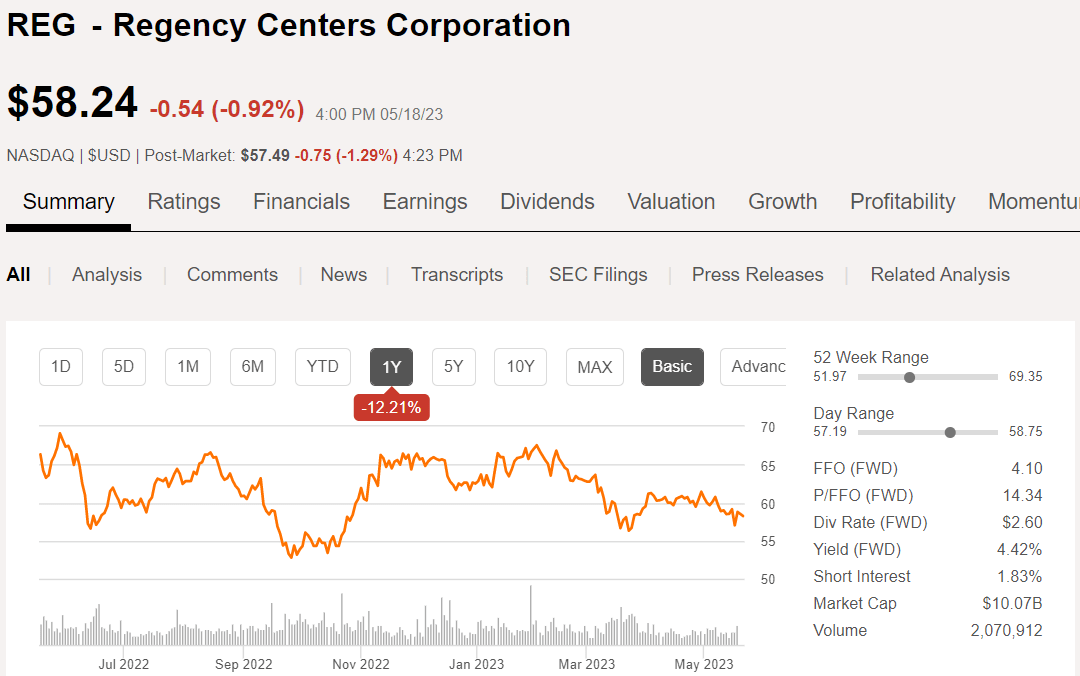

REG - Regency Center Acquiring Urstadt Biddle Is The Tip Of The Iceberg In Retail REIT M&A

2023-05-19 14:50:48 ET

Summary

- The merger looks good to me.

- REG is closer to fair value than the deeply discounted UBA which makes a stock for stock deal immediately accretive.

- I see more M&A ahead.

On 5/18/23 it was announced that Regency Centers ( REG ) agreed to acquire Urstadt Biddle ( UBA ) in an all stock deal. It is expected to close in 3Q or 4Q of this year. This is huge news as transaction activity in real estate has been low as of late.

In this article we will examine:

- Merits of the merger

- Ongoing arbitrage within REG/UBA/UBP

- The outlook for REIT M&A

- Retail REITs positioned to be the next buyout targets

Merits of the Merger

Let me preface this section by saying that I am usually not a fan of M&A. Quite often it is growth for the sake of growth and not necessarily accretive to shareholders.

This merger is the exception. It appears to be beneficial to shareholders of both companies. UBA shareholders get the immediate roughly 20% upside on which they can choose to defer taxation if they want to simply hang on to their shares. The upside for Regency shareholders is less immediately apparent as the stock is trading down by about a percent.

{kind=link}

However, my analysis suggests it is beneficial to REG shareholders in three ways:

- Property quality/location improvement

- Accretive to AFFO/share due to cap rate spread

- Accretive to AFFO/share due to synergies

As we have previously discussed , UBA’s portfolio is among the best with exceptionally high household income in its catchment radii and a strong grocery anchored tenancy. In recent years UBA’s portfolio has gained extra benefit from its suburban locations as these areas have benefitted from work from home.

In my opinion, UBA’s portfolio is better located and slightly higher quality than that of REG making the deal accretive to property quality.

