GOLD - Recent Gold Price Downturn Is An Opportunity To Add To My Barrick Stock Position

2023-10-17 07:54:12 ET

Summary

- Barrick Gold stock declined due to the decline in spot gold prices, triggered by higher real interest rates, but it remains a must-have in a portfolio.

- GOLD stock continues to produce gold at a profit and offers investors a dividend, making it an attractive investment.

- The long-term bull case for gold prices rests on rising global debt levels combined with higher interest rates amounting to an unsustainable situation. Gold should benefit, regardless of the outcome.

Investment thesis

Barrick Gold ( GOLD ) stock saw a decline recently, in line with the significant decline in spot gold prices, while now it is back on an upswing, together with the price of gold. My overall view on gold remains that it is a must-have in one's portfolio with exposure in various forms, given the increasingly uncertain times we live in. Barrick Gold continues to produce gold at a profit and offers investors a dividend, which makes it somewhat more pleasant as a buy & hold relative to physical gold. Given the decline in its stock price from over $20/share in the Spring, I decided to add to my existing stock position in Barrick Gold, because the decline is mostly a reflection of gold price movements, not a company-specific issue, meaning that when the gold market makes its next upward move, Barrick's stock price will likely move up with it.

Barrick's financial results look solid but a soft patch will probably be experienced in the next few quarters

Barrick had decent financial results for the second quarter of this year, mostly thanks to a higher realized sales price for its mined gold. Adjusted net earnings came in at $305 million, on revenues of $2.83 billion. Revenues were more or less flat compared with the second quarter of 2022, while adjusted net earnings were 20% higher in the same quarter of last year compared with the latest quarter.

Gold production declined slightly by 3% for the quarter compared with last year, however, the realized price of gold sold increased by 6%. Barrick's long-term debt declined by 7% over the past year, to $4.8 billion. Interest expenses came in at $130 million. As a percentage of revenues for the quarter, interest costs made up less than 4.6% of total revenues. It is a little bit high for my preferences, but it is by no means unsustainable. I tend to start worrying once this ratio goes over 5% and get worried if it ever approaches 10% of revenues.

{kind=link}

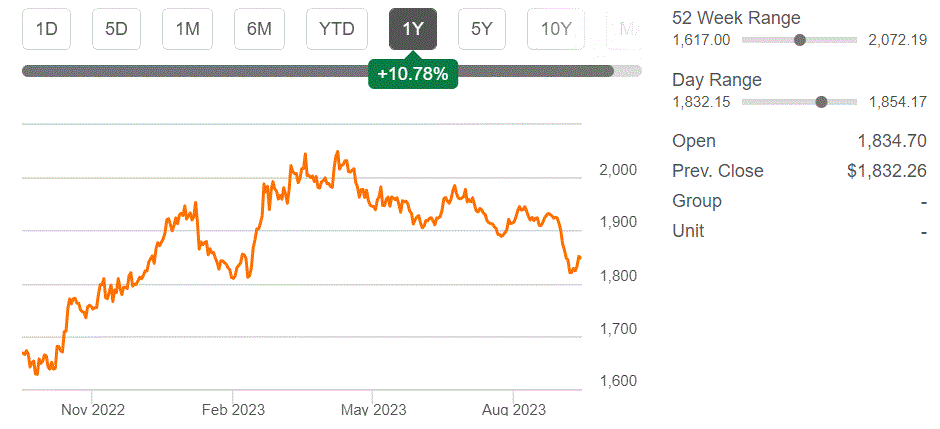

As we can see from the gold price chart, the price of gold for the third quarter will be considerably lower than it was in the second quarter. Barrick's average realized sale price of just under $2,000/ounce helped a great deal with realizing adjusted net earnings to revenues rate of almost 11% for the second quarter of the year. I don't believe earnings margins will be as generous for the third quarter. Even though I expect gold prices to rise in the current quarter, I don't think it will translate into an average realized gold sale price similar to the second quarter for Barrick. Investors should expect a few softer quarters ahead in my view.

