WU - Redefining Remittance: The Untold Investment Story Of International Money Express

2023-08-17 10:54:40 ET

Summary

- International Money Express (Intermex) offers an undervalued investment opportunity in the remittance industry, with a target share price of $24.96.

- Intermex distinguishes itself from competitors by focusing on strategic alliances, optimizing its agent network, and delivering exemplary customer service.

- The Latin American remittance industry is significant and has the potential for steady growth, driven by immigration patterns and technological advancements.

- At its current trading level, with a P/E ratio of 8.91x and EV/EBITDA ratio of 5.83x, this investment opportunity for savvy investors to seize upon is substantial.

Investment Thesis

International Money Express ( IMXI ), also known as Intermex, offers an intriguing small-cap investment prospect that might have eluded Wall Street's attention due to its association with the price-focused remittance industry it currently operates in. Following a Q2 performance that fell short of analyst expectations and a subsequent revision of its full-year guidance, the stock underwent a notable price decline, leading to a valuation reminiscent of the pandemic's lowest points. With my base case scenario pointing toward a target share price of $24.96, the present stock valuation appears incredibly undervalued in the eyes of market participants. While established competitors opt for price-cutting strategies to safeguard their market share, Intermex pursues a distinctive path by cultivating strategic alliances with highly effective partners and revolves around optimizing the efficiency and efficacy of its agent network, delivering exemplary customer services, and allocating capital efficiently. At its current trading level, with a P/E ratio of 8.91x and EV/EBITDA ratio of 5.83x, this investment opportunity for savvy investors to seize upon is substantial.

Company Overview

International Money Express, formerly known as Intermex since 1996, underwent a transformative merger with FinTech Acquisition in 2017. Under the visionary leadership of current CEO and President Robert Lisy, who assumed control in 2009, the company has amplified its unique remittance services. These services primarily facilitate money transfers from the United States of America to Latin America and the Caribbean ("LAC") region. This steadfast commitment has propelled the company to a prominent position as a leading omnichannel money remittance service provider. Moreover, the acquisition of La Nacional has bolstered the company's foothold in the Dominican Republic, which further fortifies its regional presence in the LAC region.

The cornerstone of International Money Express's success lies in catering to a specific niche: individuals in the United States with ties to Latin American and Caribbean countries seeking reliable and convenient remittance solutions. Many of these individuals lack a connection to traditional comprehensive financial institutions, making the company's offerings indispensable. Although alternate banking avenues may be accessible to these customers, they opt for Intermex's services due to the unparalleled trifecta of dependability, ease, and value. The company facilitates the movement of funds through an extensive network, which encompasses third party-operated locations across the United States and Canada, alongside company-operated stores strategically situated within the United States. The company derives revenue from remittance fees paid by consumers initiating transactions, which is then shared with agents involved in both the originating and destination countries. In addition, the company's proficiency in managing currency exchange spreads also bolsters revenue when dealing with local currencies not pegged to the U.S. dollar.

In fiscal year 2022, the agent network expanded by 27.3%, paralleled by a 21.2% surge in the principal amount sent, totaling a staggering $21.0 billion. This growth trajectory is further validated by the processing of nearly 47.8 million remittances, signifying a 19.2% surge in transactions compared to the preceding year.

Industry Overview

The Latin American remittance industry finds its momentum in the movement of immigration patterns, especially within the United States. In my view, this dynamic is intimately linked to labor trends, particularly in physically demanding sectors like construction, manufacturing, agriculture, and hospitality, which often employ hardworking Hispanic individuals who pour their efforts into these demanding jobs, driven by a common purpose of sending financial support back home. Despite not having the glamor of some industries, the remittance market holds substantial economic clout, quietly contributing its share to the GDP of various nations.

Interestingly, this market tends to fly under the radar of Wall Street, but its significance cannot be understated. Take the case of Mexico, for example, which offers a compelling narrative. Over the years, remittances to Mexico have evolved from being merely a financial trickle to a full-fledged economic stream. In fact, according to The Economist , these remittances surged from being around 1.9% of GDP in 2012 to a staggering 4.2% in 2022, which translated to an astonishing sum of roughly 60 billion dollars. To put things into perspective, this amount has even outshone traditional contributors to Mexico's foreign income like tourism, oil exports, and a large portion of manufacturing exports. This intriguing transformation exemplifies the latent power of the remittance market and how it can reshape economic narratives.

