VLO - Recession? 3 Terrific Dividend Stocks To Buy On Weakness

Summary

- In this article, we start with a macroeconomic discussion, given a high probability of severe economic weakness in 2023.

- To be prepared, I am building a bigger war chest and a watchlist of cyclical dividend stocks I want to buy on weakness.

- Hence, this article is dedicated to three of my all-time favorite cyclical dividend growth stocks I'm buying when demand weakness hits.

- All three stocks are likely to outperform the market on a long-term basis. All of them offer a decent dividend yield and high (expected) dividend growth.

Introduction

I sometimes joke with my friends that we have a win-win dividend growth strategy. We win when the value of our stocks appreciate (obviously). However, we also make the case that we win during recessions, as we get to add to the stocks we love at great prices.

Needless to say, there are a lot of strings attached. The first one is that this only works with top-tier quality stocks. Consistently adding to bad companies is an easy way to burn money. Also, it doesn't work for investors in need of cash, which creates a limited ability to buy stocks on weakness.

With all of this being said, 2023 is expected to be the first recession year since 2020. If my assessment is even remotely correct, we could see a stock market decline that moves the S&P to the low 3,000 range.

To be prepared for that, I increased my savings rate and my total cash position to buy larger corrections whenever they occur.

Hence, I'm very excited to share three of my all-time favorite stocks to buy during recessions.

All stocks are likely to fall during recessions due to cyclical characteristics. However, all companies in my selection are in a good spot to recover and deliver long-term outperforming returns.

They all have decent dividend yields, high historic dividend growth, safe payout ratios, and secular tailwinds that are often overlooked.

So, without further ado, let's dive into it!

A Quick Note

But first, I need to explain one thing. In dividend (growth) investing, time in the market, more often than not, beats timing the market. I am in no way trying to keep people from investing or trying to use the "recession" for click bait purposes - fear sells. My only goal is to discuss the economic situation and the high likelihood of more stock price weakness. While I am consistently adding to my holdings, I am building a bigger cash position as I believe that I can time the market - at least well enough to provide myself with a bit of an edge.

If I'm wrong and stocks take off, the biggest risk I will encounter is not having bought more shares at current prices. I will miss some upside. However, I will still have invested more than 90% of my net worth in dividend stocks. So, either way, betting on more stock market weakness comes with a risk/reward that I can tolerate.

Also, my biggest and best investments were all made during times of distressed market conditions or bigger corrections. I hope to do it again in 2023.

Recession Opportunities

On December 22, I wrote an article covering my outlook for 2023.

A big part of my outlook is based on my belief that the Federal Reserve cannot waste any time in its fight against inflation. According to Lawrence McDonald , roughly $10 trillion in government bonds are maturing in 2023 and 2024. When adding higher interest rates, the government could see a surge of $600 billion in debt servicing costs...

Hence, I believe there is an important time component when it comes to the Fed fighting inflation. As I wrote in my outlook article:

- The Fed is feeling tremendous pressure to control inflation. That makes sense as the US economy is consumer-driven. Also, high inflation can quickly turn into lasting above-average inflation once wages and spending habits adjust. That's a no-go!

- Hence, I believe that the Fed will not be afraid to do damage to the US economy to achieve its target of lower inflation. This includes hurting housing demand/prices, unemployment, and consumer spending.

- Once the Fed pivots (I still believe it will happen in 2023), the economy will slowly adjust to lower rates. Demand will come back. So will inflation.

- Given the aforementioned secular factors, I believe we are in a prolonged period of Fed hikes and cuts at above-average rates (versus 2009-2021).

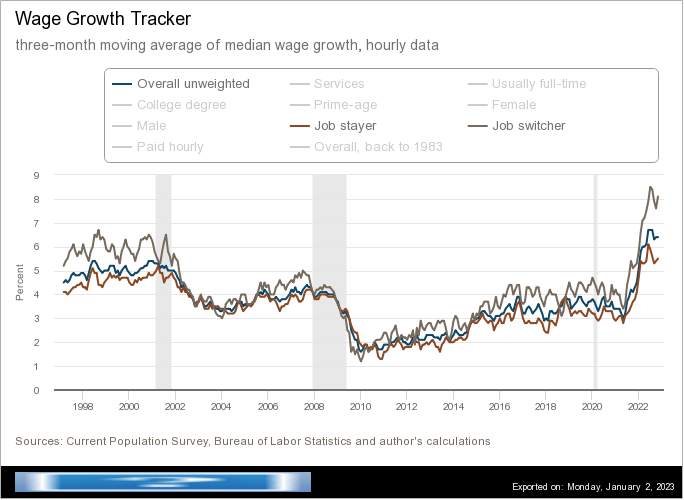

One of the reasons why I believe that the Fed will have to do economic damage is wage growth.

Wage growth remains red-hot as structural problems provide fertile ground for higher wages despite slower overall inflation and declining economic growth.

