RHHBY - Regeneron: Eylea Hype Past But '23 H2 Will Be A Gut Check

2023-07-07 05:07:59 ET

Summary

- Regeneron's stock price has suffered a setback due to concerns over the future of Eylea, its flagship drug, as competition and potential drug pricing regulations loom.

- The company's immunology collaboration with Sanofi continues to show promise, particularly with Dupixent, which recently passed Phase III clinical trials for severe cases of COPD.

- Regeneron's focus on technology platforms and genetic therapeutics, driven by its collaboration with Alnylam, is expected to produce multiple product opportunities and drive long-term growth.

- The stock is closer to fair value now than in the past; likely a good time to open a position, maybe not for adding to existing positions.

With Q1 earnings in the rearview mirror and Q2 wrapping up, Regeneron (REGN) has been busy making the rounds with analysts and conferences. Since our last article, the stock price received a short-lived bump from some promising clinical trial data before deflating back to roughly the same point as four months ago, then suffering another setback regarding the future of Eylea, retracing all of the year's gains so far. The question now, naturally, is whether Regeneron's fair value has changed at all in those four months. We contend that the best-case scenario has improved, but the current price is still on the high side.

?Eylea: Between a rock and a hard place

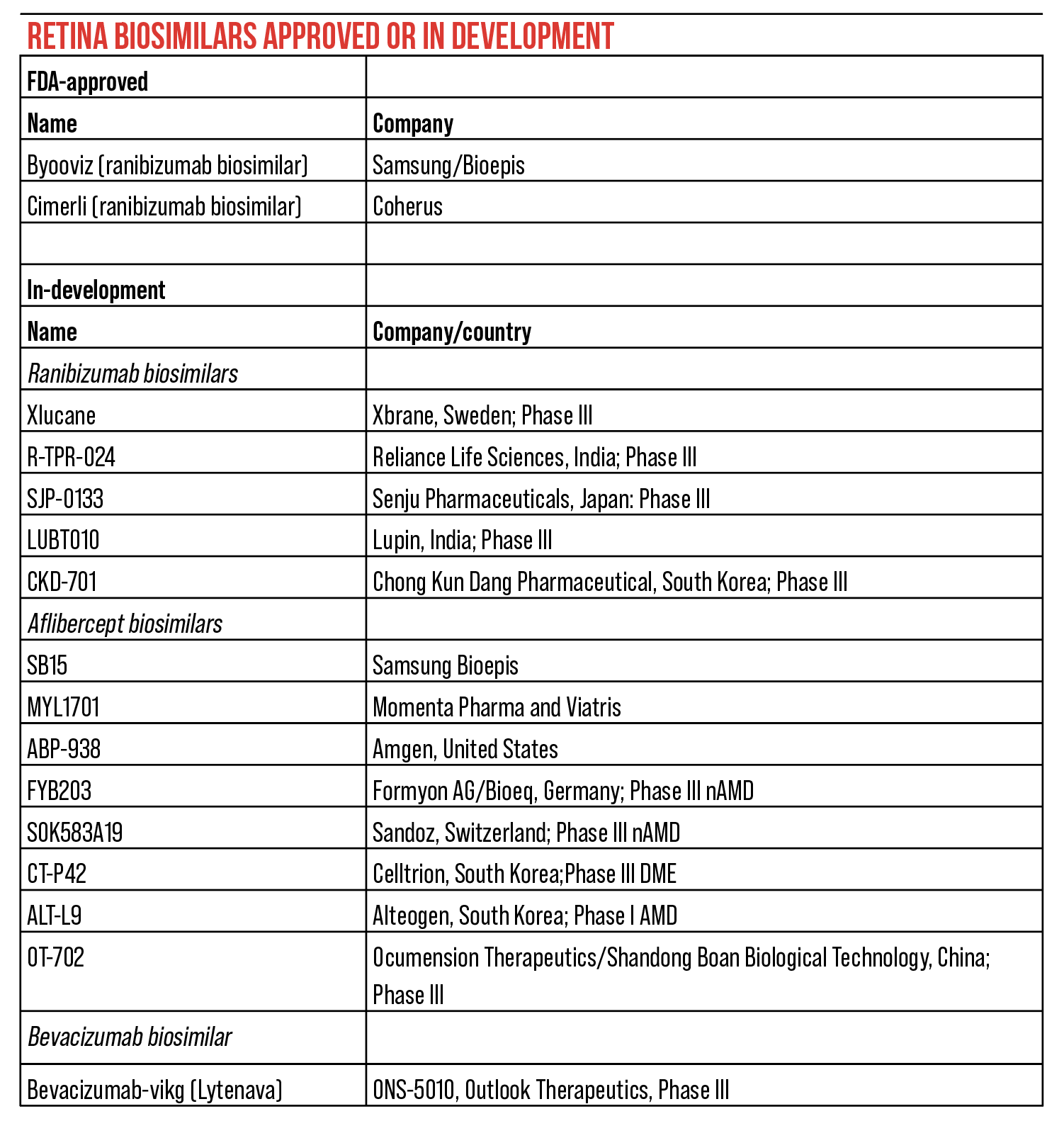

Analysts continue to focus on Regeneron for Eylea (aflibercept), now more than ever due to the increased competition, biosimilars coming closer and closer to the market, and possible drug pricing regulations. The year-over-year Eylea quarterly revenues dropped for the second quarter in a row. The Q1 '23 drop was attributed to a margin compression, but nonetheless could be the proverbial blood in the water. Meanwhile, Roche's (RHHBY) Vabysmo notched 432MM CHF ($384.96MM USD) in Q1 2023, credited mostly with switches from aflibercept.

