RDCPF - RediShred Capital: Turning Shredded Paper Into Free Cash Flow Initiate With A Buy Rating

2023-12-15 13:37:25 ET

Summary

- RediShred Capital offers investors a compelling opportunity to invest in the on-site document shredding and data protection industries.

- Trading at a steep discount to other companies in the waste management space, RediShred should continue to appreciate as the Company continues to grow and the valuation gap narrows.

- We initiate with a BUY rating and a CAD$5.70 price target, which equals a USD$4.20 price target.

Investment Thesis

RediShred Capital ( RDCPF ), together with its subsidiaries, operates the PROSHRED franchise and license business in the United States. The Company has 16 owned and 14 franchise locations throughout the U.S. RediShred is one of the only publicly traded opportunities to invest in the secure information destruction (shredding) and data protection services sectors in North America. The only other publicly traded company in the U.S. with a paper shredding business is Stericycle ( SRCL ), and paper shredding and recycling only represent approximately one-third of this multinational waste services business. Given a lack of direct publicly traded competitors in the exact same business, we look at Redishred relative to both SRCL and publicly traded solid waste management companies, and RediShred is incredibly undervalued. We believe that the Company’s strategy of growing and improving the efficiency of owned locations, coupled with the strategy of acquiring franchise locations and improving their efficiency, will enable RediShred to build a very strong, steady, cash-flowing business over the next several years.

We initiate coverage with a BUY rating and a USD$4.20 price target.

Business Overview

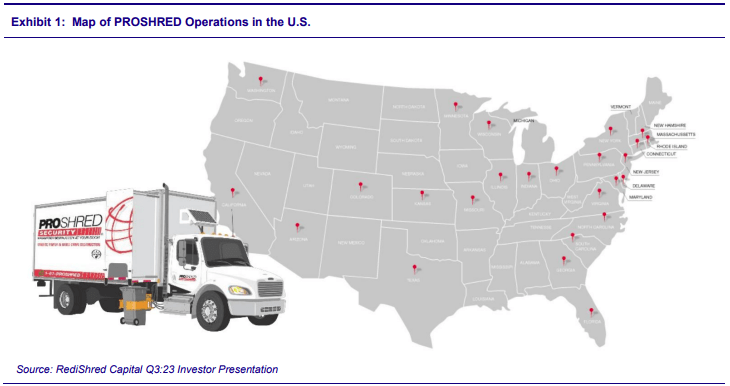

RediShred operates in three distinct but interrelated business services - mobile shredding, information management, and e-waste recycling. The mobile shredding business is the largest and most significant operation of the Company by far. With 30 locations and a fleet of over 200 trucks, PROSHRED is one of the largest mobile shredding operations in North America, providing service to 42 metropolitan markets in 25 states. These trucks come right to the customer's door to provide information destruction services, including paper shredding, hard-drive destruction, and product destruction services. The Company has a nationwide footprint in the U.S., but there is a concentration of assets in the eastern half of the country, with far fewer operations in the western half of the U.S. Exhibit one below shows the Company’s footprint of owned and franchised locations.

{kind=link}

The second line of business is information management, which consists of digital imaging, document scanning, document management, and workflow automation. This portion of the business accounts for a relatively small percentage of the Company’s overall revenue and should offer an avenue for growth, particularly as more records are digitized. Like the shredding business, this line of business is relatively fragmented, with competitors in several different industries.

The final line of business, e-waste recycling, is also relatively small as a percentage of overall revenue for RediShred and could also present a compelling growth opportunity. Within this line of business, the Company offers disposal of unwanted electronic devices, such as TVs, computers, smartphones, tablets, electronic toys, and more. With more and more electronic devices collecting dust in people's homes, this opportunity could be an interesting untapped growth market for the Company if they can have the right resources in place to grow the business.

To help investors better understand the composition of RediShred’s total revenues, the table in Exhibit Two below, from management’s Q3:23 MD&A filing, provides additional insight.

{kind=link}

As the table illustrates, shredding is by far and away the most significant portion of the Company’s revenues, and it grew by almost 7% YoY. Recycling was a material drag on revenue, down 40% YoY, due to much lower recycled paper prices, which is discussed in more detail below. Scanning makes up just under 3% of revenue but did grow by 15% YoY, making it the fastest-growing segment of the Company’s business. Electronic recycling rounds out the revenue mix at 1.5% of total revenues in Q3:23.

