QQQA - Recession Is Not The Issue For Markets - Inflation Is But Disinflation Is Around The Corner - Markets Will Be Just Fine

- The market (SPX) leads changes in GDP by at least 1 quarter. In fact, the SPX impacts GDP, instead of other way around - transmission is via looser Financial Conditions.

- The latest Nonfarm Payroll data (June 2022) should loosen Financial Conditions even further.

- It doesn't matter that the Fed Fund Rate is rising. The FFR is a severely lagged variable -- Fed severely behind the curve. It only affects market sentiment.

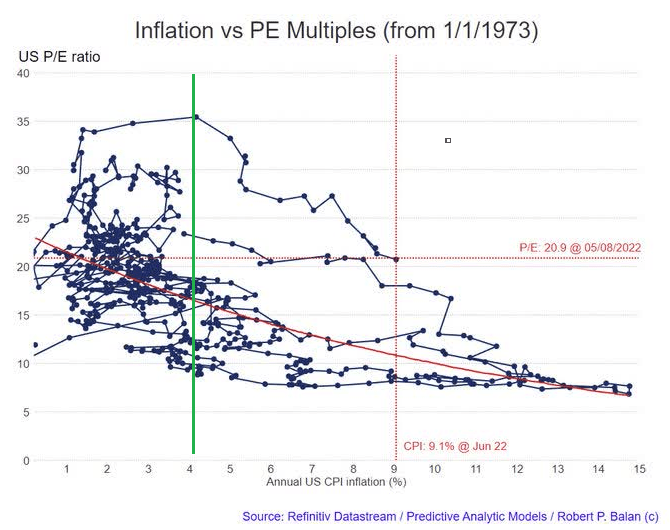

- The delayed effect of inflation shows up in current PE multiples, which tend to fall when CPI rises beyond 4.00 pct. But it may be that low P/E currently might just be indicating that the current SPX valuation is low relative to earnings.

- So, simply put, the issue is not falling GDP growth - the equity and bond markets have already discounted that months ago. The real concern is inflation, as it does impact the SPX structurally. But market-derived data have now shifted the focus to the potential for disinflation in coming months.

I was asked by a reader of the Predictive Analytic Models ((PAM)) blog the following questions:

Wouldn't higher rates infer more potential market problems if the Fed is raising into a slow down? Shouldn't GDP get worse past Q3 potentially?

(George Allen of New Yorkistan @geoallen66)

Mr. Tim Kaiser (PAM partner) observed that this set of queries are the very same questions investors are asking themselves and their financial advisors, given the very commendable equity market performance since the June 16 market low. Investors want to know if the good times can keep going. If not, they want to know what may come instead.

It was also the same set of question being asked by the PAM community, which we have addressed in several, separate instances. But we keep getting these queries. Therefore, we decided to structure the answer to these questions, including what we believe will likely happen thereafter, in the longer term. Hence, this Seeking Alpha article.

The Recession Vexation

The market ( SPX ) leads changes in GDP by at least 1 quarter. In fact, the SPX impacts GDP instead of the other way around - transmission is via looser/higher Financial Conditions ((FC)), and positive CESI, with rising SPX. The latest Nonfarm Payroll data (June 2022) should loosen FC even further.