Regarding the impending Eylea biosimilars, Marion McCourt, head of Commercial, commented at the Goldman Sachs Global Healthcare Conference in mid-June that biosimilar uptake for Lucentis, the gold standard AMD treatment when Eylea came on the market, was "modest". Granted, at the time off-label Avastin was also quite popular, and Lucentis biosimilars continue to be developed. Makers of marketed Lucentis biosimilars are also leading the way with Eylea biosimilars, such as Samsung Bioepis and Coherus , so the landscape may be more competitive in a few years than management is considering at this point.

{kind=link}

The main attraction now, though, is the "high-dose" 8-milligram injection regimen. We intentionally held off on publishing this article until the PDUFA decision came out, which resulted in a denial for the new regimen. The rejection appears to be unrelated to the efficacy of the treatment, but to production irregularities that should be sorted out before too long. That pushes back the time to market for the new product, possibly beyond 2023. It is definitely a worrisome development for a product that, for all intents and purposes, felt like a slam dunk. We aren't going to raise too much alarm given that the product itself is solid, but a rejection based on production issues smacks of leaving brown M&Ms in Van Halen's green room; are they overconfident and letting small mistakes slip in?

One interesting wrinkle to this side of the story is the potential for the Inflation Reduction Act to require some kind of drug pricing agreement for Eylea. Ryan Crowe, head of Investor Relations, gave the following response (emphasis ours):

We've...seen the Part D guidance that CMS issued a couple of months ago, which seemed to aggregate products with the same active moiety . I think we need to wait to see what the Part B guidance could look like. But should they take a similar approach for Part B drugs so long as there's enough aflibercept 2-milligram biosimilar on the market, we believe that aflibercept containing products would not be subject to price negotiation because there is biosimilar competition .

It sounds like a Catch 22: biosimilars would almost certainly hurt revenues for the 2-milligram product, but also might protect their 8-milligram product from price negotiation since it contains the same active ingredient.

