MATX - Red Sea Turmoil Is Bullish For Maersk And Peers

2024-01-10 06:54:47 ET

Summary

- Spot rates for marine transportation have surged due to geopolitical concerns, which could boost profits for the shipping industry.

- A.P. Møller - Mærsk has been affected by attacks in the Red Sea, but has a strong financial condition, making it an interesting investment opportunity.

- Shipping through the Red Sea has been suspended, causing disruptions and increased costs for shipping global freight and containers.

- Shipping companies themselves stand to benefit, with Maersk being a solid example.

For anybody who is interested in or who follows closely the shipping industry, these are most certainly some interesting times. Spot rates for marine transportation have skyrocketed once again because of geopolitical concerns. In the near term, this kind of development should prove bullish for many of the companies in the industry. This is in spite of the risks that some have faced up to this point. And although geopolitical issues, particularly those related to armed conflict, are always a net negative for the world, this could be exactly what the shipping industry needs to help boost profits just as the space has returned to normal following the COVID-19 pandemic era.

In analyzing these developments, there are a few companies that I have decided to look at. But the one that is most interesting to me at this time is A.P. Møller - Mærsk ( AMKBY ). Just like others in the industry, A. P. Moller Maersk has been negatively affected by a return to normalcy in the industry. But it truly has been ground zero when it comes to what is currently transpiring. Add on top of this the company's robust financial condition, and I see no reason why investors should not be bullish.

Fascinating developments

If you were to look at the share price of A.P. Møller - Mærsk over the past year, you would find yourself thoroughly disappointed. In 2023, the S&P 500 generated a return, including distributions, in excess of 26%. And yet, over the past year, shares of A.P. Møller - Mærsk have declined by 13.2%. It's important to keep in mind, however, that you can cherry-pick data with any investment. If you look at just the past month alone, for instance, shares of the logistics giant have generated upside of 27.6%. That's massive upside over such a short window of time.

If you heard the news regarding what is going on in the Red Sea, you might find this kind of appreciation peculiar. Earlier this month, management decided to suspend all shipping through the Red Sea ‘until further notice’. This came after Houthi militants attacked the Maersk Hangzhou vessel at the tail end of December. This followed a brief period of time in which A.P. Møller - Mærsk had previously paused operations, only electing to resume those after receiving protection from the US military.

The fact that you are reading this article tells me that you care more about understanding the business complications associated with what is going on than the geopolitical ones. But in this case, they are inexorably intertwined. The short version of the story is that, in response to Israel’s retaliatory war against Hamas in Gaza, the Houthis, who are backed by Iran, have decided that the time to stir trouble is optimal. Given the religious differences between the parties involved, this seems like a peculiar arrangement. I say this because both Iran and the Houthis are Shiites while Hamas is a Sunni group. These two different branches of Islam are highly antagonistic toward one another. But as the saying goes, ‘the enemy of my enemy is my friend’. And in the eyes of all three parties, Israel is the bigger foe.

Given all of this conflict, A.P. Møller - Mærsk is not the only company that has decided to pause operations in the Red Sea. Just recently, Cosco Shipping Holdings Co., Ltd. ( CICOF ) became the latest party to do so. Others have as well. This is an issue for the shipping industry more broadly because, according to some estimates, about 12% of all global freight and 30% of all global container volumes are transported through that region. This will require shipping to be redirected, with much of it having to transport passed the Cape of Good Hope in South Africa. This means increased costs for the transportation of many goods, most significantly those that are on their way from China to Europe or from Europe to China.

