CMI - Recession? Tailwinds? How Attractive Is Cummins' 3% Yield?

2023-06-08 11:53:13 ET

Summary

- Cummins Inc. is a trusted dividend growth stock in the cyclical engine production industry, with 17 years of consecutive dividend growth and a payout ratio of less than 34%.

- The company has outperformed both the market and its industrial sector peers, with shares returning 16.4% per year since 1999 and a five-year average annual dividend growth rate of 7.8%.

- Despite a more mature engine market and economic challenges, Cummins is benefiting from unexpected tailwinds that could enhance growth when cyclical demand returns.

Introduction

Let's talk about one of the most fascinating industrial stocks on the market. Columbus, Indiana-based Cummins Inc. ( CMI ) isn't just one of the world's most advanced engine producers, but it is also a trusted dividend growth stock in a highly cyclical industry. The company has been through countless cycles and rewarded its investors with consistent dividend hikes, buybacks, and the safety of a healthy balance sheet during downturns.

This is my first Cummins article in 2023, which means we'll assess the attractiveness of its 3% dividend yield in light of economic challenges and unexpected tailwinds.

So, let's get to it!

A Closer Look At The Cummins Dividend & Relative Performance

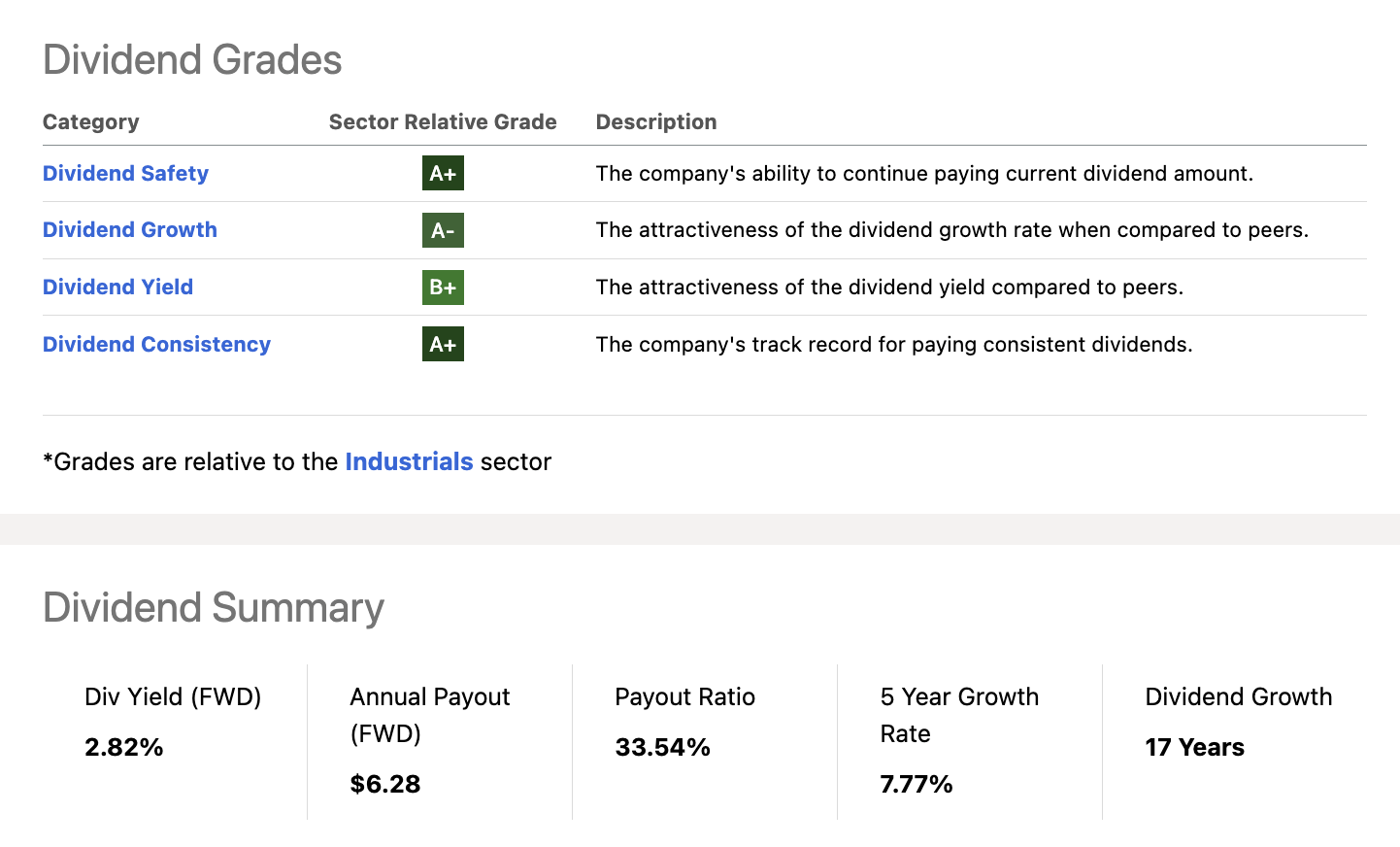

Cummins has one of the best-looking dividend scorecards in its sector. The company scores high on safety, consistency, and growth. It also has a decent yield of 2.8%.

