RRR - Red Rock Resorts: Overvalued When Accounting For Risk At Current Highs

2023-07-25 05:41:24 ET

Summary

- Red Rock Resorts has seen significant growth due to strong earnings and resilient consumer demand, but its balance sheet and overvaluation make it a hold recommendation.

- The company's strategic acquisitions, such as the Palms Casino Resort, have helped to diversify its income sources and increase its market presence.

- However, Red Rock Resorts faces risks including economic factors and dependence on the Las Vegas market, which could impact its financial performance.

Red Rock Resorts (RRR) has experienced significant growth following strong earnings due to resilient consumer demand. I believe that Red Rock Resorts is currently a hold because even though the company's core business model is solid, the firm's balance sheet along with overvaluation assuming my DCF figures means I cannot recommend a buy at this time until its fundamentals become more attractive.

Business Overview

Red Rock Resorts, Inc. creates and manages gaming and entertainment facilities in the US. Las Vegas Operations and Native American Management make up its two main operating segments. In the local Las Vegas market, the firm owns and manages nine smaller casinos in addition to six gaming and entertainment venues. Additionally, it oversees the northern Californian Graton Resort & Casino.

Red Rock Resorts

Financials

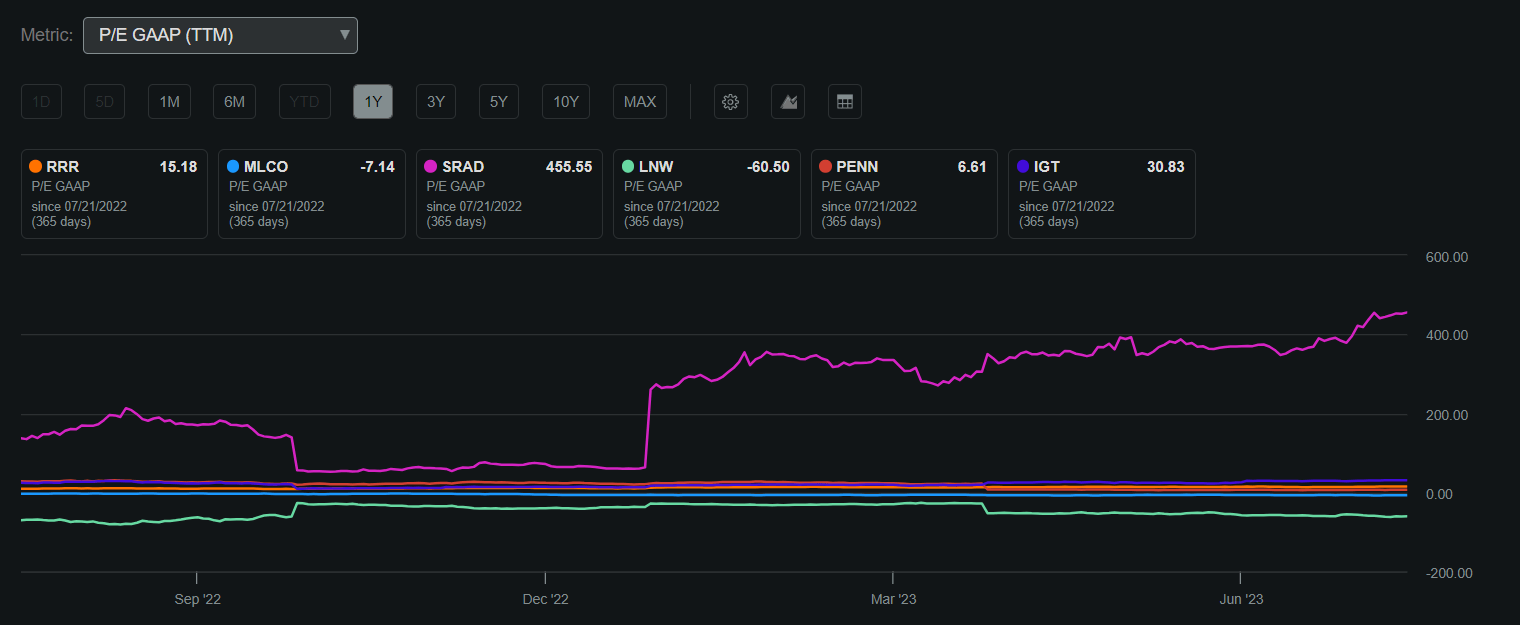

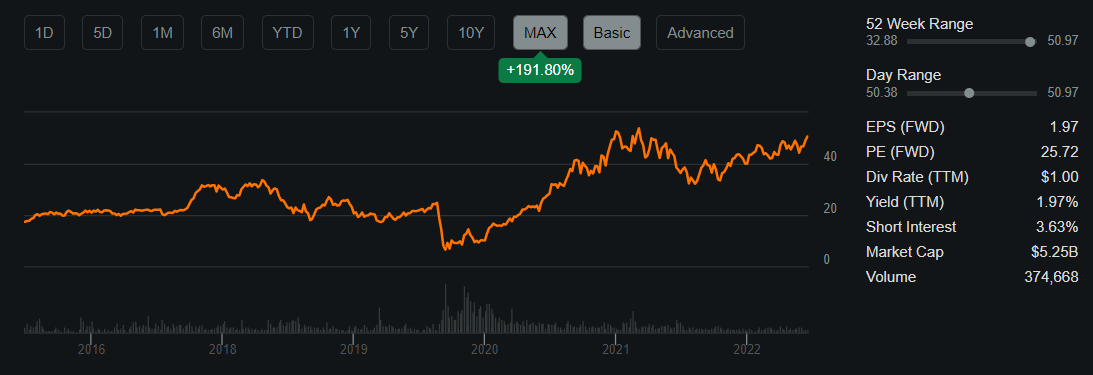

Red Rock Resorts currently boasts a market capitalization of $5.25 billion and an impressive return on invested capital of 18%. The stock price is currently trading at $50.66, which is near its 52-week high of $50.97. Notably, the company's GAAP P/E ratio stands at 15.18, indicating that Red Rock may be undervalued compared to its peers within the industry. This suggests that despite the stock's current high price, there is a possibility of undervaluation, making it an interesting prospect for investors.

{kind=link}

Red Rock also pays a dividend of 1.97% which holds a payout ratio of 29.13%. I believe that this yield allows Red Rock to reward shareholders with fairly strong income while also maintaining a safe FCF outflow and sufficient funds to remain competitive by improving its core business model along with reducing risk through improved financial resiliency.

{kind=link}

Earnings

Red Rock's Q1 2023 results came in excellent beating on the top and bottom lines with EPS exceeding expectations by $0.25 at $0.75, and revenues beating estimates by $20.55 million at $433.60 million demonstrating an 8% year-over-year growth. This beat in earnings demonstrates the firm's ability to endure headwinds such as high rates and inflation and shows the company's resiliency during such times. With earnings guidance looking positive into 2024 and 2025, Red Rock is displaying its ability to foster growth in a multitude of ways.

Earnings Estimates (Seeking Alpha)