{kind=link}

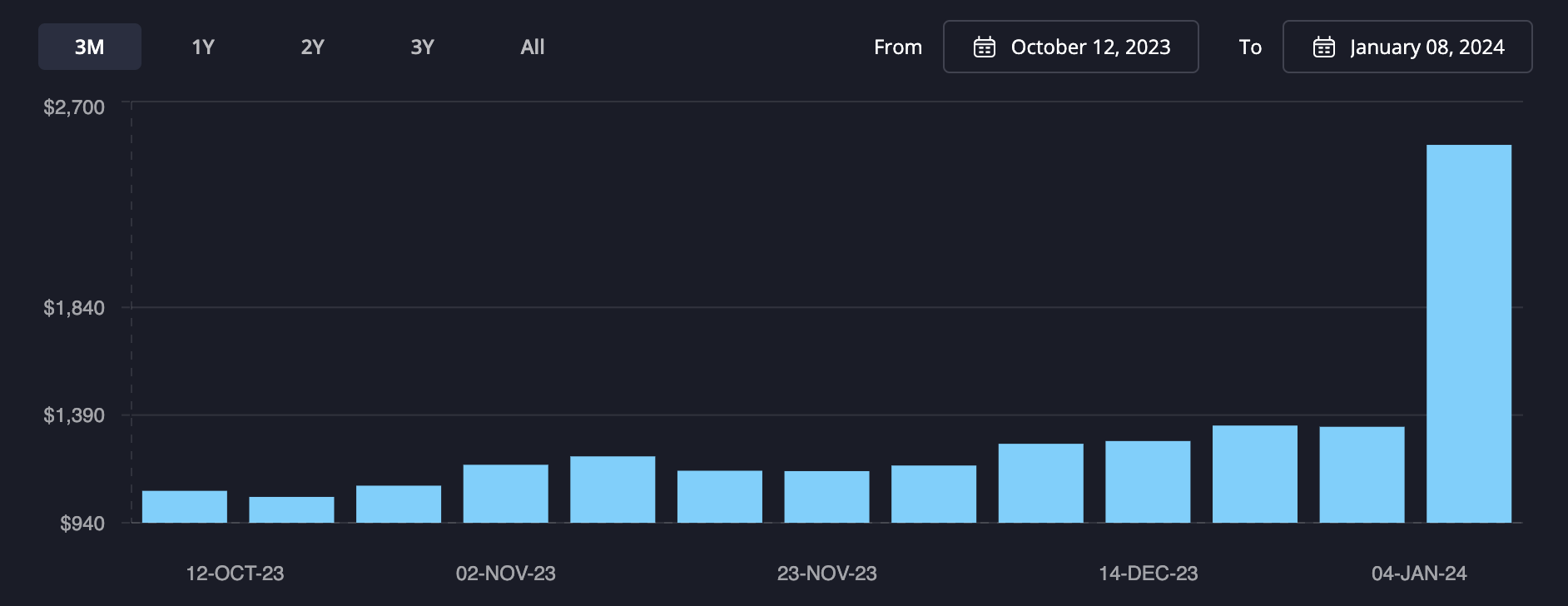

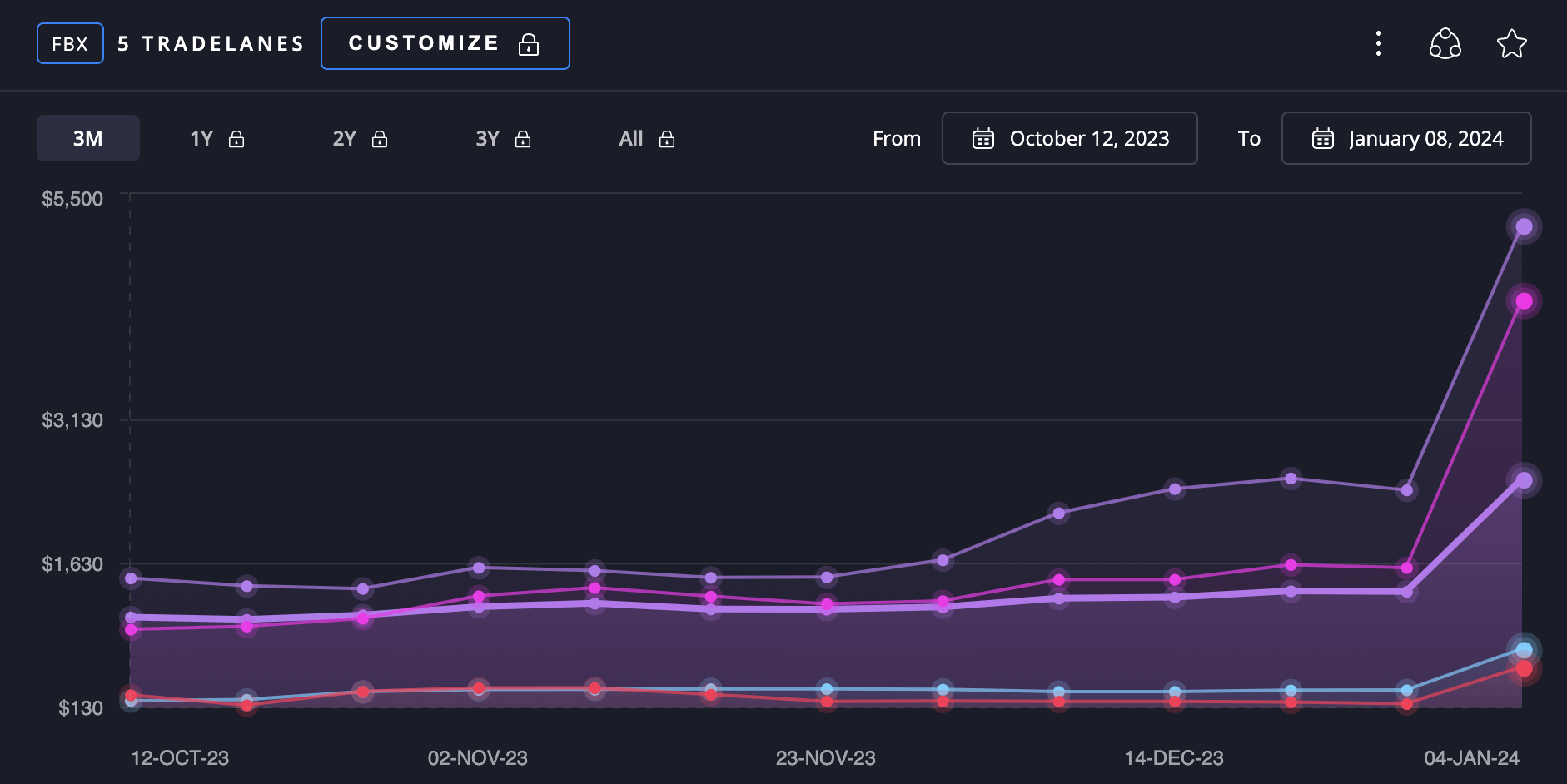

In the image above, you can see freight rates, as measured by the Freightos Baltic Index, covering the past three months. From the final week of December through the first week of January, this index skyrocketed from $1,341 to $2,519. This is the average global spot rate, according to the index, of transporting a single 40-foot shipping container from point A to point B. In the image below, you can see additional data that includes trade through the Suez Canal. The cost of transporting a 40-foot shipping container full of product from China or somewhere else in East Asia to the Mediterranean area has shot up 115% in just a week from $2,401 to $5,168.50.

{kind=link}

Traveling the other direction, from the Mediterranean to China or elsewhere in East Asia, has skyrocketed even more, in the amount of 228%, from $169 to $554.75. If this disparity compared to the other direction of travel seems odd, keep in mind that China's status as the world's factory means that there's plenty