Acquisition-Driven Growth Strategy

RediShred now has 16 corporate-owned locations in the U.S. and has been steadily growing through acquisitions. The most common type of acquisition that the Company has executed is acquiring franchisees. Since the Company is already familiar with the operations of franchisees and is easily able to leverage existing infrastructure to gain efficiencies and economies of scale, this area is a natural path to profitable growth. The Company has also acquired and will continue to acquire independent operators so long as the valuation makes sense, and the acquisition will be accretive. Synergies can be realized from routing, back-office integration, and marketing. Since 2018, RediShred has completed CAD$85 million in acquisitions and grown EBITDA at a 10-year EBITDA compound annual growth rate ((CAGR)) of 70%.

Volatile Paper Recycling Prices Pose Risk

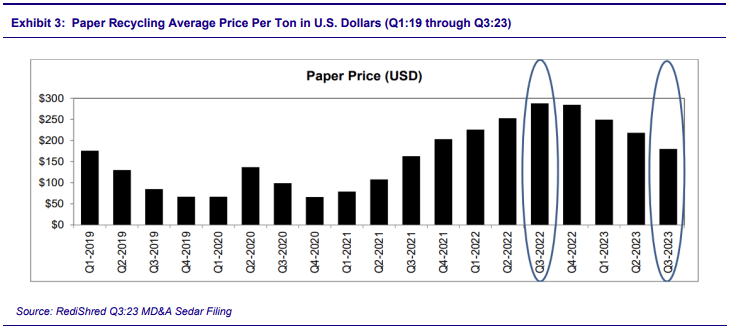

One of the largest risks that the Company faces, aside from the risk of competition, is the volatility of paper recycling prices. Fluctuations in spot prices for paper recycling can have a material effect on RediShred’s operating results. During Q3:23, the Company’s recycling revenues came in at $2.5 million, down 40% YoY versus $4.2 million in Q3:22, due primarily to declines in spot paper recycling prices. When we asked management if there was a way to potentially hedge this risk, they indicated that they have not found a viable alternative for doing so. As such, operating results from quarter to quarter can be positively or negatively impacted by these fluctuations. Exhibit three illustrates the average spot paper recycling price per ton in USD since the first quarter of 2019.

{kind=link}

As the chart illustrates, paper recycling prices were at the near-term highest rates they have experienced in Q3:22, close to $300 per ton, but declined to an average rate of $161 per ton in Q3:23. We expect paper recycling prices to continue to be a headwind for RediShred in Q4:23, as the trend line appears to point to a continuing decline. It is difficult to predict where they may bottom out, but the chart illustrates that they have been close to as low as $50 U.S. dollars per ton as recently as Q3:20. At $2.5 million in Q3:23, recycled paper revenue accounted for 16.4% of total revenue, which is down from 28.6% of revenue in Q3:22. The good news is that as the Company continues to grow scheduled services as a larger percentage of revenue, this amount will become less significant over time. But in the near term, it does bear careful monitoring, as it still can have a meaningful impact on financial results.

Competition

RediShred faces substantial competition from direct competitors as well as alternative methods of handling document destruction and data protection. The Company’s single largest competitor in the shredding business is ShredIt, a wholly-owned subsidiary of Stericycle, Inc. SRCL is a $4.5 billion market capitalization conglomerate in the waste management space, that has a range of businesses, including hazardous medical waste management, in addition to the shredding business. RediShred also faces competition from independent service providers, which the Company estimates could total over 750 in the U.S. While RediShred does not have the financial and operational resources of SRCL’s ShredIt business, the Company has stronger resources than many independent businesses, giving the Company a nice opportunity to grow its share of the market.

Financial Results and Forecast

FY:22 operating results were very impressive, with revenue growth of 58% and EBITDA growth of 59% versus FY:21. These results were driven by previous period acquisitions and assisted by recent record high paper recycling prices. FY:23 started well, with Q1:23 revenues of $17.0 million, which were up 36% YoY. However, Q2:23 and Q3:23 have seen revenue decline sequentially in each consecutive quarter and only rise 15% and 5% YoY, respectively. This result has been driven by the aforementioned highly volatile price per ton for recycled paper, which has been declining in FY:23. EBITDA, while still nicely positive, has also been down sequentially and YoY in both Q2:23 and Q3:23.