{kind=link}

Despite going through multiple cycles, the company has 17 years of consecutive dividend growth, a payout ratio of less than 34%, and a five-year average annual dividend growth rate of 7.8%, which includes two nasty pandemic years.

The most recent hike was announced on July 12, 2022, when the board approved an 8.3% payout hike.

Furthermore, the company is a consistent buyer of its own shares as a way to (indirectly) distribute its free cash flow.

Over the past ten years, CMI has bought back roughly a fourth of its shares.

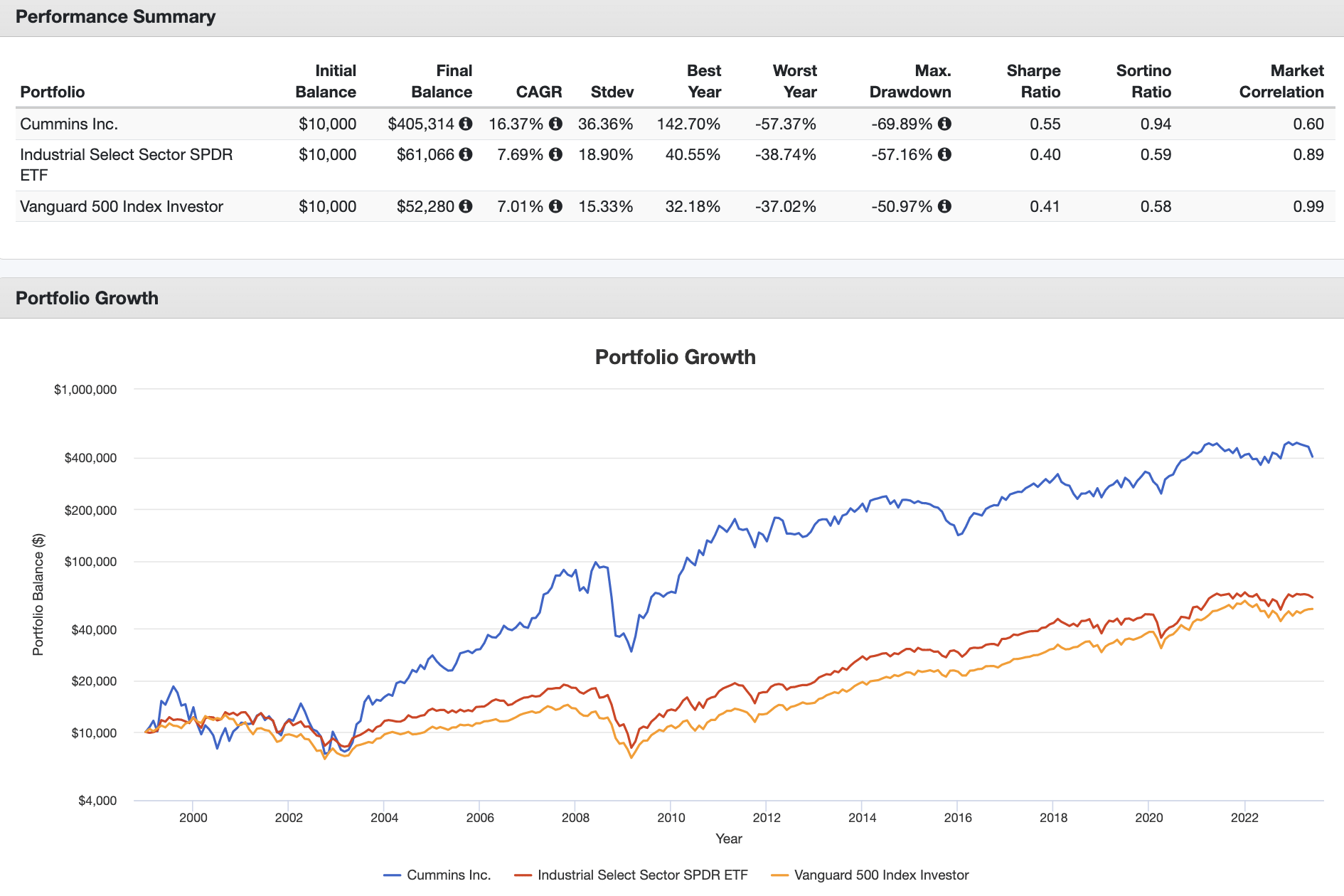

These qualities have also allowed the company to outperform both the market and its industrial sector peers.

