-of-the-napkin assumptions, the more I liked it. After Realty Income re-emphasized some thoughts I had in my mind about sale leasebacks coming into debt maturities on the horizon in the Q3 earnings presentation, I liked the stock even more.

Recent earnings

{kind=link}

Seeking Alpha

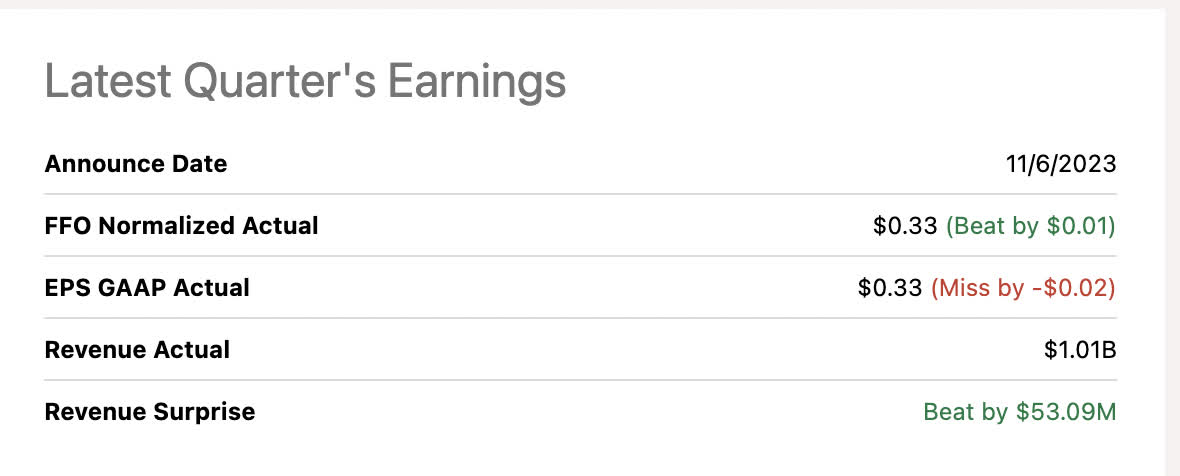

Before getting to a simple analysis of the accretive nature of the acquisition, MRQ earnings came in great. Beating revenue and FFO. I'm considering this the top and the bottom line versus GAAP EPS.

