RF - Regions Financial: Funding Pressures Hit Q3 Results And Leave Shares Unattractive

2023-10-20 12:46:24 ET

Summary

- Regions Financial Corporation shares plunged 15% after reporting a weak third quarter, adding to a difficult year for investors in regional banks.

- The bank's net interest margin continues to be squeezed by funding costs, leading to a decline in net interest income.

- Deposit flows and competitive deposit rates are crucial factors to consider when investing in regional banks, and Regions is facing ongoing deposit loss, making shares unattractive.

Shares of Regions Financial Corporation ( RF ) plunged 15% on Friday after reporting a weak quarter . This decline added to what has been a painful year for investors, as shares have suffered from the crisis that hit regional and mid-sized banks following the failure of Silicon Valley Bank. Last year , I rated shares as a "Hold," which proved to be too optimistic given the crisis. The company's results showed that the pressure in funding costs has not abated, continuing to squeeze its net interest margin ("NIM"). While the stock looks cheap, the regional banks are a sector under serious pressure, and RF stock is not the one I would take a long in.

{kind=link}

In the company's third quarter , Regions earned $0.49 in non-GAAP EPS, which was $0.09 below the consensus estimate and down 17% from last year. The bank's primary problem is that the rise in funding costs it faces cannot be fully offset by higher rates on the assets it owns. Accordingly, its NIM compressed by 31bp sequentially to 3.73% with net interest income ((NII)) falling by $91 million to $1.3 billion. This was a sharper-than-expected NIM compression, particularly as the Fed raised rates by just 25bp during the quarter. Deposits added 31bp of funding cost, meaning the bank had to pass on all of the Fed's rate hikes to customers and then some.

Within regional banks, I believe investors need to be very focused on deposit flows. Essentially the entire sector has a single-digit earnings multiple, so just about every stock screens "cheap" to the market, but I don't think you want to buy every single regional bank. With valuations compressed, you can choose carefully which ones to own, and I favor banks that appear to be through most of the pain on the deposit funding side. I look for: a) having brought deposit rates toward market levels, which means over 2% in aggregate; and b) having deposit levels that are stabilizing. Banks that have done this likely have higher funding costs already fully reflected in the results.

Unfortunately, even after the large jump in funding costs, its interest-bearing deposits still yield 1.81%, which is low. Because the rates it offers remain unattractive, we saw another $800 million sequential deposit decline to $126.2 billion, down about $9 billion from last year. The bank expects deposits to be "stable to modestly lower" in Q4. After disappointing across the board in Q3, I suspect "modestly lower" will be the outcome. Ongoing deposit loss is a sign its rates are not that competitive, which likely means further funding cost increases are set to come.

Regions Financial

As noted above, Q3's drop in NIM was a $91 million headwind. Management is guiding to a further 5% decline in NII in Q4, a $65 million headwind, or about $0.05 in quarterly earnings. Management expects net interest income to stabilize during H1 2024 and then gradually increase again, but if deposit attrition persists, its total interest-earning assets will also decline, likely putting more downward pressure on NII. Indeed, loans declined by $300 million sequentially to $98.9 billion, likely as lower deposit levels led it to tighten lending activity.