Since 1999, CMI shares have returned 16.4% per year, beating the S&P 500 by almost 940 basis points per year. This turned a $10,000 investment into more than $400,000. Even adjusted for its elevated standard deviation (after all, CMI Is highly cyclical), the company beat its peers and the market on a risk/adjusted basis (Sharpe Ratio).

{kind=link}

That said, I need to add that the engine market has become much more mature. Growth in the United States has come down a lot, and the S&P 500 has become way more competitive due to the index being overweight in tech stocks (that can be a disadvantage if we get a rotation back to value).

Hence, over the past ten years, CMI has returned 8.4% per year, which is below the performance of its industrial sector peers and the S&P 500.

The performance over the past five years beat its industrial sector peers.

{kind=link}

While I do not believe that CMI will outperform its peers by a wide margin, I do believe that CMI has the ability to outperform its peers by a slim margin on a prolonged basis.

Why?

Because its engine business is benefiting from unexpected tailwinds that could enhance growth the moment cyclical demand comes back.

Recession? Cummins Is Doing Surprisingly Well

Cummins has perfectly followed economic cycles in the past

By now, I assume that almost everyone knows that we're dealing with high recession chances.

Especially in manufacturing, we see that the leading ISM Manufacturing report shows a steep decline in new orders. As a matter of fact, new orders are expected to be worse than during the 2015/2016 manufacturing recession. Since the year 2000, only the Great Financial Crisis and the pandemic saw lower readings.

Bloomberg

Hence, it should be no surprise that Cummins has been struggling - at least on the stock market.

With a market cap of $32 billion, this giant generates roughly 90% of its revenue in its Distribution, Engine, and (related) Components segments.

CMI is currently down 6.4% year-to-date. The stock is 13% below its 52-week high and down 18% from its all-time high.