Most recent quarter capital sources and uses

{kind=link}

Seeking Alpha

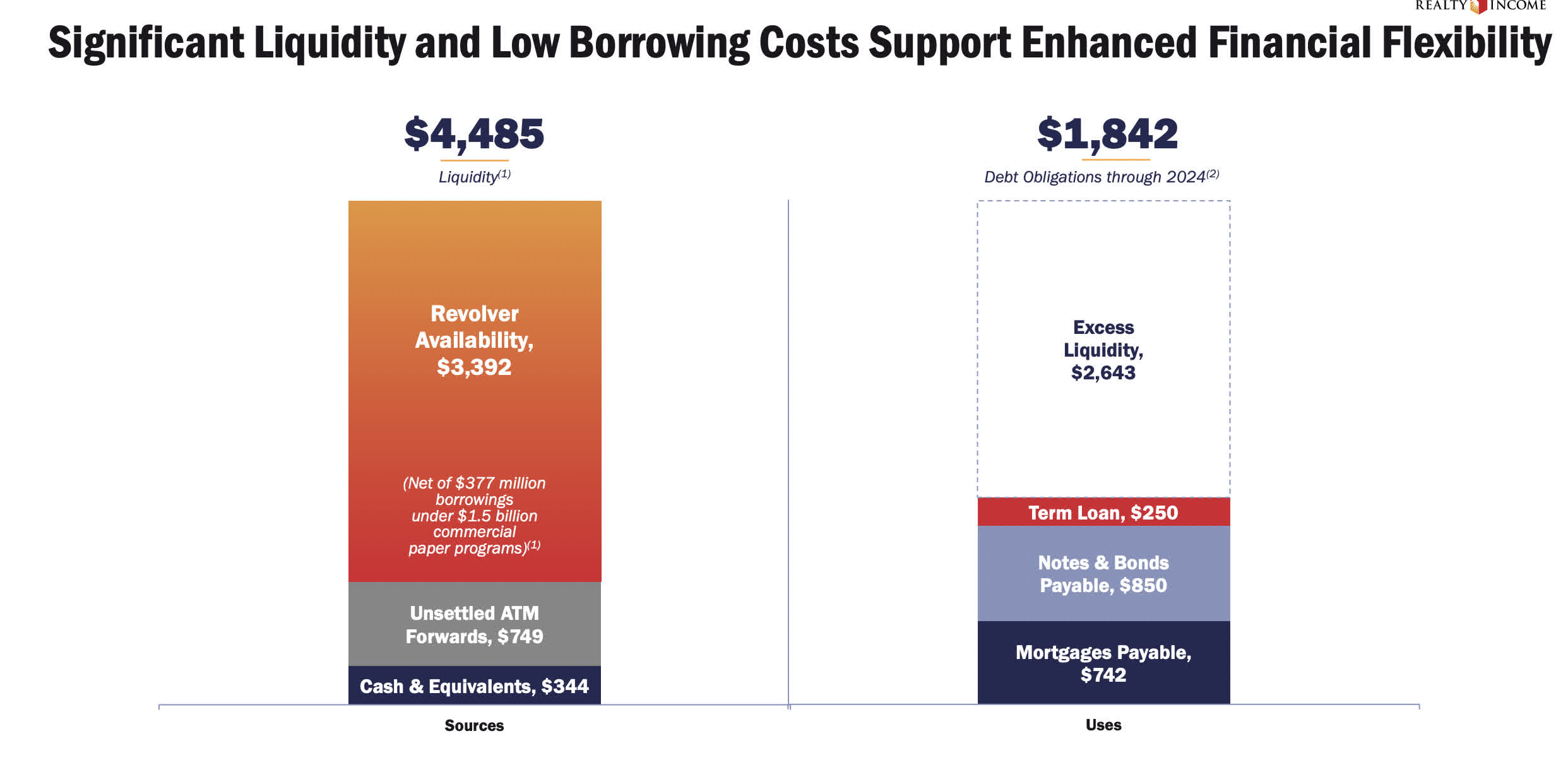

Throughout the most recent quarter's report , Realty Income continues to harp on its credit rating and capital sources. As we can see from the most recent numbers, there's $2.64 Billion in excess liquidity available to Realty Income Corporation. This has been in the back of my mind for some time. As private developers, landlords, owner operators, or REITs without excess liquidity have maturities arising in FY24 and beyond, sale-leaseback opportunities will be abundant. More on this later.

Back of the napkin

First, I'm going to take a look at the implied yield Realty Income could be getting from Spirit Realty Capital when compared to their own current FFO yield.

All data courtesy of Seeking Alpha:

Accounting for share swaps

- Share swap .762 to 1

- Realty Income Corporation shares outstanding = 723.9 million

- Spirit Realty Capital shares outstanding = 141.3 million X .762= 107.67 million after the swap.

- Total shares = 831.57 million after the merger in a static share vacuum.

FFO yield evaluation

- Realty Income Corporation : FFO/Share TTM =$4.14/50= 8.28% FFO yield to current price

- Spirit Realty Capital: FFO/Share TTM= $3.61/ ($38.93 X .762 discount equivalent to $29.66 share value)= 12.17%

Thus as we can see, the acquisition at a discounted swap could amount to as much as a 3.9% FFO yield over the current yield of Realty Income Corporation yield shares. A lot of things could occur between the two share prices before consummation, but at face value, it looks like a good deal. However, Spirit Realty Capital is a comparatively smaller company so the net effect will not cause much of a ripple in total FFO yield.

