KIM - Regency Centers: Unlock Value In This Prime Time REIT

2023-09-13 08:30:00 ET

Summary

- Regency Centers is a shopping center REIT with a high-quality portfolio of primarily grocery-anchored properties.

- The company has exhibited strong portfolio stats and a consistently high leased rate.

- The recent acquisition of Urstadt Biddle Properties is expected to result in synergies and contribute to future growth for Regency Centers.

It's been a while since I last visited Regency Centers ( REG ) with a 'Strong Buy' rating back in March, and the stock has done fairly well, despite plenty of market turmoil around higher interest rates and the Fed's proposal to raise capital requirements for banks.

The respectable performance is reflected by REG, giving investors an 8.5% total return since my last piece, which isn't too shabby considering the aforementioned economic volatility. In this piece, I reflect on recent developments and highlight why REG remains an attractive play for its high-quality real estate, and income potential, so let's get started!

Why REG?

Regency Centers is one of the largest shopping center REITs in America, but for one reason or another doesn't have as many followers on Seeking Alpha compared to large peers Kimco Realty ( KIM ) and Federal Realty Investment Trust ( FRT ).

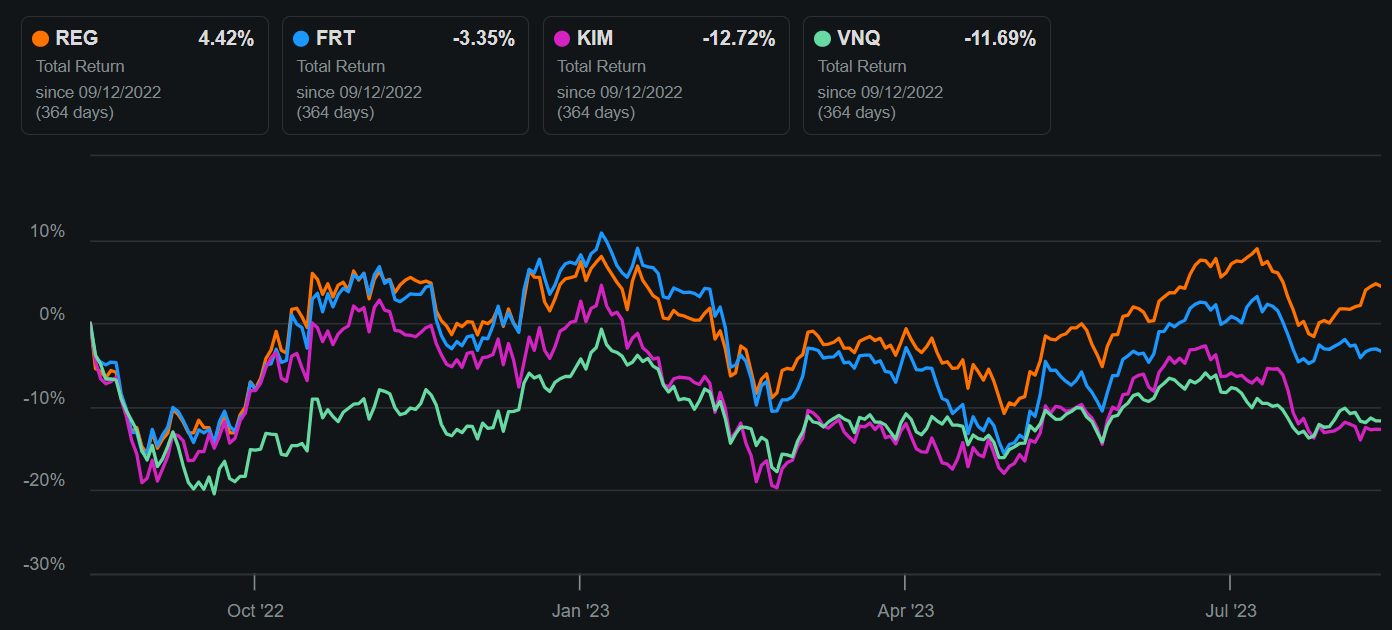

Unlike KIM, which continues to undergo portfolio transformation through mixed-use property development, and unlike FRT, REG has a higher component of grocery-anchored properties. Perhaps this is a reason why REG has produced a positive 4.4% total return over the past 12 months, comparing favorably to the negative returns for FRT, KIM, and the Vanguard Real Estate Index Fund ( VNQ ), as shown below.

