REG - Regency Centers: Quality You Can Count On With A Decent Yield

2024-01-01 08:30:00 ET

Summary

- Regency Centers is a high-quality shopping center REIT with a focus on grocery-anchored properties, making it less susceptible to recessions and e-commerce.

- The company has a strong portfolio of properties in high-density areas with above-average household income, allowing for higher rents and serving as a barrier to entry for competitors.

- Regency Centers continues to demonstrate solid operating fundamentals, and recently raised its dividend.

Quality is in the eye of the beholder, and while the market may be content with chasing high-priced names in the tech sector, I'd much rather own high-quality companies that have tangible assets which aren't going to be disrupted anytime soon.

Such I find the case to be with Regency Centers ( REG ), which I covered here back in September with a 'Buy' rating, noting its strong portfolio stats and high leased rates. The stock has done well for itself as concerns around a higher-for-longer interest rate environment have largely eased, giving investors a 5.4% total return since my last piece, nearly matching the 6.9% rise in the S&P 500 ( SPY ) over the same timeframe.

In this article, I provide an update and discuss why REG should remain on income investors' radar for profitable growth and income at the present valuation, so let's get started!

Why REG?

Regency Centers is one of the largest shopping center REITs in the U.S., especially after its acquisition of the long-time Northeast-based REIT, Urstadt Biddle Properties, in August of this year. REG was founded in 1963, which was just one year after its peer Federal Realty Investment Trust ( FRT ) was founded, and is a member of the S&P 500 Index.

What sets REG apart from its better-known peer, FRT, is its higher focus on grocery-anchored properties, which comprise 80% of its 480+ properties across the U.S. This means that REG's centers are more necessity, service, or convenience based, making it less susceptible to recessions and e-commerce.