The debt

{kind=link}

Seeking Alpha

The debt being combined will probably raise the overall interest rate blend across the two companies, let's see to what extent:

All data courtesy of Seeking Alpha:

- TTM Realty Income interest expense= $653.4 million

- TTM Realty Income total debt= $20.45 Billion LT debt + 19.9 million ST debt = $20.47 Billion total debt

- $653.4 million/ $20,470 million = 3.19% average debt interest rate.

- TTM Spirit Realty Capital interest expense = $138 million

- TTM Spirit Realty Capital total debt = $3.82 Billion total debt

- $138 million/ $3,820 million= 3.6% average interest rate

At first glance, the two rates look to be about 40 basis points apart. Realty Income puts the cost spread narrower in their most recent presentation. Not huge and of the combined debt of $24.27 Billion, Spirit Realty Capital only represents 15.7% of total debt. The numbers seem trivial. This is simply because the company is so much smaller than Realty Income Corporation.

At an enterprise value level, the total equity of Spirit is $4.492 Billion and $31.823 Billion for Realty Income Corporation. This is a combined $36.31 Billion in combined book value of equity . The debt-to-equity ratio thus works out to about .68. With more equity than debt in the capital stack, if the return on equity works out to be higher than the hike in rates on debt, I do not see where this would be a bad deal. Looking at the FFO yield implied from the first segment, it far outweighs any additional cost of capital increase.