?"Du-ing" more with Dupixent and Immunology

The immunology collaboration with Sanofi (SNY) is continuing to fire on all cylinders, both with the marketed drugs and the tip of the pipeline. In March, Sanofi and Regeneron announced that Dupixent passed Phase III clinical trials in severe cases of COPD (classified as an eosinophil count over 300; they consider this cutoff arbitrary but it suffices for a BLA). Much of the chatter from analysts and executives has been whether they will submit an FDA application with just the one trial. The company's position is that Dupixent is an established, well-tolerated drug in numerous related conditions. Many of the patients in the clinical trials, still experiencing exacerbation despite being treated with the strongest care regimen available, experienced symptom improvement with Dupixent. Moreover, they comment that COPD is a leading cause of death without a cure, meaning the market is wide and untapped for their therapeutic. It all sounds nice, but we worry they may be slightly overconfident in their ability to land another label expansion, especially after high-dose Eylea fell flat.

The company estimates 300,000 patients in the US and 500,000 in the G7 markets can immediately benefit, which we see easily expanding to less severe cases over the next few years, provided they can generate the trial data to back it up. Meanwhile, the IL-33 inhibitor itepekimab has shown promise in former smokers, which has us wondering if there's a chance that this line of research could eventually reach beyond COPD and into emerging pulmonary conditions such as "long COVID", as the long-tail effects of the pandemic become clearer and Regeneron's research strengths allow them to explore these markets.

Itepekimab in particular has been a fantastic showcase for Regeneron's basic science roots through the Regeneron Genetics Center, which now performs genome-wide association studies (GWAS) on at least half of all the human genomes that have been fully sequenced, according to management on the Q1 earnings call . Even just ten years ago, GWAS as a technology didn't have the kind of power to be revealing any real patterns, let alone driving drug design; now Regeneron is using it to identify protective mutations and back those mutations into promising drug candidates. At the Jefferies Global Healthcare Conference at the beginning of June, Ryan Crowe commented how their genetic screening identified a gene, GPR 75, that appears correlated with obesity and has opened up at least three new potential treatment avenues. Correlation does not imply causation, however, a maxim every statistics student knows by heart, and thus the challenge of relying on GWAS more extensively as a drug discovery tool.

There is also a challenger approaching Dupixent in the form of Lilly's ( LLY ) IL-13 inhibitor lebrikizumab, discussed at both the Jefferies conference and the Goldman conference. Regeneron's management remains confident that Dupixent's safety and efficacy are a strong enough moat against any competing therapeutic, regardless of the mechanism. At the Jefferies conference, Brook Jennings, VP of Commercial Dermatology at Regeneron, welcomed the Big Pharma giants into the atopic dermatitis space to do the heavy lifting of deeper market penetration:

[S]ince dupilumab launched in 2017 with the first atopic dermatitis indication, we were the only ones working to expand the market. So, with Pfizer having come to the market, with AbbVie having [come] to the market, with LEO having come to the market, the growth rate in the atopic dermatitis advanced therapeutics market has increased. I think Lilly will only add to that. I think that the benefit from a DUPIXENT perspective is when you have the lion's share of the market, you get a disproportionate share of that growth.

?Oncology: The ASCO Effect

The American Society of Clinical Oncology ((ASCO)) held their annual meeting the first week of June. Prior to the conference, Regeneron issued two press releases teasing trial results they were going to present, one for a combination fianlimab/Libtayo therapy in advanced melanoma and the other for their bispecific antibody linvoseltamab in "heavily pre-treated multiple myeloma" . Two SVPs working on these advancements also spoke at TD Cowen's Annual Oncology Innovation Summit prior to the conference proper, where they expounded upon the results of the trials and the roadmap for the therapeutics in question. Of note:

-

Linvoseltamab achieved a 71% response rate with most adverse reactions limited to Grade 1 CRS (fever); stated to be on-track for filing by the end of the year

-

Adding fianlimab to the existing PD-1 monotherapy produced a 63% response rate, with Phase III trials for melanoma getting underway and expecting to be completed by 2025

Beyond these two treatments, management and analysts highlighted other standouts in the oncology pipeline:

-

Odronextamab, a bispecific for advanced lymphomas, on track for filing in the US and EU in the second half of the year

-

Fianlimab being trialed for metastatic (Phase II/III) and perioperative (Phase II) non-small cell lung cancer