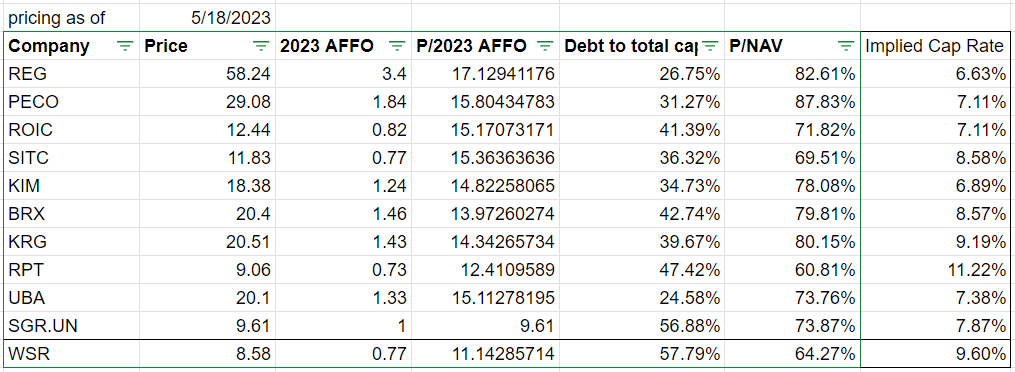

The buyout price indicates an acquisition cap rate in the low 7s. I calculate it at 7.38% using most recent quarter NOI. Regency centers is trading at a 6.63% implied cap rate. As it is a stock for stock deal, the spread in cap rates indicates that it will be immediately accretive to REG’s AFFO/share.

On top of that, there will be significant synergies, mostly in the form of cost savings. Regency already has extensive exposure to the areas surrounding NYC giving it significant overlap with UBA’s portfolio.

{kind=link}

As such, a substantial portion of UBA’s opex and overhead can be eliminated through consolidating it with Regency’s in-place teams.

Beyond cost savings, REG believes it can swiftly increase the occupancy on UBA’s portfolio by a few hundred basis points through existing tenant relationships in REG’s portfolio that would be a good fit in UBA’s properties.

I think the merger makes complete sense. The absorption looks quite straight forward which minimized integration costs and it really is accretive to all parties.

Ongoing arbitrage

REG, UBA and UBP still trade separately while they wait for the deal to close in Q3 or Q4 of this year. Even though it appears highly likely that the deal will complete, there is always some risk of it falling through and this risk can cause shares to trade disparately from the agreed upon buyout price. As of the time of writing, UBA was trading fairly close to the buyout price with a mere 0.54% upside.

I don’t consider this enough to make it an arbitrage worth playing, but UBP is trading significantly wider at $19.70 per share compared to a buyout price of $20.21.

{kind=link}

This provides 2.5% upside in UBP as compared to buying REG and UBA even though they will all likely become the same security.

It is still not huge, but perhaps worth clipping a bit of extra return on top of the forward returns of the combined company.

Stock for stock brilliancy

In this environment in which REITs are trading far below NAV and debt is expensive, it can be very difficult to transact. Buying anything at fair value will tend to result in a loss because the cost of capital is above fair value.

Stock for stock buyouts seem to be a loophole. In this case, despite being undervalued at 82% of Net Asset Value, Regency was still able to buy accretively because it bought UBA at 74% of NAV after the merger premium.

Thus, stock for stock transactions allow REITs to still engage in M&A so long as the REIT they are buying is even more discounted than they are.

With this stock-for-stock style of merger we see more mergers coming to the retail REIT space due to the extremity of discount at which some are trading.

The next buyout target(s)

In identifying buyout targets I find it useful to first identify the buyers.

In previous years the buyers were mostly private equity with Blackstone ( BX ) vacuuming up everything under the sun. However, Blackstone’s spigot has been at least partially turned off as it is fending off a wave of redemption requests at BREIT due to its self-proclaimed NAV being so remarkably far above fair market value. I suspect Blackstone will still buy some things, but with a diminished voracity.

Instead, I think the most likely buyers will be other REITs.

It will be the slightly undervalued REITs buying the dramatically undervalued REIT. Specifically, I think the most likely buyers will be Kimco ( KIM ), Regency Centers, and Retail Opportunity ( ROIC ). These companies are big and trade at implied cap rates of 6.89%, 6.63% and 7.11%, respectively.

{kind=link}

The implied cap rate at which these companies trade is functionally their cost of capital when making a stock for stock acquisition. So long as they are buying other REITs with higher implied cap rates it is fairly straight forward to make the transactions immediately accretive to AFFO/share.

Thus, the most likely targets are the shopping center REITs trading at the highest implied cap rates.

- RPT Realty ( RPT ) - 11.22% implied cap rate

- Whitestone REIT ( WSR ) - 9.6% implied cap rate

- Kite Realty ( KRG ) – 9.19% implied cap rate

- Brixmor ( BRX ) – 8.57% implied cap rate

- SITE Centers ( SITC ) – 8.58% implied cap rate

Of course there are other factors beyond just valuation. The acquiring company would also want the purchase to enhance its asset portfolio in some way so the most likely targets will be those which have particularly desirable properties or locations.