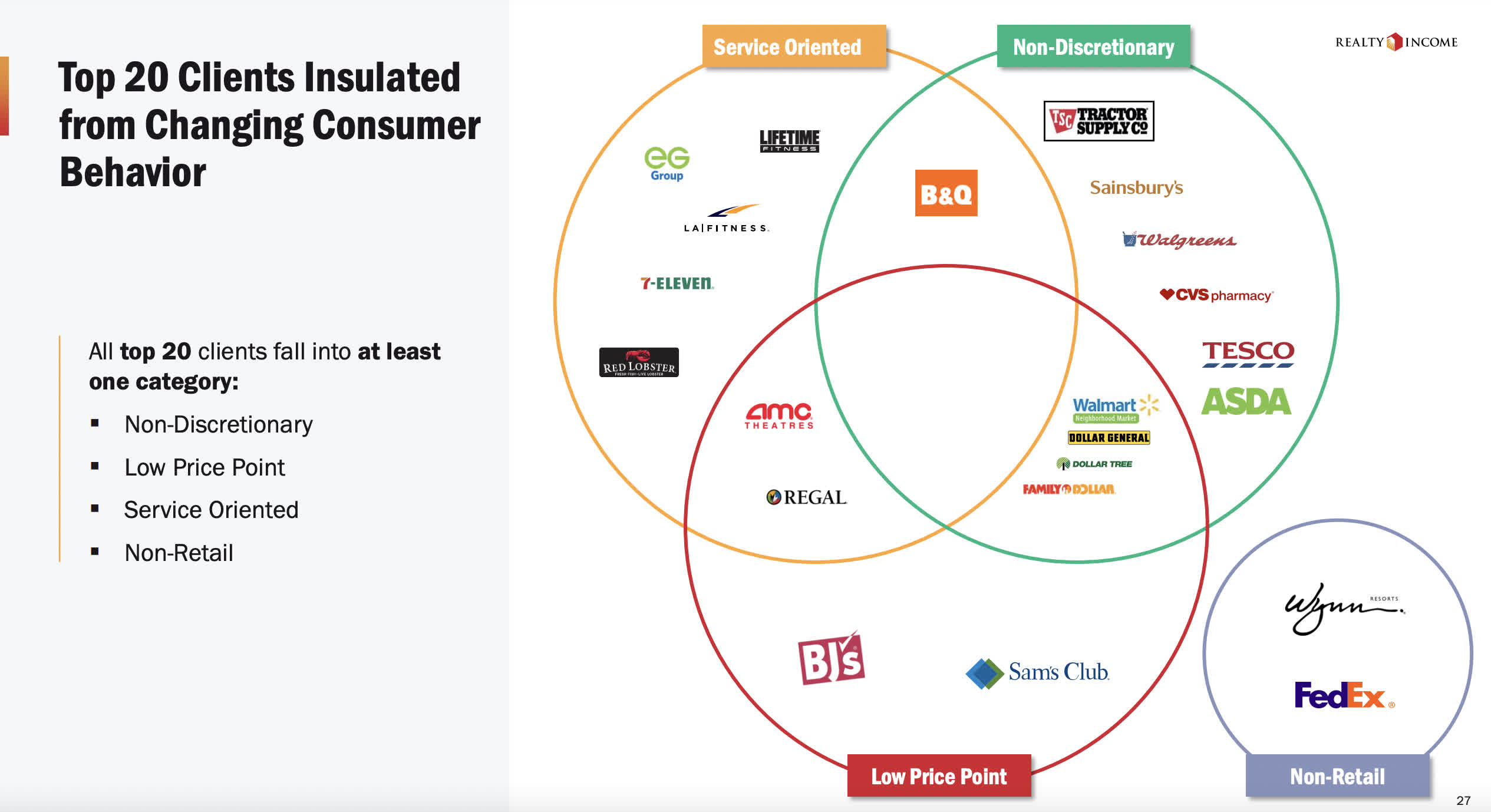

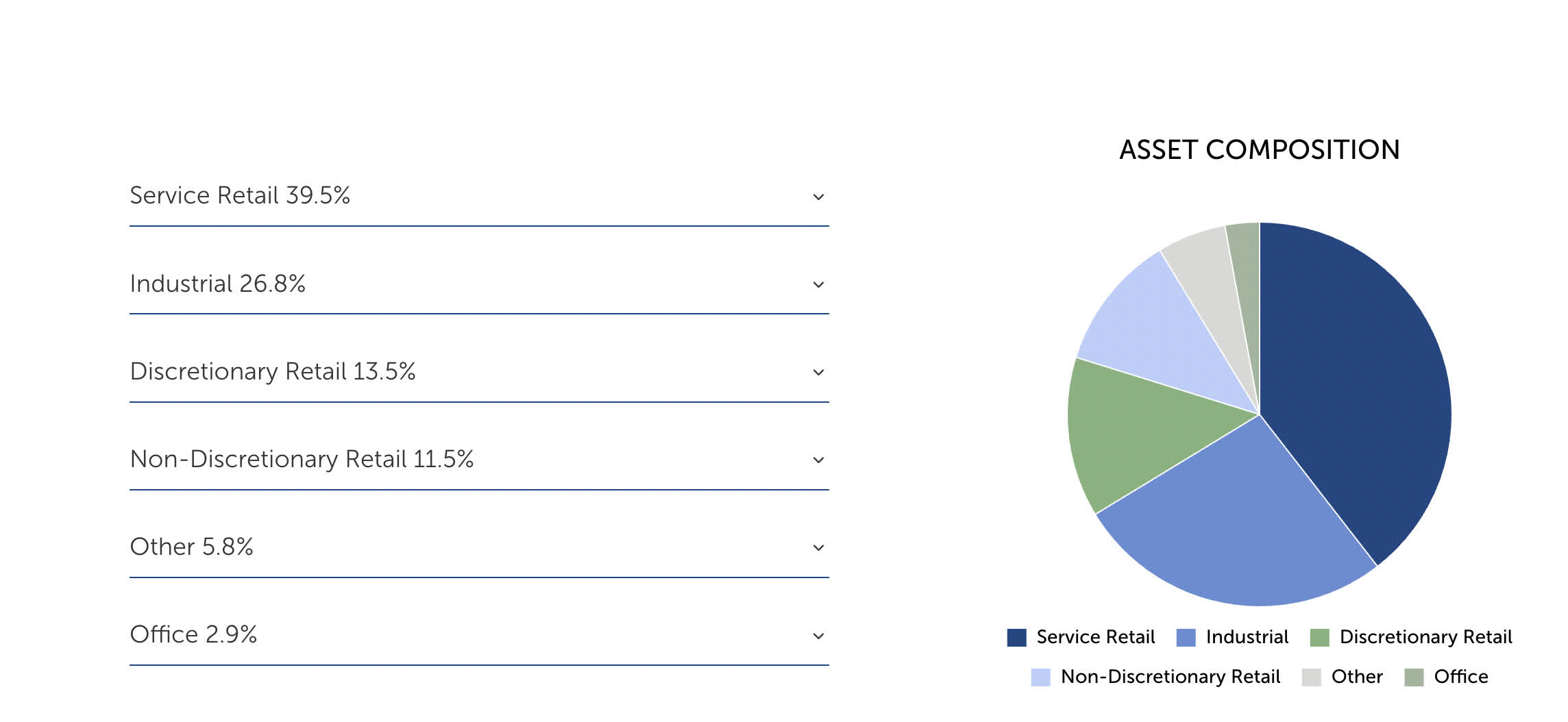

The properties are similar

Realty Income tenants

{kind=link}

Seeking Alpha

SRC tenants - Portfolio

{kind=link}

spiritrealty.com/portfolio

We can see a similar asset composition with a tad of office in the SRC portfolio. Otherwise, a lot of the same. Again, a much smaller company than Realty Income is being merged into the mix. It will be accretive and enhance growth rates at face value, but should have never garnered as much reaction as it did in the market.

Dear Mr. Market: Thanks for the cheap shares.

Now that's out of the way, let's get to my more bullish reasons to own this stock.

