QQQ - Recession? Maybe In Production But Outweighed By Still-Strong Employment

2023-05-17 15:10:39 ET

Summary

- The latest data on manufacturing and wholesale sales, and industrial production, indicate a substantial likelihood that these have peaked.

- But real personal income and employment have continued to grow.

- Fed rate hikes have finally caused total housing construction and employment to turn down, but not nearly enough to be significant yet.

- But lower gas prices, and pent-up hiring demand from spending on services are keeping a larger share of the economy growing still.

Introduction

Several months ago, I wrote in some detail about why, almost 6 months after both the long and short leading indicators had turned negative, no recession had appeared.

In that article, I noted 3 reasons: (1) the decline in gas prices; (2) employment has not caught up with sharply increased post-pandemic demand; and (3) the logjam in housing construction also thwarted the Fed's usual transmission mechanism. There have been a few changes, and I can elaborate further, so here's an update.

The producer side of the economy may already be in a mild recession

There is a very good chance that two of the four monthly series most watched by the National Bureau of Economic Research ("NBER") for coincident indicators of recession, industrial production and real total business sales, have already peaked.

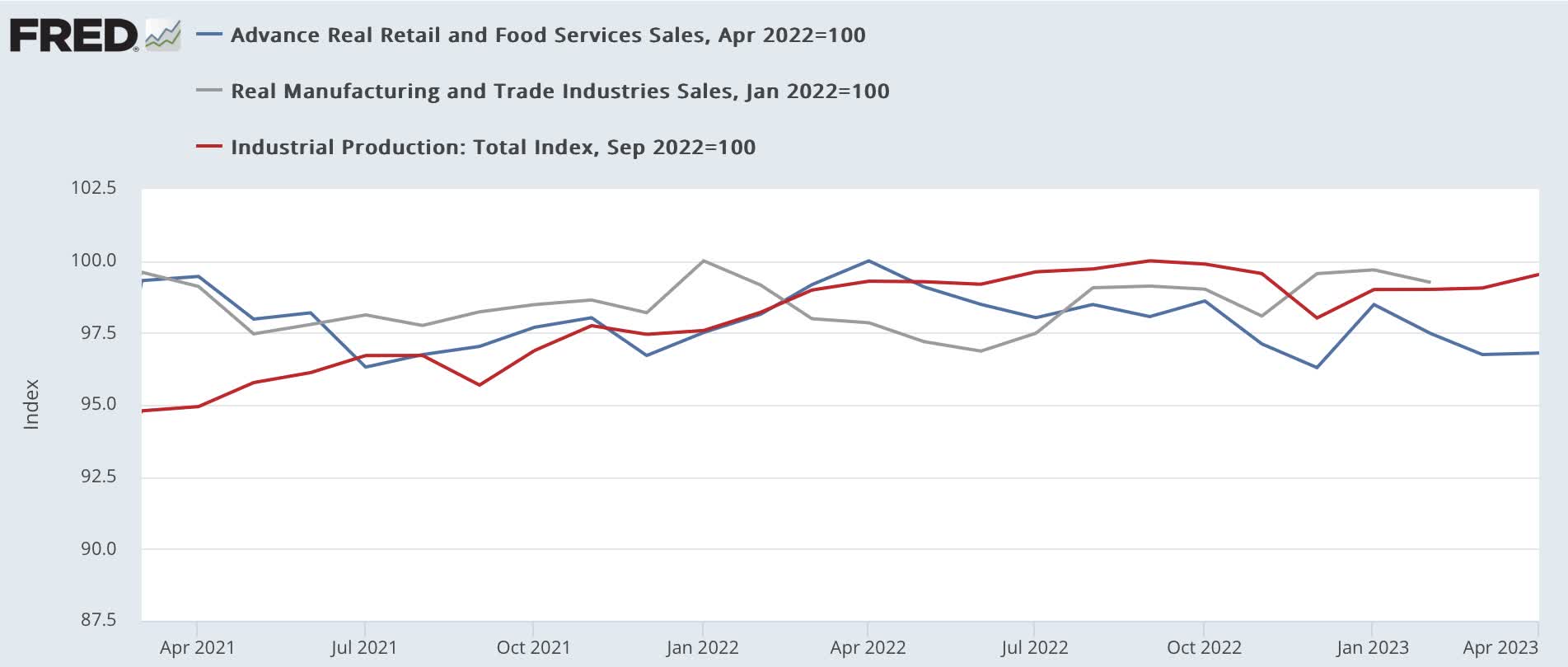

Below is a graph of industrial production (red), real total business sales through February (its last report, gray) and real retail sales, which constitutes about 1/3rd of real total business sales (blue, through April). All three are normed to 100 as of their most recent peaks:

Industrial production, real final sales, real retail sales (FRED)