{kind=link}

Grand View Research

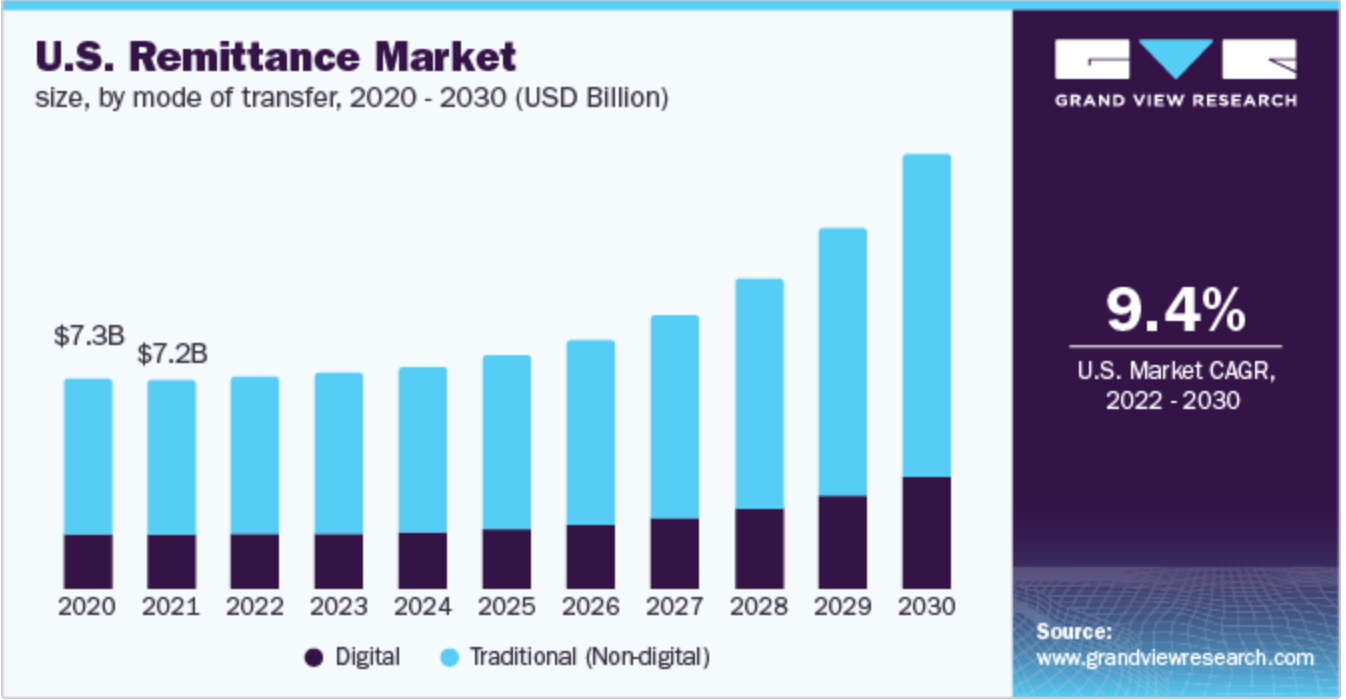

Based on the data provided by Grand View Research , the U.S. remittance market appears to be on a steady growth trajectory, with a projected compounded annual growth rate of 9.4% from 2022 to 2030. This growth is primarily attributed to the adoption of technological solutions, particularly the incorporation of real-time banking technology such as Immediate Payment Service ("IMPS"). Furthermore, factors like increased consumer spending power, rapid urbanization, and industrialization in emerging economies seem to be contributing to this upward trend. Additionally, a shift toward digital solutions seems to be taking place, driven by the preferences of the younger generation.

Within the current industry landscape, an interesting development worth noting is the competitive strategy of aggressive discounting during periods of market slowdown. As revealed in Intermex's Q2 2023 earnings call , there has been a moderation in year-over-year growth in the Latin America and Caribbean markets. This has prompted several competitors to adopt aggressive discounting, often involving the reduction of foreign exchange gains, as a means to sustain growth rates. Considering these changes, Intermex's management has made strategic adjustments to their outlook. Revenue guidance, previously projected in the range of $667.00 million to $688.50 million, has been revised to a new range of $644.9 million to $673 million. The prevalence of diminishing fees and narrower foreign exchange spreads has led to what can be described as a 'race to the bottom'. In this context, companies in the industry are required to adopt a comprehensive approach to succeed and demonstrate value.

A successful strategy, in my view, involves excelling across various dimensions, which encompasses strengthening brand equity, fostering proprietary technological advancements, and expanding the reach of the agent network. These elements collectively contribute to distinguishing companies within the industry and enabling them to differentiate themselves amidst the competitive pressures stemming from price-based strategies. For investors who prioritize companies with strong moats and a presence in industries characterized by high barriers to entry, the remittance sector might not immediately capture your attention. However, it's worth noting that within this seemingly straightforward industry, there exists a standout player that defies the odds. Allow me to illustrate how Intermex distinguishes itself from competitors, showcasing a track record of robust growth and impressive returns on capital despite the intensively competitive landscape.

Key Drivers & Main Catalysts

Foremost, Intermex strategically forges partnerships exclusively with highly productive agents, strategically positioning them within geographies of optimal profitability. In my view, this approach hinges on vigilant monitoring of individual sending agent performance and discerning money remittance trends. By doing so, the company is primed to extend real-time technical support and efficacious marketing assistance to bolster agents' productivity and amplify remittance volumes. CEO Robert Lisy aptly expressed this strategy in his conversation with FXC Intelligence , stating:

When I first took over, this company had over 5,000 retailers. I’ve cut it down to 2,000, and we grew throughout all of that. Western Union doesn’t do any more business to Latin America than we do, and they’ve got 75,000 retailers capturing 10 times as many wires in the US as we have. It’s about productive retailers in the right neighborhoods. Our average retailer probably does four to five times what the average retailer in the industry does, because we precisely place them in the right neighborhood. We do an onsite business review to understand how many wires we’re going to be able to get from that retailer. We just wouldn’t add them if we couldn’t get 150-200 wires per month within the first few months. In terms of the customers, that is an ultimate offshoot of putting up new retailers. Sometimes, when you put up new retailers in areas where you haven’t been, you’re going to see new customers because they haven’t been exposed to your brand. That growth in new customers is pretty solid. That, along with the same-store growth that we have, drives overall business growth.

In other words, this approach is underpinned by an astute recognition of the pivotal role that the selection of right agents plays in generating substantial remittance transactions. I believe the CEO’s vision highlights a strategy that prioritizes quality over quantity, fostering deeper engagement with agents while ensuring they are optimally positioned to yield significant volumes. With an exceptional CEO who is deeply committed to the company's long-term success, I am confident in his dedication to making decisions that align with Intermex's best interests. His ownership of approximately 1.073 million outstanding shares, acquired through both direct and indirect ownership, further underscores his personal investment in the company's growth and prosperity since this alignment of interests reinforces the notion that his decisions will consistently prioritize the company’s well-being.

{kind=link}

Company's 10-K's and 10-Q's

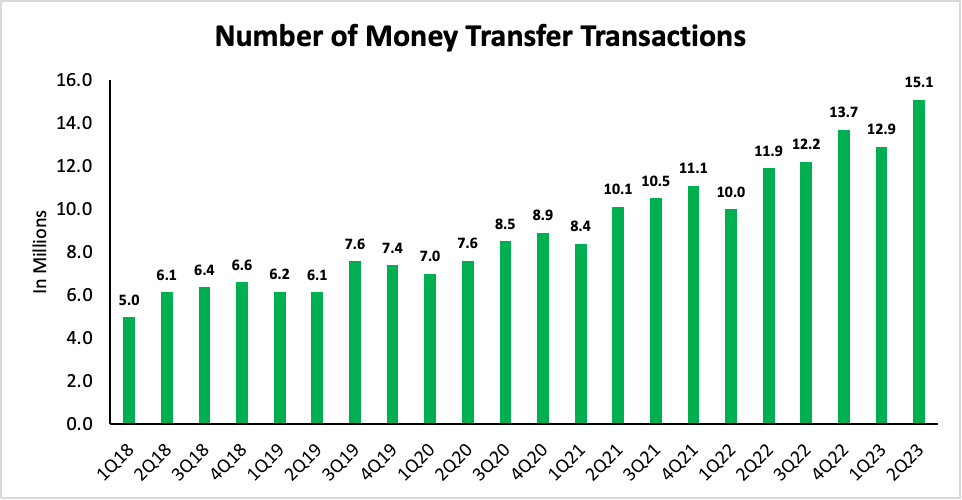

As illustrated in the chart above, the number of money transactions, commonly referred to as wires, has demonstrated a steady upward trend over the past five years. From my perspective, this growth can be attributed to Intermex's strategic approach of expanding its agent network through collaborations with exceptionally efficient partners, coupled with the successful adoption of digital solutions. This dual strategy has been instrumental in driving the company's expansion. A contributing factor to this growth has been the company's focus on forging partnerships in strategic locations, driving both customer acquisition and the growth of existing outlets as stated previously.