According to the Wall Street Journal :

Faster wage growth is contributing to historically high inflation, as some companies pass along price increases to compensate for their increased labor costs. Prices rose at their fastest pace in 40 years earlier in 2022. Inflation has cooled in recent months but remains high. Federal Reserve officials are closely monitoring wage gains as they consider future interest-rate increases to slow the economy and bring down inflation.

{kind=link}

But wait, it gets worse. The US economy is already very far in a slowing cycle. This means that additional pressure from the Fed could easily push the economy over the edge.

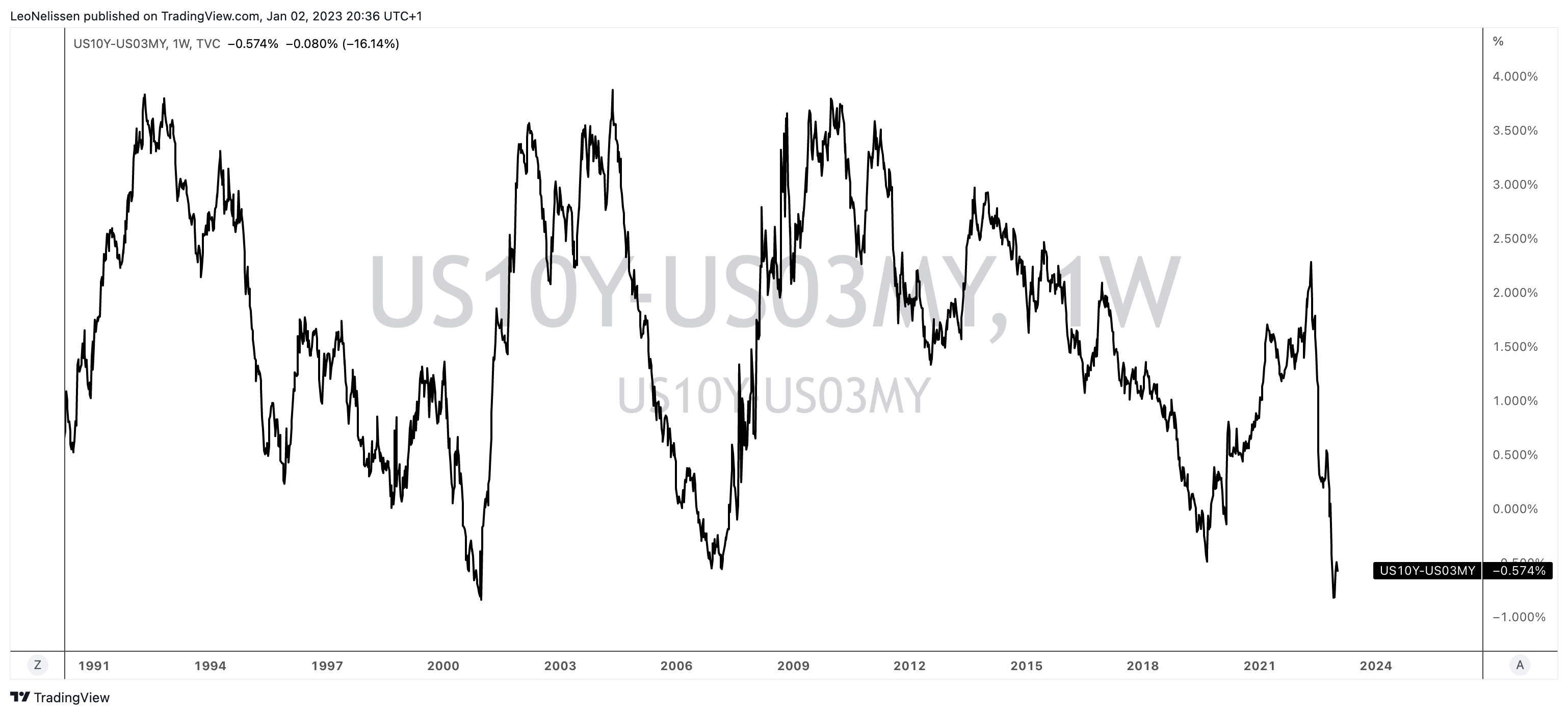

The Fed's favorite recession indicator, the ten-year minus three months yield curve, hasn't been this inverted since the early 2000s.

{kind=link}

Now, even major banks are coming out, making the case for a recession. According to the Wall Street Journal :

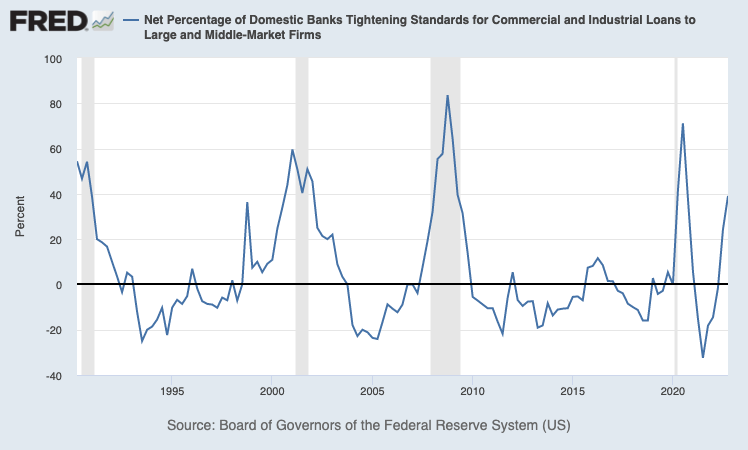

The firms, known as primary dealers, are a collection of trading firms and investment banks that include companies such as Barclays PLC, Bank of America Corp., TD Securities and UBS Group AG. They cite several red flags: Americans are spending down their pandemic savings. The housing market is in decline, and banks are tightening their lending standards.