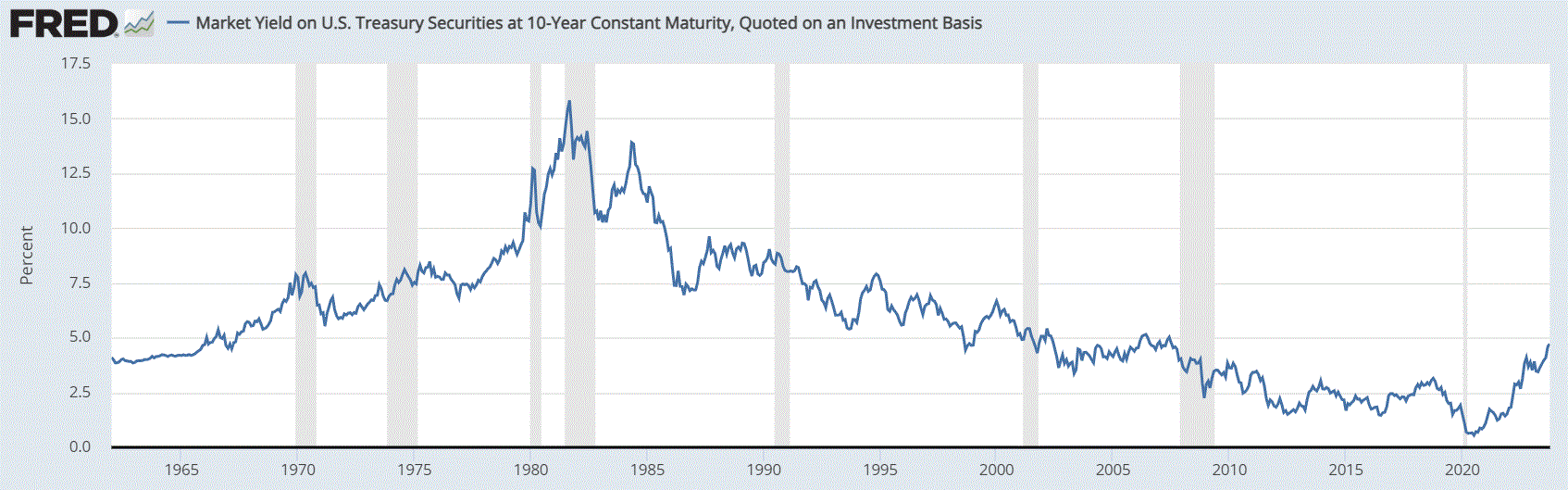

Gold price expectations going forward are based on the current negative correlation between interest rates and the price of gold

