RXRX - Recursion Pharmaceuticals: More Hype Than Substance Amid Signs Of Progress

2024-01-12 11:03:11 ET

Summary

- Recursion Pharmaceuticals stock price has risen by nearly 50% in the past month, currently trading at around $11 per share.

- The company raised over $500 million in its IPO, making it the sixth-largest biotech-focused IPO of the decade.

- Recursion's business model focuses on using AI and big data to discover new drugs, but the high costs and risks involved are a concern.

Investment Overview

The last time I covered Recursion Pharmaceuticals, Inc. ( RXRX ) for Seeking Alpha was back in May last year , when I gave the company's stock a "hold" rating. Shares were priced at ~$9 at the time, and briefly spiked to a high of $15.5 in June last year, before falling to a value of ~$5.5 late in the year. Across the past month, however, the share price has risen by nearly 50%, and currently trades at ~$11 per share.

Recursion IPOd in April 2021, issuing 27.88m shares at a price of $18 per share, and raising >$500m - making it the sixth largest biotech-focused IPO this decade. Recursion refers to itself as a "techbio" company, and, according to its Q3 quarterly report / 10Q submission :

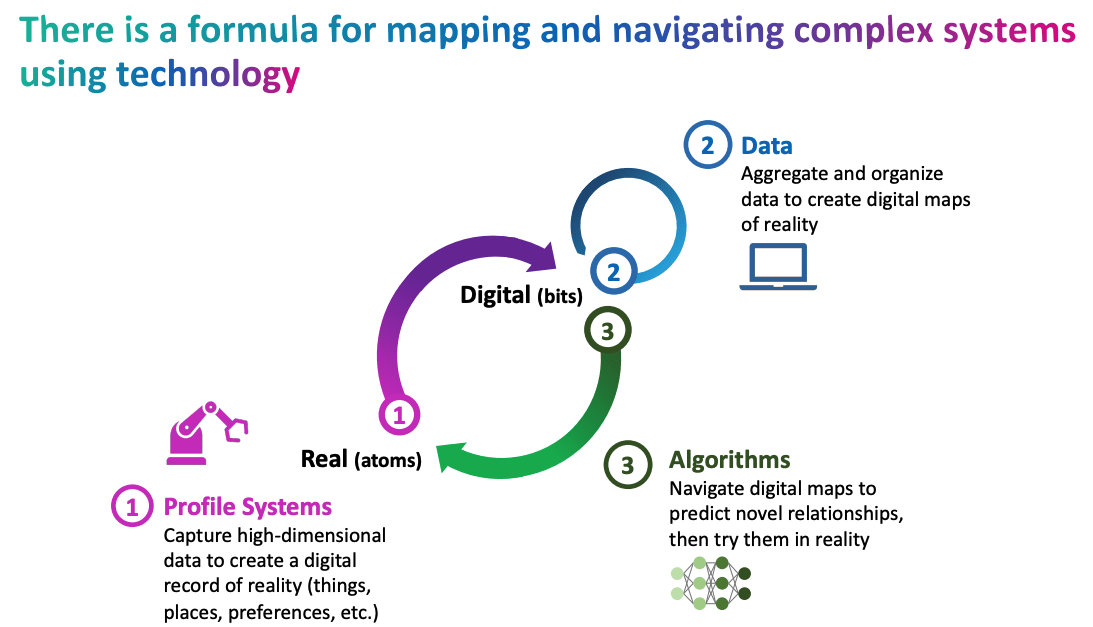

Central to our mission is the Recursion Operating System ((OS)), a platform built across diverse technologies that enables us to map and navigate trillions of biological and chemical relationships within the Recursion Data Universe, one of the world’s largest proprietary biological and chemical datasets.

We frame this integration of the physical and digital components as iterative loops of atoms and bits. Scaled ‘wet-lab’ biology and chemistry data built in-house (atoms) are organized into virtuous cycles with ‘dry-lab’ computational tools ((BITS)) to rapidly translate in silico hypotheses into validated insights and novel chemistry.

Our focus on mapping and navigating the complexities of biology and chemistry beyond the published literature and in a target-agnostic way differentiates us from other companies in our space and leads us to confront a fundamental cause of failure for the majority of clinical-stage programs - the wrong target is chosen due to an incomplete and reductionist view of biology.

A more straightforward description of the business model can also be found in Recursion's latest investor presentation (which runs to >100 slides), as shown below:

Recursion - business description (investor presentation)

{kind=link}

As I discussed in my two previous notes on Recursion for Seeking Alpha, while the mere mention of Artificial Intelligence ("AI") is capable of giving any company's stock price a lift across almost any sector, it can be hard to pin down precisely what benefit AI might be playing in improving outcomes.