of demand to send goods from that region elsewhere. The return trip often sees far less demand, resulting in significantly lower spot rates. And it's better to charge something small and book product than to return completely empty. Traveling from China or elsewhere in East Asia to north Europe has shot up by 176% over the same window of time, growing from $1,590 to $4,391 while costs in the other direction has grown 138% from $312 to $744.

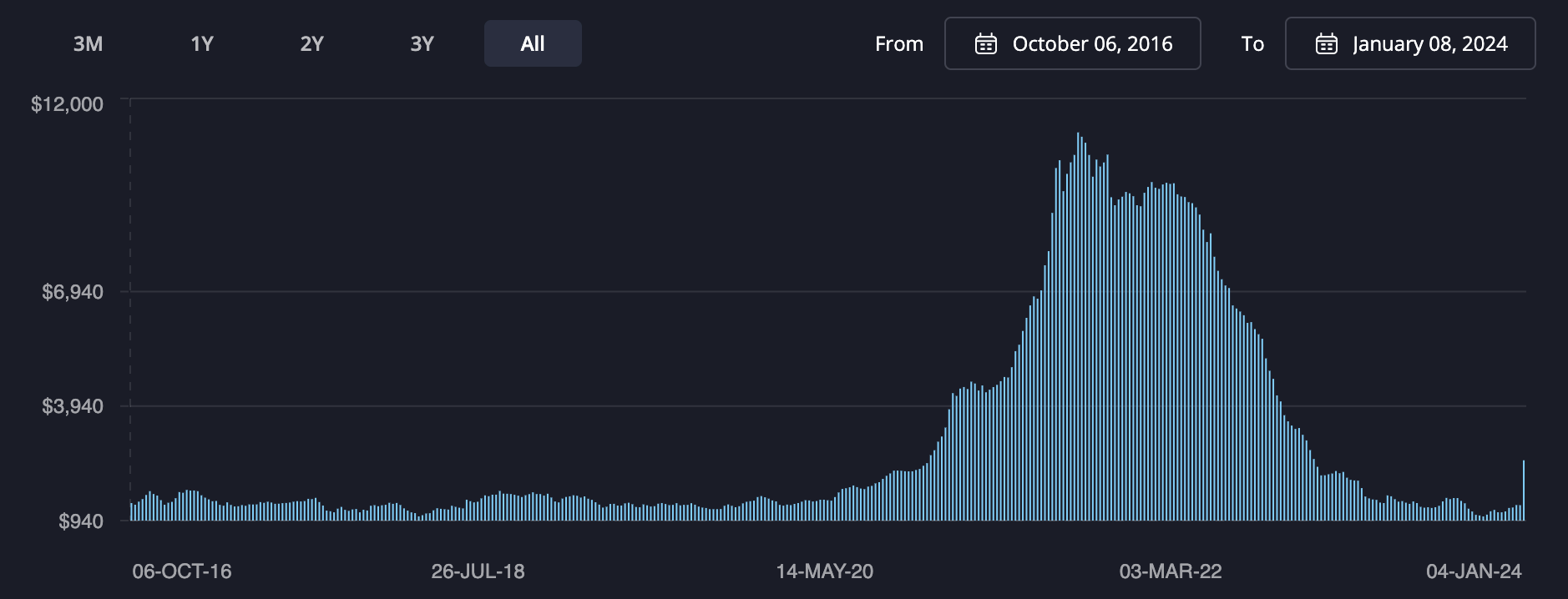

Honestly, this comes at a fantastic time for the shipping industry. Although it has certain inconveniences, the space has come under a lot of pain over the past year or so. As you can see in the chart below, spot rates in the shipping space spiked tremendously following the emergence of COVID-19. As late as May of 2020, the global spot rate averaged less than $1,500. But during the height of the supply chain crisis that emerged because of the pandemic, prices exceeded $11,000. But as the aforementioned chart illustrates, prices have come down hard since then, returning to a state of normalcy.