Management does not provide formal financial guidance, but they do publish strategic targets in the MD&A section of their SEDAR filings and provide status updates throughout the year. For FY:23, the Company’s strategic targets include growth of same location system sales to $57 million U.S. dollars, growth in same location EBITDA to $22 million U.S. dollars, EBITDA margin of at least 35%, operating income margin of 20% before transition and acquisition costs, acquiring $5 to $6 million in revenue through accretive acquisitions, and keeping G&A costs at 12% of total revenue. The Company is generally on target on two of these goals but behind target on the EBITDA and G&A goals and slightly behind target on the EBITDA margin goal.

For FY:23, we are projecting revenue of CAD$63.3 million, adjusted EBITDA of CAD$15.9 million, and EPS of $0.03 per fully diluted share. For FY:24, we are projecting revenue of CAD$65.1 million, EBITDA of CAD$15.8 million, and EPS of $0.04 per fully diluted share.

Investment Risks

- RediShred is subject to risks related to fluctuations in the price of recycled paper, which can be quite volatile and can have a material impact on operating results.

- Secular risks related to digitization of records and reduced paper usage could have a material adverse impact on operating results if this trend gains significant momentum. For the time being, this risk does not appear to be a significant risk, but it bears watching.

- The Company does use leverage to help fund operations and acquisitions, and as such, the firm is subject to interest rate risk, particularly in a rising rate environment.

- The Company faces credit risks from its customers and franchisees. If either experiences financial hardship, they may not be able to pay their obligations to the Company, which could negatively affect cash flow and liquidity.

- Financing risk could become an issue if the Company were to seek out a larger acquisition that would require more funding than is currently available through credit agreements and cash on hand.

Valuation

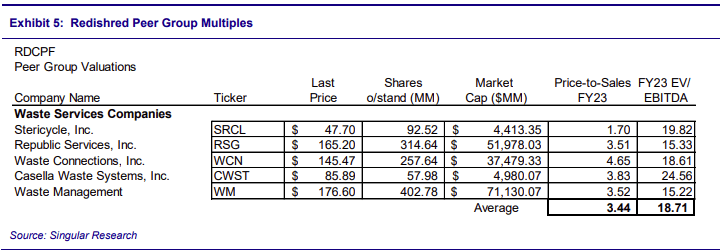

We value RediShred using a blend of peer multiples and a Discounted Cash Flow model ((DCF)). While there are really no publicly traded competitors that do exactly what RediShred does, SRCL, which owns ShredIt, is a major competitor. More broadly, we believe that RediShred is best compared against SRCL and other waste management companies because, effectively, RediShred is also in the business of managing waste. There are several publicly traded solid waste management companies that we believe can also be used as comparables to help provide a valuation framework for RediShred. Exhibit five below shows that the publicly traded peer group trades at an average FY:23 EV/EBITDA multiple of approximately 18.7 times. The peer group includes Stericycle, Republic Services ( RSG ), Waste Connections ( WCN ), Casella Waste Systems ( CWST ), and Waste Management ( WM ).

{kind=link}

RediShred currently trades at approximately 5.0 times projected FY:23 EV/EBITDA. While we fully expect the stock to continue to trade at a discount to the much larger, more diversified peer group, we would expect the Company to be able to close this almost 75% valuation gap over time through solid operational execution and free cash flow generation. Therefore, we value RediShred at 10.0x FY23 EBITDA to arrive at a peer group valuation price target of CAD$7.09.

In our DCF model, we estimate the firm would earn a return on capital of 15%, reinvesting 40% of this return into their business and growing EBITDA by 2% over the next seven years and at a steady rate of 2% through the terminal period. We use an 11% cost of debt, a levered Beta of 1.26, and arrive at a WACC of 12.79%, which we use to discount the Company’s cash flows. These assumptions lead to a DCF price target of CAD$4.32.

We then equally blend the relative valuation price target, CAD$7.09, and the DCF valuation price target, CAD$4.32, to come to a final rounded target price of CAD$5.70, compared to a recent trading price around CAD$3.00. The CAD$ price target equates to ~USD$4.20, at the prevailing exchange rate.

For further details see:

RediShred Capital: Turning Shredded Paper Into Free Cash Flow, Initiate With A Buy Rating