{kind=link}

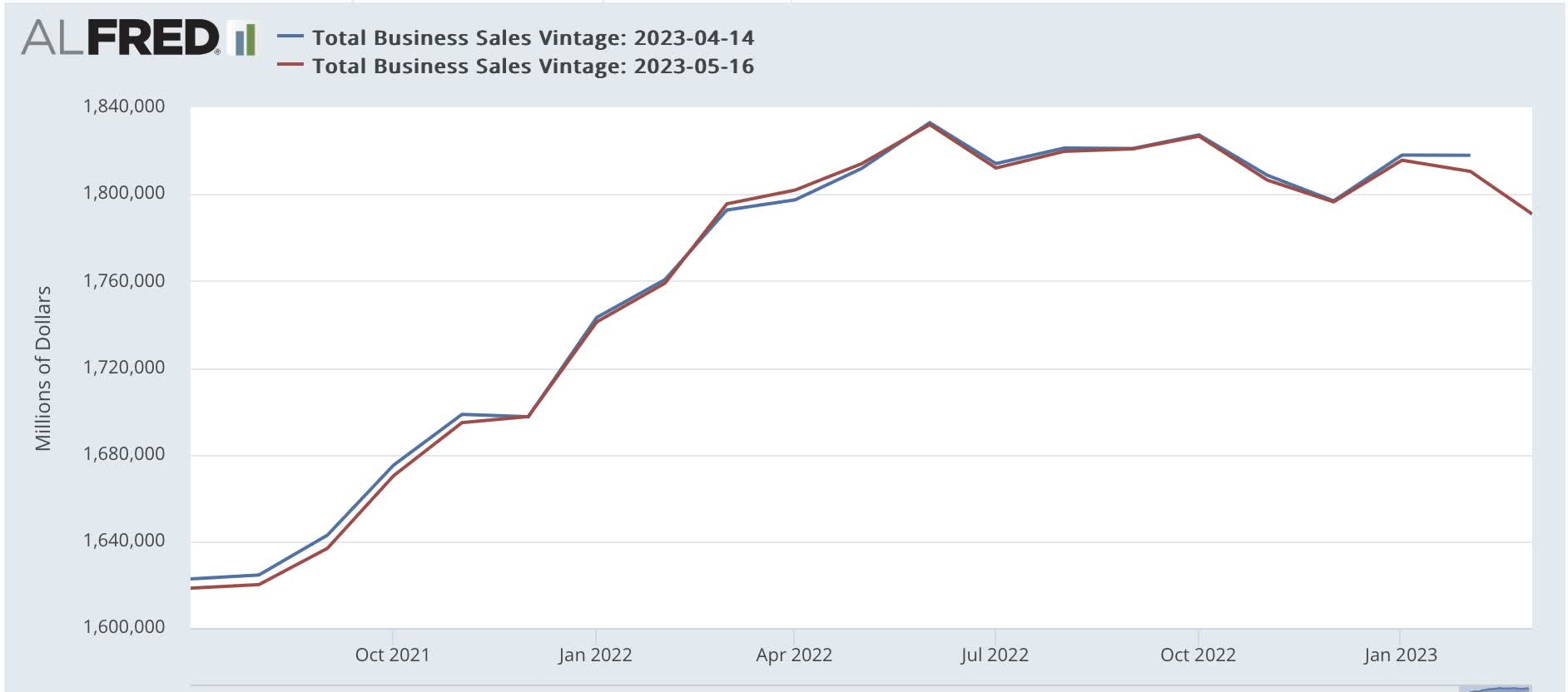

Industrial production has not made a new high in 7 months. Real retail sales are close to a 2-year low. Further, nominally total business sales declined -1.1% in March, and January and February data were both revised slightly down:

Total sales with revisions (FRED)

{kind=link}

Deflating by an average of producer prices at various states, plus consumer prices, has typically given a result close to the actually reported number, as shown below:

Real final sales vs. estimate (FRED)

{kind=link}

It is likely that real manufacturing and trade sales declined another -0.8%-0.9% in March.

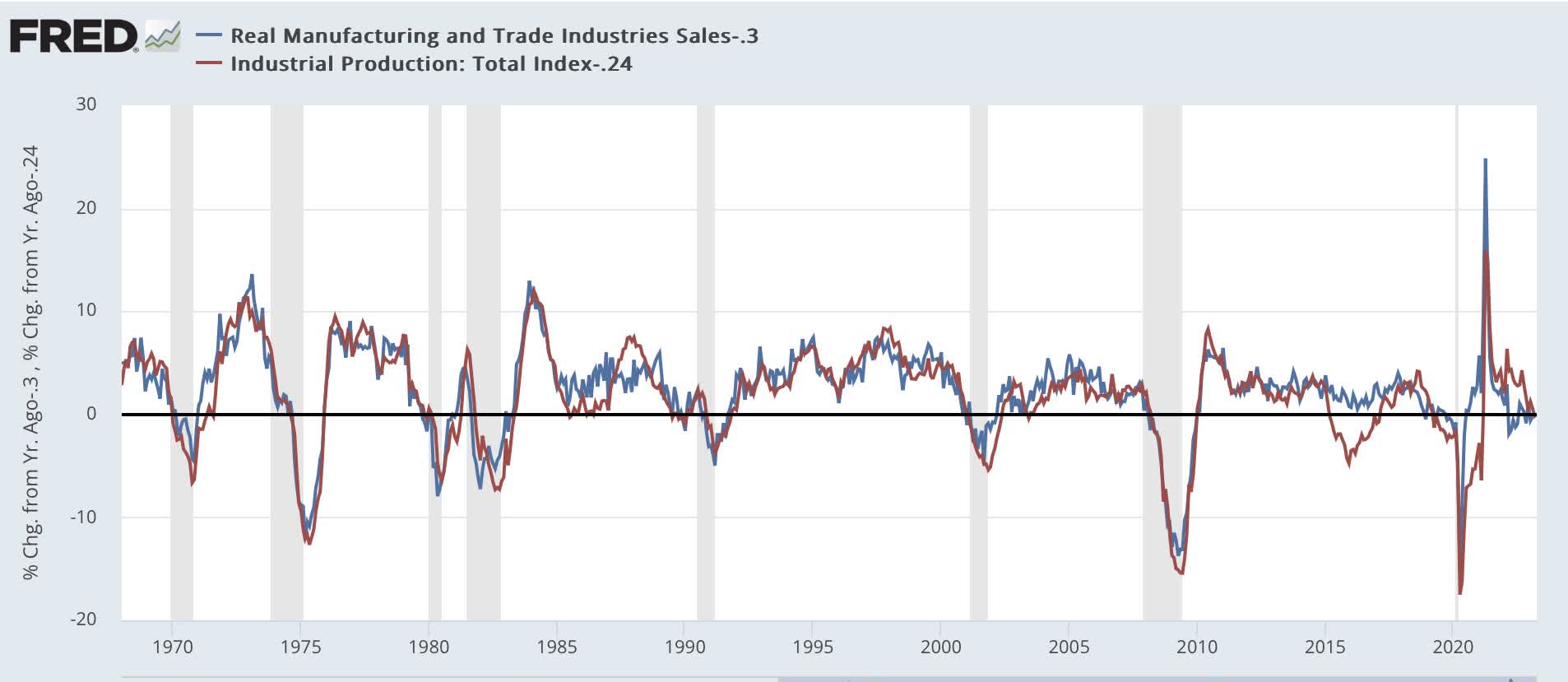

In the past, when these measures have been at their latest YoY readings, it has almost always been coincident with recessions:

YoY industrial production & real final sales (FRED)