{kind=link}

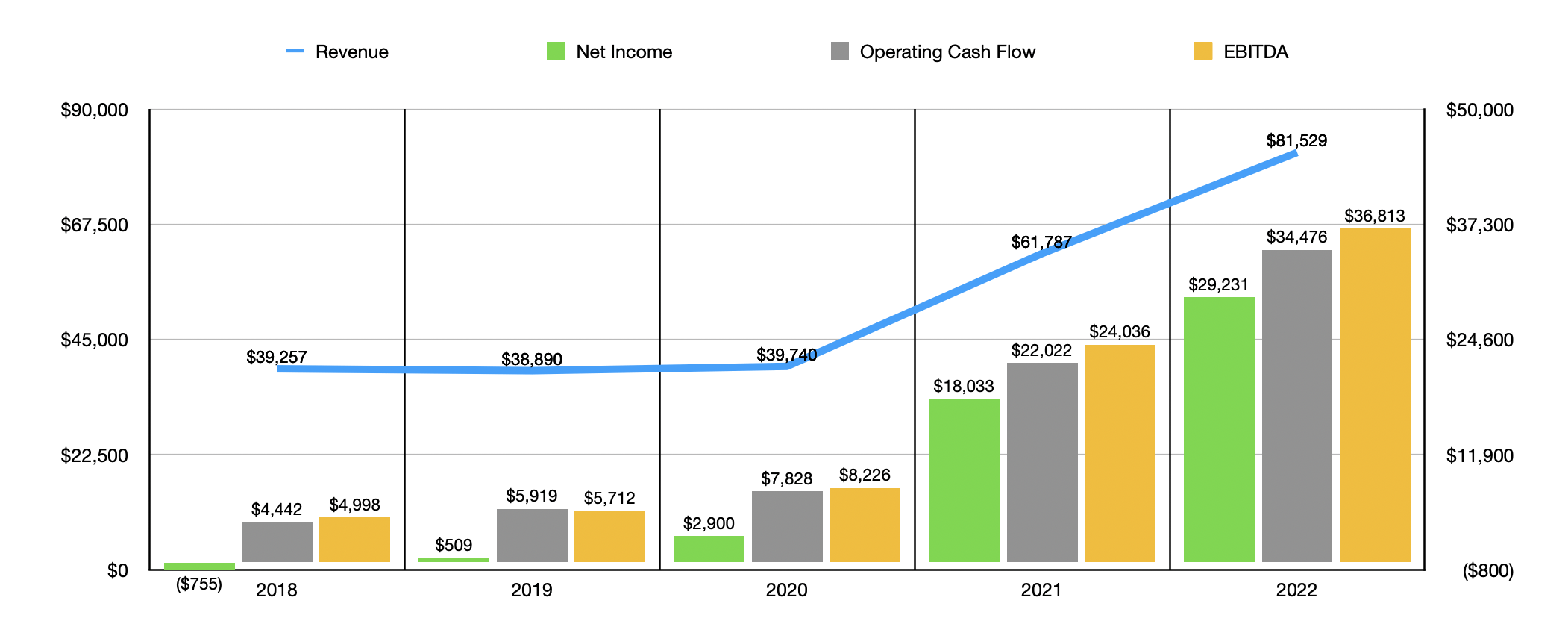

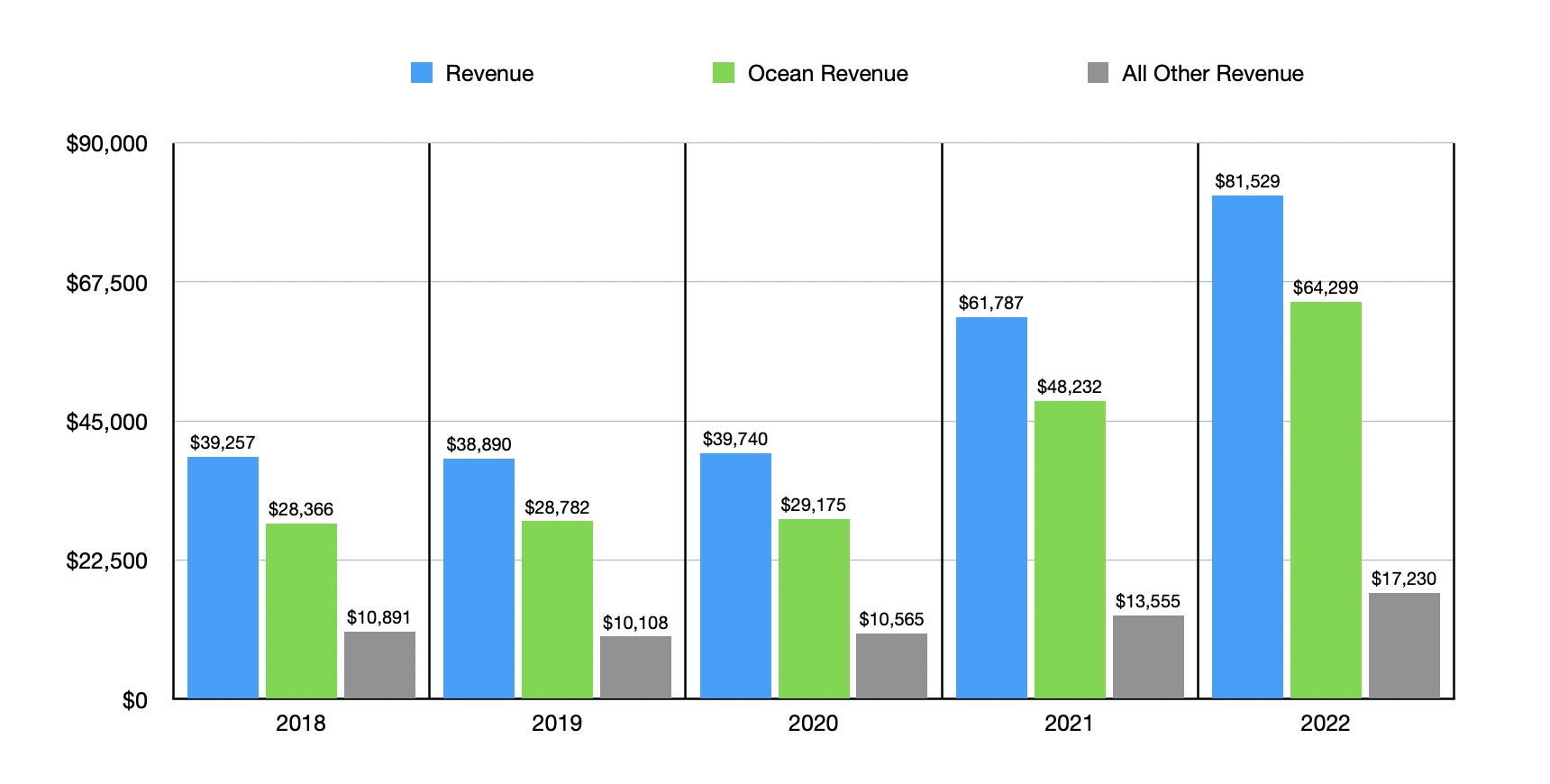

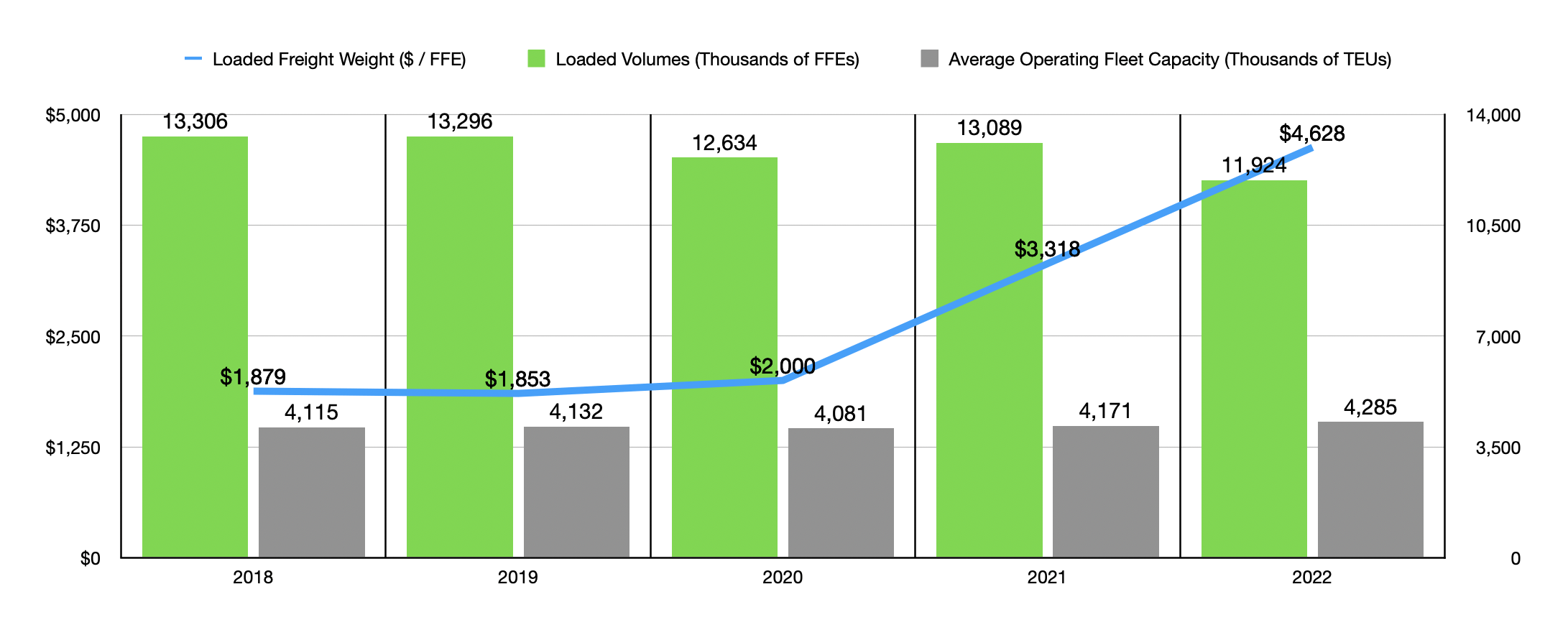

The end result of this decline has been painful for every player in the space. As an example, just look at financial performance reported by A. P. Moller Maersk. Back in 2020, the company generated $39.7 billion of revenue. This shot up to $81.5 billion in 2022. While the TEU (twenty-foot equivalent units) operated capacity for the company increased during that time from 4.08 million TEU to 4.29 million TEU, the loaded volumes of goods transported by the company dropped from 12.63 million FFEs (forty-foot equivalent units) to 11.92 million FFEs. While the company did actually see a small increase in 2021, the general downtrend began even before 2020. Back in 2018, for instance, loaded volumes came in at 13.31 million FFEs.