Recursion believes it can make the process of drug discovery faster and more precise via use of "big data," algorithms, machine learning, etc., allowing itself and its partners to search for and discover exciting new drug candidates directed against novel targets, and ultimately develop drugs that can establish themselves as standards of care in commercial markets. Turning to the latest 10Q again, Recursion says it has:

a portfolio of clinical-stage, preclinical and discovery programs and continues scaling its Recursion OS with more than 200 million total phenomics experiments, multi-timepoint live-cell microscopy, transcriptomics, proteomics, inVivomics, data related to multi-target compound interactions and physicochemical properties, as well as large language model derived disease relevance and target-compound relationships.

Data have been generated in-house by the Recursion OS across approximately 50 human cell types, an in-house chemical library of approximately 1.7 million compounds, and an in silico library of over 1 trillion small molecules, by a team of approximately 550 Recursionauts that is balanced between life scientists and computational and technical experts.

I have several issues with this type of business model, however. To begin with, Recursion is focused on finding and developing completely new drugs, starting at the very beginning of the process, by feeding data into a supercomputer and hoping it finds some positive correlations.

That means that, partner milestone payments aside - which are generally lower when a drug is in its earlier stages of development - Recursion has no prospect of earning any revenues from the drugs it discovers until it has guided them through pre-clinical studies, established proof of concept in e.g. mouse of non-human primate models, gained approval from the Food and Drug Agency ("FDA") to begin in-human studies, conducted Phase 1, 2 and 3 clinical trials to prove its drug is superior presently on the market, applied for full approval, and waited 6-12 months for the FDA to study the data and make a decision on approval.