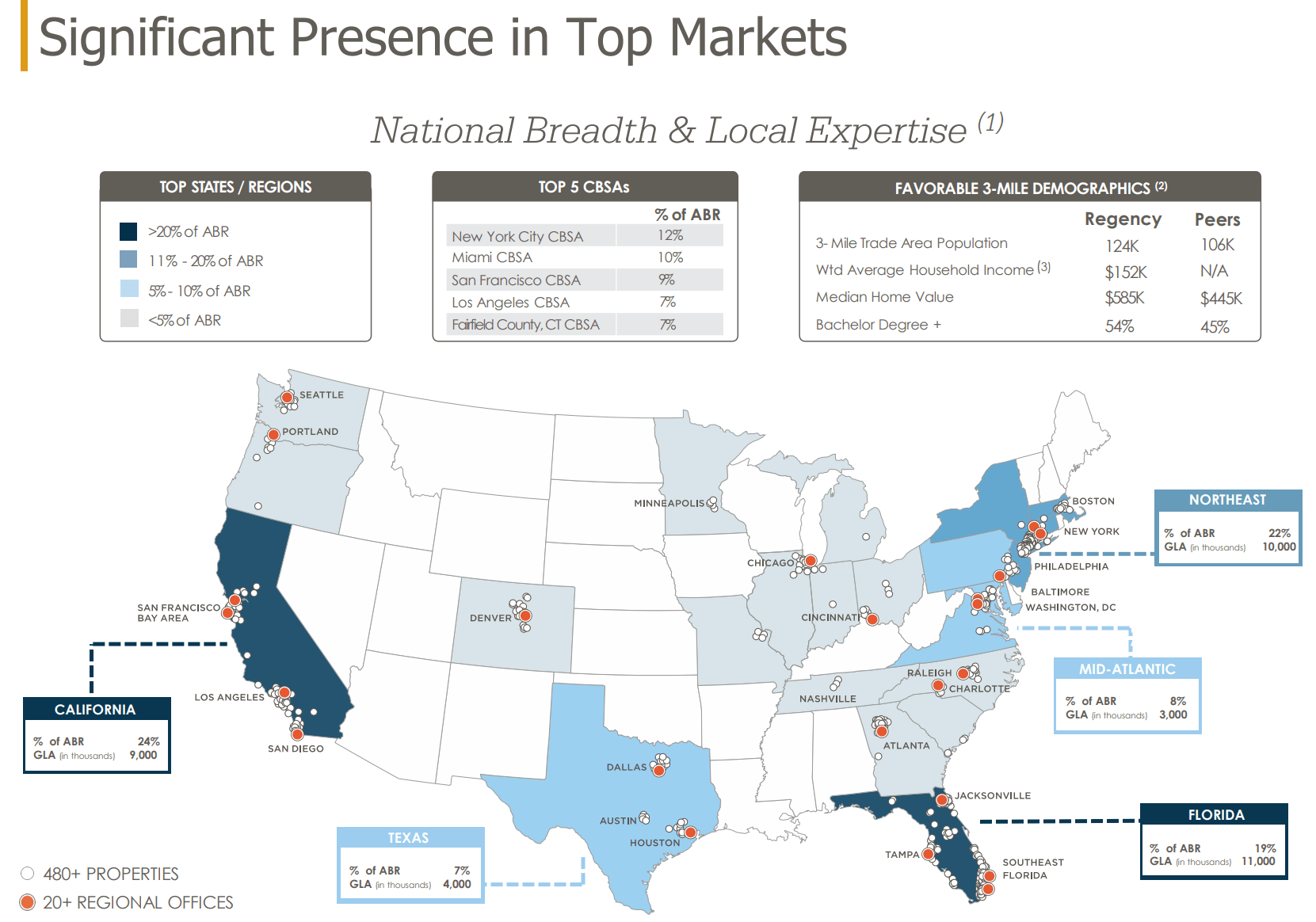

REG maintains close relationships and management of these 480+ properties through 20+ offices nationwide. As shown below, REG's geographic exposure is tied primarily to either major metropolitan areas or growing secondary markets such as those, including Nashville, Raleigh, Charlotte, and Austin across the Sunbelt.