{kind=link}

While the company did benefit tremendously from strength in its Logistics and Services operations during this window of time, almost all of the upside from a revenue perspective came from its Ocean business, which is the part of the business responsible for transporting goods. Revenue for this unit jumped from $29.2 billion in 2020 to $64.3 billion in 2022. And that was largely attributable to an increase in the loaded freight rate from $2,000 to $4,628 per FFE. This allowed the profitability of that particular segment soar, resulting in overall profits for the company shooting up as well. Keep in mind that in 2020, net profits were only $2.9 billion. They jumped by a multiple of 10 to $29.2 billion by 2022. Operating cash flow and EBITDA followed a very similar trajectory.

{kind=link}

{kind=link}

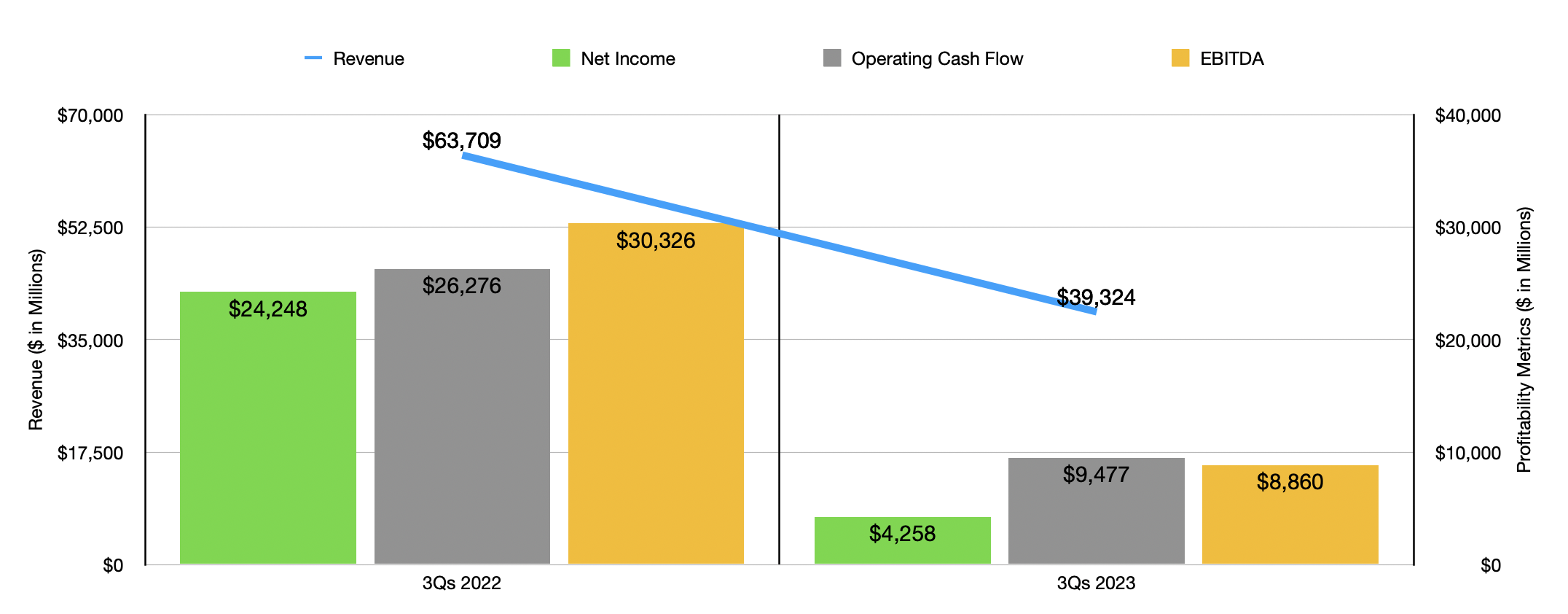

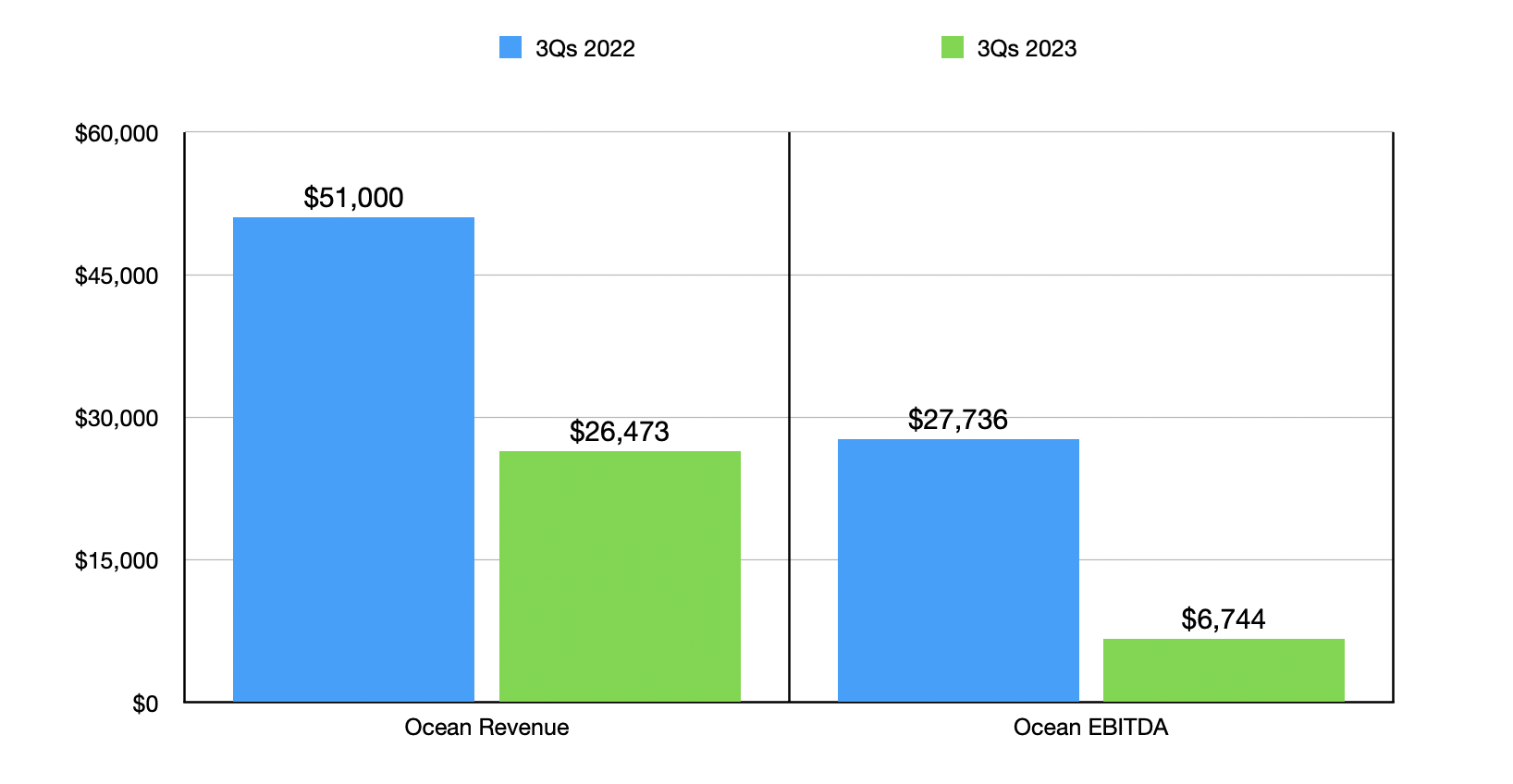

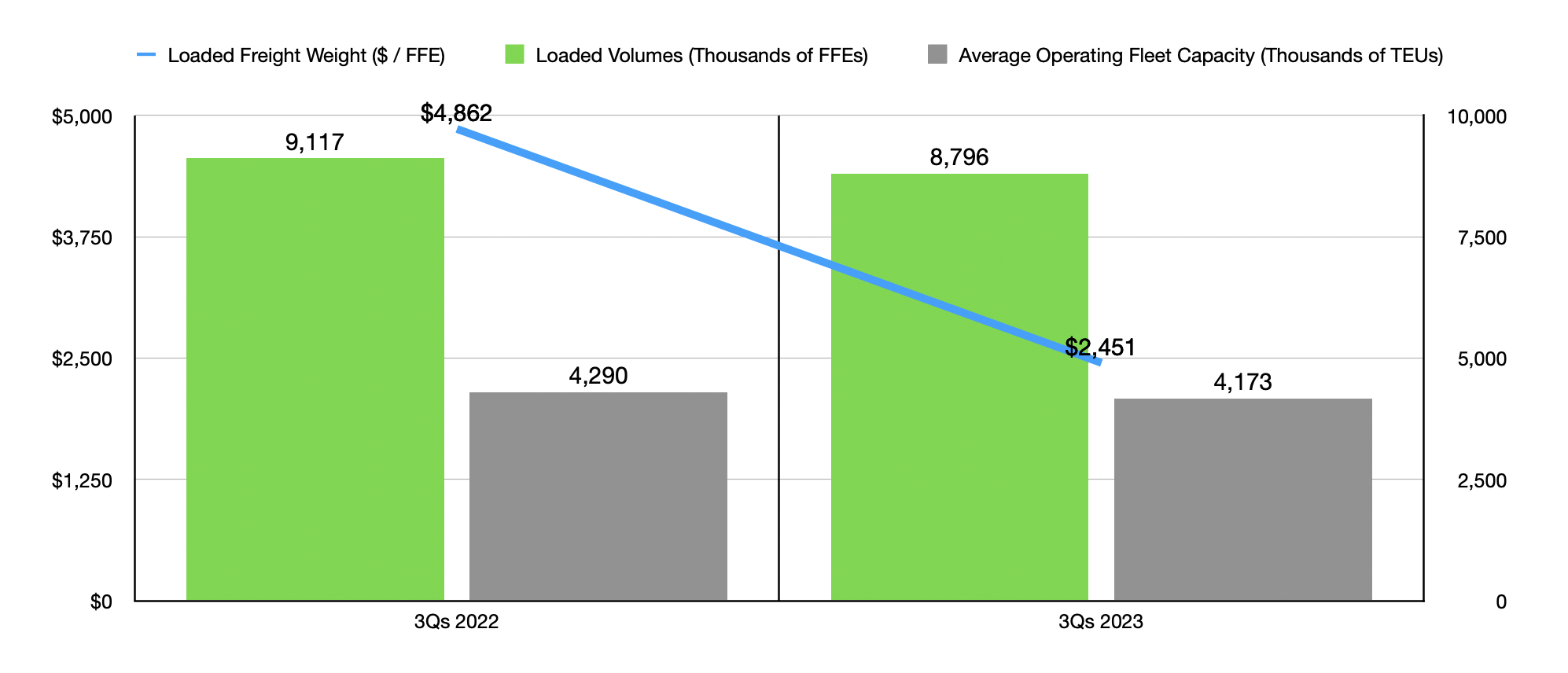

It's not difficult to know what transpired once rates began normalizing. As supply chains cleared up, economic growth slowed, and new ships came into the industry, it was destined for rates to fall. Total revenue for the company in the first nine months of the 2023 fiscal year, for instance, came in at only $39.3 billion. That's a little more than half the $63.7 billion reported the same time one year earlier. Net profits plummeted from $24.2 billion to $4.3 billion. Operating cash flow declined from $26.3 billion to $9.5 billion. And EBITDA fell from $30.3 billion to $8.9 billion. While a 3.5% drop in loaded volumes did not help, a plunge in the loaded freight rate for the company from $4,862 to $2,451 did most of the damage.

{kind=link}

{kind=link}