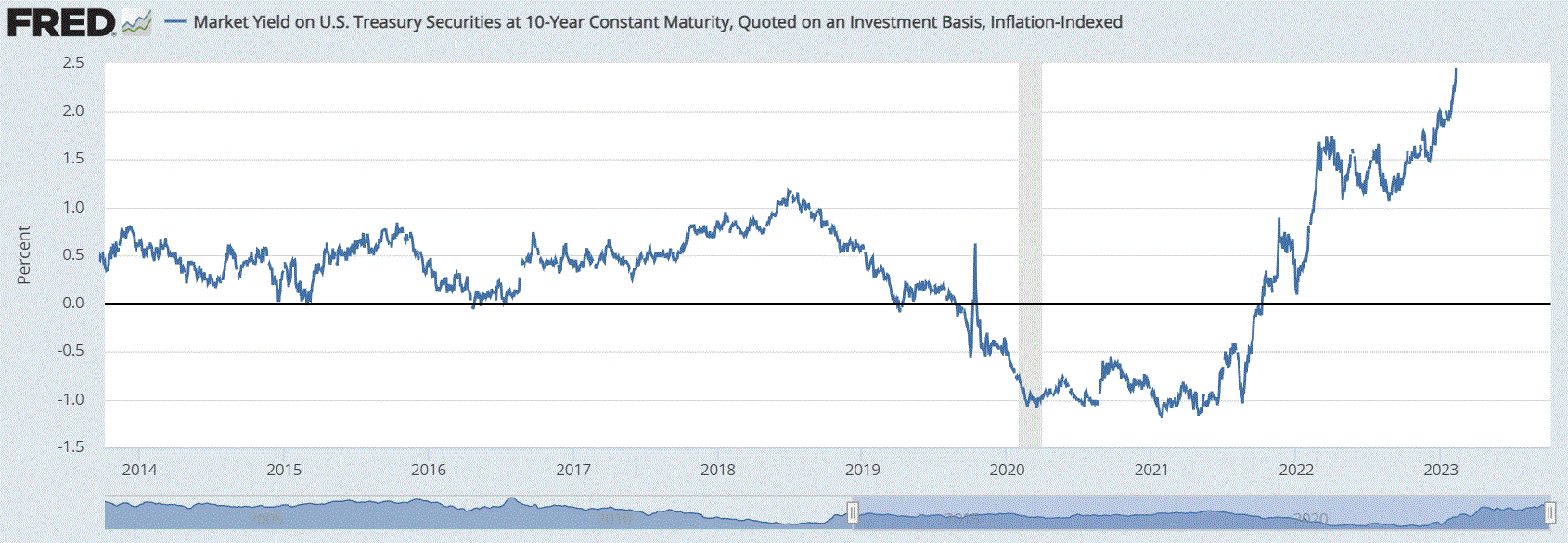

The main factor that the market seems to be looking at when contemplating the gold price outlook going forward is the progression of interest rates. Some take a more complex and arguably more relevant approach and look at inflation-adjusted interest rates as a signal regarding whether there is a case to be made in favor of a bull market in gold prices.

{kind=link}

As we can see, going by this measure, treasuries can currently provide a real wealth preservation alternative to gold, therefore in theory gold should be out of favor with the market.

{kind=link}

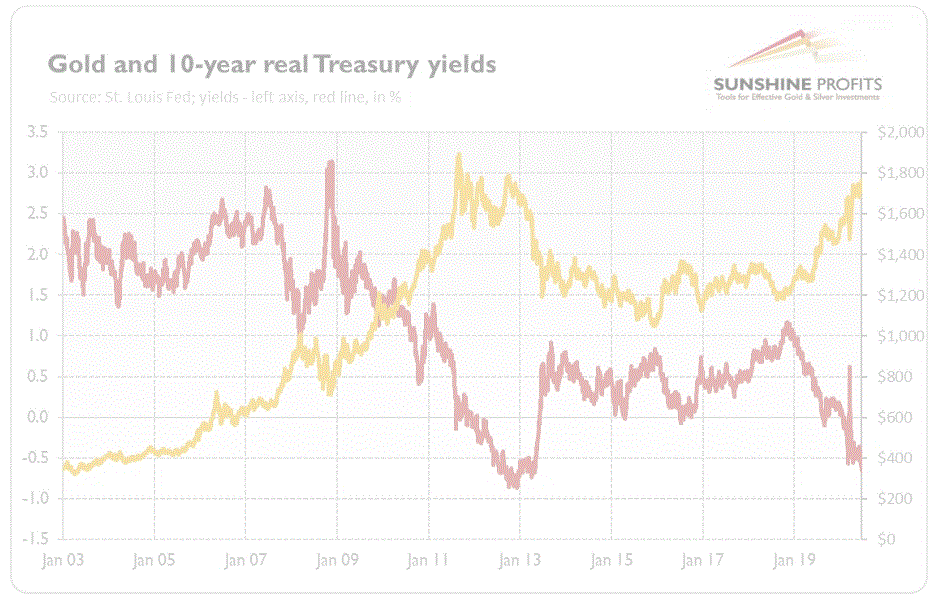

There tends to be a great deal of inverse correlation between real treasury yields and gold prices historically, especially in the past decade or so, which seems to be a trend that is currently intact.