“We expect a downturn in global GDP growth in 2023, led by recessions in both the U.S. and the eurozone,” economists at BNP Paribas SA wrote in the bank’s 2023 outlook, titled “Steering Into Recession.”

In this case, banks have started to tighten lending standards, something that's very typical for a recession.

{kind=link}

I think a perfect storm is emerging of much weaker economic growth and the need to fight inflation. It's why I expect leading economic indicators to weaken until at least the second half of 2023.

It's also why I expect the S&P to fall again to the low 3,000 range before an attractive risk/reward triggers the return of buyers.

With that said, if I'm right, I will suffer as I have more than 90% of my money invested in long-term dividend stocks. However, it also means we get new opportunities, which I'm very excited about. After all, using recession opportunities can tremendously enhance one's ability to generate long-term wealth.

Hence, allow me to present you some of my all-time favorite dividend (growth) investments on weakness.

1. Caterpillar ( CAT ) - 2.0% Yield

Caterpillar was one of my first dividend growth holdings in 2020. Back then, I bought the stock with a great yield thanks to the impact of the pandemic on stock market valuations. This producer of yellow heavy machinery is now located in Irving, Texas, after leaving Illinois like so many other people and corporations.

Caterpillar isn't necessarily the perfect stock for my portfolio. After all, it is very capital intensive, it operates in a very competitive industry with peers like Liebherr, Volvo, and Komatsu, and it is extremely cyclical.

Over the past ten years, the stock has outperformed the market by slightly more than 20 points (including dividends). However, the chart below also shows that investors have been through three major corrections.

The 2015/2016 manufacturing recession resulted in a market cap loss of roughly 50%. The pandemic sell-off was shorter, yet of similar magnitude. Last year, the stock briefly lost more than 30%.

Generally speaking, these sell-offs aren't a problem if you know:

- T hat they will continue to occur regularly (know what you own).

- H ow to deal with it (use it to your advantage).

What makes these sell-offs worth dealing with is CAT's dividend.

Caterpillar has a stellar Seeking Alpha dividend scorecard showing high dividend consistency (CAT is a dividend aristocrat!), yield, growth, and safety.

{kind=link}

The current dividend yield is 2.0%, based on a $1.20 per quarter per share dividend. While this is nothing to write home about, dividend growth is strong.

The 10-year average annual dividend growth rate is 9.0%, which is very satisfying. The dividend payout ratio is 36%.

Moreover, the stock is currently benefiting from strong secular growth.

In October, I wrote an article covering this secular tailwind, which provided the company with very high EPS growth despite economic growth slowing.

Bloomberg

The energy transition is about to cause significant material shortages for decades to come, which makes mining investments more important than "ever".

According to the company :

In Resource Industries, our mining customers continue to exhibit capital discipline. However, commodity prices remain supportive of continued investment despite trending lower recently. We expect production and utilization levels will remain elevated, and our autonomous solutions continue to gain momentum. I’ll highlight an example in a moment.

We expect the continuation of high equipment utilization and a low level of park trucks, which both support future demand for our equipment and services. We continue to believe the energy transition will support increased commodity demand, expanding our total addressable market and provided opportunities for profitable growth. In heavy construction and quarry and aggregates, we anticipate continued growth in the fourth quarter.

In other words, Caterpillar is a great buy during a recession as it gives us a better yield (I'm aiming to buy at a 2.5% yield, excluding dividend hikes), a business model capable of high dividend growth, and strong secular growth making outperformance very likely.

2. Norfolk Southern ( NSC ) - 2.0% Yield

Most of my long-term readers won't be surprised that I'm putting a railroad stock in this article. I love the value most Class I railroads bring to the table. The only problem is that most are very cyclical.

However, that's perfect for the sake of this article as recession corrections offer tremendous opportunities.

Norfolk Southern is an Atlanta-based Class I railroad covering the Eastern half of the United States with its peer CSX Corp. ( CSX ).

Norfolk Southern

The company is the nation's largest intermodal (containers and trailers) railroad with exposure to all other major transportation groups as well.

Just like Caterpillar, there are two major reasons why I like Norfolk Southern.

- The company is a terrific dividend growth stock.

- It benefits from a secular tailwind.

In a recent article , I covered the company's ability to benefit from supply chain re-shoring.