-

Multiple costimulatory bispecifics in the solid tumor space and lymphoma should be getting more data in the coming months

The combination LAG-3/PD-1 treatment may have an easier time from a regulatory perspective but a more difficult time from a commercial perspective thanks to Bristol-Myers (BMY) launching their LAG-3/PD-1 therapy Opdualag a little over a year ago . BMS is already trialing Opdivo (PD-1) and relatlimab (LAG-3) for lung, liver and colon cancers as well (and don't think they won't expand to other indications where Opdivo or Opdivo/Yervoy are established: bladder, kidney, prostate...), so the race is on now to see which of these treatments has the safety and efficacy profile to achieve approval as a first-line treatment or a treatment for less-severe cases. It looks to be a two-horse race at the moment, since the only other LAG-3 inhibitor mentioned out there is ieramilimab from Novartis ( NVS ), and we can't find it listed in their pipeline.

Bristol Myers Squibb Website Bristol Myers Squibb Website Bristol Myers Squibb Website

{kind=link}

{kind=link}

{kind=link}

?Emerging platforms

Regeneron's business model has always focused on the broadly-applicable underlying technologies - platforms as management refers to them - versus the individual indications or branches of medicine, and this approach is one of the main reasons we're bullish on them for the long-term. During the RBC Capital Markets Global Healthcare Conference in May, Aris Baras, director of the Regeneron Genetics Center, summed up how deep this mentality runs (emphasis ours):

We really believe in technology platforms. We invest heavily. You know Regeneron as a company as a technology development company , antibodies, traps[,] been prolific in that over the last 30 years. And we like technology platforms that are not a single product opportunity, but they can be multiple product opportunities from the platform.

It is an interesting thought experiment to chart the trajectory of their various biotechnology platforms and how even the platforms appear to be reaching an inflection point alongside the commercial side of the business. Eylea was their breakout therapeutic from the "traps" era, followed by Dupixent and Libtayo for VelocImmune and antibodies, now moving into bispecifics, costimulatory and beyond.

With this "beyond" bucket, genetic therapeutics appear to be the next opportunity waiting to burst out, driven largely by the Alnylam ( ALNY ) collaboration. During his schooling, Derek heard lots about RNA-interference as one of the bleeding-edge discoveries of modern molecular biology, with the Nobel Prize awarded for it in 2006, only eight years after the key breakthroughs. The pharmaceutical applications of the technology, however, eluded researchers for similar reasons as immunotherapies: a hair-trigger innate immune system and high risks of off-target effects if the drug was not precisely targeted. Enter Regeneron, using their expertise with antibody platforms to deliver genetic payloads with the necessary precision.

The promise is reaching a fever pitch, as during Q1 earnings calls, the two companies reported they were able to demonstrate a drastic, long-term reduction in cerebrospinal fluid levels of amyloid precursor protein ((APP)), which eventually breaks down into peptides making up the plaques found in brain tissue. Not only is this approach orthogonal to the plaque-clearing mechanisms being pursued by names such as Biogen ( BIIB ) and Roche, it has broader applicability as both a prophylactic treatment (stop the plaques before they start) and a first-line intervention (prevent the existing damage from getting worse). Furthermore, given a gene-based mechanism is more easily tuned by simply changing the complementary nucleic acid sequence of the payload being delivered ( orders of magnitude simpler and cheaper than producing a modified protein therapeutic at production-scale), the opportunities in adjacent neurological conditions appear ripe for the picking if all goes right.

This transformative breakthrough is alongside the incremental work being done on liver disease, which checks all the boxes for the kind of challenge Regeneron likes to take on: urgent need, lack of good current treatment options, poor prognosis for patients. GPR 75, the obesity lead target from the Regeneron Genetics Center, has also been floated as a candidate for RNAi-based intervention. There hasn't been much chatter recently regarding the gene editing-based therapeutics collaborations with Intellia and Decibel, but they did announce an investment into Sonoma Biotherapeutics and their novel approach to (mostly type 1) autoimmune conditions through regulatory T cell engineering. True to the philosophy, they aren't resting on the laurels of Dupixent and itepekimab and are continuously looking out for the next platform on which they can bound forward.