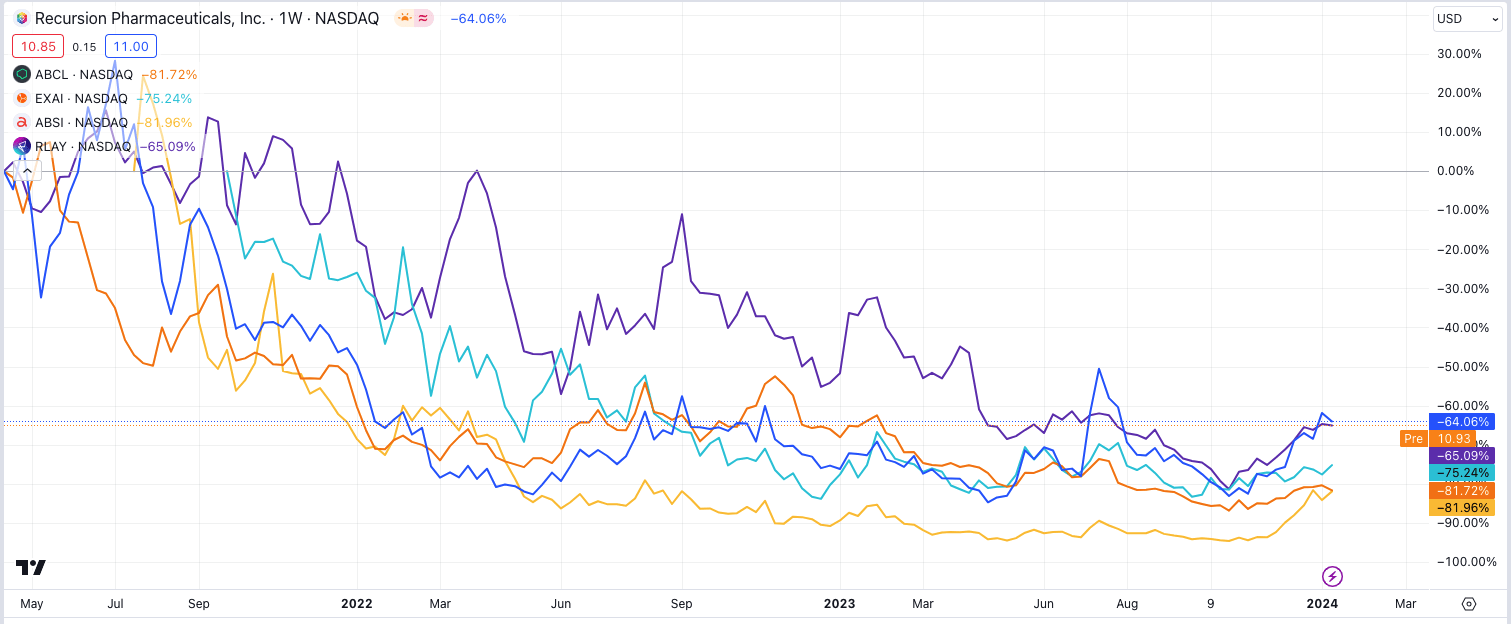

This is why, when AI-driven drug discovery companies - and there are a few, e.g., AbCellera Biologics ( ABCL ), Exscientia ( EXAI ), Absci Corp ( ABSI ), and Relay Therapeutics ( RLAY ) - discuss the prohibitive costs of drug development and the remote chances of a drug making it all the way to approval - Recursion states in a corporate video on its home page that the costs are ~$2bn, and failure rate ~90% - I consider this to be a weakness of the company, rather than a strength.

The drug developers clearly believe they can reduce costs, and increase likelihood of approval, whereas in fact their expensive super-computers likely increase the costs of the initial drug discovery stage. Based on evidence to date, at least, there is no compelling reason to believe a drug target identified by a supercomputer is any more likely to succeed than one picked by scientists who have a detailed working knowledge of which drug types work in which types of disease.

The present reality seems to me to be that if you are investing in an AI-driven drug discovery company, you will need to be extremely patient, as drugs presently take ~5 years to develop from preclinical studies through to approval, whether they are discovered by AI or by a PhD student, and embrace a high level of risk. This industry is still in its infancy and has no tangible track record of success to point to, although AI evangelists will doubtless argue that the data driven approach will eventually become all-pervasive, and in time, these companies will reap the benefits.

In the meantime, witness the 5-year share price performance of the 4 companies mentioned above, and Recursion, over a 5-year period (or since IPO), with all 5 stocks trading down >65%.

Share price performance of selected AI drug discovery companies (TradingView)

{kind=link}

Recursion - Partnership & Pipeline Overview

Despite my reservations around a business model that requires a very high cash burn - Recursion has recorded net losses of $(187m) and $(240m) in 2021 and 2022 respectively, and $(251m) across the first nine months of 2023 - that is essentially wagered on the prospect of discovering a drug capable of one day generating "blockbuster" (i.e., >$1bn per annum) revenues, however remote that possibility may be, Recursion has been able to both develop a pipeline and attract partners, theoretically de-risking its business somewhat.

Recursion's partner of most significance may be the German Pharma Bayer (BAYZF), which signed an amended and restated agreement with Recursion last year. According to Recursion's Q3 10Q:

Bayer will pay Recursion increased per program milestones which may be up to $1.5 billion for up to 7 oncology programs as well as royalties on net sales.

$1.5bn per successful oncology candidate certainly sounds impressive, with Recursion additionally earning mid-single digit royalties on future net sales of any drugs developed, but the deal has in fact cost Bayer only a $30m upfront payment and $50m equity investment to date, while it seems to me at least that Recursion assumes almost all of the costs of finding the candidates, and all of the risk, only receiving meaningful milestones when the candidate is substantially derisked.

Bayer only makes payments if Recursion successfully discovers a drug with "blockbuster" potential. However, as Recursion freely admits, the chances of finding such a candidate are extremely low, while the costs of looking for such a candidate are almost prohibitively high.

Nevertheless, Recursion also has deals in place with Swiss Pharma Roche ( RHHBY ), and its Genentech drug discovery subsidiary, which included a $150m upfront payment with $500m of milestones on the table, and up to $300m across a further 40 programs potentially, and on the technology platform side, in its Q3 earnings press release Recursion notes a deal done with Nvidia (NVDA), involving a $50m equity investment, as follows:

Expansion of Recursion’s in-house supercomputer, BioHive-1, with NVIDIA H100 GPUs will likely make it the most powerful computer wholly owned or operated by any biopharma company and among the 50 most powerful supercomputers on the Top500 List

Recursion is also partnering with Tempus in order to gain access to "over 20 petabytes of multimodal oncology data for the purpose of training causal AI models together with Recursion’s proprietary data."

At the JPMorgan Healthcare conference this week, Recursion has been providing live demos of its LOWE drug discovery software and interface that "can be used by any of our scientists from the comfort of their laptop." Presumably, Recursion may one day roll out LOWE as a bespoke product for biotech companies, but again, investors will need to be patient here and acknowledge that the risks involved in launching an untested product into a competitive life sciences market, in which budgets dictate that supply generally exceeds demand.