With that in mind, here are two that I think make quite a bit a sense.

Kimco buying Whitestone

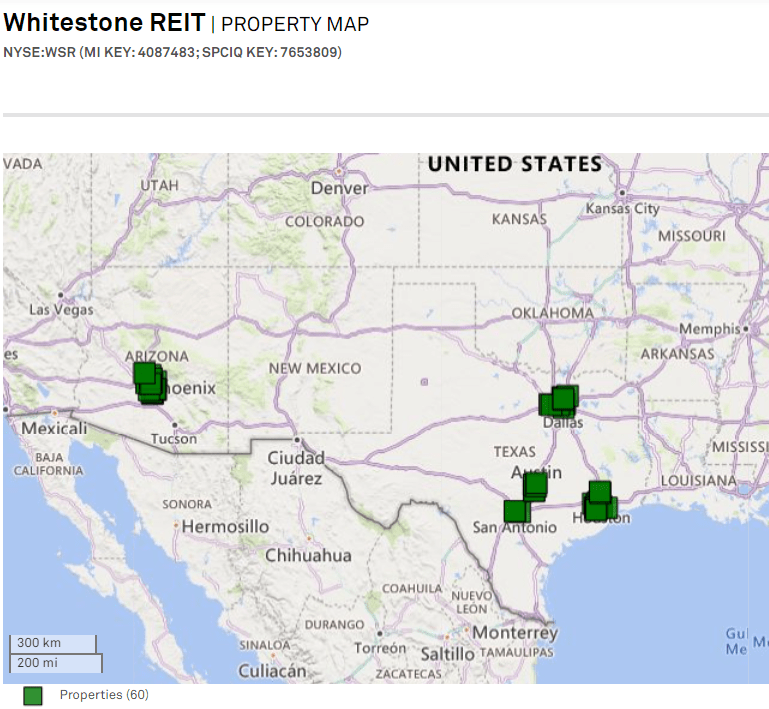

Whitestone has phenomenal properties which much like UBA have wealthy catchment radii. With better property level metrics than KIM it would be beneficial to KIM’s overall portfolio metrics. WSR’s main difficulty as a company is its small size which would be immediately remedied by a huge REIT like KIM buying it. Further, KIM would enjoy substantial opex synergies due to the overlap of their portfolios.

Whitestone is heavily in Phoenix, Dallas, Houston, San Antonio and Austin.

{kind=link}

Kimco already has large exposure and full operations in each submarket.

{kind=link}

The main question I have here is whether WSR would be willing to sell.

Kimco Buying Brixmor

BRX also has quite a bit of property location overlap with KIM which lends itself to similar opex synergies.