Furthermore, the latest earnings presentation from the company highlights that the digital channels now account for 31% of the company's total transactions, which indicates a conscious effort by management to integrate technology into its operations for the benefit of its customers. Additionally, the Intermex App's ratings, averaging around 4.6 on the Google Store and 4.8 on the Apple Store , underscore its user-friendly features. Therefore, I believe that Intermex's ongoing investments in enhancing its digital mobile money remittance applications are a testament to its commitment to providing secure and user-friendly experiences for its customers. This initiative not only aligns with the growing relevance of digital transactions for consumers in the Latin America and Caribbean corridor but also reflects broader industry trends toward online financial activities. As consumers increasingly turn to digital solutions , these strategic investments position the company well to cater to evolving customer preference.

{kind=link}

Q2 2023 Presentation

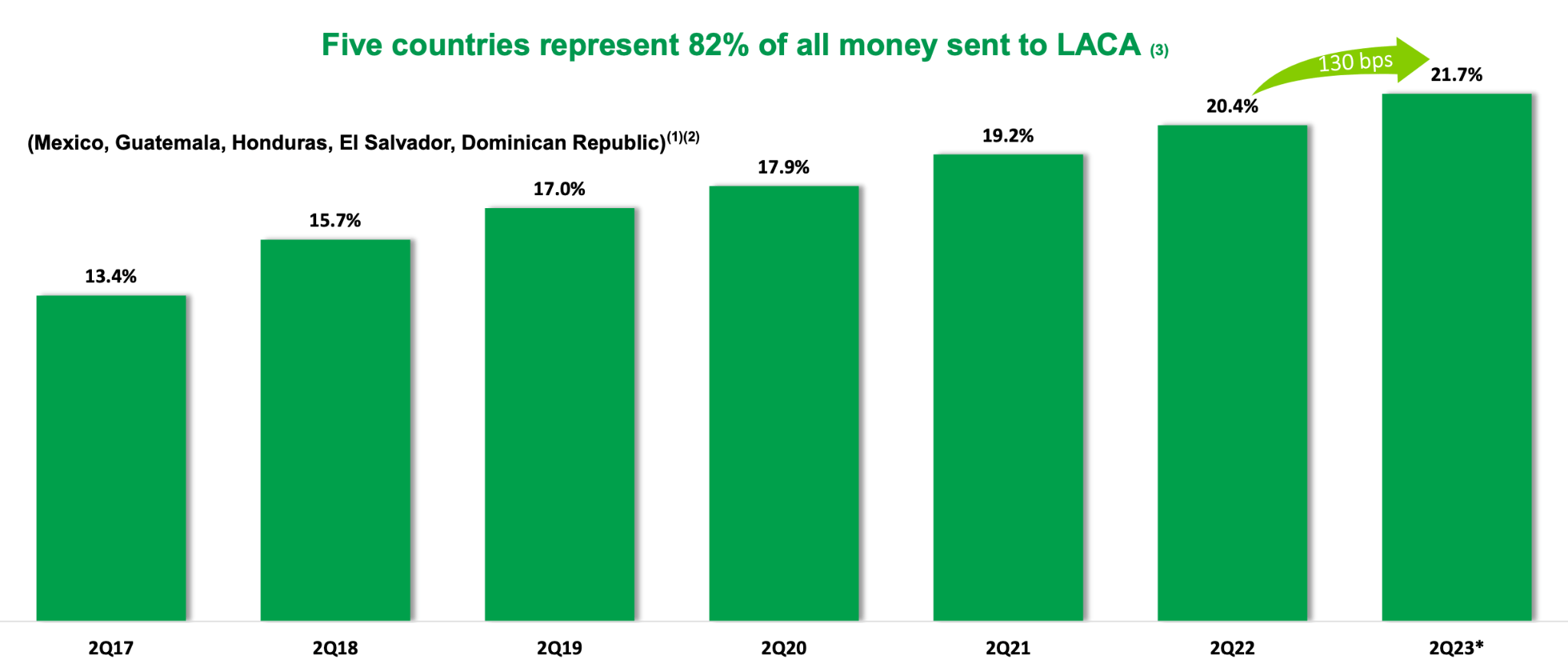

Intermex's consolidation of brand value within the remittance sector can be attributed to three fundamental factors: its unwavering reliability, robust commitment to customer service, and the secure facilitation of fund transfers. This cohesive approach has propelled the company to assertively expand its market presence across key nations like Mexico, Guatemala, Honduras, El Salvador, and the Dominican Republic over the past six years. The accompanying chart above provides a visual representation of this growth, depicting a surge from 13.4% in Q2 2017 to approximately 21.7% in Q2 2023 in terms of remittance volume within these specific markets.

In contrast to incumbent competitors like Western Union ( WU ) and MoneyGram, who primarily hinge their competitiveness on price-based strategies, Intermex distinguishes itself through a unique approach by placing more importance on enhancing the efficiency and effectiveness of their network of sending agents. This strategic focus enables these agents to process remittance transactions swiftly, reliably, and with cost-efficiency. A noteworthy facet of their strategy involves the development of a platform capable of accommodating transaction volumes well beyond the current load. This platform has demonstrated its reliability, as evidenced by a mere 0.05% downtime recorded in 2022.