Unfortunately, the industry is destined to return to these more normal levels. In fact, I would be surprised if rates don't ultimately drop further. But that's not the end of the world. Even at the company reverts back to the kind of profitability it achieved in 2020, shares look quite cheap. The firm is trading at about 3.9 times 2020’s operating cash flow. Add on top of this that the business has cash that exceeds debt totaling $6.84 billion, and the enterprise is truly in a solid position for the long haul. Having said that, this surge in rates should definitely help it as it passes on higher costs to its customers. It helps that, at present, about 32% of its volume is associated with either the spot rate or short term contracts.

{kind=link}

There are other players to keep in mind

Although this article is primarily focused on A. P. Moller Maersk, I would be lying to you if I said that it is the only player that will benefit from these developments. Another key beneficiary is certain to be Cosco Shipping. Looking at the first half of the 2023 fiscal year , we see that the ‘group’ for the company came in at $11.7 billion compared to the $30.6 billion reported the same time of 2022. Cosco Shipping Lines, meanwhile, reported a drop in revenue from $20.4 billion to $7.9 billion. All of this was driven by a plunge in rates, with the group rate dropping from $2,895.81 to $1,159.22 and the Cosco Shipping Lines rate falling from $2,957.49 to $1,213.32. Given that about 23.3% of the revenue associated with Cosco Shipping Lines comes from the Asia and Europe route, the company should see some rather meaningful disruption caused by these issues. But since it is a Chinese company and its goods are still in demand from places like Europe and the US, the general rise in rates should, at least temporarily, serve as a boon for the business.