I expect that over the next 10-15 years, we'll see a significant shift in supply chains. Manufacturing in the United States is strengthening with support from Mexico and Canada. Producers are leaving China due to geopolitical and economic risks. European producers are being pressured by high energy costs and unfavorable business developments. They move production closer to the consumer.

Moreover, according to a Bloomberg report:

According to a report Wednesday, Deloitte said some 62% of manufacturers it surveyed have started reshoring or near-shoring their production capacities. The survey included 305 executives at transport and manufacturing firms, mostly in the US, with annual revenue of $500 million to more than $50 billion.

American firms are expected to reshore almost 350,000 jobs in 2022 -- an increase of 25% from 260,000 in 2021, according to figures cited in Deloitte’s ‘Future of Freight’ report. Ultimately, the shift could reduce by 20% the share of Asia-originating shipments to the US by 2025 and by 40% by 2030, it said.

Norfolk Southern has bet on these tailwinds since 2013, as it works on servicing new factories in the United States, emerging market opportunities via ports, and energy investments (among others).

Concerning its dividend, the company currently pays a $1.24 per share per quarter dividend. This, too, translates to a 2.0% yield.

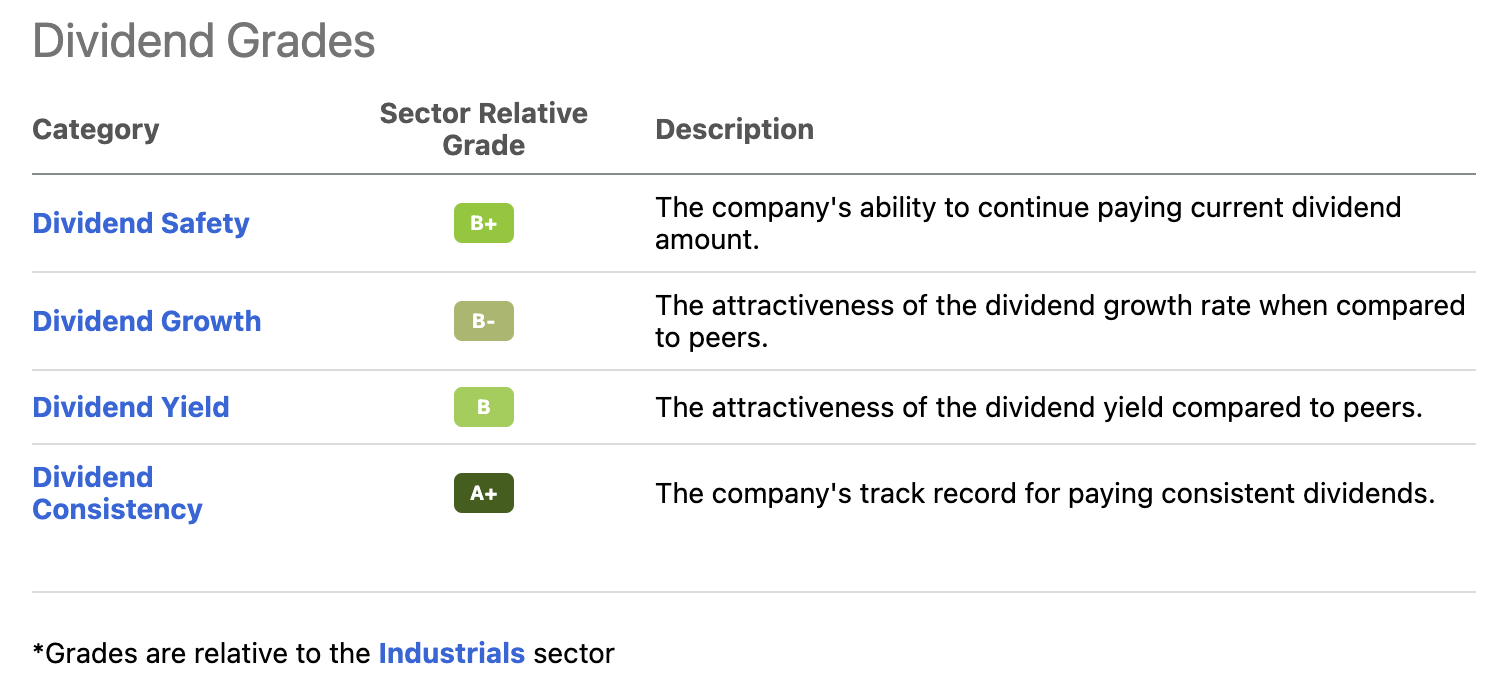

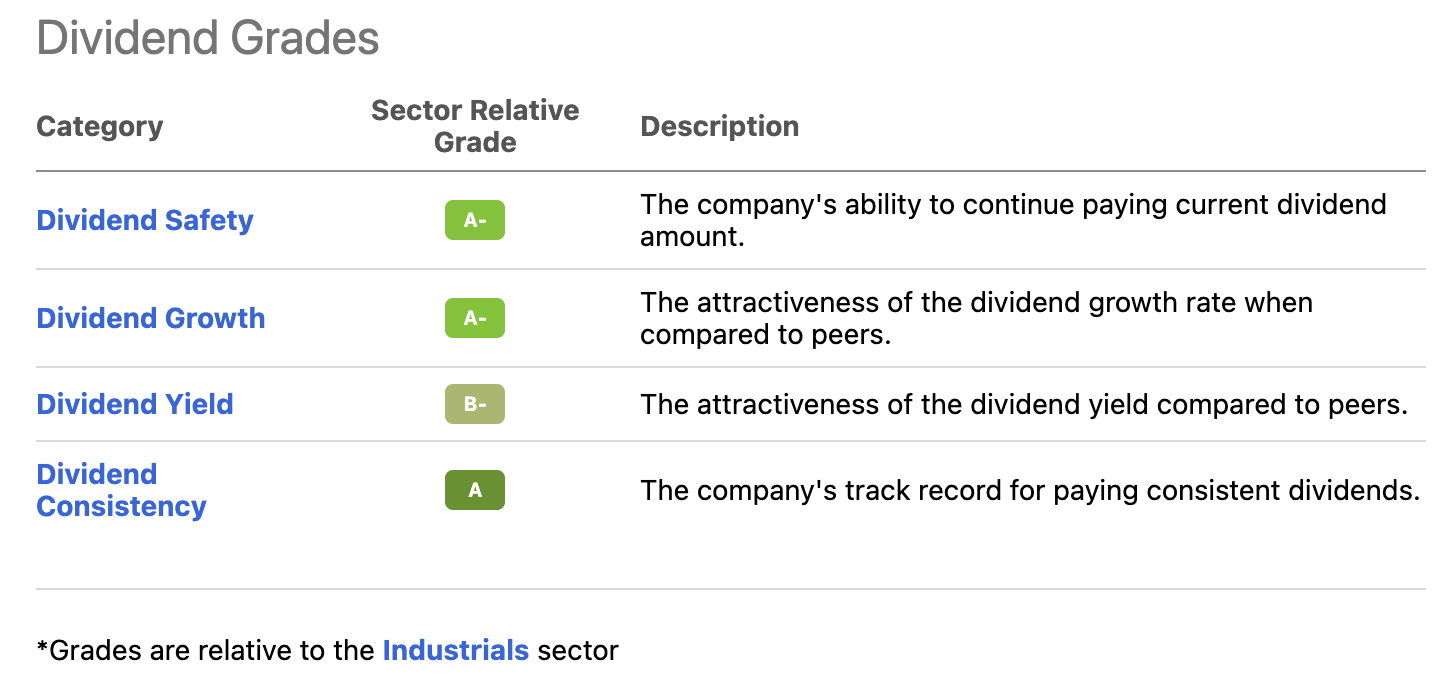

While a 2.0% yield isn't exciting, it comes with an even better dividend scorecard than Caterpillar. The company scores higher on safety and growth, thanks to the 15.2% average annual dividend growth rate over the past five years. The dividend payout ratio is 37%.

{kind=link}

The most recent hike was announced on January 25, 2022, when management hiked by 13.8%.

Moreover, the company has a long history of outperforming the stock market.

Over the past ten years, NSC shares have returned 384%, beating the S&P 500 quite consistently and by a wide margin. Even steep recession sell-offs were not able to ruin this outperformance.

Going forward, I expect NSC to maintain its long-term outperformance. However, I believe that the stock may fall back to $200 (or lower) if we indeed enter a somewhat severe recession.