{kind=link}

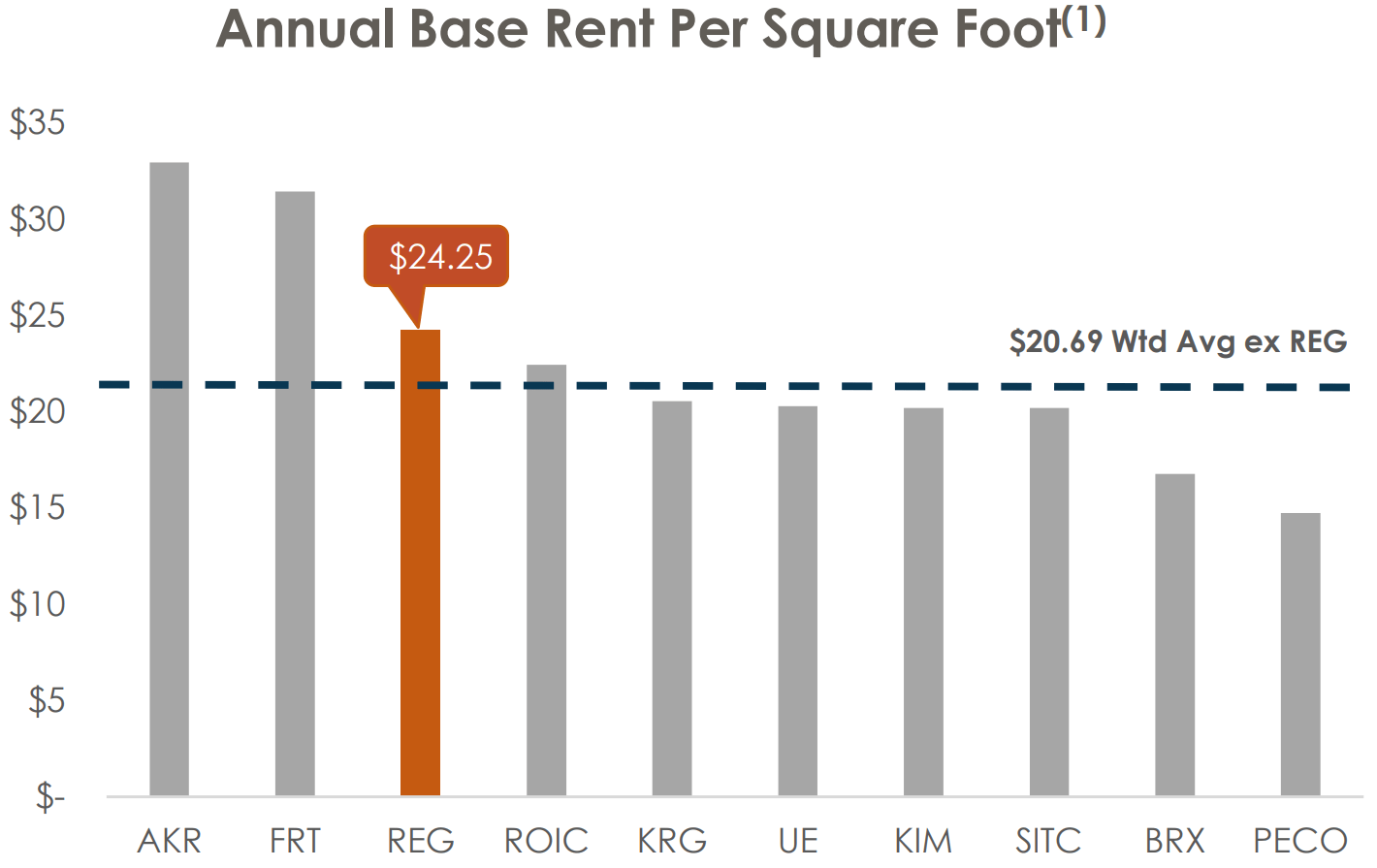

Having exposure to areas with high population density and above-average household rent enables it to charge above-market rents, especially considering that the higher cost of development in these areas serves as a natural barrier to entry for competitors. As shown below, REG ranks third in annual base rent per square foot compared to its peers, sitting behind Acadia Realty Trust ( AKR ) and FRT.

{kind=link}

REG's attractive rent metric is supported by its high-quality tenant base, which includes high-profile grocers like Publix, Kroger ( KR ), Whole Foods ( AMZN ), and Safeway ( ACI ). This is reflected by the fact that 77% of REG's grocers have either a #1 or #2 share in their markets.