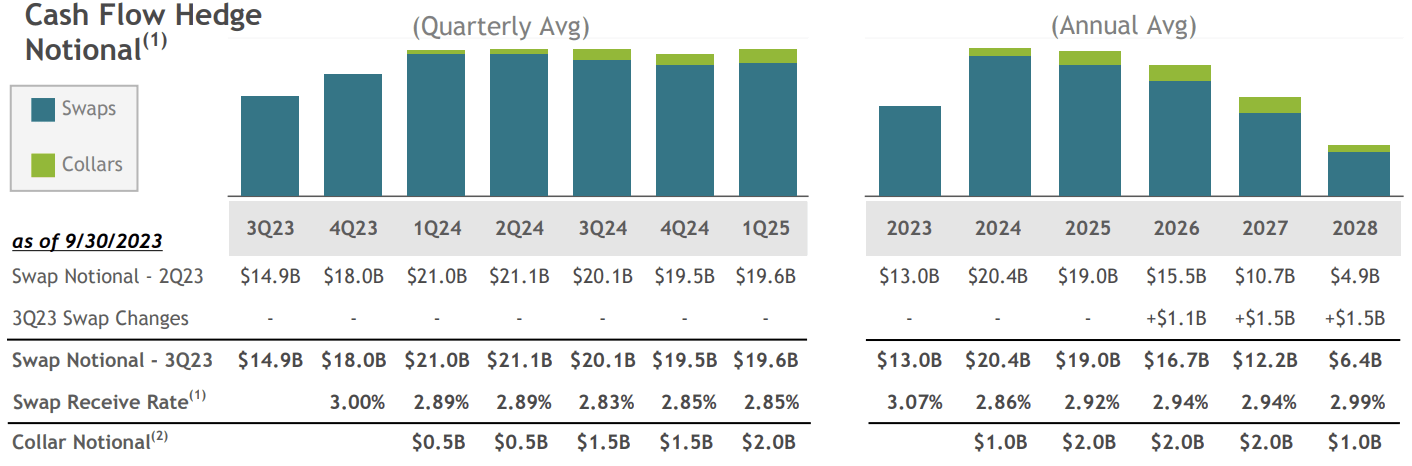

Exacerbating the problem of higher deposit costs, Regions, like many regional banks, also hedged away floating-rate yields at lower levels via swaps, which dragged $49 million on quarterly results. I can understand why after years of low rates management chose to lock in some of the increase in 2022, but this proved to be unwise. As you can see, these hedges at ~2.9% will continue to weigh on results in 2024-2025. As a result, assuming a stable deposit base, RF expects to be fairly limited in its exposure to higher or lower rates. However, my concern continues to be that its cost of deposits rises more quickly than the overall level of rates, which would be a headwind.

{kind=link}

Looking beyond its interest rate exposure, weaker capital markets activity led to a 2% decline in noninterest income to $566 million. The company did reduce expenses by 2% thanks primarily to lower incentive compensation to employees, offsetting this headwind. Regions is also seeing some credit deterioration. Its net charge-off rate was broadly stable at 0.4%, but nonperforming loans increased by $150 million to $0.65% of loans, a sizable quarterly increase. Regions took $145 million in provision for credit losses, up $27 million sequentially. This represented a $44 million reserve build

Allowances for losses of $1.68 billion provide 261% coverage to nonperforming loans. This should be an adequate level, barring a further deterioration in charge-offs. I do expect modest reserve builds to continue over the course of the economic cycle.

Regions ACL to office loans is 3.1%, which is lower than some peers like Citizens Financial Group (CFG). It is a little surprising not to see a higher office coverage relative to total loan coverage, given the significant pressures facing office space. Regions only has $1.6 billion in business office loans, so even adding another 5% ACL coverage over the next year would be just a $0.02 quarterly headwind. This is a risk but a manageable one.

Regions' common equity tier 1 capital ratio rose 100bp from last year to 10.3% as RF has halted its shared repurchases. RF needs to retain capital due to the phase-in of accumulated other comprehensive income/losses ((AOCI)) into its regulatory calculations. AOCI is where it houses its losses on its fixed income securities portfolio, which total about $4 billion, given the rise in rates. Including AOCI, CET1 is just 7.6%. Now, the securities portfolio has a 4.5-year duration, which is a bit on the longer side relative to peers, but it still means bonds at a loss today will gradually mature and pull toward par. The process will take several years, though. As you can see below, over the next two years if the forward curve plays out, about $1.3 billion of these losses will close.

Regions Financial

Importantly, Regions has the liquidity to let these bonds mature, rather than take losses. The combination of retained capital and shrinking AOCI losses will help RF manage capital headwinds without too much trouble. However, I would not expect share repurchases for at least 18 months. Its dividend is safely covered, and shares do offer a 5.8% yield.

This was a weak quarter, and it shows the impact of the bank funding crisis is still impacting results. Regions has been hit particularly hard, and unfortunately, I expect higher funding costs to persist as a problem into next year. Based on the company's guidance, Q4 earnings are likely to be $0.42-$0.44, and given its swaps and deposit headwinds, growth from there will be slow. Whereas earnings were expected to be over $2.40 next year prior to this quarter, they now are on track to be below $2.00 in my view.

At $1.90-$2.00, Regions Financial Corporation shares do have just a ~7-7.5x forward multiple, but I do see risk to earnings if deposits continue to fall and/or deposit rates move higher in response. Until we see signs deposits are on a better footing, I think regional bank investors should look elsewhere, and I would sell shares to buy a bank like CFG or Valley National ( VLY ) where the deposit outlook is better.

For further details see:

Regions Financial: Funding Pressures Hit Q3 Results And Leave Shares Unattractive