Two other companies that investors should at least have on their radar include ZIM Integrated Shipping Services ( ZIM ) and Matson ( MATX ). The former of these is based out of Israel. Over the past month, shares have spiked by 72.4%. Although this may sound odd considering that an Israeli company might be more impacted than one that is not just based on geography, it's important to note that only 13.3% of its shipping volume for the first nine months of 2023 was associated with the affected regions. Matson, meanwhile, does not have any exposure to the Red Sea area. However, it does have meaningful routes from Asia to the US. While rates on a global scale have been impacted, those involving the regions in which Matson operates should be comparatively less affected. This means that the company gets all of the benefit of higher rates without dealing with any of the risks.

Takeaway

All things considered, we are definitely in a period that is interesting. In the near term, it's clear that rates are going to remain elevated. And given that there is significant uncertainty regarding when the tensions in the Middle East will end, this should be a boon for the companies that benefit from higher rates. I personally believe that A.P. Møller - Mærsk makes for a great prospect during these times. But it's important for investors to understand that these rate increases will not last. At some point, we will see a decline again. But so long as the company does not see downside that would take its fundamentals lower than what they were shortly before the pandemic, the stock still looks attractively priced and the company's balance sheet is robust.

For further details see:

Red Sea Turmoil Is Bullish For Maersk And Peers