Gold is more than just an alternate wealth preservation mechanism that the market seems to see it as, based on the above correlation. It is an insurance policy in case the fiat currency experiment, which is a relatively short one by human history standards, may see a spectacular failure. It may not necessarily be a case of a complete demise of the system, but it might degenerate into a widespread, global-scale devaluation of most of the world's currencies, with few places of refuge available to investors.

{kind=link}

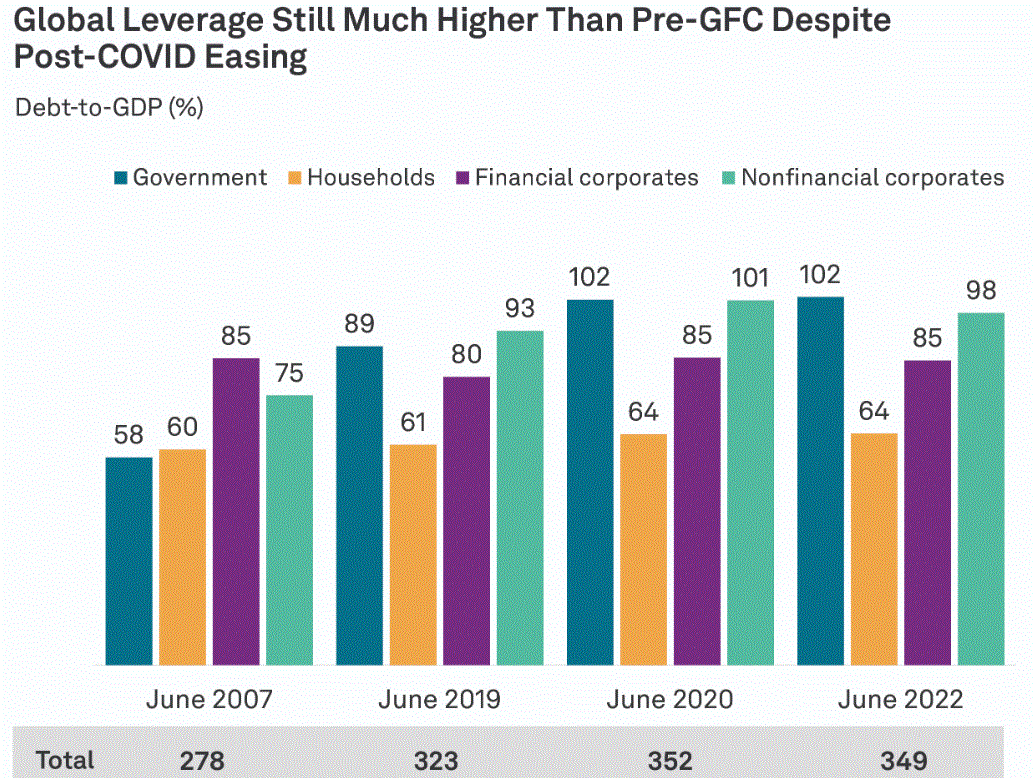

As we can see, total debt as a percentage of global GDP keeps rising. In other words, the world's economy is becoming more and more leveraged. This was fine as long as long-term interest rates kept declining in the last four decades, which helped to accommodate the higher debt/GDP load, by lowering the costs of carrying debt.

{kind=link}

Given the highly indebted global economy, it can hardly afford to cover the costs of carrying so much debt, while interest rates are rising, therefore something will most likely have to give. The timing of when something may break is uncertain, but the outcome seems less so. I see three potential outcomes that will break the current state of things, all of them mostly dependent on policy decisions, all of which are long-term bullish for gold.

A Japanification of the entire global economy (least likely to happen, but hypothetically the least painful option)

The obvious response to higher interest rates making it harder for the global economy to carry the high debt load is to drive interest rates down. In the absence of a world of plenty, it can only be achieved by pushing the world's economy into a deflationary trap. A stagnant economy would relieve the pressure on the world's supply chains to increase production which in turn should relieve inflationary pressures. With inflationary pressures low, interest rates can be allowed to decline to low levels as well, making borrowing costs easier to service. This would arguably be a positive for gold since low interest rates will make treasuries and other debt instruments unattractive.