{kind=link}

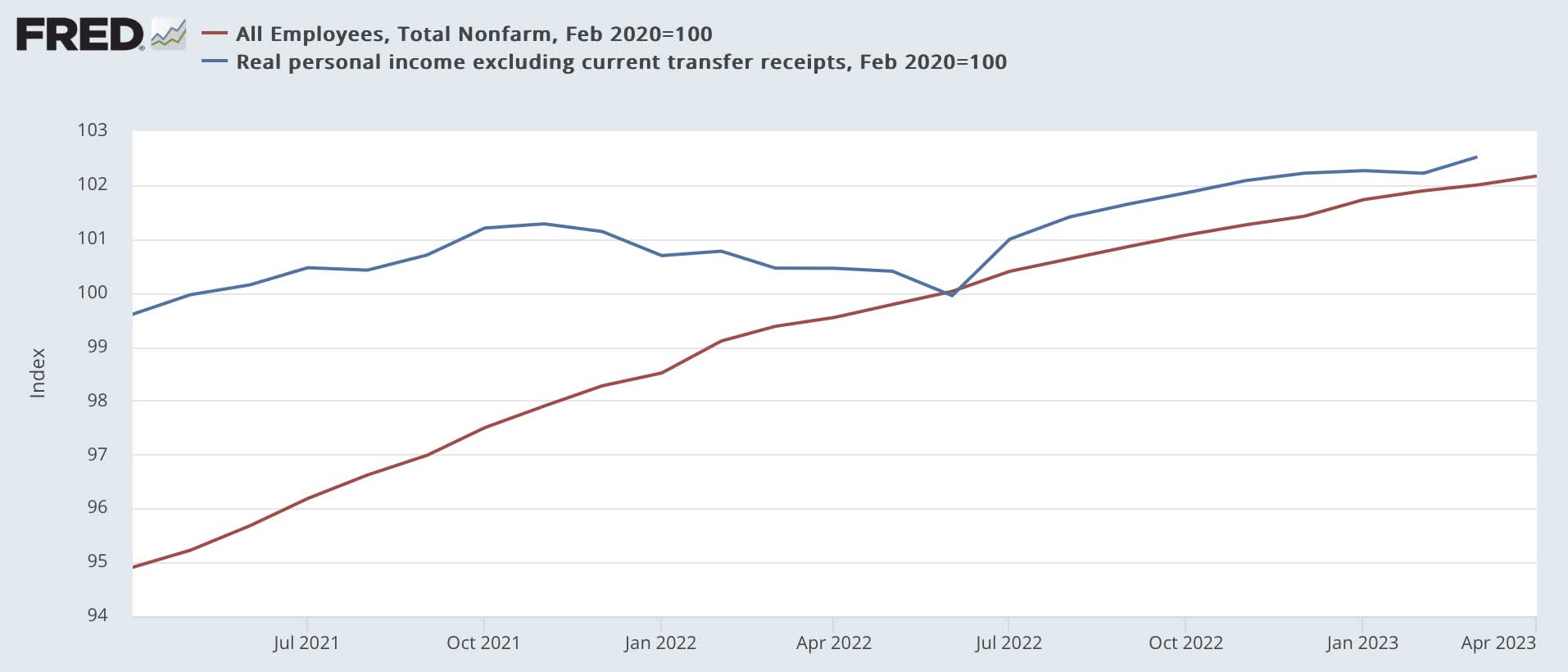

This tells us that it is the consumer side of the economy, typified by real personal income and nonfarm payrolls (the other two monthly series most watched by the NBER), that is still growing:

Real personal income and nonfarm payrolls (FRED)

{kind=link}

Why is this time different - so far?

1. The decline in producer prices, as well as in gas, continues to be a tailwind for the economy.

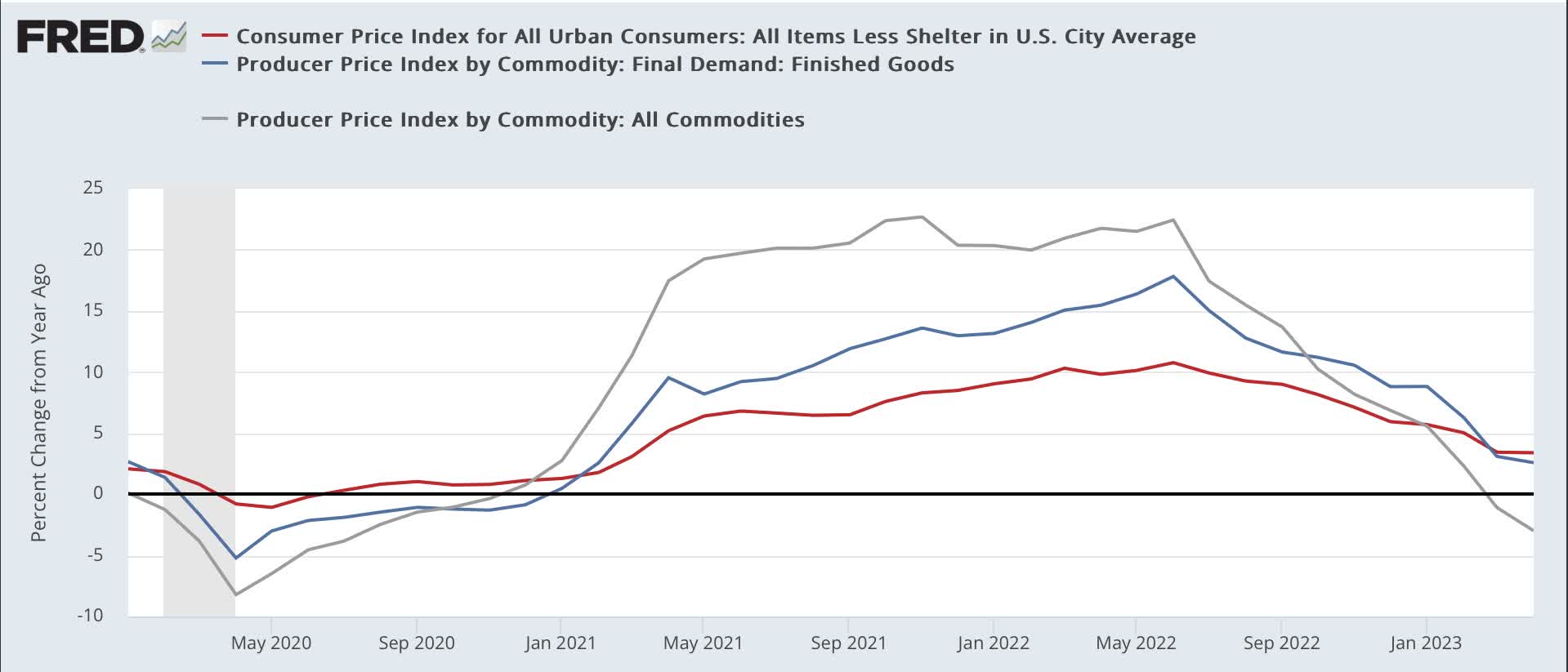

Let's get right to the point: here is a graph of the YoY% change in producer prices for commodities, for final demand, and for consumer prices ex-shelter:

YoY producer and consumer prices (FRED)

{kind=link}

Consumer prices ex-shelter only increased 0.5% in the 1st Quarter (and are only up 0.8% (!!!) in the 10 months since last June). Gas prices remain down about 30% from their peak last June. Producer prices both for commodities and finished inputs are also down since then, the former by over 8%, the latter by 1.7%. In fact, producer prices for commodities have actually declined YoY:

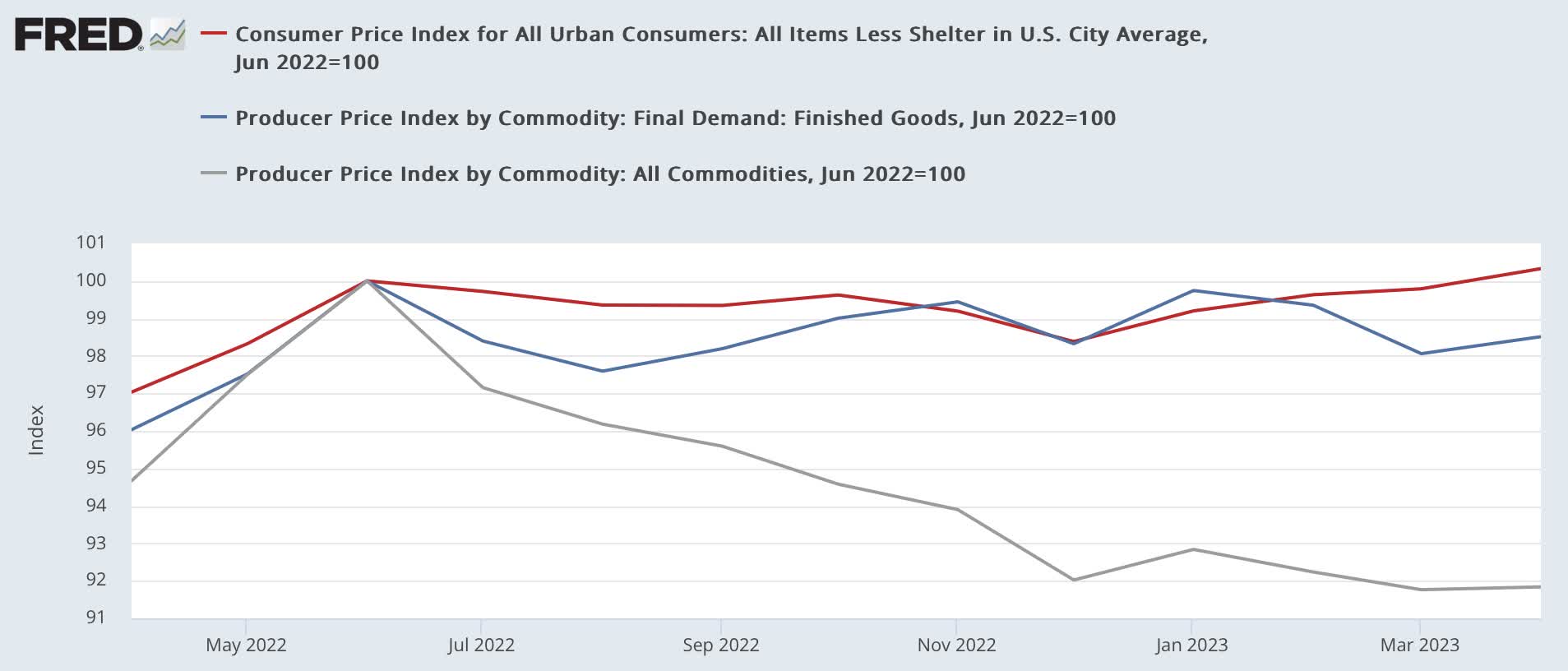

Producer and consumer prices ex-shelter since June 2022 (FRED)