{kind=link}

?Operations

The company continues to churn along, and we're quite happy with their operational performance alongside the scientific progress. Two pieces we want to address are the company's use of capital and the leadership question we called out in our previous article.

?Capital

It is refreshing to see a biotech company strive for cost-effectiveness and applying their advanced technology not just to the development of new medicines, but to the efficient commercialization of those medicines. At the Goldman conference, when asked about margin expansions for Dupixent, CFO Bob Landry credited the numbers to an improvement in the production process:

[W]e've changed the cell line of the drug substance product that makes up Dupixent in which we are now getting kind of 3x, 3x the active protein yield per batch than we were getting before ... So my batch costs and the Sanofi batch costs are not changing, but the amount of protein we're able to get out of that is a multiplier of 3, which means we can obviously do 3x as many doses off of the same batch costs…

Derek can attest to the painstaking amount of work required to scale up commercial production of therapeutics, especially biological therapeutics like antibodies; entire PhD theses are written out of this desire for more efficiency, so a 3x yielding cell line is a big win for the business.

M&A frequently comes up as a capital-related operational question to Landry when he speaks to analysts, especially with over $12B on the balance sheet as of Q1. In his two conference appearances since Q1 earnings - the Goldman conference and the BofA Global Healthcare Conference - Landry (and McCourt, in her one appearance) echoed the company's mindset of investing in technologies and platforms that can produce franchises, not one-offs or bolt-ons. It's important to remember that cash reserves on the balance sheet represent prior earnings and are not necessarily indicative of how much the company is able to spend or earn moving forward.

Relatedly, the subject of returning capital to investors was also broached at the BofA conference, possibly in the form of a dividend. Landry remarked that he believes they are still a "growth company" and their capital priorities are, first and foremost, all about reinvesting in the business as long as it can continue to provide an outsized return. His opinion is that a token dividend is not worth it for investors:

I don't think 100 basis points is kind of a meaningful yield to investors... It's not going to move the needle. And if you can't do something meaningful, then you're better off kind of reallocating it and wait until you can do something meaningful for the investor base.

As numerous financial experts have pointed out, once you start paying a dividend, you can't stop paying one without taking a massive credibility hit. Buybacks, however, have been employed skillfully by Landry and his team, buying back nearly $3 billion in stock over the last five quarters at an average share price of $545, as clear a sign as any that those are bargain purchases (agreed) and that the ROI from those buybacks beats most other opportunities (also agreed).

?Leadership

We mentioned in our last article that the company's founders, Len Schleifer and George Yancopoulos, have been the only ones in charge since inception, and we were curious what the succession plan was, if any. The plot thickened in April when the company's Chairman, Roy Vagelos, announced his retirement , and Schleifer and Yancopoulos were named as co-Chairs. There was no mention of whether their appointment was "interim", which likely means that they'll be calling the shots for the foreseeable future. Frankly, this is one instance where we believe their interests are firmly aligned with shareholders', so we'll let it ride for now, but we are paying ever closer attention to the dynamics here, especially after high-dose Eylea. If they do submit an application for Dupixent in COPD with just the BOREAS trial data and it is rejected, that would be a massive red flag to us in terms of their pipeline management.

Also in our previous article, we floated a few possible names that could step up to the top management spot if necessary. After reading the conference transcripts, we would add Aris Baras, the head of the Regeneron Genetics Center, to that shortlist. Given the importance of RGC to Regeneron's basic science and their drug development pipeline, it stands to reason they place a high degree of confidence in the individual charged with overseeing that entity.