A well-managed deflationary trap might be perhaps the least painful way out, but it is unlikely to occur. Most of the world's population still lives in conditions where most basic needs that we take for granted are not met, like electricity in the household or clean water for instance. Transport infrastructure is also deficient in many parts of the world, even as population growth continues at a robust pace. All these needs require an expansion in commodities demand, as well as demand for finished goods & services, therefore the Japanification of the entire world economy does not seem viable.

Inflate the debt away

When the debt load reaches levels that become unsustainable to service, especially within a context of rising interest rates, the easiest path to rebalancing the economy is arguably to let inflation get out of control, in effect bailing out the indebted to the detriment of savers. If central banks decide on this path as a way out of the debt trap we seem to be getting stuck in, real yields will most likely go into negative territory once more, even if nominally speaking yields will rise. In this scenario, bonds will lose their wealth-preservation role, thus parking wealth into tangible assets, such as gold becomes more attractive. If I were to bet on what the most likely chosen path would be, this is the most likely one, although the timing of it is still uncertain.

Massive defaults at personal and corporate levels, with several smaller sovereign states potentially also defaulting

There is always the possibility that central banks and governments will let higher interest rates take their toll and allow consumers, companies, and even local and sovereign governments to go into default. This outcome is the least likely to be allowed to occur in my view, because of the systemic damage that it might inflict on the global financial system. There is no telling how the systemic risks will play out if we just allow for defaults to occur as a means to rebalance the global economy, which is why I doubt that anyone wants to risk it. If it were to happen, however, it would most likely lead to a flight to safety which should benefit gold prices.

It is difficult to tell whether we are at the point of reckoning regarding the worsening debt leverage situation that we see throughout the world, combined with what now seems to be the end of the road for the four-decade period of declining interest rates. We could be at that point, or perhaps we still have many more years to go, before one of the three possible paths will be taken. At this point, I doubt that the situation will rebalance itself. I thus see gold prices headed higher for the long term, although the timing of it might not be entirely certain.

Barrick has the reserves, and its mining operations produce gold at a cost that is significantly below current gold price levels

The reason why I tend to dwell on the big picture of macro-factors that may affect the economy or segments within it is that I like to invest in companies that have prospects of long-term success. I see the confirmation of solid long-term fundamentals for any particular position within a certain sector as being an extra layer of safety, where short-term factors that may drive any particular stock down can be waited out until those short-term factors dissipate and the longer-term fundamentals kick in. The obvious aspect that is needed to make it work is the overall financial health of the company, as well as its other fundamentals. In this particular case, I already covered the financial fundamentals, which look overall solid. As a mining stock, the main company-specific fundamentals aside from the financial aspect are reserves and the current cost of producing those reserves.

Barrick Gold currently has 1,400 Tonnes of proven & probable gold reserves in place as of the end of 2022. That is equivalent to 49.4 million ounces. Current production is going at a rate of about 4 million ounces per year, with about a million ounces produced quarterly on average. In other words, it has enough resources to produce at current levels for about 12 years. By comparison, The estimated global gold reserves to production ratio is about 19 years. Some of the entities with longer production lives are however uninvestable because they may be state-owned, may be located in countries under sanctions, or because some reserves are counted as a by-product within mining operations that target different minerals.