{kind=link}

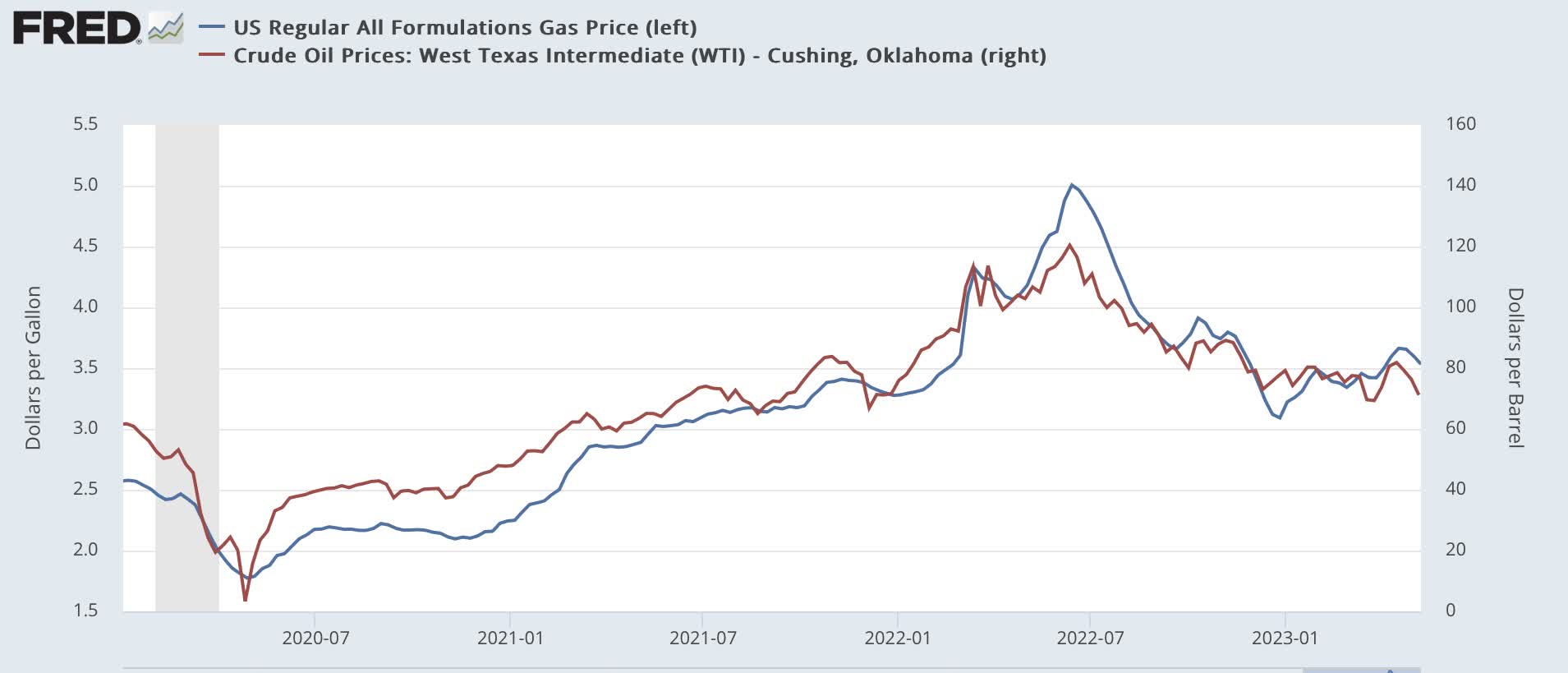

Producers are simply not feeling any upward pressure on any inputs aside from labor. The incipient downturn in production and sales has been driven by changes in consumer demand. And meanwhile consumers, compared with last spring, continue to enjoy the windfall of lower gas prices:

{kind=link}

It's hard to get a recession going with that kind of support.

2. Consumption leads employment - and employment hasn't caught up yet

Going back 75 years, when real retail sales (which are concentrated on goods rather than services) have turned negative YoY, a recession has almost always occurred simultaneously or within a few months thereafter. Here's what that looks like:

Long term view real retail sales YoY (FRED)

{kind=link}

A close-up on the past 18+ months indicates we ought to be in a recession by now:

{kind=link}

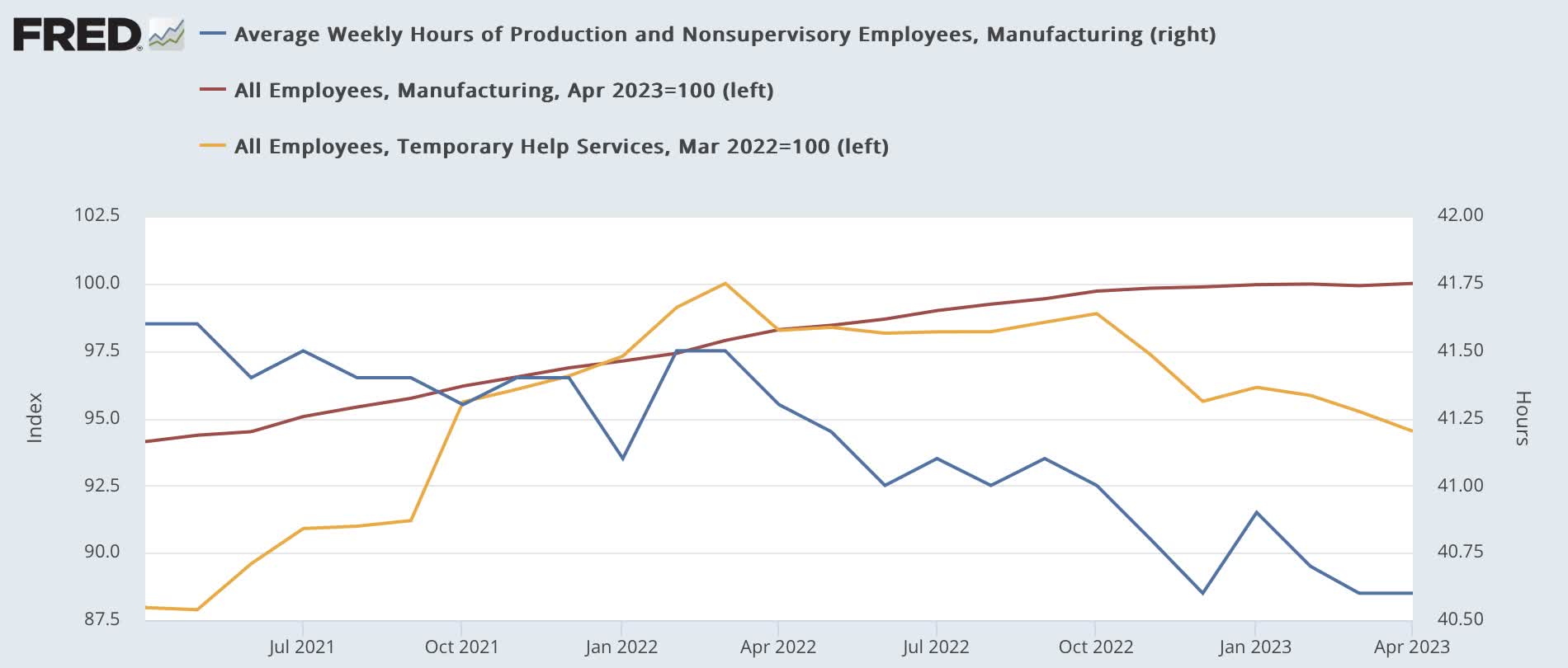

Indeed, several leading indicators in employment - the average manufacturing workweek and temporary employment - are down significantly from their peaks. But at this point, manufacturing employment isn't down at all:

Leading sectors of employment (FRED)