?Valuation

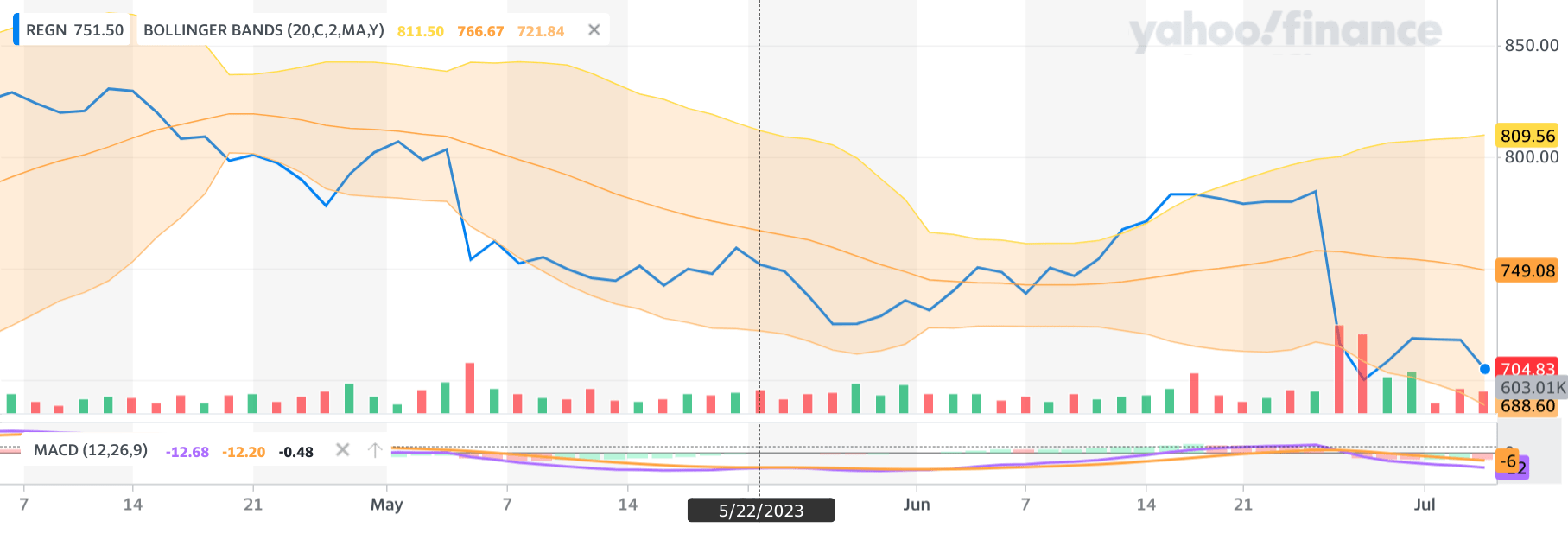

Regeneron is facing short-term pain with Eylea but has even stronger long-term prospects for the rest of their portfolio, thus we can increase our fair value estimate but not by much. Their valuation metrics have improved a bit as of late, and we believe this is more froth-skimming than any true deterioration of the company's prospects. Don't think that people didn't use the high-dose Eylea rejection as an excuse to take profits; volume in the days after the decision was higher than their Q1 earnings miss and rivaled the positive volume after the Dupixent COPD results in late March, with a sharp rebound towards the end of the week. Most technicals also seem to suggest that this dip is oversold, which is encouraging as far as a potential price rally in the near-term.

{kind=link}

From a DCF perspective, we previously used a lumpy 8.4% growth rate and 17% discount rate for an estimate of $620/sh. Improved prospects for Dupixent and some potential for high-dose Eylea mean we can spot them another 50 basis points on the discount rate, which brings our revised fair-value estimate to $660/sh . Current prices may be close enough for those holding off to initiate a position. Meanwhile, we're still sitting on a lot of gains, so we'll wait and see how the next big moves pan out.

?Conclusion

The Eylea madness has, more than anything, caused a reset of the price to near-fair values. The treatment itself is in no immediate danger, and the next major breakthroughs are looking promising enough to allow the company to produce solid returns. We're confident in their tech, their pipeline, and their people, so we'll keep a close eye on the next few earnings, trials and applications, and make sure everything is lining up as expected in another few months.

For further details see:

Regeneron: Eylea Hype Past, But '23 H2 Will Be A Gut Check