{kind=link}

Capital IQ

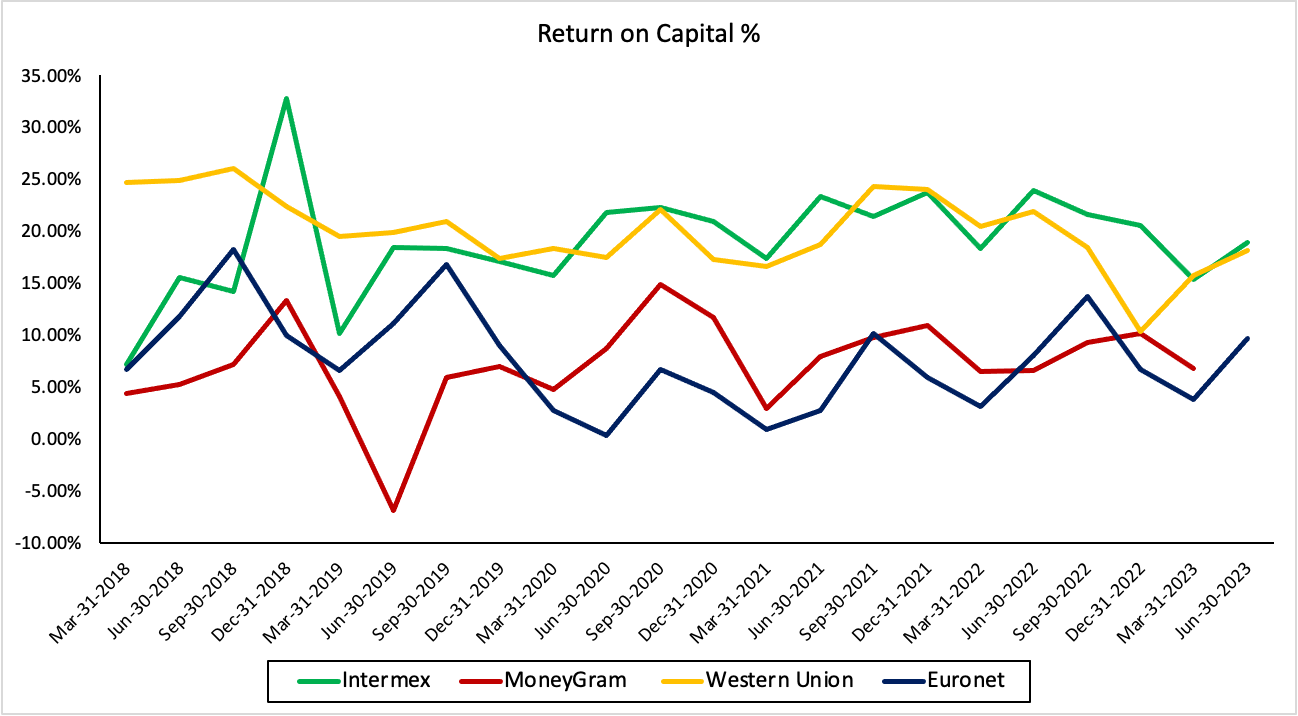

With that being said, we can gauge Intermex's return on capital since it serves as a robust indicator of a company's competitive advantage in relation to its rivals. A comparative analysis of Intermex's return on capital vis-à-vis its competitors reveals a substantial disparity since the company has demonstrated a remarkable capacity to effectively leverage capital, yielding returns of over 20% for its shareholders. In contrast, MoneyGram and Euronet ( EEFT ) often grapple with sustaining a return on capital hovering between 2.50% and 10%, except for Western Union which stands out. Despite its higher return on capital, the Western Union’s continuous revenue decline over the past decade and consistent loss of market share raise red flags. The absence of a discernible turnaround strategy further diminishes its appeal to potential investors.

{kind=link}

Company's 10-K's and 10-Q's

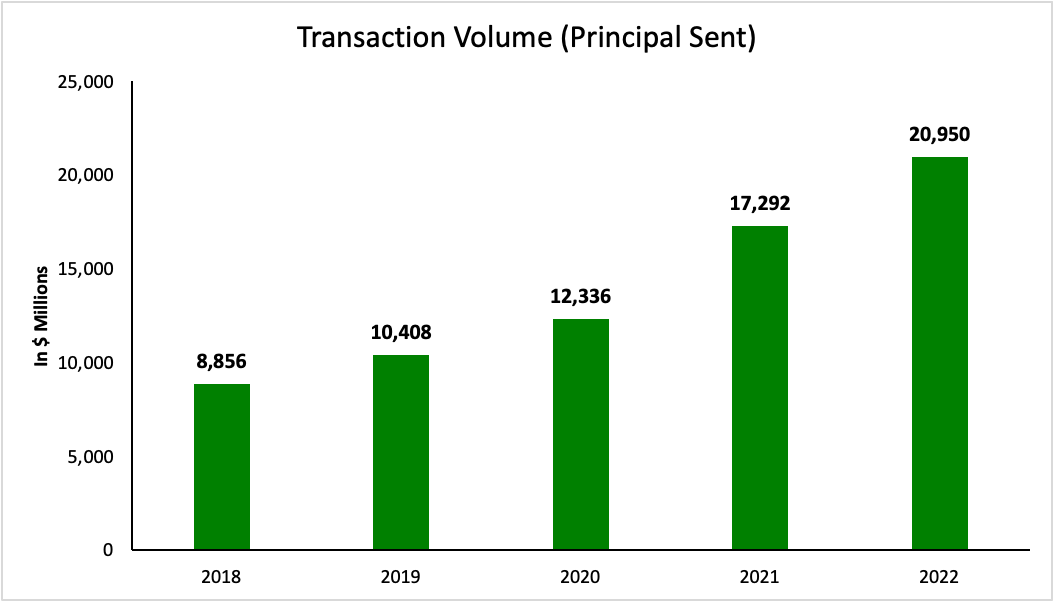

Analyzing data spanning from FY 2019 to FY 2022 , we can observe a notable surge in Intermex's transaction volume, increasing from $8.856 billion to $20.95 billion over the span of five years. From my perspective, this upward trajectory underscores both the resilience of the company's distinct offerings and its strategic acumen in customer acquisition because the responsibility of managing entrusted funds and facilitating secure transfers necessitates establishing a profound level of trust. Simultaneously, delivering top-tier customer services becomes paramount to cultivate enduring brand loyalty. Considering potential disruptions to Intermex's established position, it is worth noting that new entrants aiming to reshape Intermex's business practices face a substantial challenge because building intricate relationships with major banks and financial institutions requires considerable time and effort, particularly given the current regulatory landscape. Moreover, devising distinctive and compelling offerings poses a significant hurdle, especially given Intermex's entrenched market presence.