Performance Compared to the Broader Market

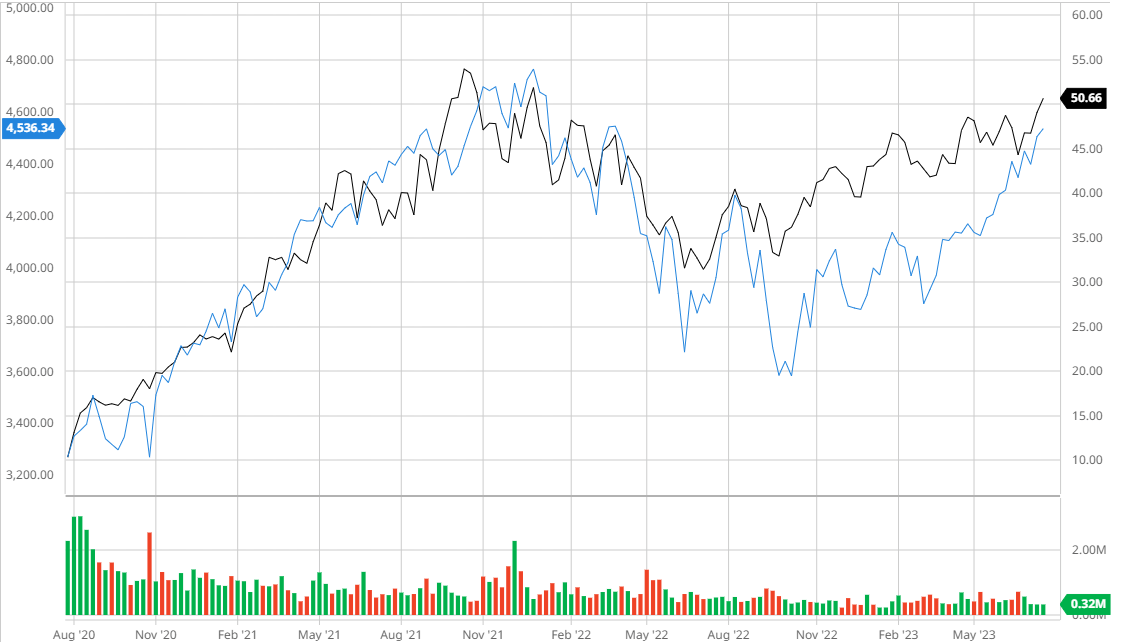

Over the past 3 years, Red Rock has outperformed the S&P 500 when adjusting for dividends. I believe that this outperformance exemplifies Red Rock's ability to effectively allocate cash flows to create compounding growth and strengthen the company's top and bottom line, creating shareholder value.

Red Rock Compared to the S&P 500 3Y (Created by author using Bar Charts)

{kind=link}

Analyst Consensus

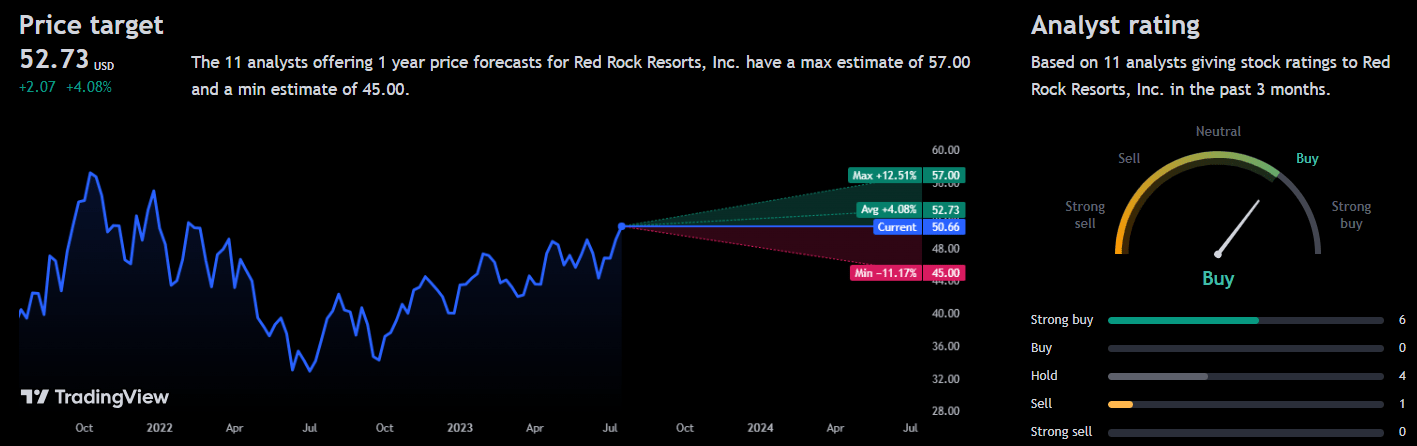

Over the past 3 months, analysts have rated Red Rock as a "buy" with an average 1Y price target of $52.73 presenting a potential 4.08% upside. This demonstrates that although the company has seen strong growth recently, analysts believe that there is still room to expand but also recognize that valuation must keep pace to expand its price targets.