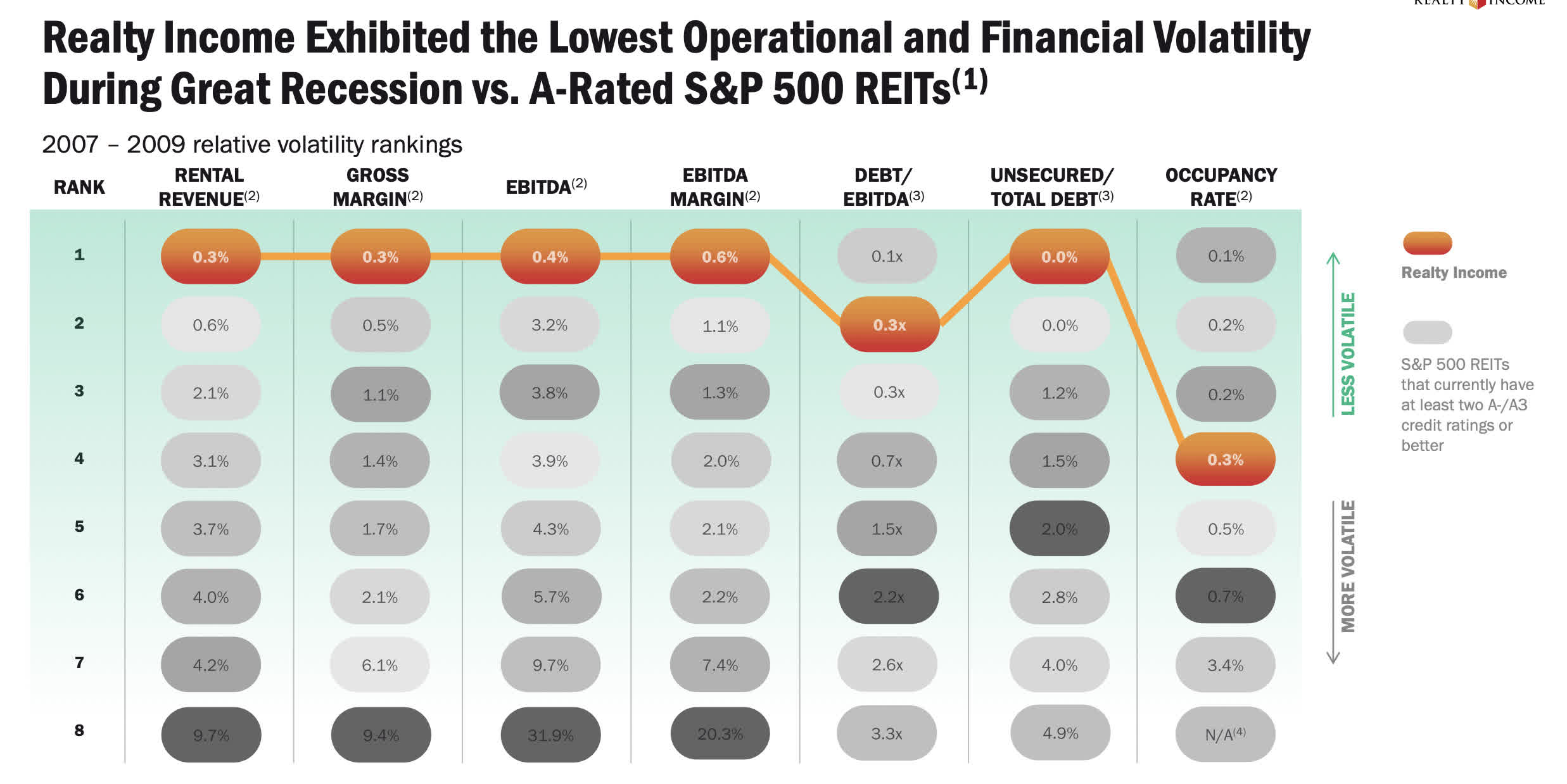

If we hit a recession

{kind=link}

Seeking Alpha

The volatility rates in revenue, gross margin, and EBITDA all ranked first amongst A/A3-rated REITs during the previous great recession circa 2007-2009. Regardless of the metric, Realty Income volatility spiked less than .5% on any of these metrics during the worst of times. As someone who worked for asset managers selling foreclosures during the 2009-2012 time frame, we are nowhere close to that terrible situation yet.