REG & Peers Total Return (Seeking Alpha)

{kind=link}

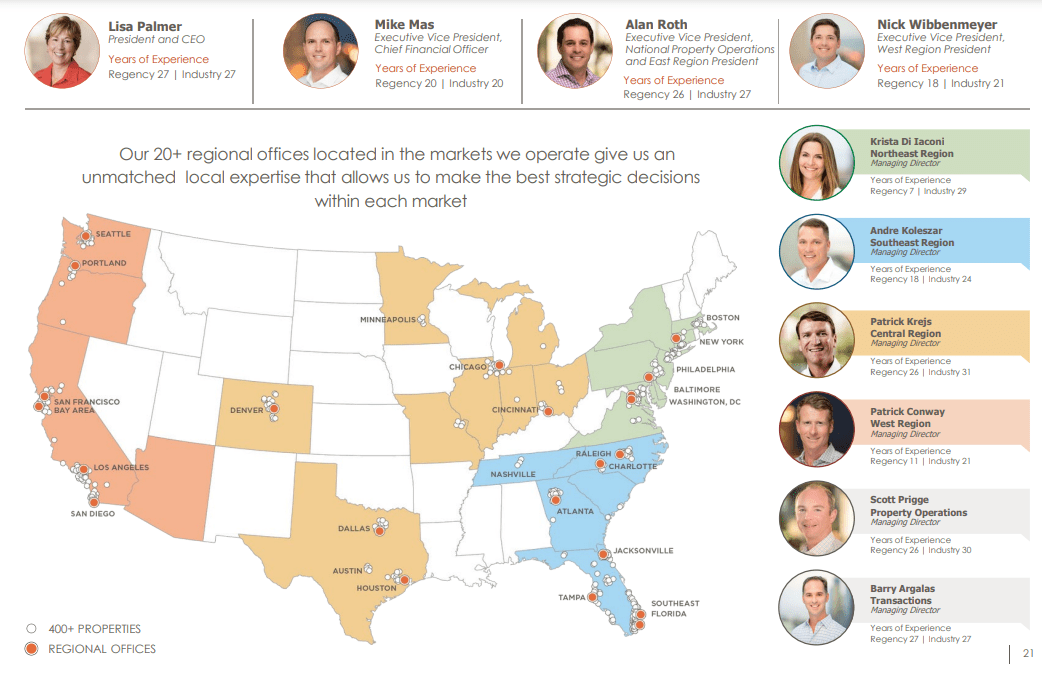

REG's high-quality portfolio of primarily grocery-anchored properties makes up over 80% of its annual base rent. It's also diversified by geography, with 400+ properties spread across the U.S. As shown below, it has a presence in large MSA markets across the U.S. and is led by a seasoned management team with an average of over 20 years at the company.

{kind=link}

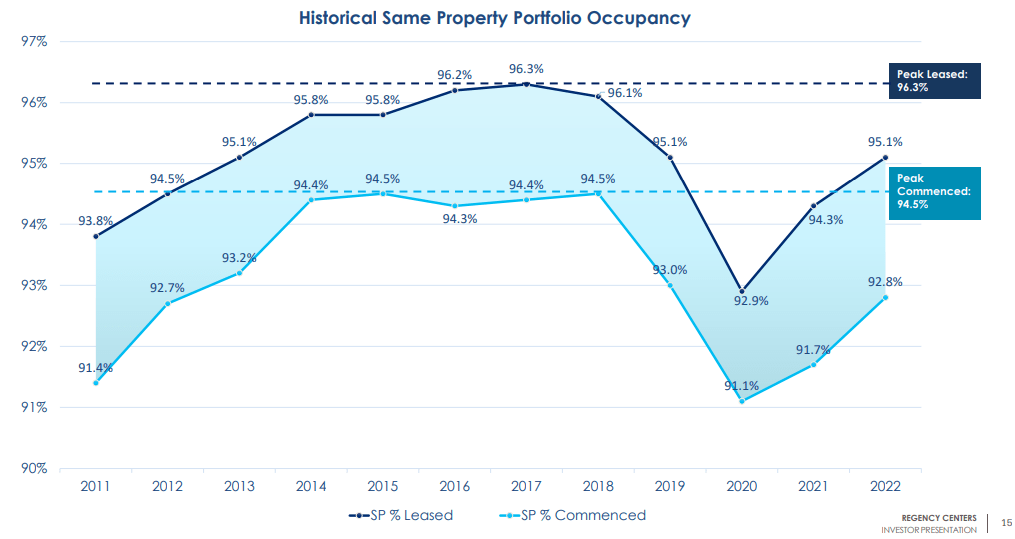

REG has also exhibited strong portfolio stats over its history, with a portfolio leased rate that's never fallen below 90%, even during 2020 when the pandemic hit, as shown below.