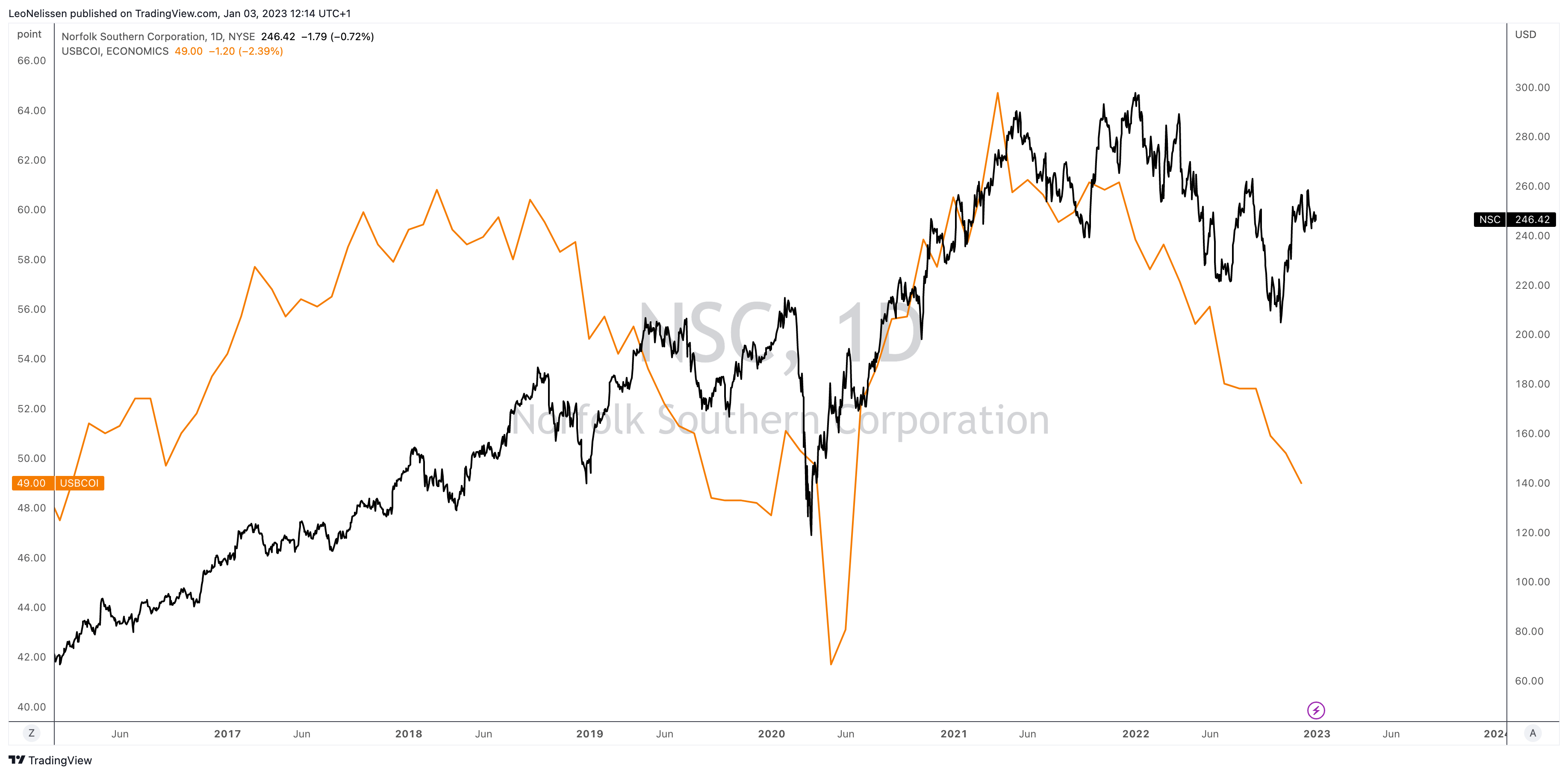

Last year, I aggressively added to NSC close to $200 per share. I am planning on doing that again. If economic indicators like the ISM index (orange line in the chart below) are any indication, the odds are in our favor of buying NSC lower again.

{kind=link}

Now, onto number three.

3. Valero Energy ( VLO ) - 3.1% Yield

I initially wanted to go with its peer Marathon Petroleum ( MPC ). However, as I already gave you two stocks with somewhat low yields, it's time for a higher yield.

Valero was the first dividend energy stock I bought for my dividend portfolio in 2020. Back then, I got in cheap as a result of the pandemic, which annihilated fuel demand.