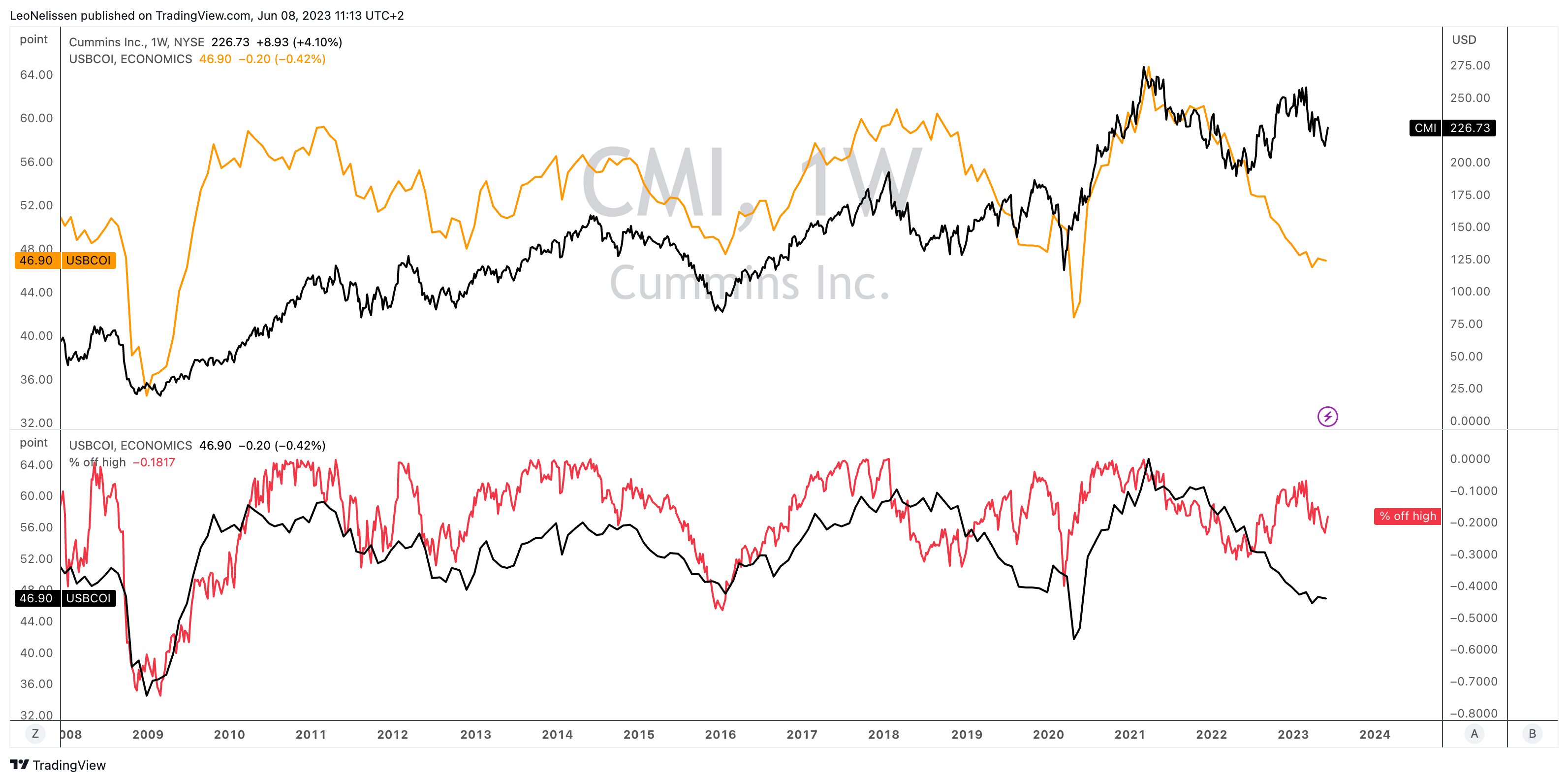

The chart below compares Cummins stock price to the ISM Manufacturing Index.

- The upper part of the chart below compares CMI to the ISM index outright.

- The lower part compares the distance CMI shares are trading below their all-time high (in %) to the index.

{kind=link}

As we can see, CMI shares are highly cyclical. They get dragged down every time economic sentiment declines. That makes sense, as it causes investors to de-risk their portfolios and shift money into other areas. As soon as economic growth bottoms, money flows back into cyclical stocks.

With that said, as the charts above show, CMI isn't listening to leading indicators anymore. The stock is doing quite well again.

- CMI shares are up 10.9% on a rolling weekly basis.

- Shares are 23% above their 52-week lows.

So, what is going on?

The decline in economic growth expectations started in 2021.