As I noted in a recent post on AbCellera , it strikes me that in biotechnology / drug discovery, it is much better to be the drug developer rather than the drug developer's partner, as if you genuinely have a "blockbuster" drug candidate on your hands, you may well extract billions of dollars of revenues, or be bought out by a Big Pharma concern at a huge premium to your last traded share price. The drug developer's partner, despite actually discovering the drug, stands to gain much less.

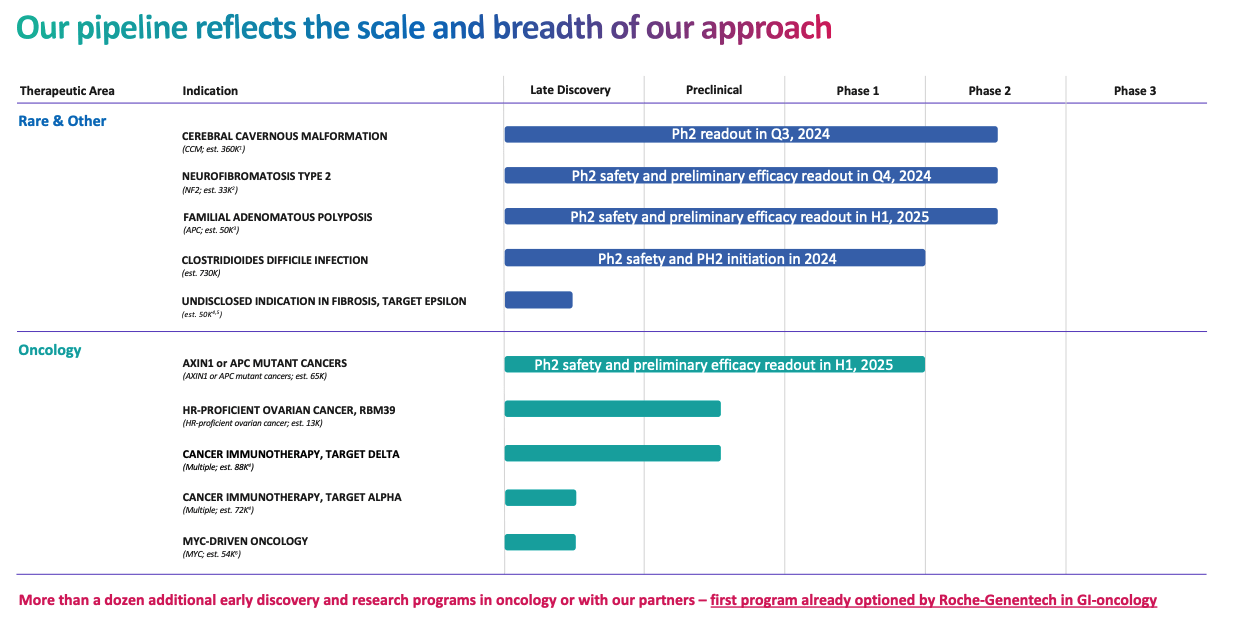

In that spirit, Recursion has been developing its own pipeline, as we can see below:

Recursion pipeline (investor presentation)

{kind=link}

I find it impressive that Recursion has been able to move three assets into Phase 2 studies, although the market opportunities in play may be somewhat uncertain.

For example, Recursion believes that cerebral cavernous malformation ("CCM") could be a 360k patient market, based on the number of symptomatic patients in the U.S. and EU - which is five times larger than the Cystic Fibrosis market - a market that has enabled Vertex Pharmaceuticals to generated nearly $10bn revenues per annum and command a market cap valuation of >$100bn.

With that said, the fact that there are no approved treatment for CCM may imply that patients only seek a medical cure in more extreme cases, substantially limiting the market opportunity. Either way, Recursion has promised Phase 2 data in Q3 2024, which is a catalyst investors should take note of.

There are also no approved therapies for Neurofibromatosis type 2 ("NF2") - a genetic condition that causes tumors to grow along the nerves, with a patient prevalence of ~33k, Recursion estimates. A Phase 2/3 study is underway, with data from the Phase 2 portion, involving 23 adults and 9 adolescents, has also been promised for 2H24.

The third Phase 2 stage study is in an oncological indication, tumors harboring AXIN-1 mutations, which are presently considered "undruggable." This is arguably a perfect use case for Recursion, its technology, and its brains trust of staff - helping drug targets that are well known, but inaccessible, as, for example, Mirati Therapeutics ( MRTX ) was able to do with the KRAS gene / protein, leading to the approval of its Krazati drug, indicated for non-small cell lung cancer ("NSCLC"), and a buyout by the Big Pharma Bristol-Myers Squibb ( BMY ), for nearly $5bn.