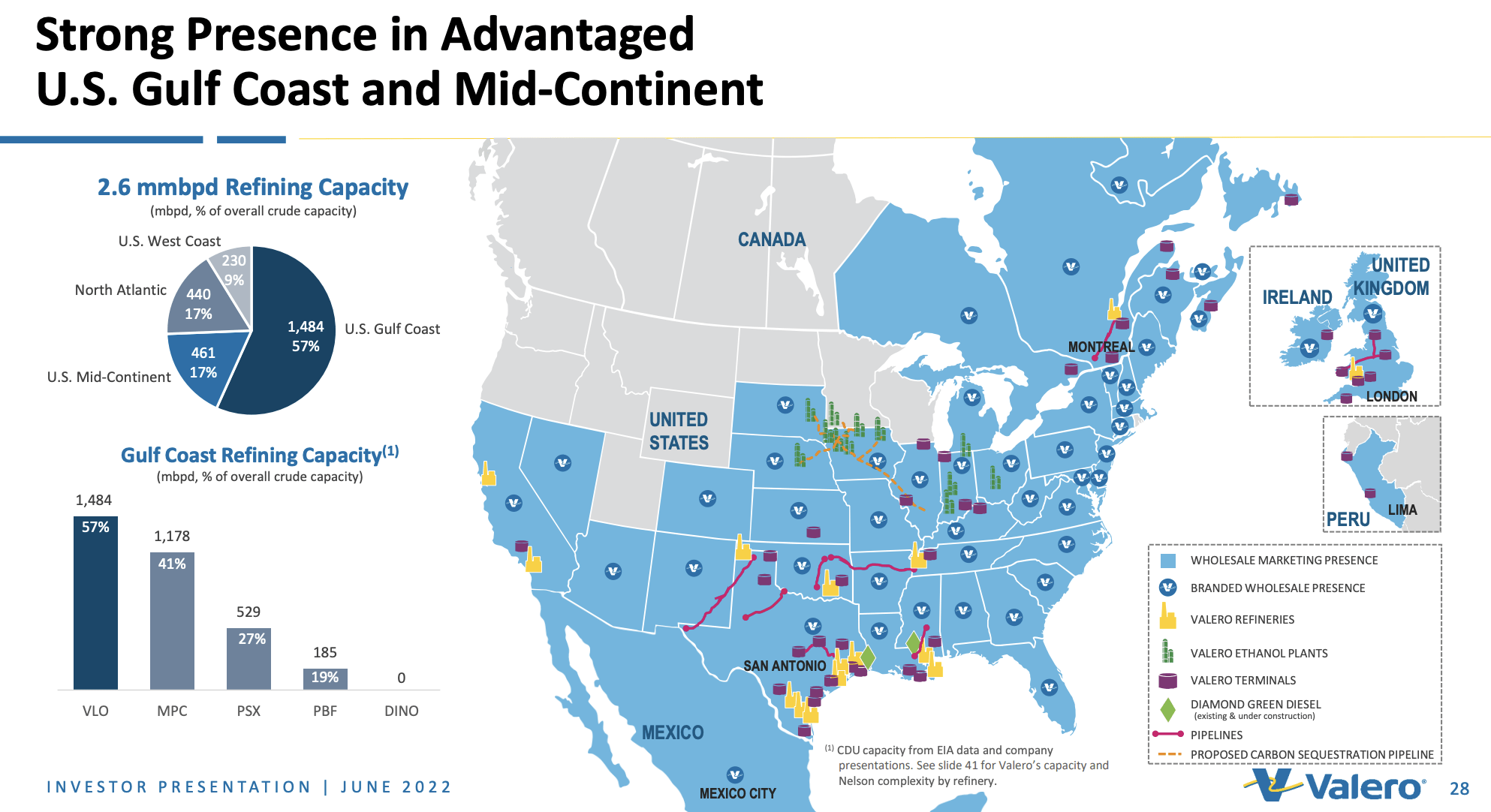

Valero is one of America's largest refiners, turning oil into a variety of fuels and byproducts. The company has 15 petroleum refineries in the US, Canada, and the UK with a capacity of 3.2 million barrels per day. As the map shows, most of these assets are located on the Gulf Coast, which allows for good access to feedstock and export facilities to satisfy overseas demand.

{kind=link}

The company also produces renewable diesel in its Diamond Green Diesel joint venture, as well as 1.6 million gallons of ethanol per year. These assets are mainly located in the Midwest where it has access to high-quality corn.

In 2022, the company returned close to 90% as it benefited from rising post-pandemic demand and global fuel shortages.