{kind=link}

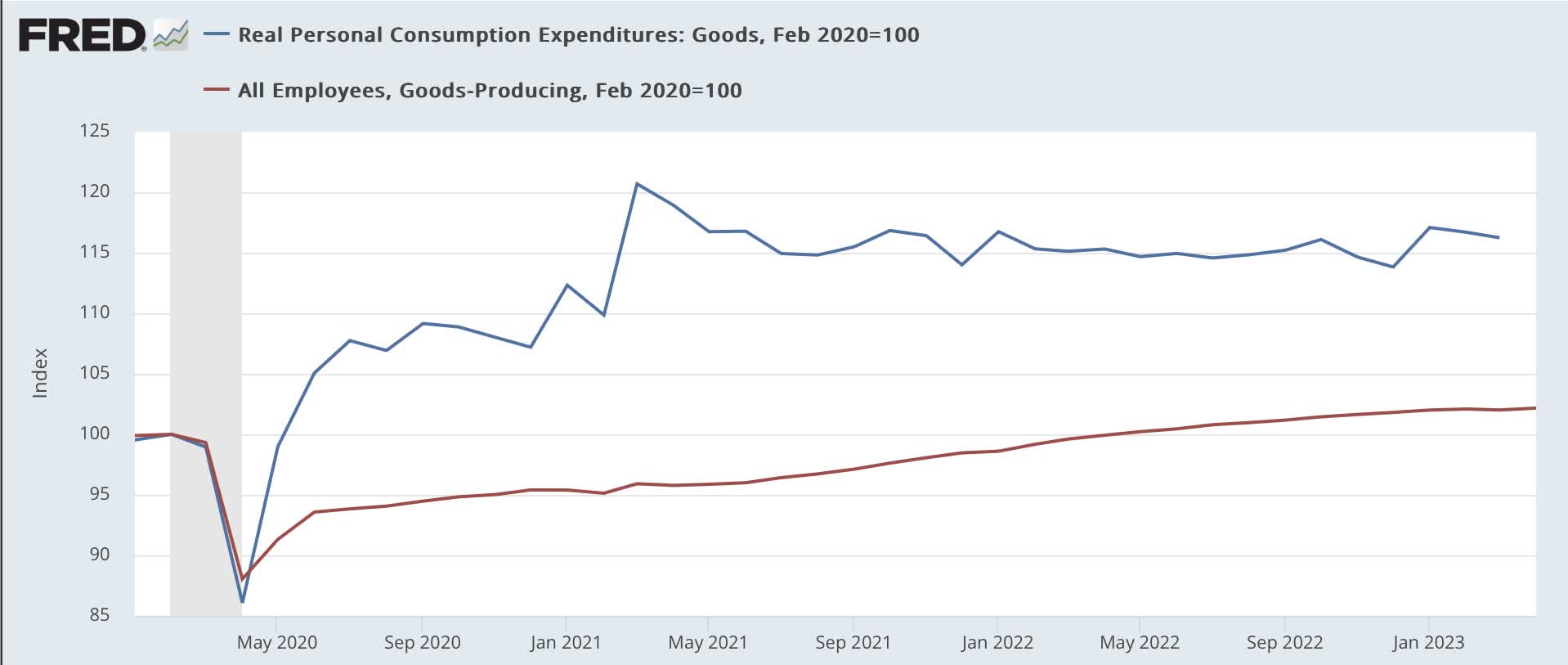

The downturn in spending noted above still puts real consumer spending on goods as of April higher by more than 15% compared with just before the recession. But employment in goods-producing industries is only up 2%:

Real personal spending on goods vs. goods employment (FRED)

{kind=link}

Typically, employment in goods-producing industries has proceeded at about 1/2 the rate of growth in goods consumed, so the 15% gain in demand for goods "ought" to mean roughly a 7%-8% gain in employment in those industries. Not 2%!

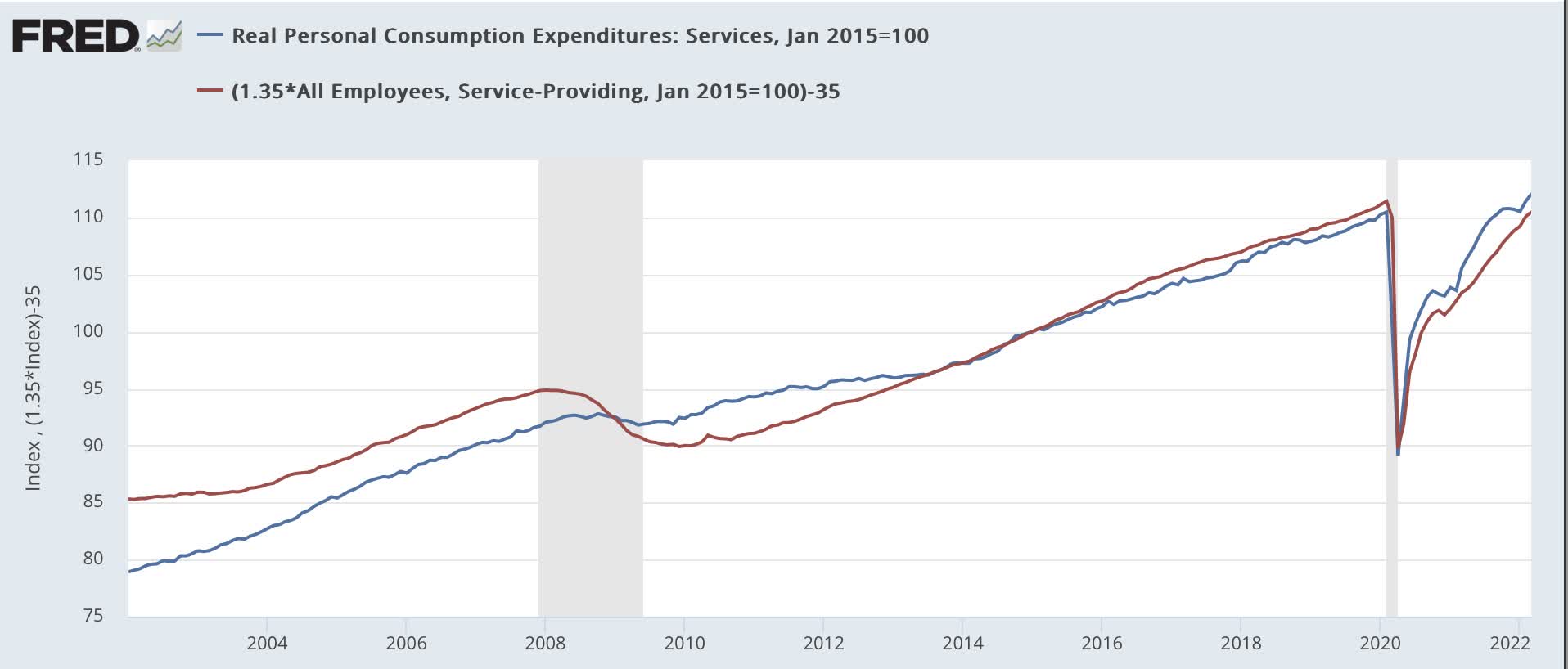

In contrast, employment in services industries has increased at about a 1:1.4 rate compared with services consumption:

Real personal spending on services vs. service employment (FRED)

{kind=link}

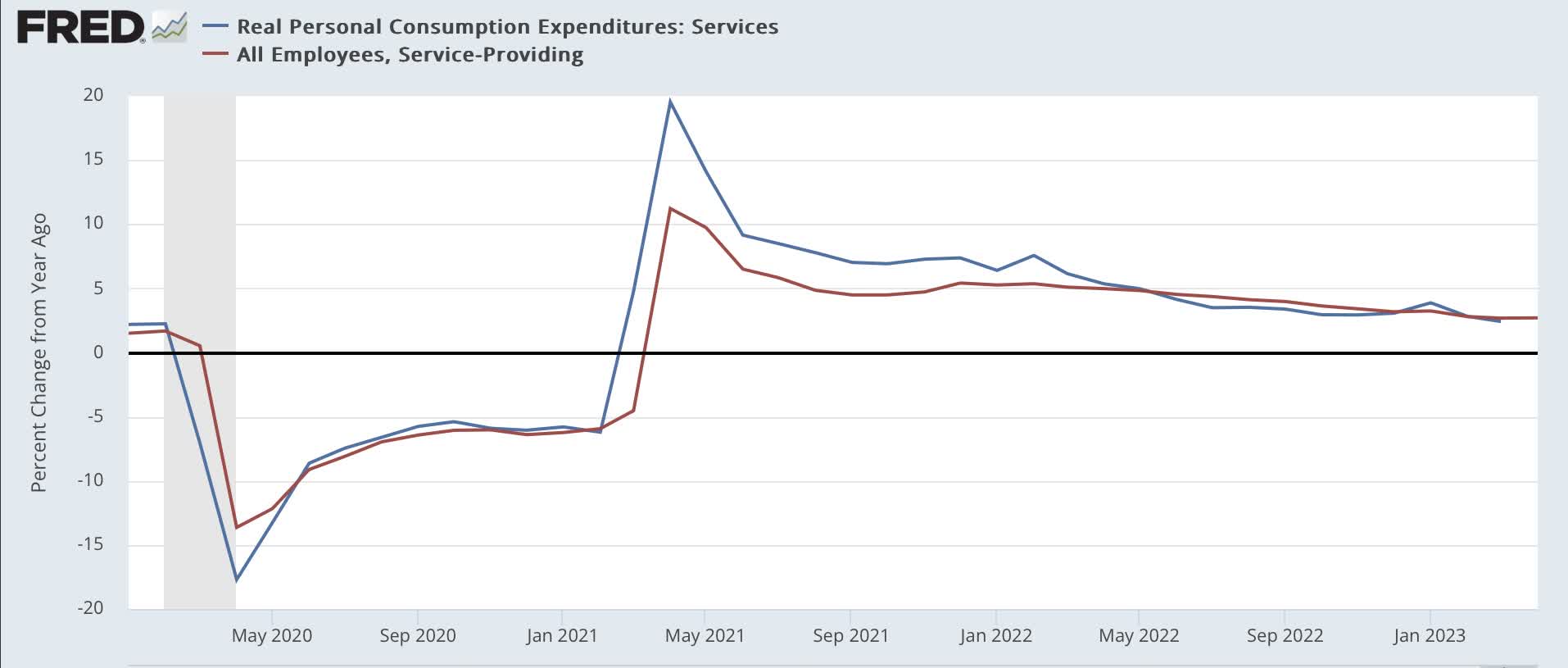

And, while consumption of goods, as reflected in both real retail sales and real personal consumption for goods, has turned negative or close thereto on a YoY basis, the still-hot pace of growth in consumption of services - most recently up about 2.5% YoY - has meant that employment in those industries has continued to grow strongly - also close to 2.5% YoY:

YoY growth in real spending on services vs. services employment (FRED)

{kind=link}

So we have a continuing strong need for more employment in goods-producing industries to catch up with demand, even as demand is lower than one year ago, and continuing strong demand for services has allowed strong growth in services employment to continue.

3. On the other hand, the Fed's transmission pipeline through housing has finally engaged - but not enough yet to signal recession

When I last wrote, the total number of housing units under construction was at an all-time record. That's because of supply issues secondary to the pandemic.