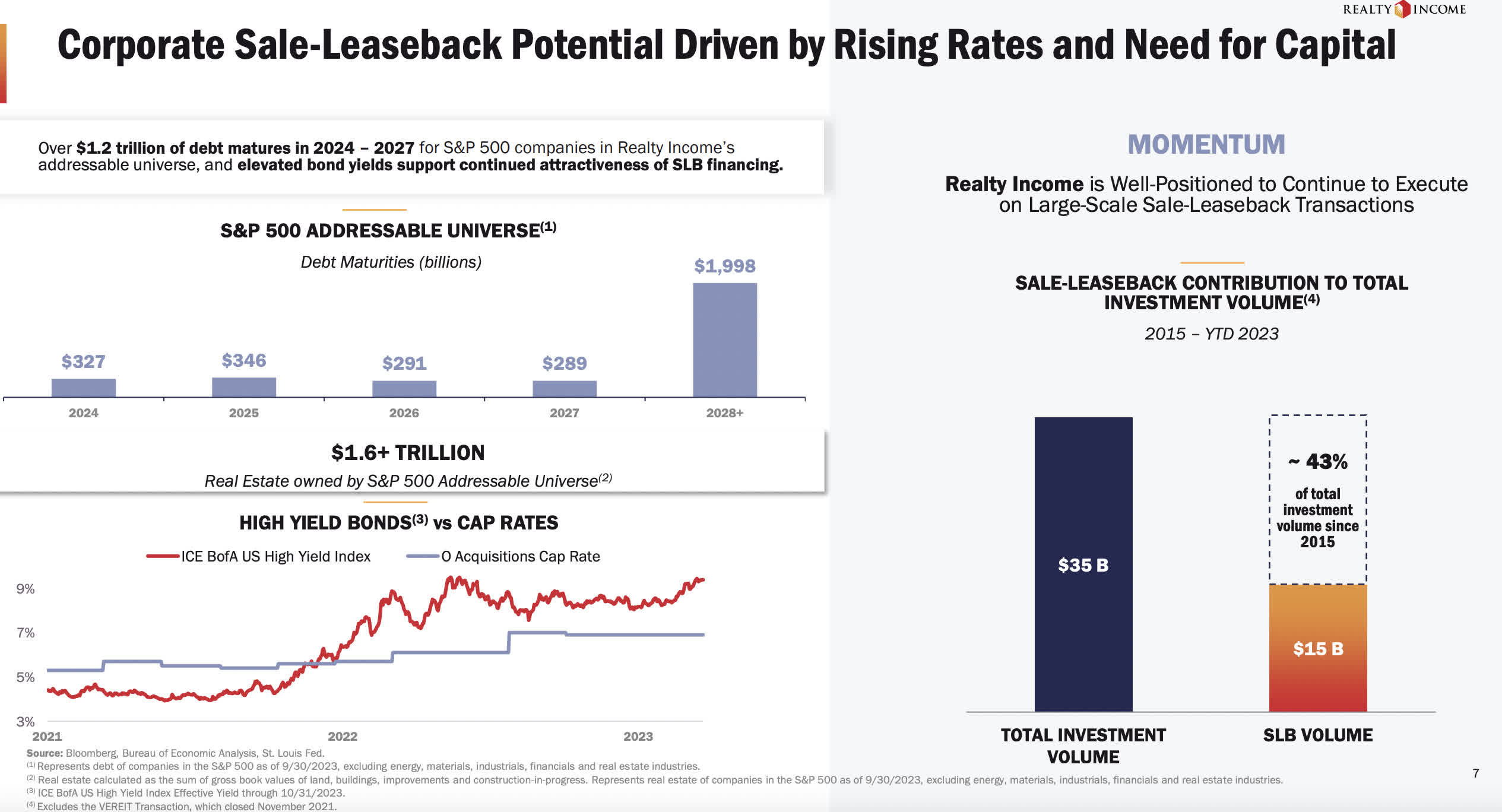

Back to sources and uses and CRE maturities

{kind=link}

Seeking Alpha

Being bullish on the most creditworthy of REITs with excess liquidity coming into the commercial real estate loan repayment periods of 2024 and beyond is logical in my opinion.

The best REITs will have the opportunity to buy commercial real estate at amazing prices from pinched operators. These will be cash-flowing from day one, with a sale-leaseback. This should be a catalyst to consider for the best REITs with the liquidity to take advantage of this situation.