{kind=link}

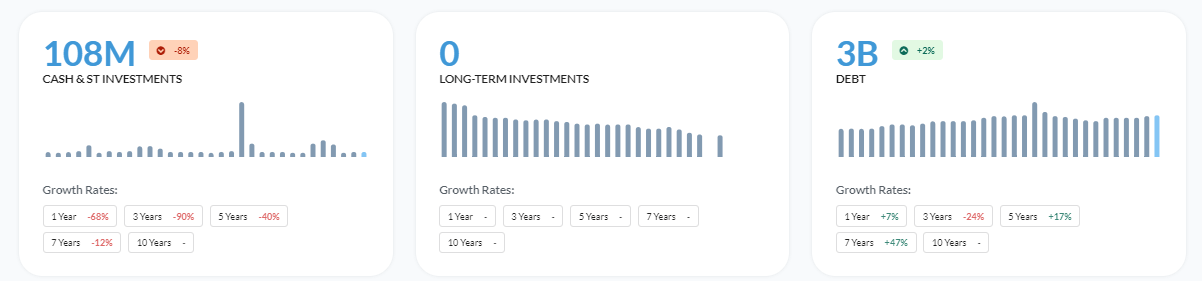

Balance Sheet

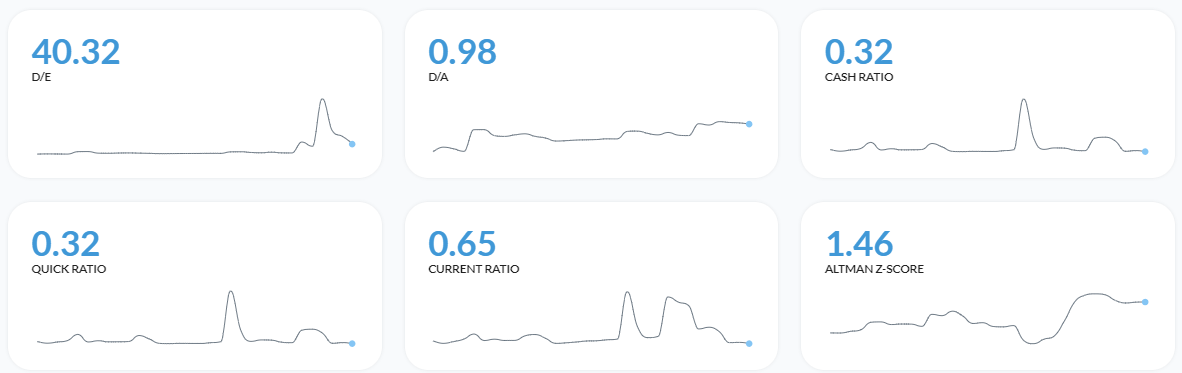

Although Red Rock Resorts has seen great success this year, the company's balance sheet is fairly weak, especially in current macroeconomic headwinds. With debt expanding while cash and investments decline, the company's liquidity and short-term ability to pay liabilities have deteriorated. But, one positive aspect of Red Rock's debt is that they still hold an interest coverage of 4.48x demonstrating that the company can endure a high rate environment with current income levels. But, with a low current ratio of 0.65 and Altman Z-Score of 1.46, investors must take this risk into account as it may pose problems for the company in recessionary times.

{kind=link}

{kind=link}

{kind=link}

Valuation

Before finding Red Rock's fair value using a DCF, I was able to pinpoint an accurate discount rate to utilize in order to receive a fair value when compensating for all internal and external factors. First off, I was able to calculate a Cost of Equity of 7.79% by using a risk-free rate of 3.84% which is in line with the current yield for the 10-year treasury.

Cost of Equity Calculation (Created by author using Alpha Spread)

Assuming the previous calculation, I was able to use the Cost of Equity value to find a WACC of 5.73% for Red Rock Resorts. This WACC is under the industry average of 9.18%.

WACC Calculation (Created by author using Alpha Spread)