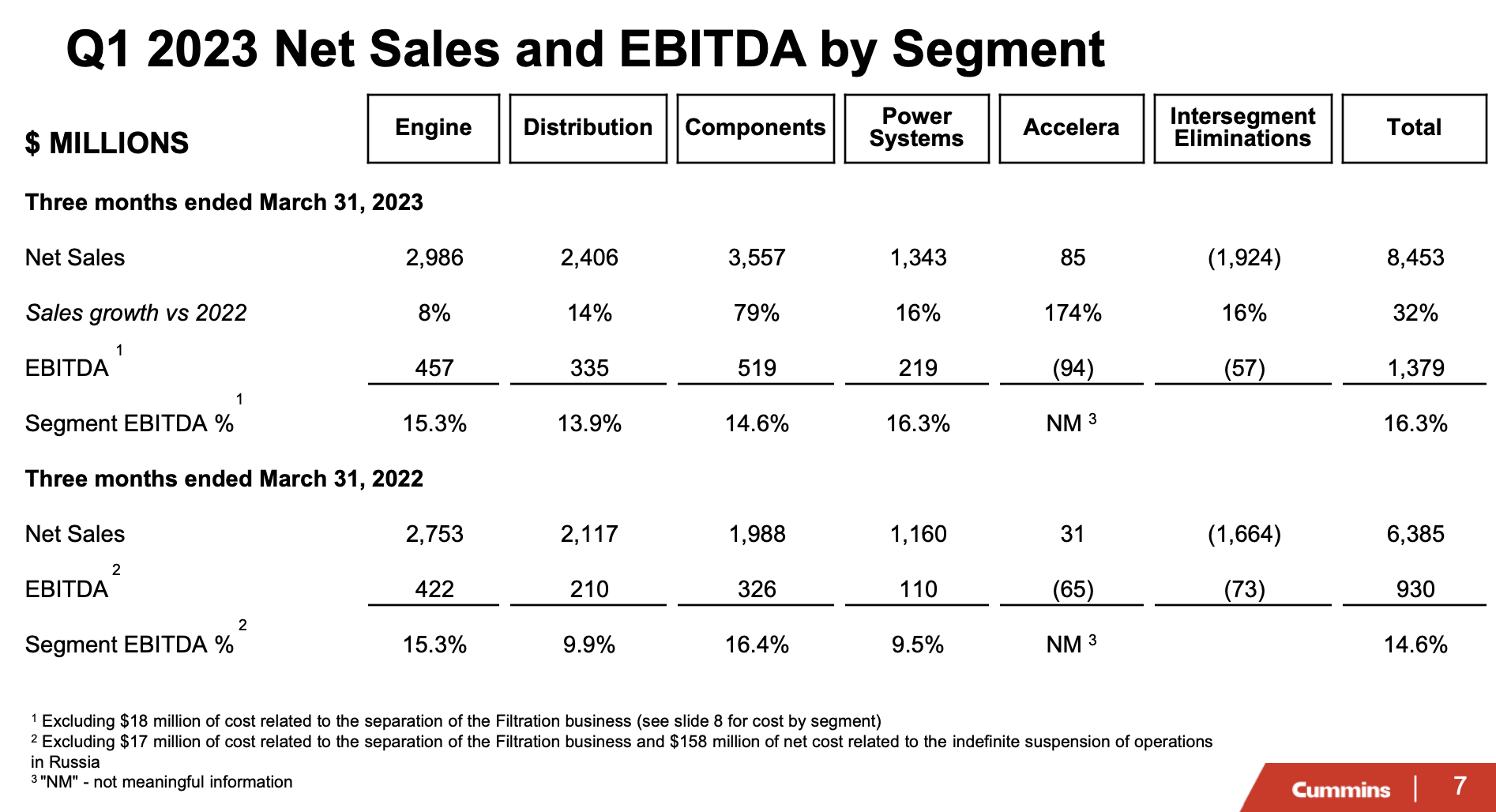

However, this decline has not yet translated into slower earnings. Looking at the numbers below, we see that Cummins did exceptionally well in its most recent quarter.

{kind=link}

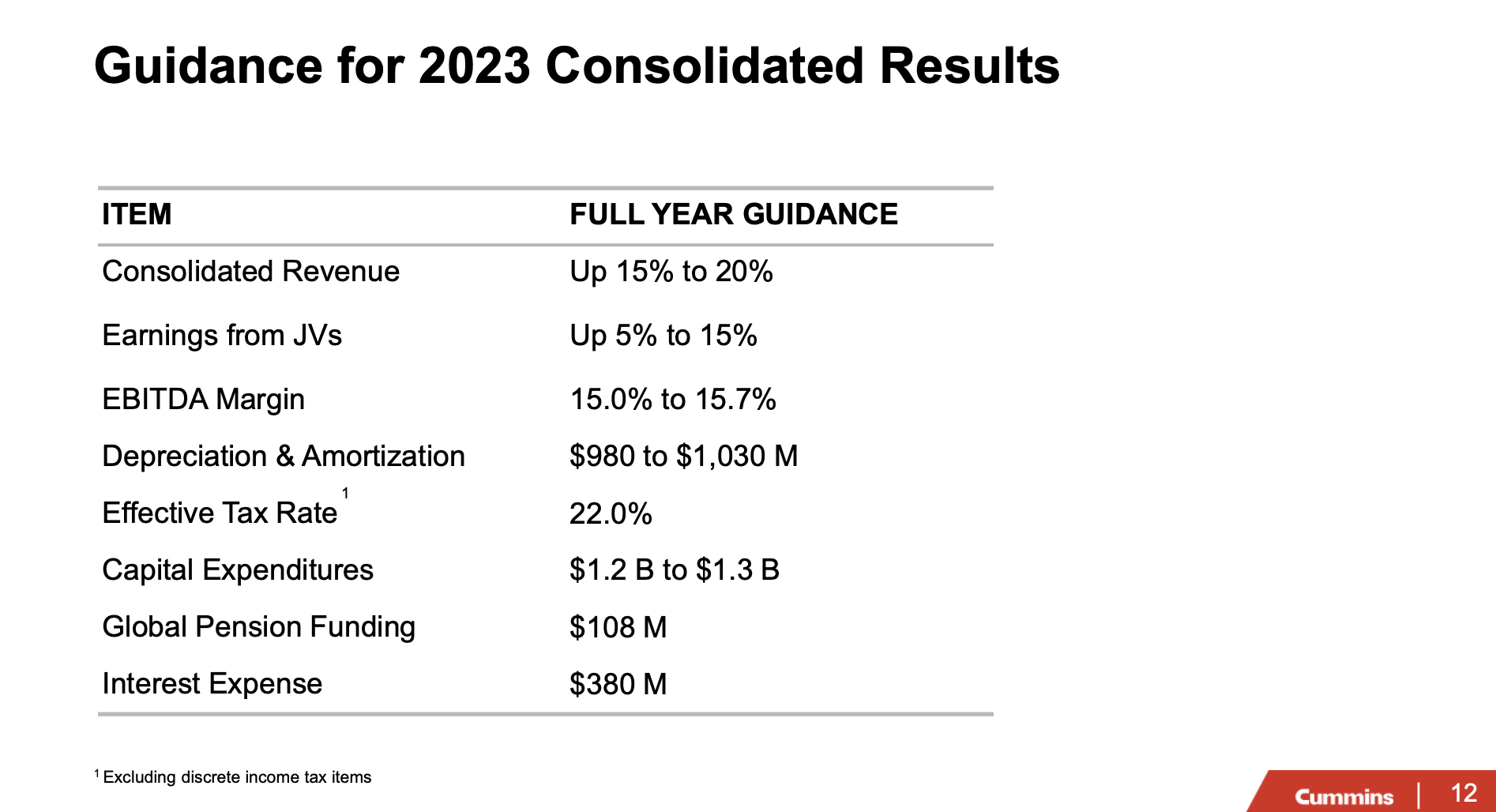

Despite slowing economic growth, Cummins experienced strong demand for its products across all key markets and regions, resulting in record revenues of $8.5 billion in the first quarter of 2023. That's a 32% increase compared to the same quarter in 2022.