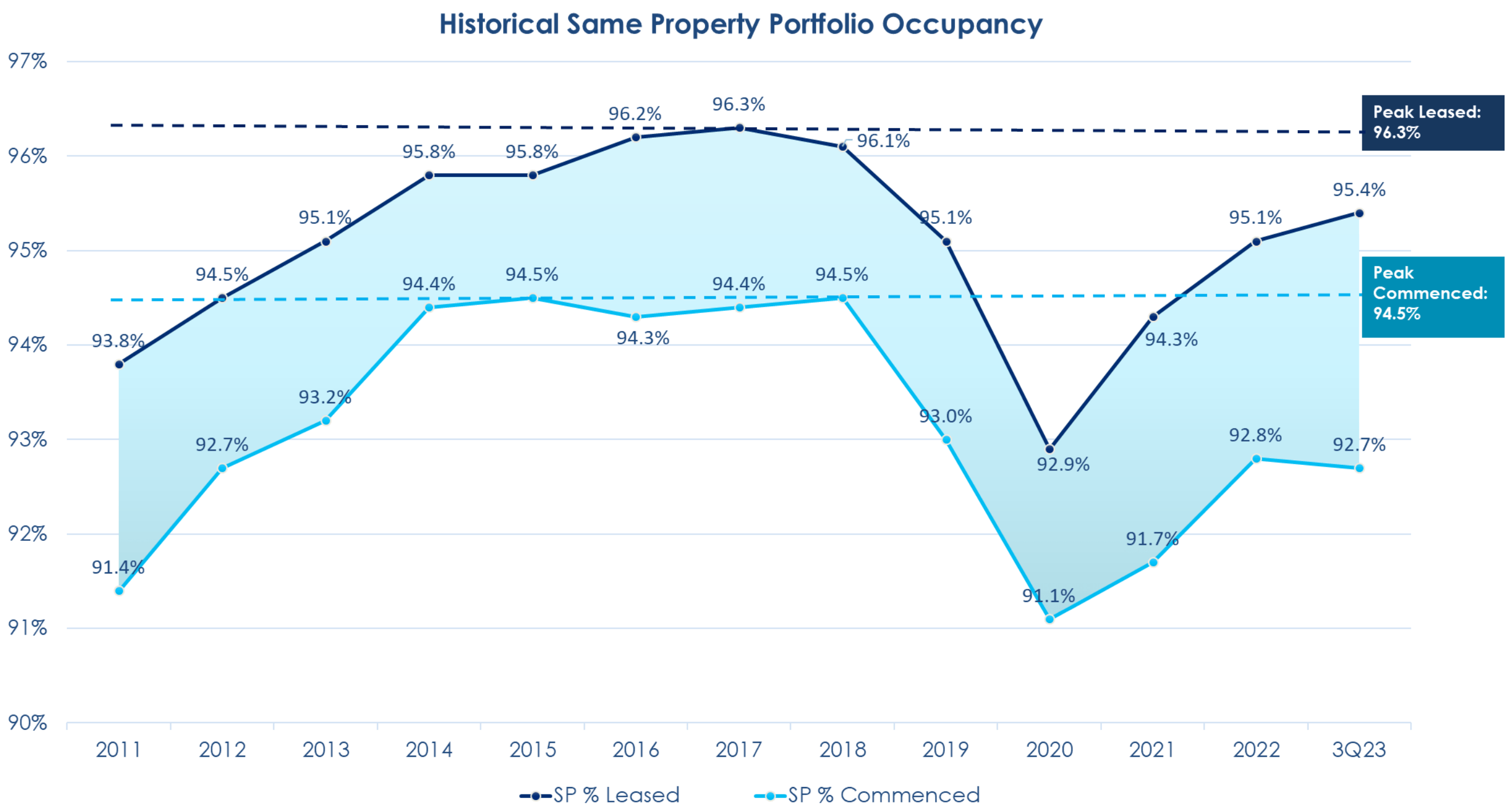

Meanwhile, REG continues to see respectable performance, with the same property NOI growing by 3% YoY during the third quarter, while the same property leased rate also rose by 70 basis points YoY to 95.4%. REG still has room for improvement, as the leased rate remains below where it was in pre-pandemic times, despite being materially up over the past couple of years, as shown below.

{kind=link}

Moreover, tenant demand remains solid, as REG saw blended rent spreads (on new and renewal leases) of 9.3% on a cash basis and 17% on a GAAP straight-line basis. Notably, these strong results enabled REG to raise its full year FFO/share guidance to $4.14 at the midpoint, up from $4.10 earlier his year.

Looking ahead, the investment thesis in REG is supported by structural tailwinds supporting grocery-anchored shopping centers due to low new supply , creating scarcity of value. In addition, per Coresight Research , after several years of investing in e-commerce, the tide is shifting back toward brick and mortar as retailers seek to capitalize on renewed demand for in-person shopping experiences.

The most prolific of which includes discount retailers like Nordstrom Rack ( JWN ), Ross Stores ( ROST ), and Dollar General ( DG ), and this serves to disproportionately benefit REITs like REG with high-quality locations. This is also supported by the addition of Urstadt Biddle's locations in the northeast (primarily surrounding regions of New York City) with high population densities. Management continues to target $200 to $250 million in annual development and redevelopment costs to support the necessity-nature of its last mile centers, as noted during the last conference call :

We remain really encouraged by the structural supply-demand trends that are supporting our business today. Our tenants continue to invest in brick-and-mortar stores that are profitable as a last mile distribution channel, and our suburban trade areas continue to thrive. And while we continue to create value through ground-up development, overall, there is very little new retail space being added in the U.S., supporting the value and scarcity of existing space.

Risks to the thesis include economic uncertainty heading into 2024, as household spending is growing but slowed down this holiday season, according to Mastercard ( MA ). Also, while the Federal Reserve signaled three quarter-point rate cuts in 2024 at its last meeting, interest rates still remain elevated compared to the past decade, and this introduces refinancing risk through higher borrowing costs.

Nonetheless, REG maintains a BBB+ investment grade credit rating from S&P and a strong balance sheet, which was a contributing factor in REG not cutting its dividend during the pandemic in 2020, when many of its peers had to cut theirs.