{kind=link}

The upward trajectory in REG's leased rate continued during the second quarter, with the same property leased rate improving by 70 basis points in the second quarter to 95.2%. Higher rental income contributed to 3.6% YoY growth in the same property NOI. This includes 11.7% cash lease spreads on 2 million square feet of new and renewal leases signed during Q2.

One of the most exciting events that transpired at REG since my last piece is its acquisition of Urstadt Biddle Properties (UBA) in a 100% stock for stock exchange that didn't require debt issuance as a direct result of the merger. For those unfamiliar with UBP, it's a shopping center REIT with a portfolio concentration in high-income and barrier-to-entry markets surrounding the Greater New York City area.

The resulting company is one in which 93% and 7% of the stock of the combined company belongs to pre-Merger REG and UBP shareholders, respectively. Management expects to achieve synergies as a result of this merger, which are expected to be fully realized in 2024, as described during the last conference call :

Our expectation is to deliver incremental per share core operating earnings accretion of $0.01 in 2023, reflecting about 4 months of impact and plus or minus 1.5% accretion for the full year of 2024, which continues to include an estimated $9 million of annual G&A cost synergies.

Risks to REG include merger integration risk as it relates to the UBP acquisition, but this shouldn't be too much of an issue given management experience and the similar nature of the properties. Other risks include REG's exposure to Florida properties, which may be subject to higher insurance premiums due to hurricane risk.

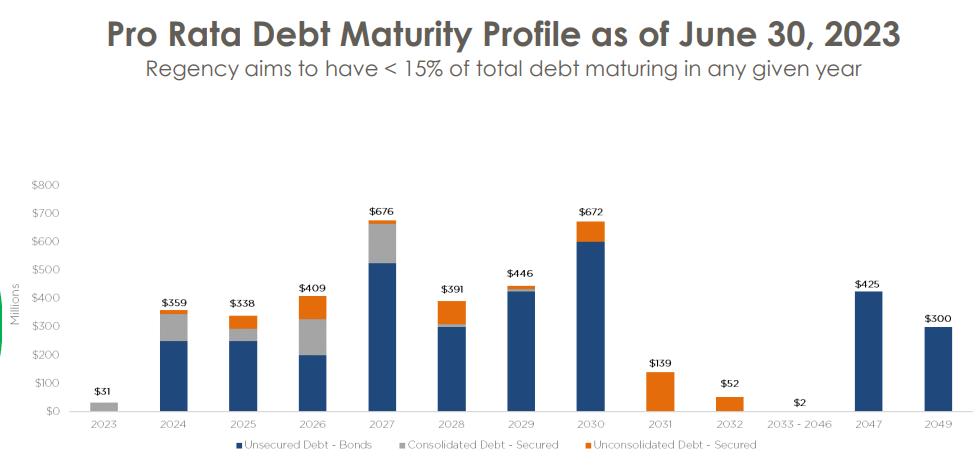

Also, REG is expected to have slightly higher pro forma leverage (net debt to EBITDA) at the low end of the 5.0 to 5.5x range, which is slightly higher than the pre-merger level of 4.9x. Nonetheless, this sits well under the 6.0x level generally considered safe by ratings agencies, and REG carries a BBB+ investment grade credit rating from S&P. As shown below, debt maturities are well-staggered with the aim of having less than 15% of debt maturing in any given year, thereby mitigating interest rate risk.

{kind=link}

Importantly for conservative income investors, REG currently yields 4.1% and the dividend is well-covered by a 63% payout ratio. While this isn't a particularly high yield, I view it as being a reasonable one considering the low leverage and high-quality portfolio, which didn't necessitate a dividend cut during 2020. Plus, REG grew its dividend by 4% this year, and mid-single-digit annual dividend growth going forward could contribute to 8-9% annual total returns for the stock.