Robert P. Balan

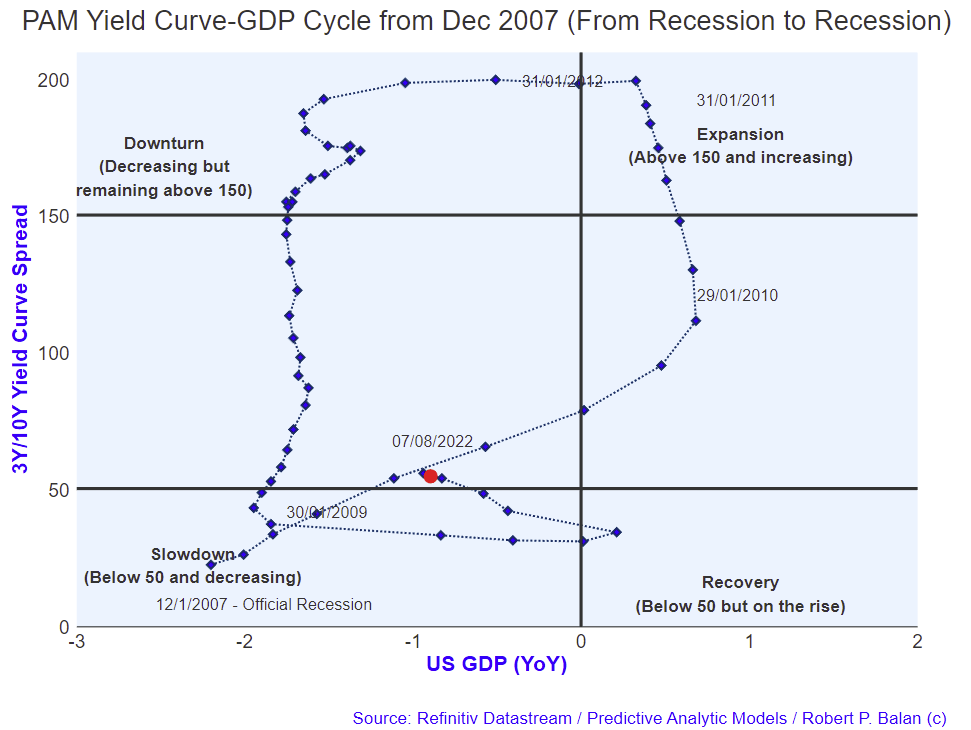

Oh, there will be a recession as defined by NBER conventions, and Q3 decline may be deeper than the initial Q2 estimate 0f -0.9 pct. Our proprietary GDP forecasting model based on the historic relationship between the changes in 3Y/10Yr Yield Curve and GDP changes is now flagging -0.96 GDP decline going into early Q3 (as from 07/08/2022, Suisse reference date). The PAM GDP forecasting tool showed -0.9 GDP reading as well in the last estimate of the BEA.

{kind=link}

Some of the estimates we have made using other tools suggest Q3 reading south of -2.00 pct. Worse than Q2, thereby cementing an official recession label, but by no means a disaster. Pundits anticipate a lot worse, so if that is all that we get, then risk assets will fare very well thereafter, indeed.

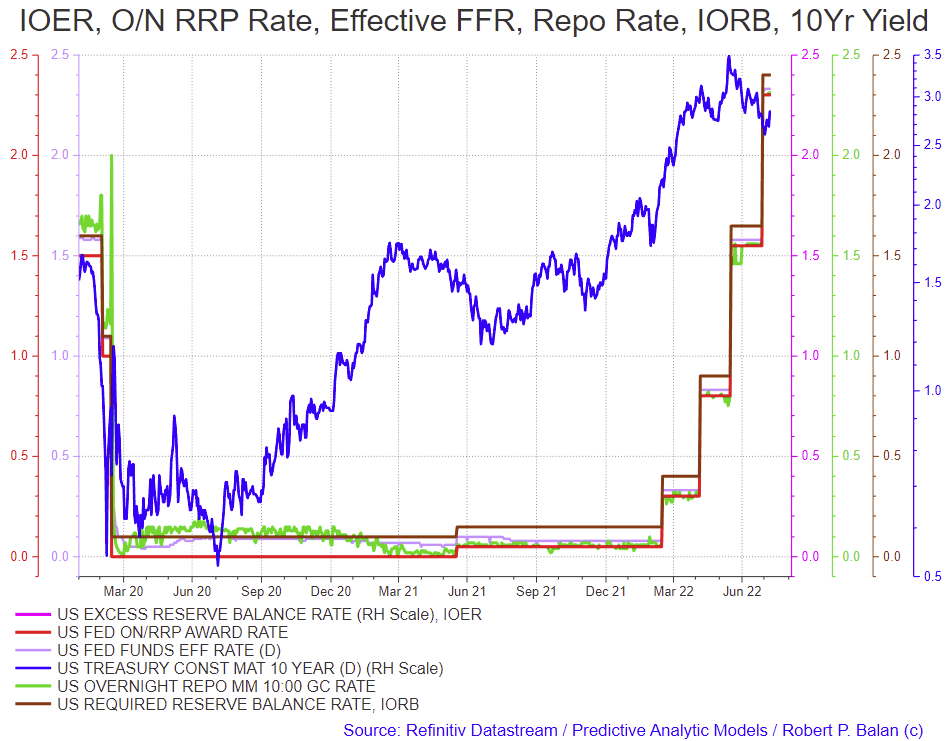

That FFR will rise is no surprise

The other thing that vexes pundits is that the Fed will likely rise in their desire to defeat inflation. But it does not matter if the Fed Fund Rate will rise further. The FFR is a severely lagged variable - indeed the Fed is severely behind the curve. It only affects market sentiment in the short term, but does not enter inflation dynamics, structure-wise, until a few months later.