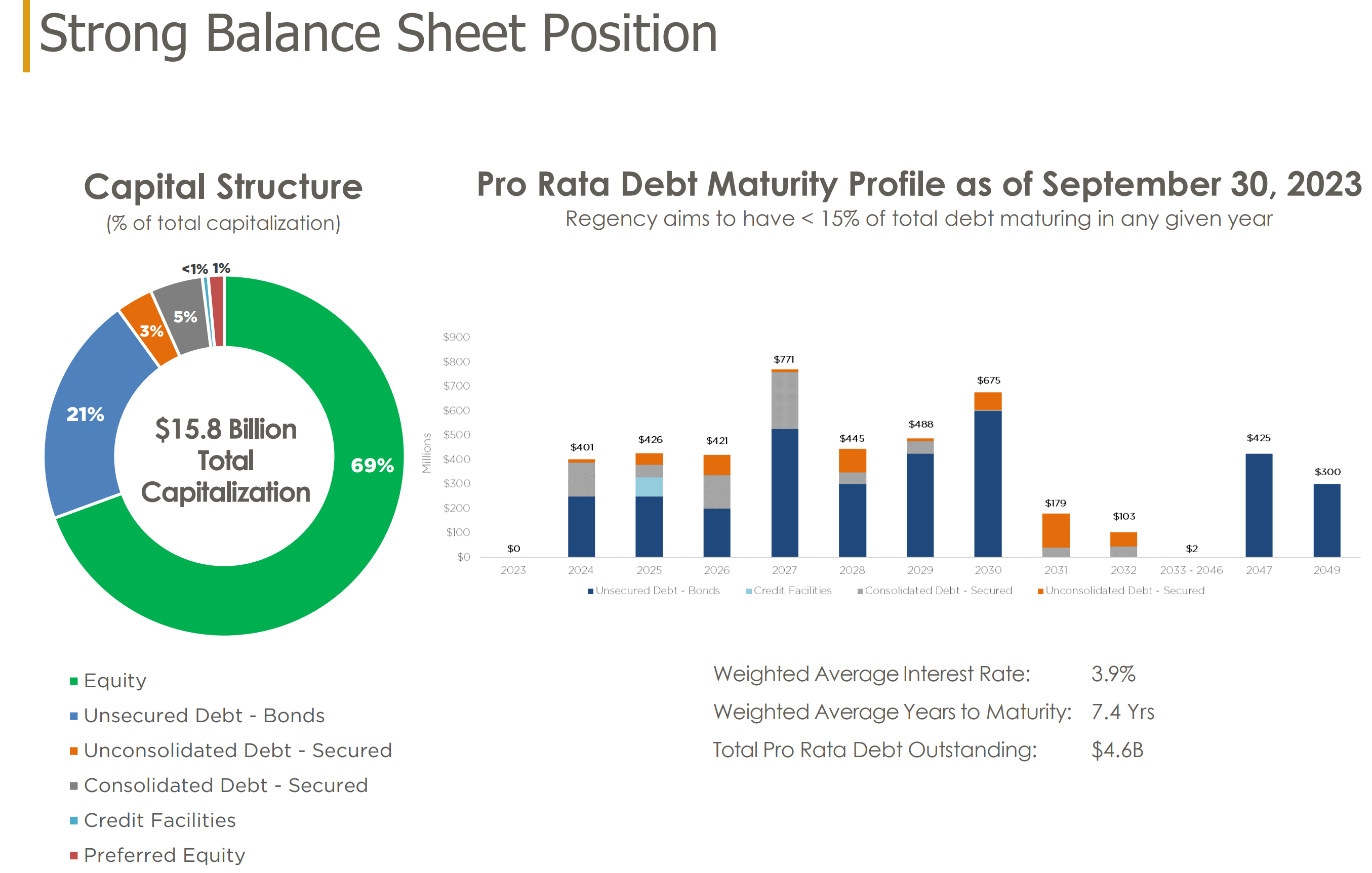

REG also carries a safe amount of leverage with a net debt and preferred stock-to-operating EBITDAre of 5.0x, sitting well below the 6.0x generally considered to be safe for REITs, and has strong fixed charge and interest coverage ratios of 4.7x and 5.2x, respectively. As shown below, REG's debt maturities are well-laddered between 2024-2026.