{kind=link}

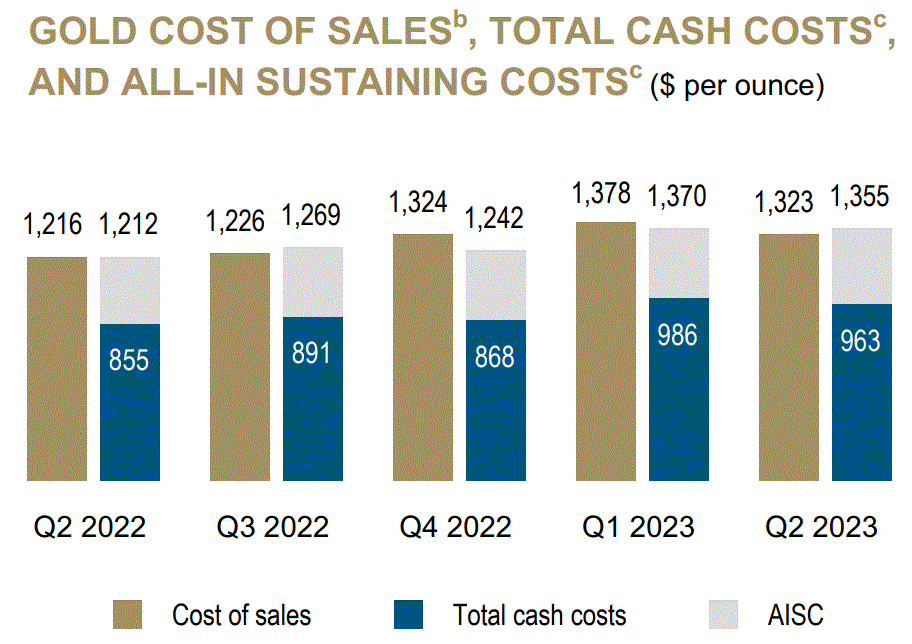

Based on its financial results as well as its internal estimates on production costs, Barrick currently seems to have a decent potential profit margin above its all-in breakeven costs, given that gold prices seem anchored in the $1,800/ounce range for the time being. It should be noted that there is some positive correlation between AISC costs and certain inputs such as oil prices, which could impact Barrick Gold's breakeven level, given that oil prices are trending upwards. However, it should also be noted that gold and oil prices are also historically correlated to a great extent.

Investment implications:

I added to my already existing position in Barrick Gold stock once it went under $15/share. Given its forward P/E ratio of just over 17 currently, I do not see a great deal of sustained downside to its stock price. If there is to be a severe decline in gold prices, which I see as very unlikely in the current global economic & geopolitical context, Barrick stock will most likely decline significantly in price from current levels. I expect any such decline to be relatively short in duration, and if that is the case, I am prepared to add more to my position. Its dividend yield of 2.6% makes it extra attractive to buy & hold this stock for the long term, while I feel somewhat confident in my higher long-term gold price trajectory thesis.

The more likely source of risk to my bullish thesis on this stock comes from Barrick's business strategy. I am referring to its major project development in Pakistan , which changes Barrick's geopolitical risk profile, given that Pakistan itself has been a less than stable country recently, and it is located in a somewhat unstable region, next to India, its rival, as well as Afghanistan & Iran. The project itself is set to shift Barrick's minerals production profile, more toward copper, given that at recent market prices, the Pakistani project could add about $1.2 billion/year in gold revenues, as well as $3 billion in copper revenues, with half of the revenues attributable to Barrick from the project. I should note that my thesis on a bleak economic trajectory going forward could mean that Barrick's growing copper footprint could become a financial liability, therefore it can have a net-dampening effect on any benefit it may see from its gold segment.

While there may be some risk to my thesis, ranging from gold prices doing the unexpected and declining for the foreseeable future, to rising geopolitical risks, I feel that Barrick's current valuation, trading at a P/E that is roughly 2/3 of the ratio of the overall market is a good entry point, with reduced risks from current stock price levels. While there are some risks to my bullish thesis, if the thesis turns out to be roughly accurate, Barrick Gold is a company that will benefit from it a great deal. One particularly enticing aspect of it is that unlike being invested in physical gold, where one just waits for the desired price movement to happen, Barrick pays a dividend while waiting for the thesis to play out, which is why I currently prefer it to the alternative of buying more physical gold.

For further details see:

Recent Gold Price Downturn Is An Opportunity To Add To My Barrick Stock Position