{kind=link}

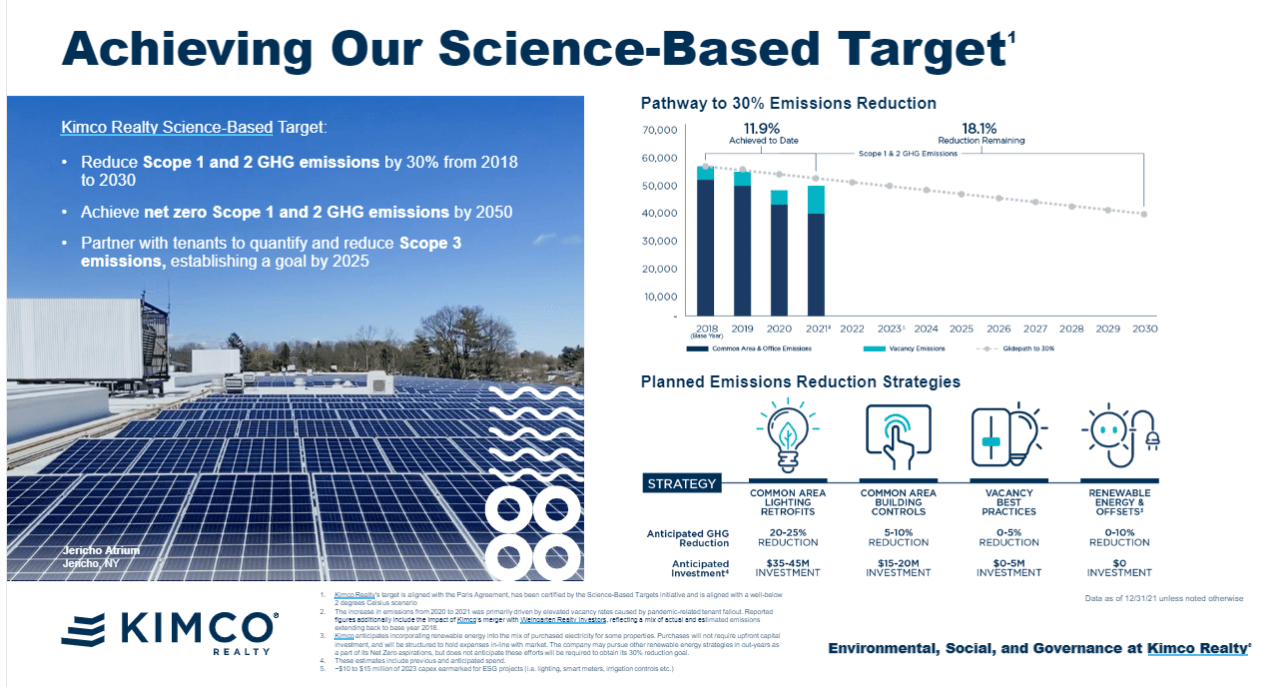

BRX has an additional angle in that it can help KIM achieve its stated ESG goals. In a recent presentation KIM spent about 15 pages declaring its goals related to energy savings and greenhouse gas reductions. The thrust of KIM’s goals is in the slide below.

{kind=link}

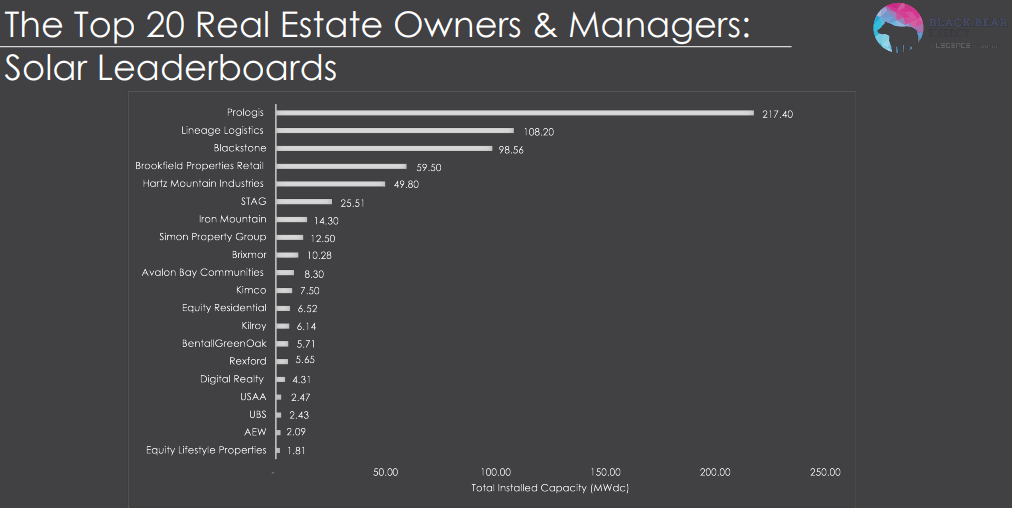

I don’t think much of the market is aware of this, but pound for pound Brixmor is the leader among retail REITs in solar. BRX comes in at #9 for total solar generation among real estate companies. It is #3 among retail.

{kind=link}

The above chart, however, is not relative to size. So while Simon Property Group ( SPG ) has more solar in absolute MWdc, SPG is a behemoth. Brixmor has nearly as much despite being a midcap. At half Kimco’s size, BRX has significantly more solar than KIM. Thus, KIM buying BRX would represent significant progress toward KIM’s rather difficult to achieve ESG goals.

That, of course, would be on top of the accretion that comes from a 6.89% implied cap rate company buying an 8.57% implied cap rate company with significant additional opex synergies.

It would be sad to see Brixmor’s James Taylor go as I believe he is among the best CEO’s in the space, but I would still welcome the merger premium

Wrapping it up

Stock for stock mergers allow higher valuation REITs to gobble up lower valuation REITs in a way that can be good for shareholders of both parties. Given how choked off capital markets are I think stock-for-stock will be an increasingly utilized tool.

It is made possible by disparities in valuation and right now the disparities are particularly wide so I anticipate an acceleration of stock-for-stock merger activity. One could still participate in the UBA buyout with the slight arbitrage favoring UBP shares, but my preferred method is to own the undervalued REITs that are most likely to be the targets of the upcoming M&A.

For further details see:

Regency Center Acquiring Urstadt Biddle Is The Tip Of The Iceberg In Retail REIT M&A