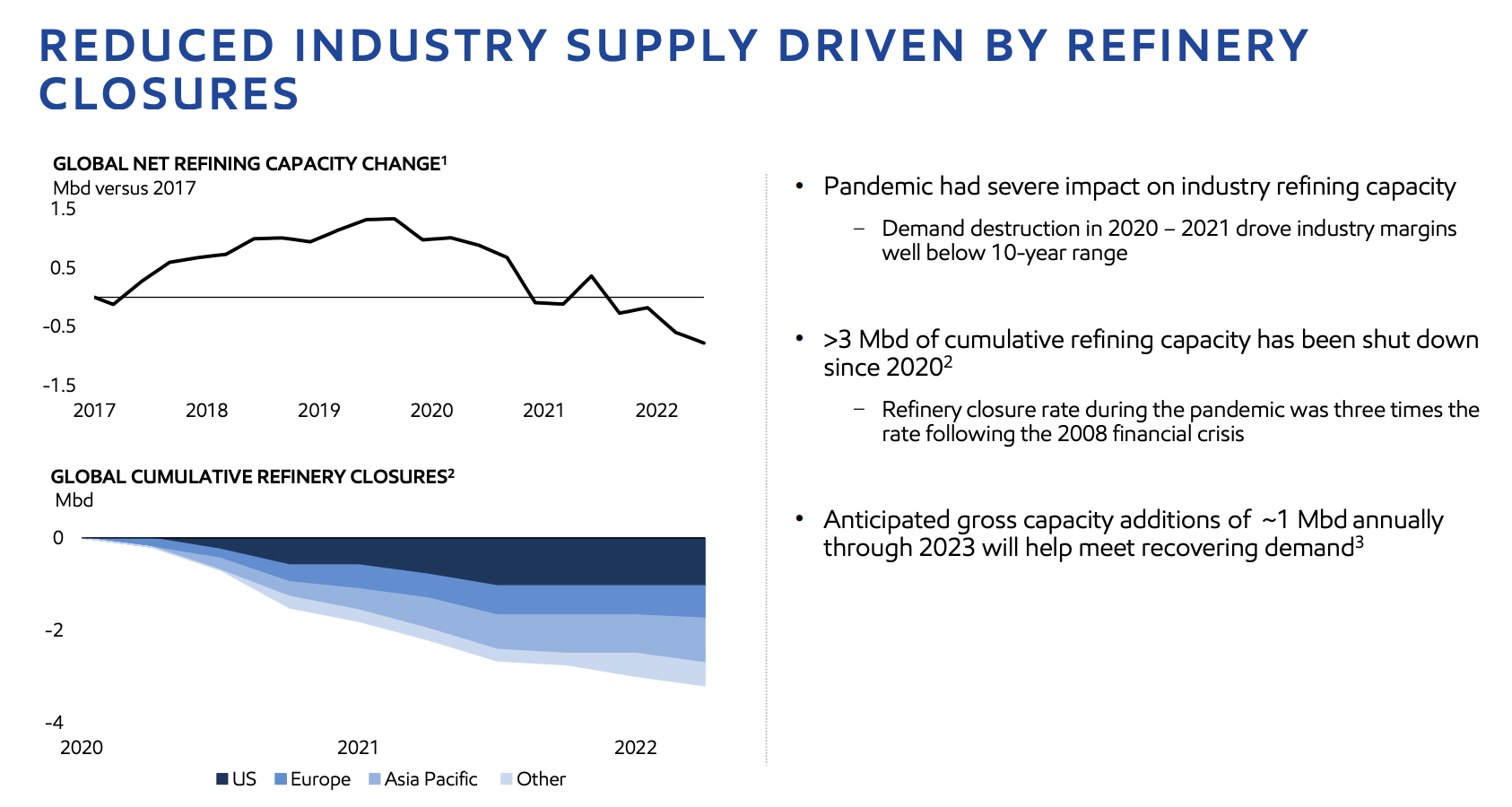

Global refinery supply has been declining since 2020 as producers shut down facilities as a result of lower demand. Meanwhile, western nations did not invest in new facilities due to environmental reasons.

{kind=link}

While these reasons will keep supply tight for many years to come, I believe that Valero will dip at least 25% at some point in 2022 - as I discussed in this article .

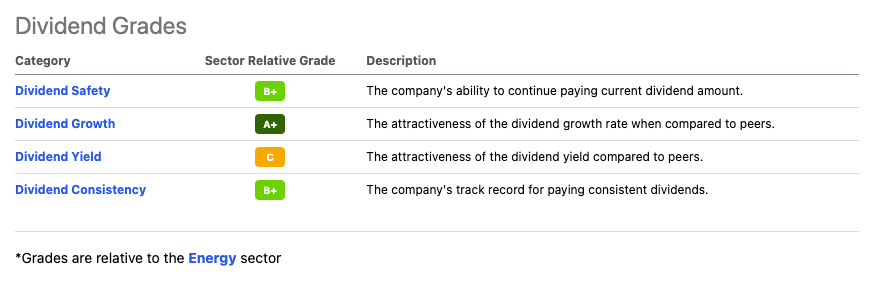

Valero currently yields 3.1%, which is one of the lowest yields since pre-pandemic times.

Hence, the company's dividend scorecard shows a relatively low score on its yield.

{kind=link}

Valero also hasn't hiked its dividend since January 2020. In 2020, it did not have enough money to cover maintenance costs (due to lockdowns). However, instead of cutting its dividend, it maintained the dividend. This resulted in higher debt. The company has used the past two years to reduce debt instead of hiking its dividend.

Yet, the 10-year compounded annual dividend growth rate is still 20.8%. The payout rate is just 17%.

Despite slower economic growth, I expect Valero to hike its dividend in 2023. This is what I wrote in the aforementioned article :

The company itself did not mention a specific target date to hike the dividend. It is trying to assess the changing macroeconomic environment and looking to lower its debt-to-capital ratio to the lower end of the 20% to 30% range. Right now, that number is 24.5%.

In other words, I'm positive that the first half of 2023 will see a dividend hike. The size of that hike will likely depend on the company's macroeconomic outlook.

Moreover, like the other stocks in this article, VLO is very volatile and prone to large sell-offs. However, it always bounces back when demand rebounds, resulting in high long-term outperformance.

Now, onto my closing thoughts.

Takeaway

I don't know at what level the S&P 500 will trade the next time we wish each other a Happy New Year. However, I strongly believe that 2023 will offer some fantastic buying opportunities as the recession might be worse than expected.

In this article, we discussed my view on 2023, which includes my expectations of a retest of last year's stock market lows.

However, instead of panicking, I'm working on a watchlist of high-quality stocks to buy at great valuations.

In this article, I presented three of my favorite cyclical dividend growth stocks. Stocks with great historic dividend growth, stellar (buy cyclical) business models, safe payout ratios, and the ability to generate outperforming total returns on a long-term basis.

If things go according to plan, I will use the war chest I'm building to aggressively add to these stocks.

I have more stocks on my list, so prepare for more model portfolios and discussions of interesting recession opportunities in the weeks and months ahead.

Let me know your thoughts in the comment section! Do you think I'm too bearish? What are you doing differently in 2023? What stocks are you watching?

(Dis)agree? Let me know in the comments!

For further details see:

Recession? 3 Terrific Dividend Stocks To Buy On Weakness