{kind=link}

Capital IQ

{kind=link}

Capital IQ

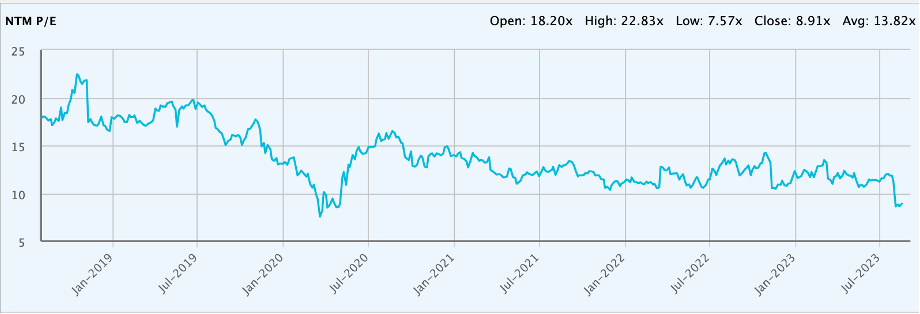

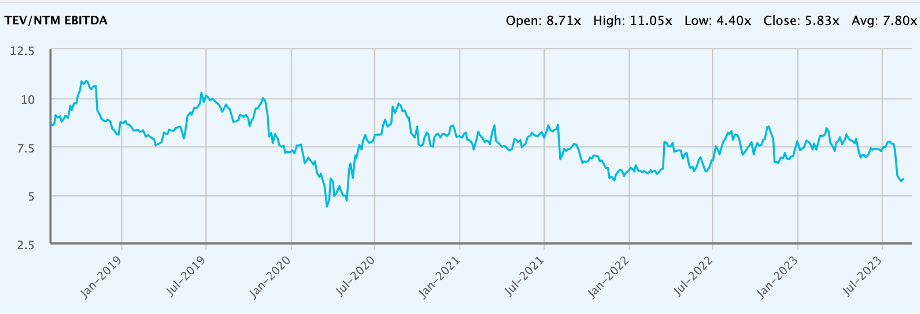

Lastly, the recent market response to the company's guidance adjustment seems to have been somewhat overreacted since it has pushed the stock's valuation to levels akin to those observed during the depths of the pandemic. As a result, an intriguing proposition emerges for investors, presenting an appealing chance to secure a valuable investment. While the trajectory of long-term revenue growth remains steadfast, the promise of multiple expansion holds considerable potential. This could facilitate a return to a more balanced valuation, characterized by a NTM P/E ratio of around 14x and an EV/EBITDA ratio of approximately 7.50x. More importantly, the management team has been very opportunistic in capitalizing on the lowered valuation, which is evident in their execution of a $30.515 million buyback in the first half of 2023, following the announcement o f a $100 million buyback program in the fourth quarter of 2022 . Given the recent decline in share price, there seems to be a promising opportunity for management to capitalize on this scenario since they still have $90.7 million available for future share repurchase according to the latest 10-Q .

Capital Structure

{kind=link}

10-Q for 2nd Quarter of 2023

Author's Contribution

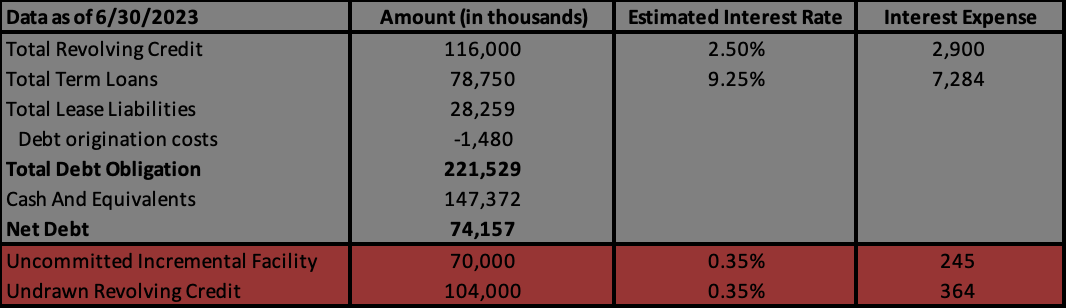

Examining the company's current capital structure reveals a healthy state, even amidst the Federal Reserve's hawkish stance on interest rate hikes. The EBITDA projections from my conservative base case scenario indicate that there is still room for the company to consider additional leverage or utilize more of its cash for the buyback program. Notably, the company holds a substantial cash balance that could provide a buffer during uncertain economic times. Additionally, the company still has access to a significant credit pool of $174.00 million, which aligns with its expansion plans. Given these factors, my concerns about the company's debt obligations are somewhat alleviated. Its track record of achieving profitable growth and prudent capital allocation gives me confidence in its ability to navigate its financial commitments.

Financial Valuation

Before delving into financial valuation, let me provide you with a concise overview of the primary driving factors shaping my model. The total transaction volume will be derived through the multiplication of the principal sent per transaction and the number of money transactions. Both wire transfer and money order fee revenue, along with FX gain revenue, will be depicted as a percentage of the total transaction volume. Additionally, other income, predominantly encompassing revenue generated from technology services offered to the independent agent network, is projected to scale in tandem with transaction volume.