Robert P. Balan

During the last FOMC Q&A session, there was a portion of Fed Chair Jerome Powell responses to questions which sounded like the Fed chair was hinting of a possible Fed pivot from its Quantitative Tightening regime. But the market was wrong.

The Fed is ignoring the impact of recession - that is very clear. All the Fed talking heads came out in the past few days underlining the resolve of the Fed in defeating inflation. They cannot do that if financial conditions ease (e.g., falling long term yields, rising equities). That is why this chorus of Fed speakers is trying to reverse the market's impression of a Fed pivot.

That said, there is also a generally positive correlation between the FFR and SPX.

The decline in SPX has been mainly due to low total, national corporate profitability (NIPA) , not due to rising inflation.

Robert P. Balan

Although retail investors mention the FFR when speaking about interest rates, that mental image usually conflates with the long-term bond rate, the 10Yr Yield. Therefore, the focus on *rates* usually and eventually redound to queries as to what the 10YR yield will do during a regime of rising Fed Funds Rate.

Before the Fed initiated Quantitative Easing on November 2008, the covariance between FFR and the 10YR Yield was arguably negative, especially when monetary policy rates are rising. The prism in this relationship was the effect of rising FFR on GDP growth (negative), and again arguably, falling GDP growth will likely be accompanied by a falling 10Yr yield. After QE started however, that negative covariance has flipped: rising FFR now tends to push the 10YR yield higher, with the ultra-short term rates (proxy: Repo rate ((GC)) as transmission mechanism.

{kind=link}

The day to day relationship between the 10Yr Yield and equity indexes is generally positive -- to the point that we take a positive covariance as a sign of risk-on mode for the day. The longer-term correlation between the 10Yr Yield and SPX is also broadly positive. The best positive covariance is provided by a one week advance of the 10Yr Yield. This is a historic, general relationship which has barely changed over the past decades.

Robert P. Balan

Rising inflation's punch is real but may be short-lived

Nonetheless, the delayed effect of inflation shows up in current PE multiples, which tend to fall when CPI rises beyond 4.00 pct, despite inflation being a lagging variable. But it maybe that current low P/E may just be indicating that the current SPX valuation is low relative to earnings. For this, we may have to wait for another week or so, until the current earnings picture is complete.

{kind=link}

So, simply put, the issue is not falling GDP growth - the equity and bond markets have already discounted that months ago. The real concern is inflation, as it does impact the SPX structurally (chart above). But market-derived data have now shifted the focus to potential for disinflation up ahead.

Robert P. Balan

More importantly, Final Demand PPI has already turned lower, and should significantly fall, nay, even collapse, over the next few months, as the growth of all the prime contributors to PPI Final Demand have been falling heavily.

Robert P. Balan

We will go back to worrying about Fed and Treasury liquidity issues

In a few days, we will have the July CPI data which has a high degree of certainty to be significantly lower than that of June. That of course removes the biggest bugaboo for equity markets, at least in the medium-term. Thereafter, market metrics will shift again to Fed and Treasury systemic liquidity issues, as well as global government expenditures. The short-term still looks problematical as aggregate Fed credit is still rolling over. But that should not last.

Robert P. Balan

However, the bigger picture is constructive. Global equities and other risk assets are impacted by global government expenditures, but the distributed lags are long (2.5 years). Those leading expenditure variables are promising a better environment for equities during the rest of the year, and into 1H 2023.

Robert P. Balan

For one, it may be a short-lived lift. H2 2023 risk asset prices may be impacted by the lagged impact of falling government expenditures 2.5 years prior, and by the very weak economic conditions which were direct cause of the yield curve inversion that we are seeing now. We should see the negative impact of the current Yield inversion to US GDP growth 5 to 6 quarters hence, i.e. during late part of 2023.

Robert P. Balan

Unfortunately, the weakness in late 2023 being flagged by the 3Y/10Yr Yield curve now will coincide with the seasonality of global government expenditures' outflows at that time, so risk assets will likely be dealt a double-whammy in late 2023 and part of 2024. That is THE RECESSION which we should fear, not the garden variety of growth decline that we will likely see during Q2-Q3 2022.

For further details see:

Recession Is Not The Issue For Markets - Inflation Is, But Disinflation Is Around The Corner - Markets Will Be Just Fine