{kind=link}

Importantly for dividend investors, REG currently has a forward yield of 4.0%, after the company raised its quarterly dividend rate by 3.1% in November. The dividend is also well-covered by a 63% payout ratio, leaving plenty of retained capital to fund developments and for future dividend raises.

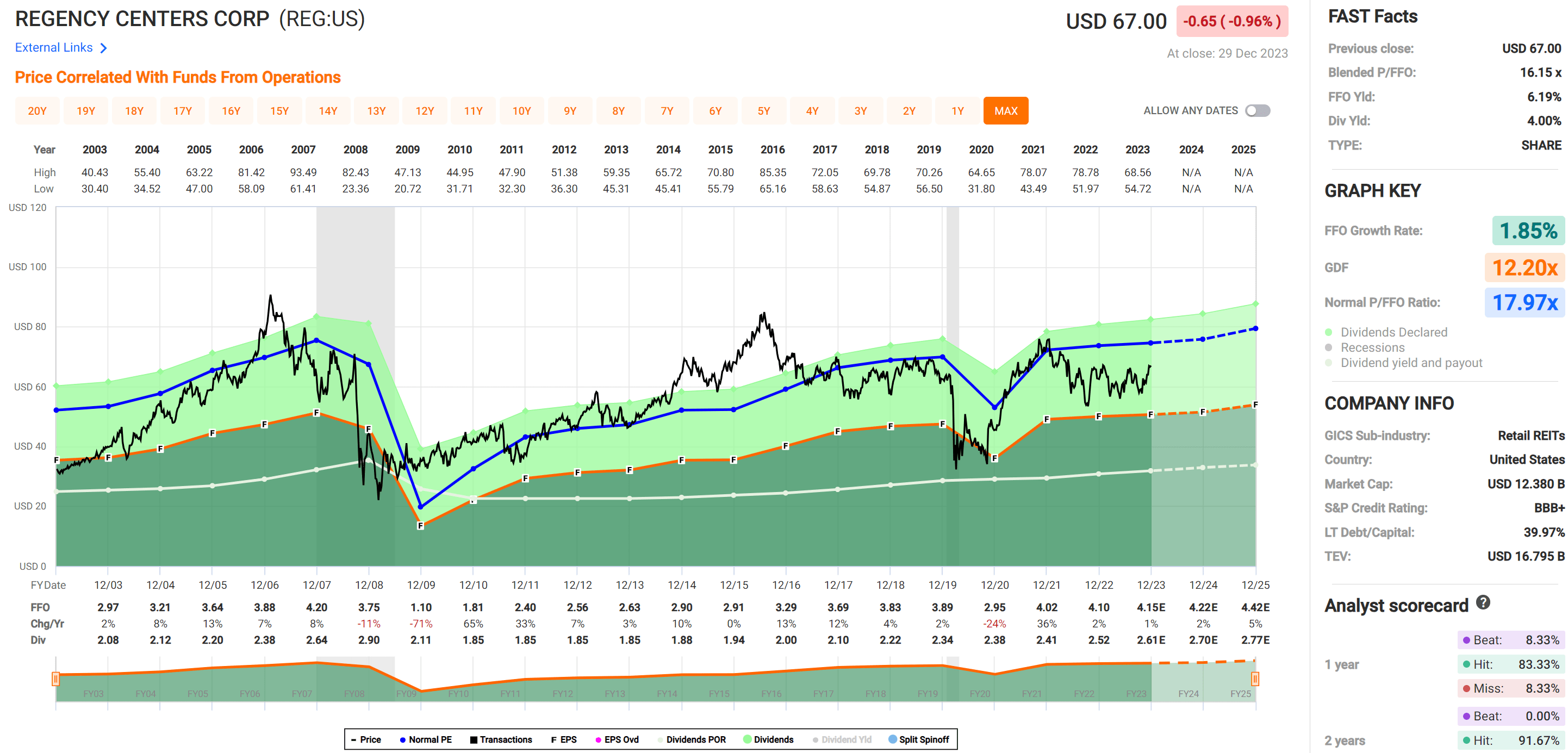

Turning to valuation, I continue to find REG attractive at the current price of $67 with a forward P/FFO of 16.2, sitting below its normal P/FFO of 18. Analysts also expect mid-single-digit annual FFO/share growth over the long run, which when combined with the current dividend yield, could match the 9-10% long-term total return of the S&P 500, but with far higher cash flow than the 1.4% yield that SPY is currently paying.