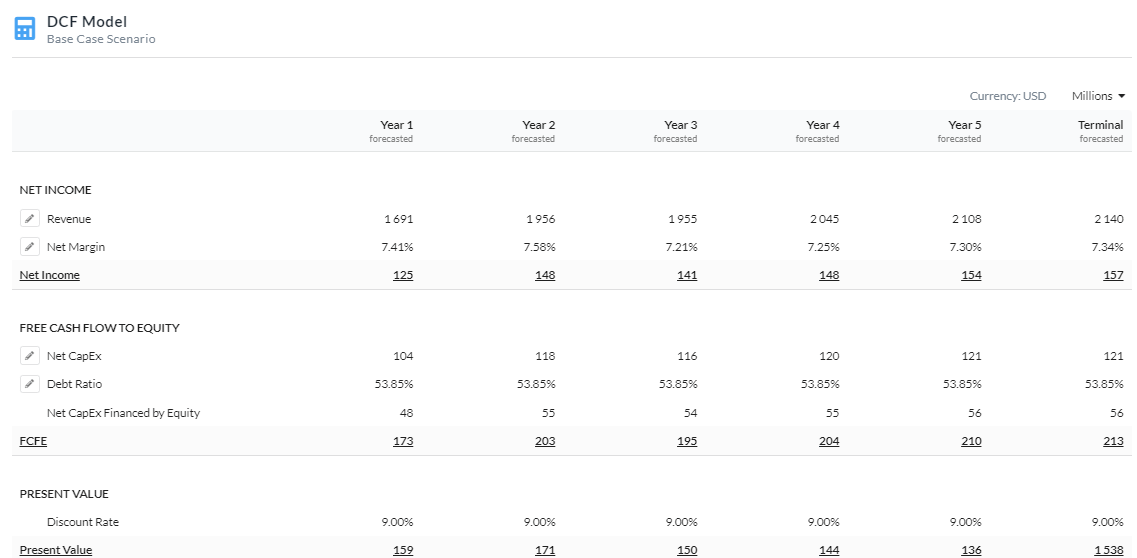

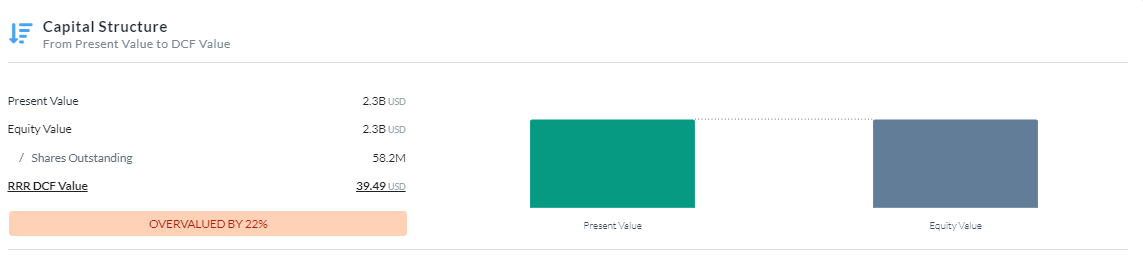

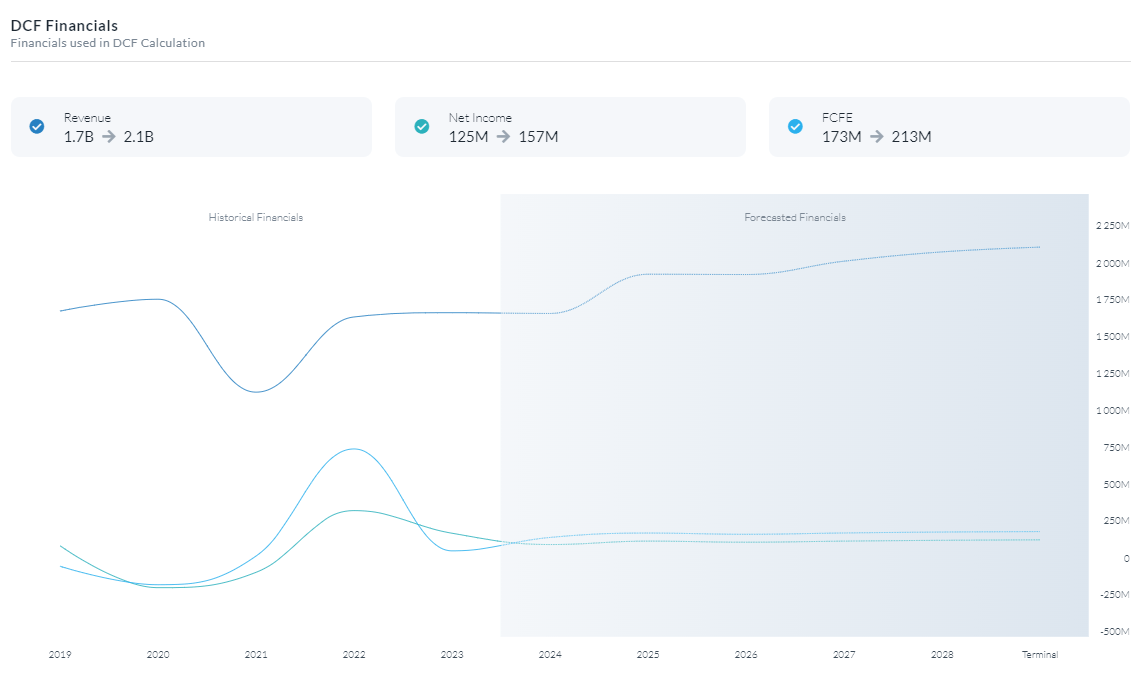

Now that I have an accurate discount rate, I was able to compute Red Rock's fair value using a 5Y Equity Model DCF using FCFE. Using a discount rate of 9%, Red Rock is currently overvalued by 22% with a fair value of $39.49. I decided to add a 1.21% risk premium to my assumptions to account for the firm's rather risky balance sheet coupled with macroeconomic headwinds weighing the firm's ability to leverage to withstand declines or to foster growth. Furthermore, I estimated that margins and revenues will continue to grow in line with expectations.

5Y Equity Model DCF Using FCFE (Created by author using Alpha Spread)

{kind=link}

{kind=link}

{kind=link}

Strategic Acquisitions Resulting in Compounding Growth

By making smart acquisitions of gaming and entertainment sites, Red Rock Resorts hopes to increase its market presence and diversify its sources of income. The company's purchase of the Palms Casino Resort in Las Vegas is a famous illustration of this tactic.

Red Rock Resorts bought the Palms Casino Resort for $ 312.5 million in May 2016 through its subsidiary Station Casinos LLC. The purchase included the casino resort building, which has a gaming floor, numerous dining options, bars, and entertainment options. The Palms is a desirable addition to Red Rock Resorts' portfolio of properties because of its opulent amenities, celebrity-endorsed suites, and exciting nightlife options.

Red Rock Resorts was able to increase its footprint in the local Las Vegas market and reach a new consumer base as a result of this transaction. Red Rock Resorts' previous properties were enhanced by The Palms' distinctive brand and entertainment options, which also gave the firm the chance to draw in a wider spectrum of clients, including younger and more affluent ones. Due to a bigger target market and more opportunities to grow its devoted client base, Red Rock was able to take advantage of more consistent cash flows as a result of market diversification.