{kind=link}

Author's Contribution

{kind=link}

Author's Contribution

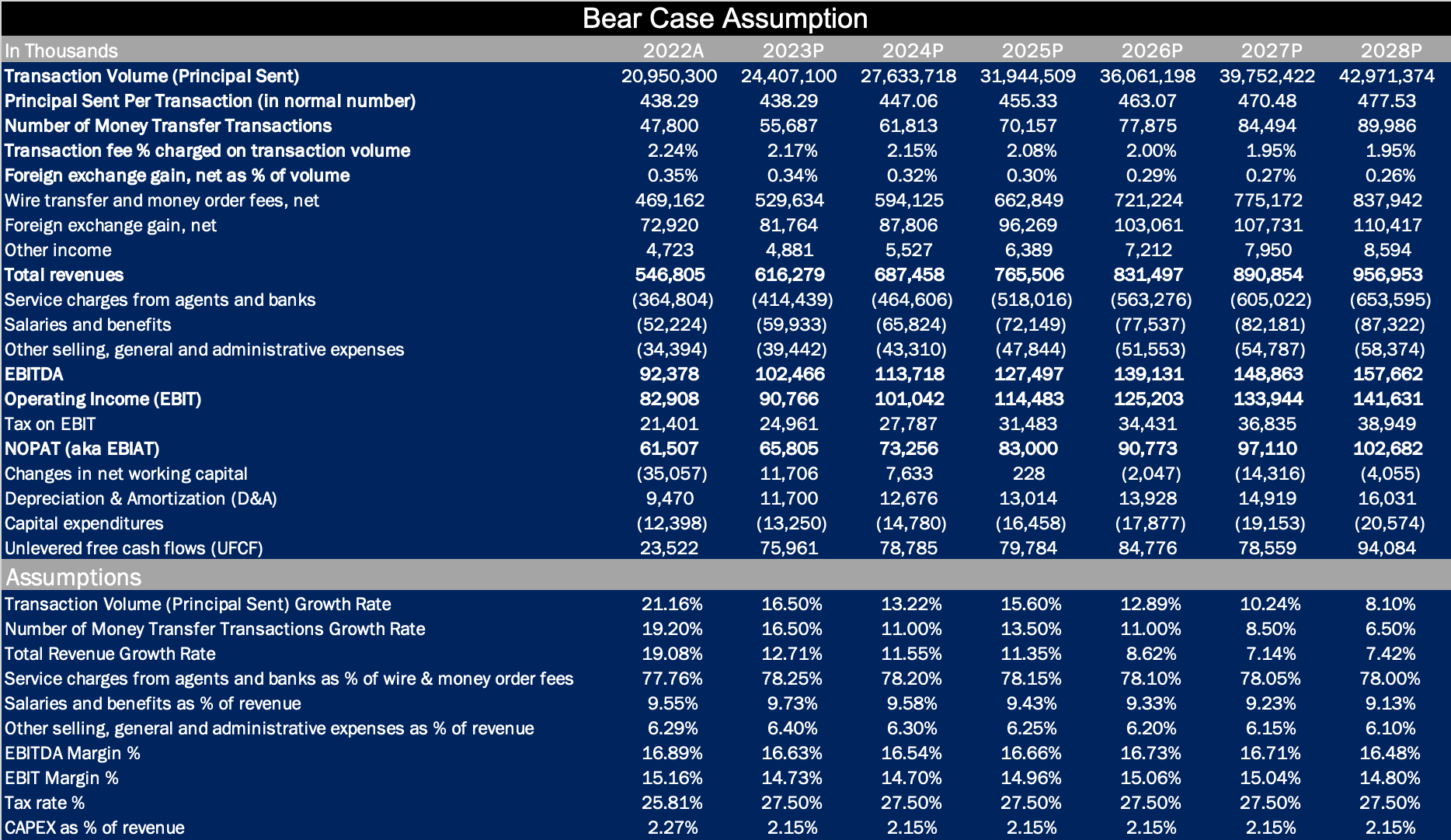

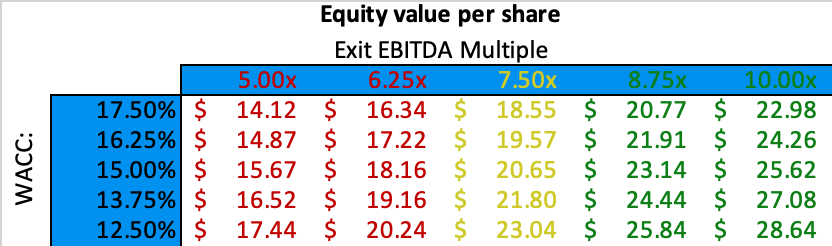

Drawing from my analysis of a bear case scenario, I have estimated IMXI's intrinsic value to fall within the range of $15.67 to $25.62, accounting for a discount rate of 15.00%. In this projection, the principal sent per transaction is projected to experience a relatively modest growth rate of 1.40%, which notably lags behind a more normalized U.S. inflation rate of 2-3% annually. The trajectory of money transactions is expected to slow due to increased industry-wide discounting efforts. This growth rate is anticipated to reach a low of 11.0% in 2024, partly influenced by a projected economic downturn, before gradually recovering to 13.50% in 2025 and subsequently tapering off.

Over time, both wire transfer and money order fee revenue, as well as FX gain revenue expressed as a percentage of total transaction volume, are anticipated to decrease. This shift aligns with the intensification of competition and the differentiation strategies employed through discounting, ultimately impacting industry-wide profitability. Consequently, the growth of total revenue is expected to be modest, residing within the low-teen to single-digit range over the next five years. The EBITDA margin is projected to slightly dip below the historical average, with no anticipated margin expansion due to the company's inefficiency in cost allocation.

In light of this analysis, I want to emphasize that the current stock price appears to carry minimal risk even in the context of my bear case scenario. Despite the overreacted decline in stock price following the earnings announcement, the stock has been trading within the range of $17 to $19. This positioning makes the current opportunity very attractive, even when considering the potential for a worst-case scenario.