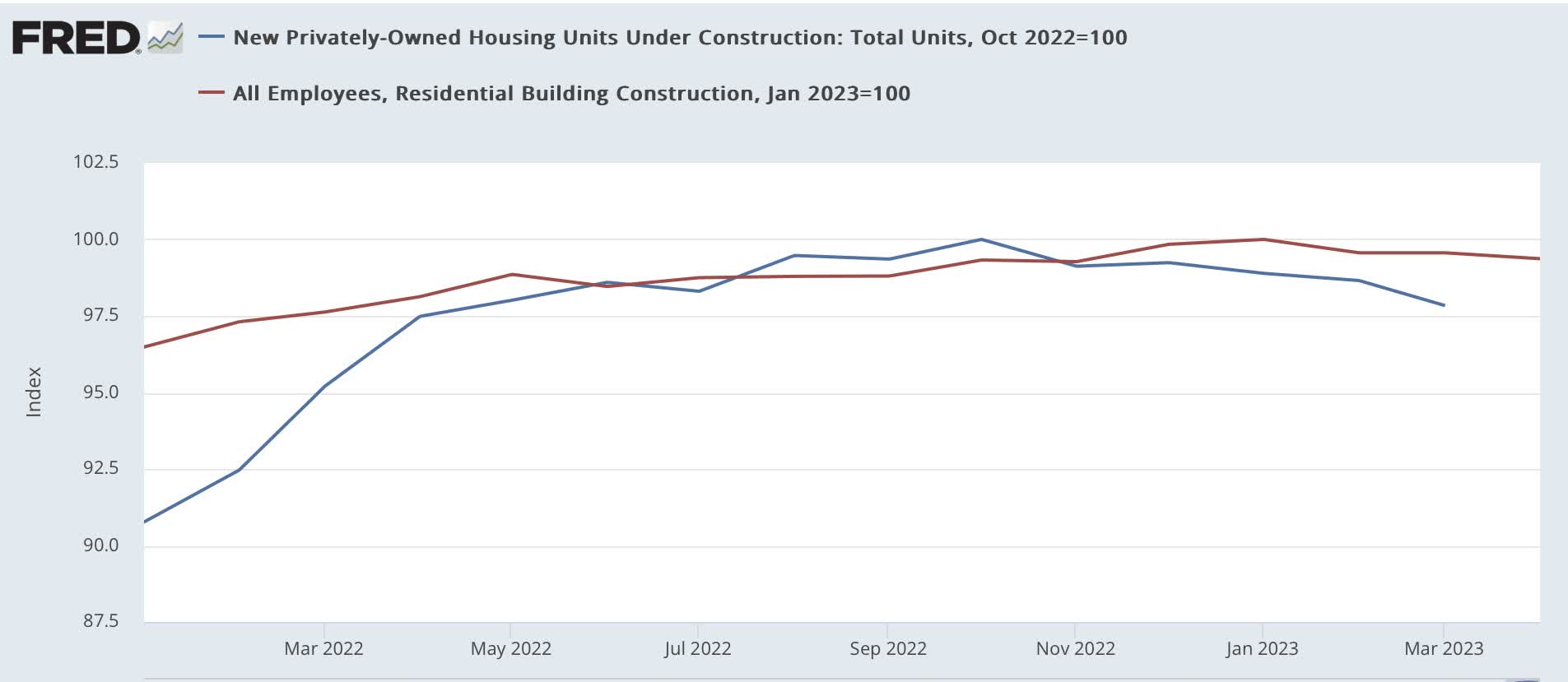

Between the resolution of those issues, the steep downturn in housing permits and starts, and revisions to past data, housing construction did peak, as did residential construction employment (note: below graph does not include April's slight increase in housing units under construction from Wednesday's report):

Residential units under construction; residential construction jobs (FRED)

{kind=link}

Still, in the past, recessions have usually started once the downturn in construction and construction employment were down close to or over 10%. Currently, we're down a little over 2% on the former, and less than 1% on the latter

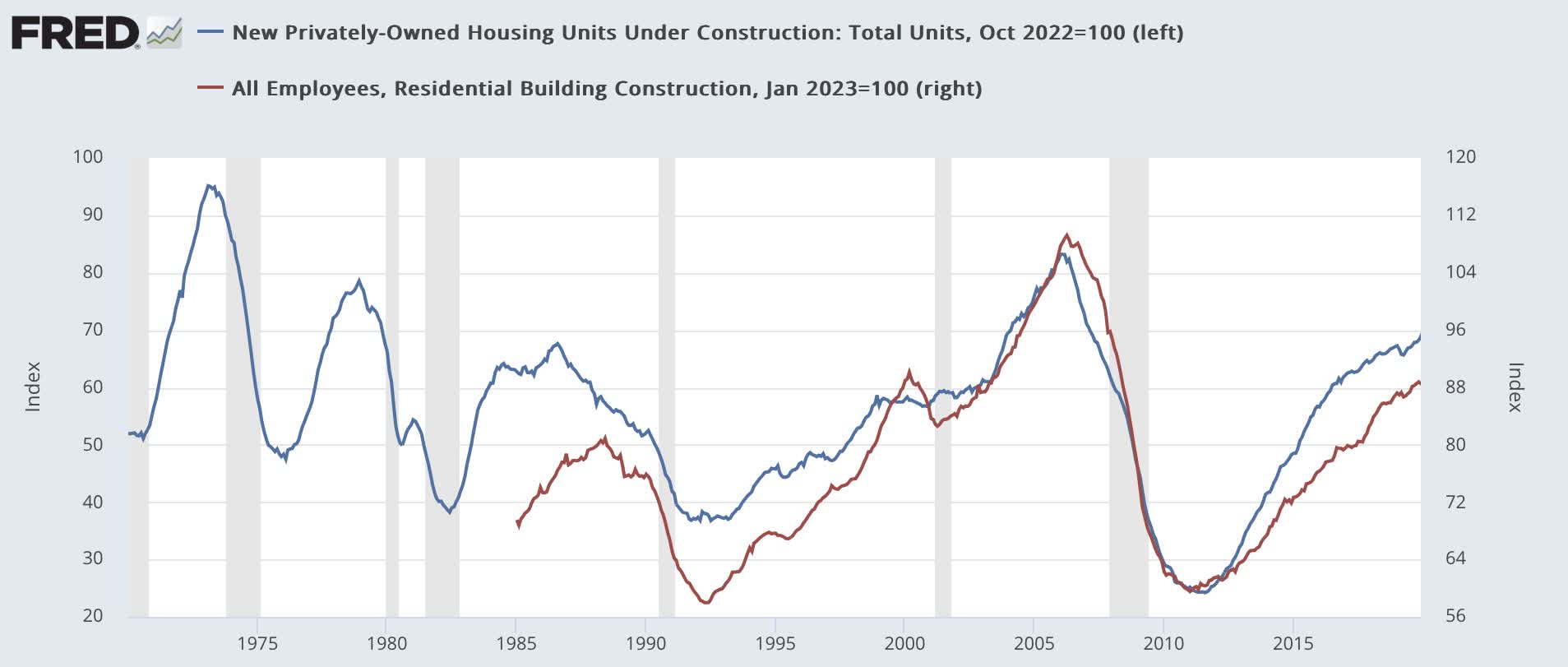

Long term view residential construction vs. construction jobs (FRED)

{kind=link}

Conclusion

A downturn in goods-producing industries - especially manufacturing and housing construction - has typically been a leading indicator for recession. And both have indeed now turned down.

But as services as a share of the economy has grown, it has taken a deeper downturn in the leading industries to translate into recession. The downturn in manufacturing and production so far is not yet at a pace sufficient to overcome the atypically strong increase in services spending. This is, in part, fueled by, well, the extra $$$ in consumers' pockets due to the downturn in fuel prices; and the Fed's transmission mechanism through housing has not yet had enough "bite" to make a significant difference.

For further details see:

Recession? Maybe In Production, But Outweighed By Still-Strong Employment