The company's EBITDA also reached a record high of $1.4 billion or 16.1%.

Revenues in North America grew by 39% to $5.1 billion, driven by the addition of Meritor and strong demand.

In China, revenues increased by 16%, with improvement in on-highway markets. The company also mentioned growth in other international markets, like India and Brazil.

Not only that, but Cummins raised its forecast for total company revenue in 2023 to be up 15% to 20% compared to the previous guidance of up 12% to 17%.

The improved outlook is driven by stronger demand for Meritor in North America. The company also expects higher demand in the heavy-duty truck and power systems markets, as well as increased aftermarket revenues compared to 2022.

{kind=link}

But wait, there's more!

During the very recent Deutsche Bank Annual Global Industrials & Materials Summit , Cummins reiterated the massive tailwinds it benefits from.

The company started by making the case that weakness in truck orders is temporary.

Chris Clulow, Head of Investor Relations at Cummins, mentioned that while truck orders have seen a moderate increase in recent months, the order boards for 2024 are still mostly closed, and 2023 is already quite full.

The company had initially expected moderation in the fourth quarter, but now it seems that the second half of the year will be equally strong in the truck market.

Clulow also noted that there is no indication of a slowdown in builds, as the OEMs are requesting more trucks, and backlogs continue to grow.

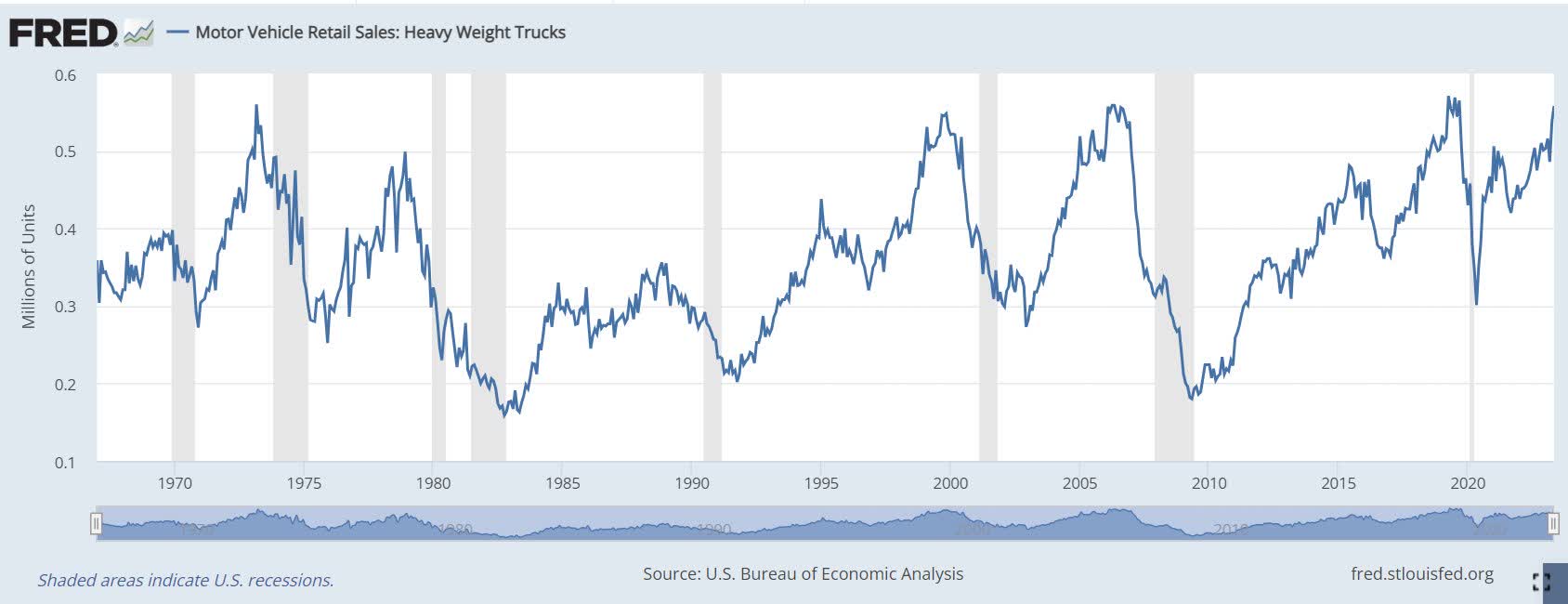

Related to this, the chart below shows sales of heavy-weight trucks.