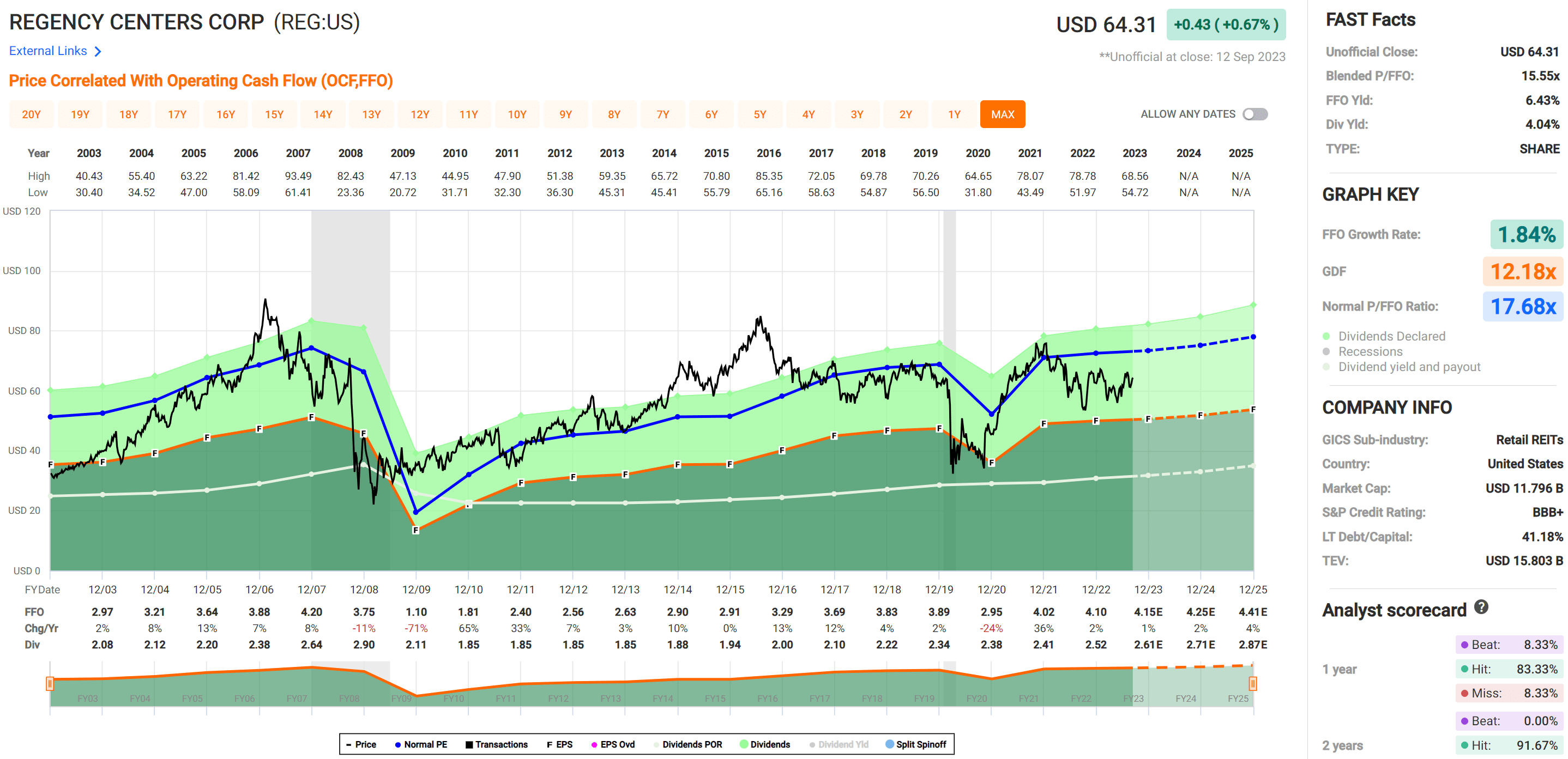

Lastly, I continue to find REG to be reasonably attractive at the current price of $63.88 (as of writing) with a forward P/FFO of 15.4. I'm downgrading it from a 'Strong Buy' to a 'Buy' as it's not as cheap as the 14.4 P/FFO when I last visited the stock. Nonetheless, REG still trades at a discount compared to its normal P/FFO of 17.7, as shown below.

{kind=link}

At the current valuation, REG could potentially produce the long-term return of the S&P 500 ( SPY ) with a higher yield and the satisfaction of owning high-quality income-producing real estate. I also see the potential for REG to return to its mean valuation with slowing inflation in the U.S. as seen during the month of August, which could lead to a more favorable interest rate environment.

Investor Takeaway

Regency Centers has a number of attractive features, making it an appealing play for income and total return-oriented investors. Its experienced management team, low-leveraged balance sheet, high-quality portfolio, and recently completed UBP merger make REG an attractive REIT in today's market. With its ~4% dividend yield and potential mid-single-digit dividend growth going forward, REG could produce the long-term return of the S&P 500 with a higher yield from high-quality income-producing properties.

For further details see:

Regency Centers: Unlock Value In This Prime Time REIT