{kind=link}

Author's Contribution

{kind=link}

Author's Contribution

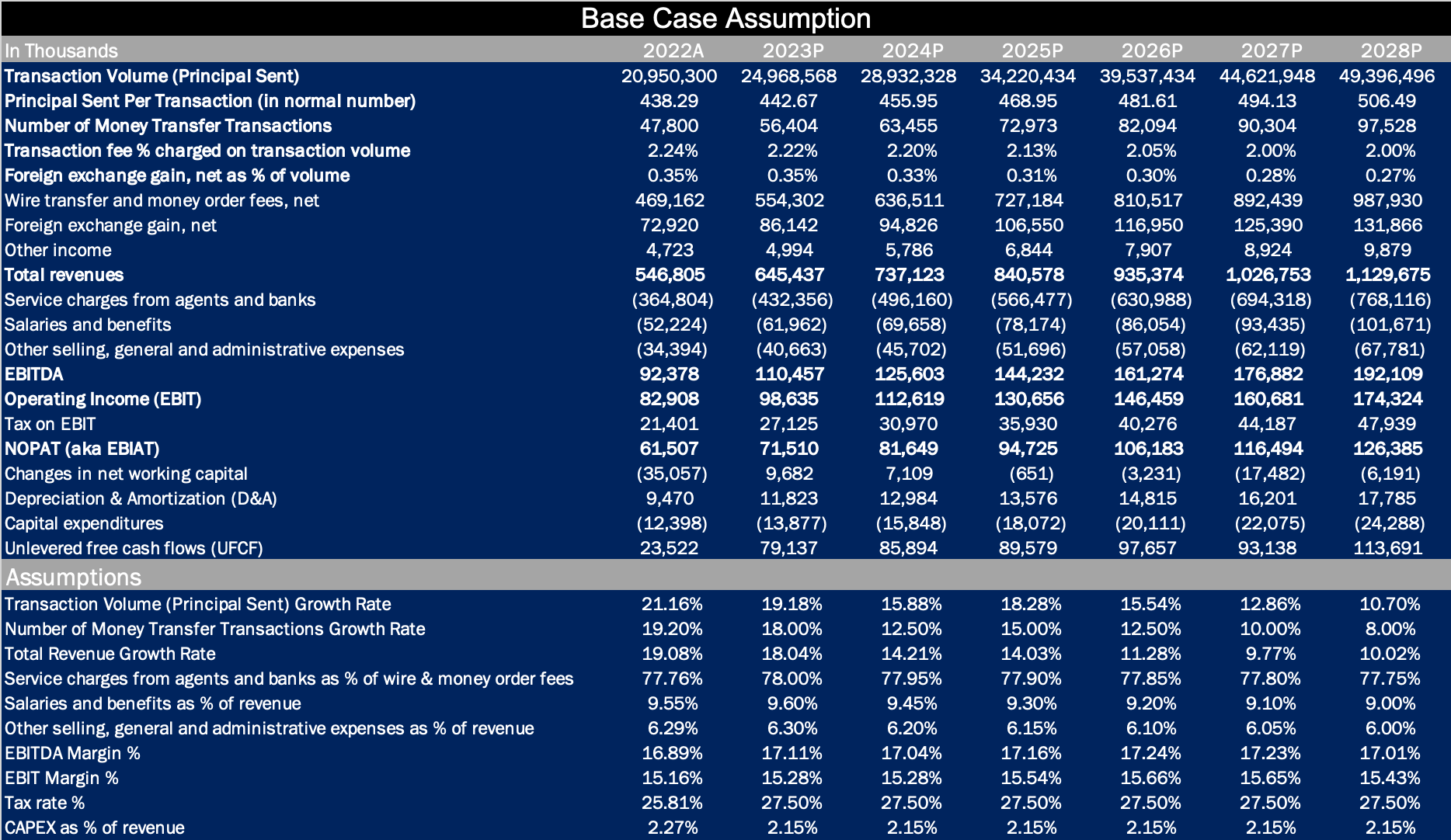

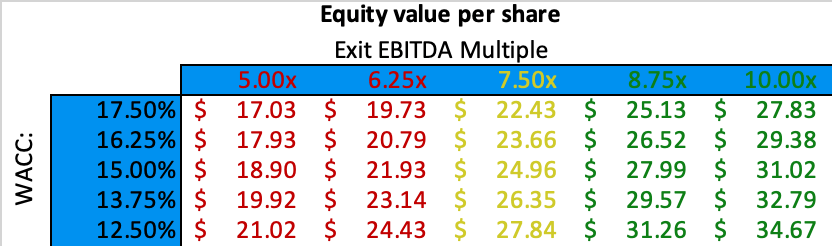

Moving on to my conservative base case analysis, I have projected the intrinsic value of IMXI to reside within a range of $18.90 to $31.02, considering a discount rate of 15.50%. The principal sent per transaction is forecasted to undergo a growth rate of 2.40%, harmonizing well with the more normalized U.S. inflation rate of 2-3% per year. A notable facet is the slightly more favorable growth projection for the number of money transactions, which shifts from mid-teen expansion to high single digits. This favorable outlook is driven by the company's ongoing expansion into Europe and the Eastside of the U.S., positioning it ahead of industry averages. The total revenue estimate for 2023 closely aligns with the company's bottom guidance for the year, which offers a cushion for any potential inaccuracies. In a parallel vein, both wire transfer and money order fee revenue, as well as FX gain revenue presented as a percentage of total transaction volume, are anticipated to contract for reasons previously outlined. A notable observation is the projected marginal expansion in both operating income and EBITDA margins. These figures are set to stabilize around 15.50% and 17.00%, respectively, as the company effectively streamlines its SG&A costs. Considering this scenario's potential outcomes, it is worth noting the compelling prospect that lies ahead. If these projections align, there is a high likelihood of witnessing a doubling or even tripling of returns over the next five years.