Federal Reserve Bank of St. Louis

{kind=link}

Founder and CEO of FreightWaves, Craig Fuller , commented on this somewhat unusual development. I added some emphasis.

Mid-sized and large fleets buy their trucks at regular intervals, regardless of the economy . In fact, some increase purchases during recessions (thanks to easy access to drivers and OEM incentives).

From 2020 - 2022, mid-sized and large fleets were not able to get allotments due to supply chain shortages and a robust retail truck market (dealer scalping). They also held on to trucks longer than usual (2 years older than normal).

[...] Now, truck drivers are much easier to find, the "apocalypse" uncertainly is long forgotten, and those trucks they held onto for 2 extra years are worn out.

The largest fleets also know with the availability of truck drivers (so long "shortage"), they will be able to grow market share. So what we are looking at in truck order data is not related to robust freight demand, but rather a bulking of orders from the COVID economy among mid-sized and large fleets .

This has been confirmed by Cummins. During the Deutsche Bank summit, the company highlighted that medium-duty fleets are underserved due to supply chain challenges, leading to pent-up demand.

The industry currently has an 80,000-unit backlog in medium-duty, indicating strong future production.

Cummins also suggested that the average age of the fleet remains extended, and there is still a need to bring in new vehicles to reduce the average age further.

Furthermore, new trucks are seen as an advantage in attracting and retaining drivers.

Additionally, fleets perceive the freight recession as temporary, expecting a return to normalcy after an inventory correction. Needless to say, if that doesn't happen, weakness in new orders down the road might be amplified.

It's also important to mention that Cummins expects to benefit from new emission standards.

During the summit, Cummins mentioned that its Components segment is experiencing significant growth due to the emission standard changes in China and India.

With the implementation of BSVI in India and NS VI in China, there are now enhanced fuel systems, turbos, and after-treatments on everything in operation in these markets.

The business has expanded as emissions regulations progress, presenting opportunities for Cummins to gain market share. Automated manual transmissions in China, along with the company's partnerships with Isuzu and Daimler, further contribute to the growth of the Components business.

Cummins believes that Components could be one of the higher growth aspects of Cummins' portfolio in the ICE-driven segment, particularly as emissions regulations continue to evolve.

In 2022, India and China accounted for 14% of total sales. In 2021, that number was 18%. I believe that the aforementioned benefits and the Chinese economic reopening will cause that exposure to exceed well beyond 20% in the next few years, making these secular developments major drivers of long-term growth.

Additionally, CMI is improving its supply chain.

{kind=link}

In May, Cummins announced the acquisition of two CV manufacturing plants from Faurecia in Indiana and my home country, the Netherlands.

This move is part of the company's strategy to secure its supply chain for critical components at favorable prices. The acquisitions aim to ensure the continuity of supply and mitigate potential risks.

This deal also helps Cummins meet the USMCA content requirements, which will come into effect in 2027.

So, what about the valuation?