Red Rock Resorts also benefited from cost savings and operational synergies as a result of the purchase of the Palms. The business was able to improve the operations of the Palms and boost profitability by utilizing its current managerial know-how and infrastructure. Due to this, Red Rock was able to increase its FCF and use the increased revenue to further benefit from compound growth.

Red Rock Resorts' strategic purchase of the Palms turned out to be a wise choice that helped the business expand and develop in the very competitive Las Vegas gaming market. Since the company sold the company for $650 million in 2021 , the acquisition of Palms Casino proved to be successful due to the income it produced for the firm and the large return on investment, doubling its initial investment in a period of 5 years.

I believe that future acquisitions such as the purchase of Palms Casino will allow Red Rock to improve cash flows and result in great investments as the firm has demonstrated its ability to choose promising peers and use its large scale to tap into undiscovered growth.

Palms Casino

Risks

Economic Factors: Revenue and profitability at Red Rock Resorts are vulnerable to shifts in the economy, including changes in consumer spending, unemployment rates, and consumer confidence. Discretionary expenditure on gambling and entertainment may decrease during economic downturns or recessions, which could have an impact on the company's financial performance.

Dependence on the Las Vegas Market: The regional Las Vegas market is where Red Rock Resorts has the majority of its assets. As a result, the company's performance is highly correlated with the regional economy and tourism patterns. The financial success of the corporation could be impacted by any unfavorable changes to the Las Vegas market.

Conclusion

To summarize, I believe that Red Rock Resorts stock is currently a hold because even though the company's core business model is solid, the firm's balance sheet along with overvaluation assuming my DCF figures means I cannot recommend a buy at this time until its fundamentals become more attractive.

For further details see:

Red Rock Resorts: Overvalued When Accounting For Risk At Current Highs