Recursion's pipeline includes several more intriguing drugs and target indications, such as the 50k patient market in Familial Adenomatous Polyposis, Clostridioides Difficile infection, ovarian cancer, and most recently, fibrosis, a condition that has defied most therapeutic approaches.

In summary, we can certainly make the case that Recursion has a nicely balanced portfolio of in-house drugs, with some intriguing targets, perhaps most notably CCM, that could lead to "blockbuster" revenue opportunities, provided the drug is effective and safe enough, and partnership opportunities, where any breakthrough of note is likely to be rewarded by a triple-digit million milestone payment, helping Recursion continue its heavy R&D spending.

Looking Ahead - RXRX In 2024 - Still More Hype Than Substance

Although it is possible to feel relatively upbeat about the progress Recursion is making, it could also be argued that the company has been given a considerable amount of leeway owing to its AI capabilities, and that most companies in a similar position to recursion - heavily loss making, with no near-term revenue prospects - would be severely testing shareholder's patience.

Despite Recursion - and AbCellera, Exscientia, and others' efforts to demystify and rationalise the drug development process, and boasts of having world class super computers doing their bidding, there must eventually come an inflection point where the market considers what specific value proposition these companies offer?

Will Recursion ultimately be able to create a production line of best-in-class drugs, that it will develop with its partners, earning billions of dollars in milestone payouts? Will the company successfully launch a safe and effective CCM therapy, and open up a new market within the pharmaceutical industry? Will the company find ways to turn "undruggable" targets into "druggable ones."

Unfortunately, the reality may be that nobody knows how effective the AI-driven drug discovery business model may become, because the industry is so new. These companies, like every other Pharma and biotech, are attempting to find the "needle in the haystack" - the next blockbuster drug - faster, reaping the financial benefits of doing so.

It may be interesting to note, however, that drugs are discovered in all sorts of different ways - for example, Novo Nordisk's ( NVO ) GLP-1 agonist semaglutide, approved in weight loss and diabetes as Wegovy and Ozempic respectively, and expected to become an all-time best-selling drug, was discovered through the study of a lizard's venom. Would a supercomputer have been able to discover a GLP-1 agonist?

This neatly articulates my problem with AI drug discovery companies. So long as they hype their super-computers and processing powers, these companies will likely find enough investors willing to invest large sums of money, and not panic about heavy losses - Recursion spent $172m on R&D in 2023 to the end of Q3, but it is hard to know if its partnerships will ultimately reap any milestone payments - the Pharma can walk away at any time without paying a cent - or if its pipeline has genuine promise, or is being pushed towards more obscure targets and indications due to a lack of genuinely promising targets discovered to date.

Investors are prepared to be patient, but it is hard to effectively quantify what return on their investment they are expecting. It can feel as though investors are expecting a miracle, akin to buying a lottery ticket, given how difficult, lengthy, expensive, and risky the drug development process is.

This dilemma helps to explain why Big Pharma will often pay a triple-digit percentage premium to acquire a biotech with a later study stage, derisked drug with a good chance of making it to market. The further back you start, the higher the risk, AI supercomputer or no AI supercomputer, and the higher the cost, which encapsulates my issue with drug discovery / target identification as a business model.

As such, my belief is that in 2024, Recursion stock will likely meander somewhat, as the company continues its search for effective drug targets, while the goodwill of investors is retained. There will be a couple of significant data readouts - in CCM, NF2, and Clostridioides Difficile - although I would argue that these indications are not the ones that Recursion and its clients and investors would ideally like to work within long-term, with oncology and autoimmune the substantially more lucrative fields.

In summary, I think frustration with AI-driven drug development may be a theme of 2024, as investors face up to the fact that overnight success is not a feature of this industry, despite what may have been promised. There is enough substance to what Recursion and others are doing, however, in my view, for the market not to lose faith.

I hope I am wrong and we see genuine volatility in 2024, but ultimately, if you are an investor looking for volatility and price catalysts galore in 2024, Recursion stock may not be for you. If you want to buy a ticket for the great AI drug discovery lottery, a small investment in Recursion Pharmaceuticals, Inc. stock may pay out in 3-5 years' time.

For further details see:

Recursion Pharmaceuticals: More Hype Than Substance Amid Signs Of Progress