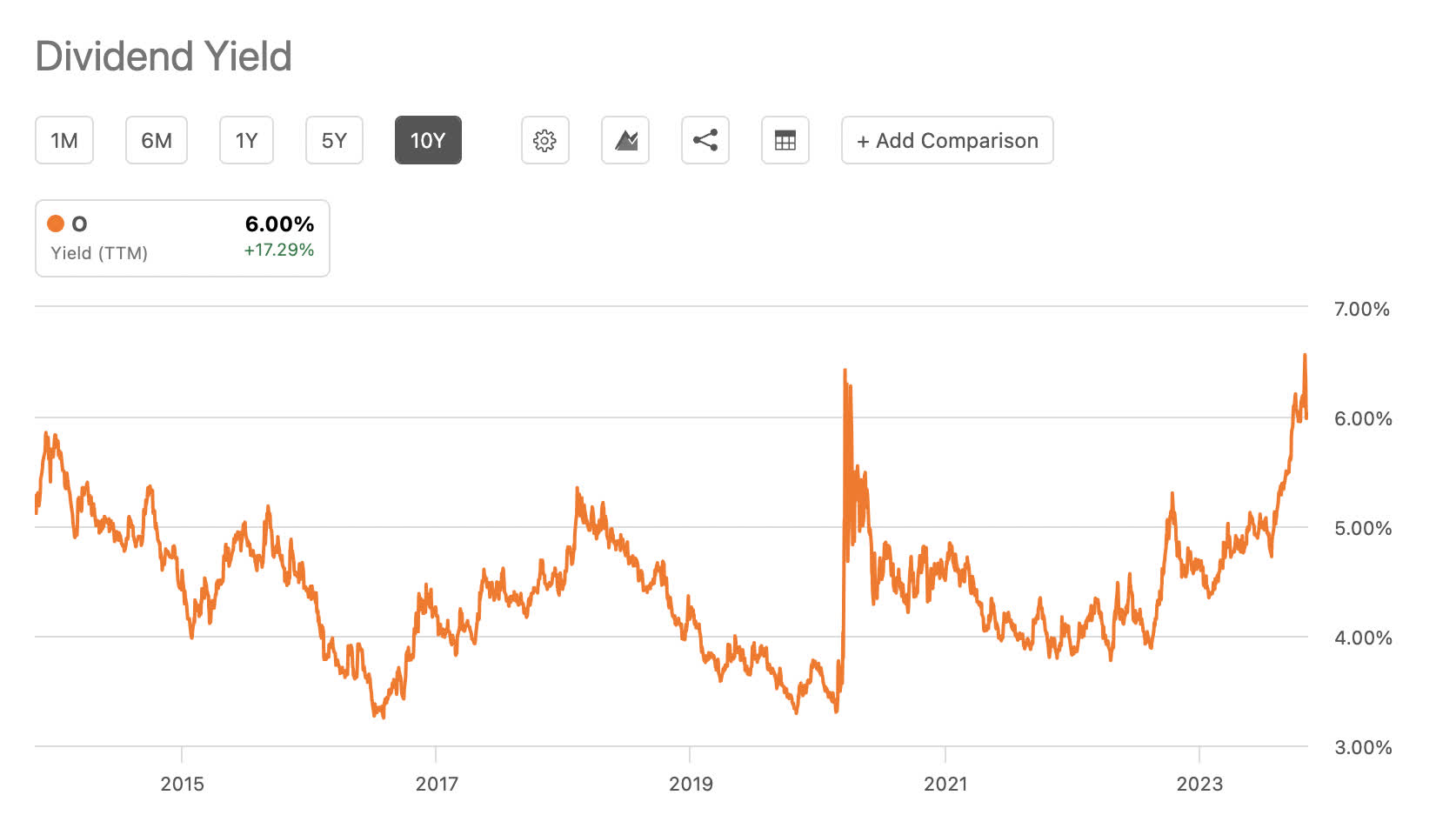

Historic yield

{kind=link}

Seeking Alpha

Discounting the Covid-19 "flash crash", we are at decade-high dividend yield levels. Regardless of net asset value, the value of one of the 3 REITs in the dividend aristocrat list selling at a decade-high yield with the highest credit rating amongst the trinity is value enough for me.

Finally, looking at the 10-year EBITDA growth compared to the price growth, we can see the lines trace one another until 2019. EBITDA has continued to grow, and yes, so have shares outstanding to acquire the growth. However, the rates of dilution versus growth in cash flow have quite a healthy spread. This is a unique historical divergence where the share price appreciation has disconnected from growth in cash flow.

Throughout Peter Lynch's One up on Wall Street and Beating The Street , you are treated to graph after graph comparing the growth rate in earnings to the growth rate in share price. Consider buying when the price growth rate is below the earnings growth rate, and stay away when the opposite is true. REITs are a bit unique because of the dilutive financing structure. Nonetheless, we can see the EBITDA growth rate [a proxy for cash flow versus GAAP EPS on non-REITs] well on the uptrend and the share price on the downtrend. Indicative of value.

Summary

I am remiss to have not put this together when Realty Income briefly dropped into the $40s. I bought as much as I could during that period and continue to do so. With the dividend yield now about 100 basis points over the risk-free rate, this is my favorite proxy to lock in the high rates that may revert south next year according to some pundits.

As rents on all types of real estate have been increasing at a rate of about 8% per year since 1940, and the fact that REITs pay nearly all their cash flow as dividends by law, the play is as close to collecting taxes with triple net lease REITs as you can get. Operating expenses also have seniority to interest payments on the debt in case a tenant goes bankrupt. They have to pay the lease even in bankruptcy unless a judge allows the tenant to reject the lease. Buy as a fixed-income proxy with a growing yield rather than static.

For further details see:

Realty Income Stock: Future Growth Opportunities In SLBs