{kind=link}

Author's Contribution

{kind=link}

Author's Contribution

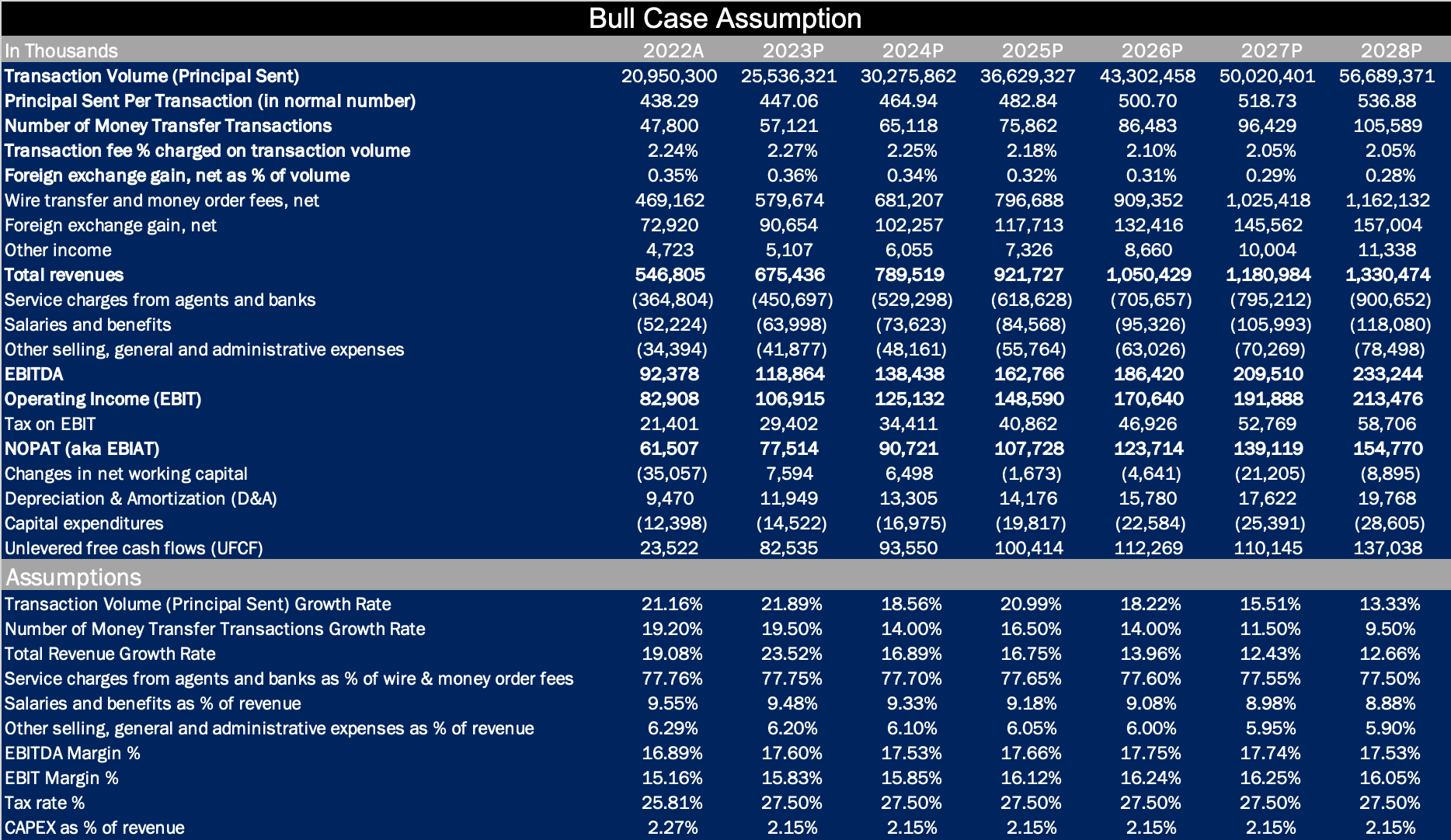

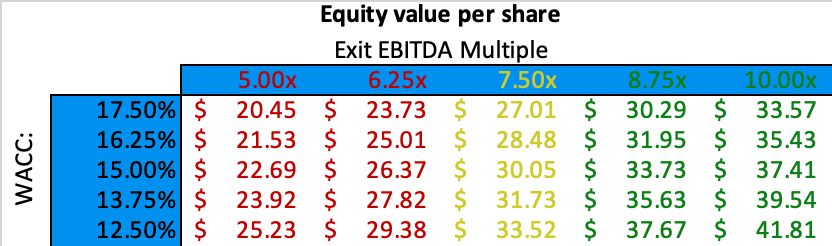

Finally, let's explore the bull case scenario, which paints a more optimistic picture for IMXI's price target range, projected between $22.69 and $37.41, with a discount rate of 15.00% factored in. In this scenario, the principal sent per transaction is predicted to grow at a rate of 3.40%, driven by a combination of steady U.S. economic growth and a healthy inflation level. The forecasted trajectory for the number of money transactions starts with a robust high teen growth and tapers off as the company matures. This is anticipated to result in an initial transaction volume increase of around 20%, followed by a gradual moderation starting around 2026. Furthermore, the revenue streams from wire transfer and money order fees, as well as FX gain revenue represented as a percentage of total transaction volume, are expected to maintain competitive positions and exhibit slower declines compared to other scenarios. This is projected to lead to a strong revenue growth trajectory, peaking around 20% before finding a more sustainable pace by 2026. Regarding the EBITDA margin, the projection remains attractive at approximately 17.50%, which aligns with a realistic assessment of the optimal margin the company can attain as it progresses and matures.

Risks

- Competitive Discounting: One primary risk arises from the ongoing efforts of competitors aiming to undercut FX gains and transaction fees. While I've accounted for this risk in my financial projections, there's an underlying uncertainty regarding the extent to which competitors might further reduce prices to enhance their appeal within the industry. This trend, beneficial for immigrants but less so for investors, poses a challenge for Intermex's positioning as a high-quality business with limited competition. This dynamic might deter investors seeking stability and less price-driven sectors.

- Cryptocurrency Impact: The pervasive adoption of blockchain technology and cryptocurrencies in money transfer processes is another potential risk. This transition could potentially lower the cost of money transfers for consumers. However, it's crucial to acknowledge that the widespread adoption of such technology might take time due to the inherent volatility of cryptocurrencies, which could compromise the safety of money transfers. This introduces a nuanced interplay of technological advancement, consumer safety, and cost efficiency.

- Immigration Trends Uncertainty: The unpredictability of U.S. immigration trends over the coming decade is a noteworthy challenge. These trends can fluctuate based on political dynamics, rendering long-term forecasts challenging. It's worth noting that a consistent workforce, particularly in labor-intensive sectors like construction and housing, remains pivotal to support the growing needs of a burgeoning population. However, forecasting the specifics becomes complex given the evolving political landscape.

Summary

In conclusion, I am assigning an overweight rating to IMXI's stock, accompanied by a target share price of $24.96. This valuation is predicated on a discount rate of 15.00% and an exit EV/EBITDA multiple of 7.5x, grounded in an exceedingly conservative base case assessment. In my view, Intermex's strategic emphasis on cultivating efficient agent partnerships and delivering exceptional customer service, coupled with its consistent growth trajectory, positions it as a formidable contender for the future. Despite confronting industry headwinds such as competitive discounting and the potential implications of cryptocurrency adoption, Intermex's distinct approach and well-established market presence set it apart from rivals. The valuation span that encompasses various scenarios, including an exceptionally prudent base case projecting considerable upside potential, underscores the remarkable undervaluation opportunity presented by IMXI. The company's judicious capital structure, resilient financial performance, and proactive managerial decisions further bolster its investment allure. In totality, I believe Intermex stands out as a standout performer within the remittance arena, poised to deliver favorable returns to perceptive investors.

For further details see:

Redefining Remittance: The Untold Investment Story Of International Money Express