Valuation

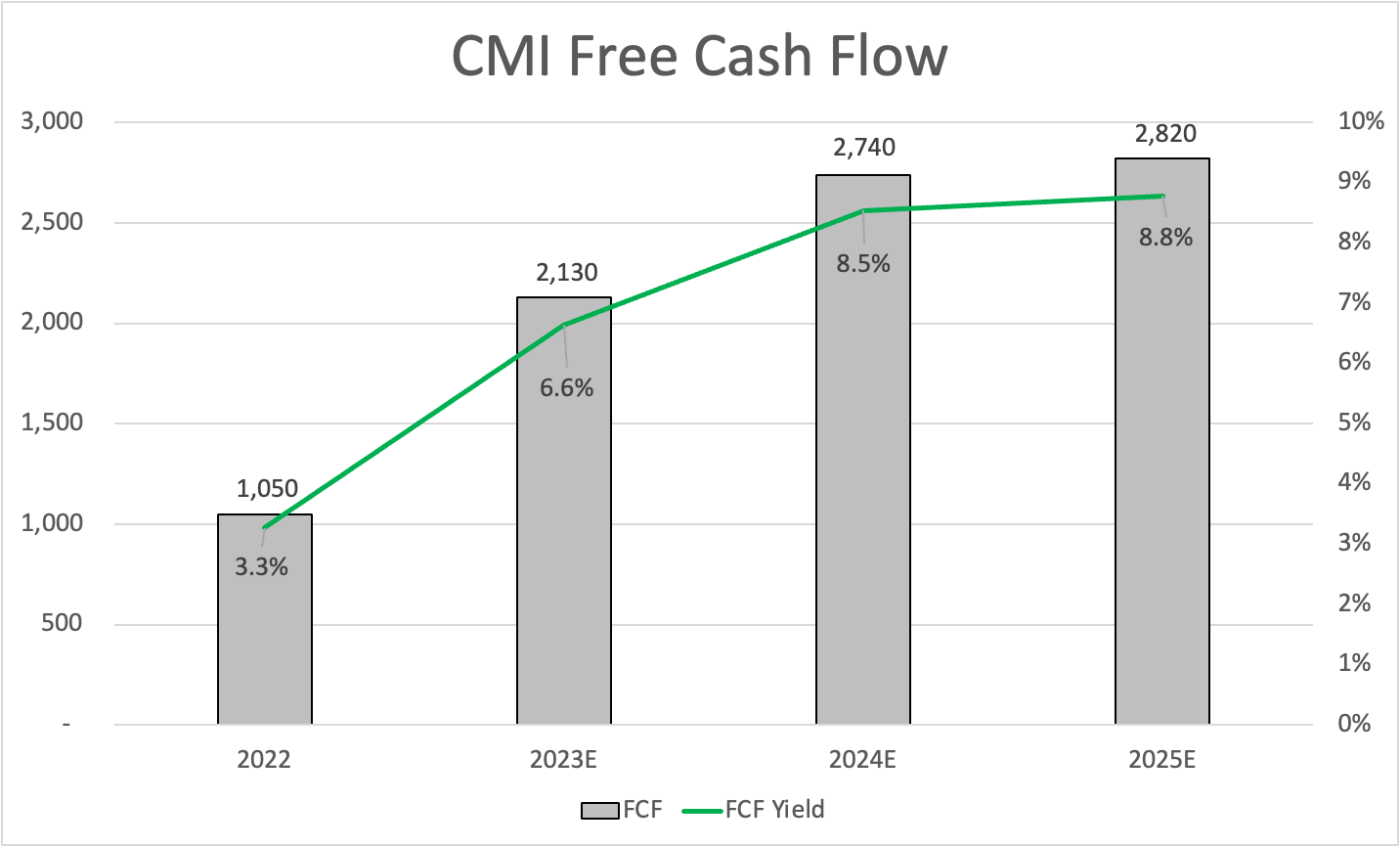

Looking at free cash flow estimates, it seems that the company's outlook is expected to be accurate by analysts. Free cash flow is expected to gradually increase to $2.8 billion by 2025, which would imply a free cash flow yield of almost 9%.

{kind=link}

When adding that the company has an A+-rated balance sheet with a net leverage ratio of less than 1x EBITDA, we get a favorable environment for more aggressive dividend growth and buybacks down the road.

Furthermore, these numbers imply that CMI is trading close to 11x 2024E free cash flow, which would imply that the CMI stock price has significant upside potential in the next two to three years, as CMI usually trades close to 15x free cash flow.

This would imply a longer-term price target of $300, which is roughly 30% above the current price.

The same goes for the forward EV/EBITDA ratio, which is below the longer-term median.

Needless to say, macroeconomic risks remain elevated. While I do believe that CMI has a bright future with a high likelihood of peer outperformance, we could see more downside to the $180 to $200 area if the economy deteriorates further.

I have close to 50% industrial exposure. While I am enjoying the current upswing, I'm not chasing any rallies but mainly buying on weakness.

The only reason why I do not own Cummins is that I own both Deere & Company ( DE ) and Caterpillar ( CAT ), which gives me enough machinery exposure.

My bullish rating is a longer-term rating.

Takeaway

Cummins stands out as a compelling industrial stock with a strong dividend track record and the potential for outperformance in the future. Despite being part of a cyclical industry, Cummins has consistently rewarded its investors with dividend hikes and buybacks.

The company's dividend scorecard is impressive, with 17 consecutive years of growth and a payout ratio of less than 34%.

Moreover, Cummins has demonstrated its ability to outperform the market and its industrial sector peers, delivering a 16.4% annual return since 1999.

While the engine market has become more mature and economic challenges persist, Cummins is well-positioned to benefit from unexpected tailwinds. The company has shown resilience in the face of a potential recession, reporting strong demand and record revenues in its recent quarter.

With a positive outlook, Cummins expects higher revenues in 2023 and anticipates continued growth in its components segment driven by emission standard changes and strategic acquisitions.

Considering the favorable valuation, high free cash flow estimates, and solid balance sheet, Cummins presents an attractive investment opportunity, albeit not without risks.

For further details see:

Recession? Tailwinds? How Attractive Is Cummins' 3% Yield?