{kind=link}

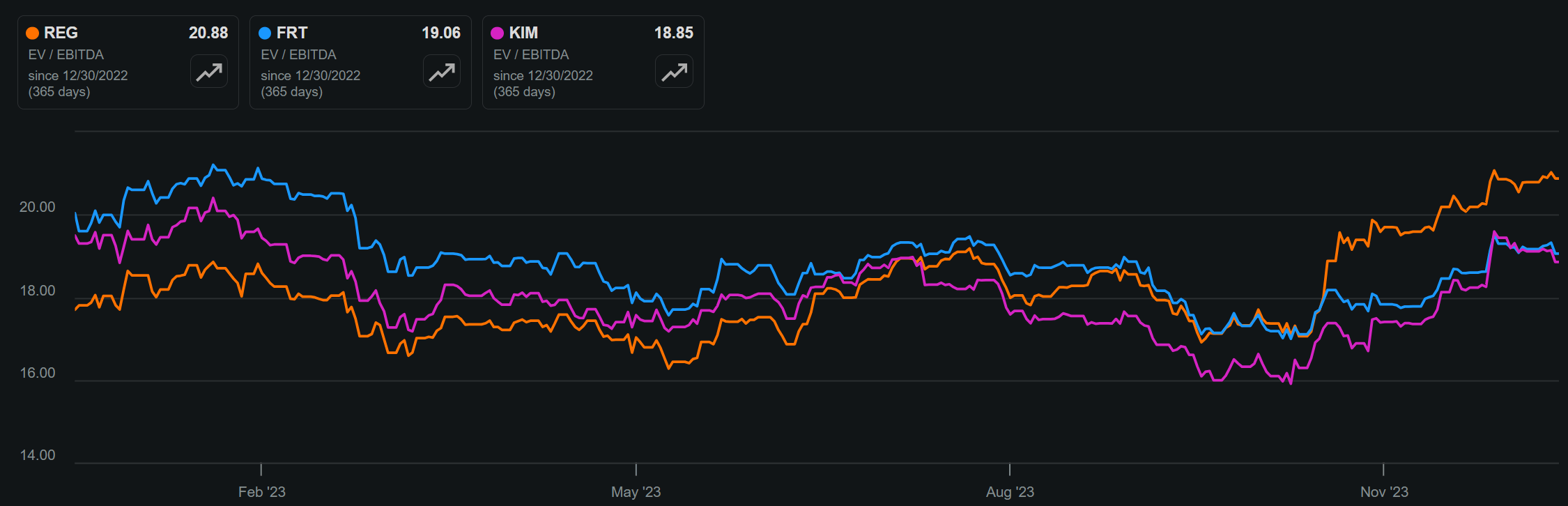

It's worth noting that REG is somewhat pricier at present than its two large peers, FRT and Kimco Realty ( KIM ), with an EV/EBITDA of 20.1, sitting higher than the 19.1 of FRT and 18.9 of KIM. However, there's nothing wrong with owning a basket of stocks, as REG has more grocery-anchored exposure than FRT and a better balance sheet than KIM.

REG vs Peers EV/EBITDA (Seeking Alpha)

{kind=link}

Investor Takeaway

Overall, REG is a strong choice for investors looking for sensible growth and reliable dividend income from the shopping center space. The company has consistently delivered solid operating results, while also protecting its dividend through good times and bad. With continued tailwinds supporting grocery-anchored shopping centers and a well-positioned balance sheet, REG should continue to deliver long-term value for shareholders. While REG is no longer cheap, I continue to find value in the shares at present and maintain a 'Buy' rating on the stock.

For further details see:

Regency Centers: Quality You Can Count On With A Decent Yield