RF - Regions Financial: Q2 2023 Performance Instills Confidence To Remain Bullish

2023-07-24 21:25:31 ET

Summary

- RF reported strong 2Q23 performance, with an EPS of $0.59 and a pre-provision net revenue of $858 million.

- The bank's CET1 ratio increased from 9.9% to 10.1%, indicating a robust balance sheet and the potential for share buybacks in the future.

- Despite potential industry risks, RF's strong earnings, solid core PPNR, and conservative approach to maintaining excess capital support a continued buy rating.

Summary

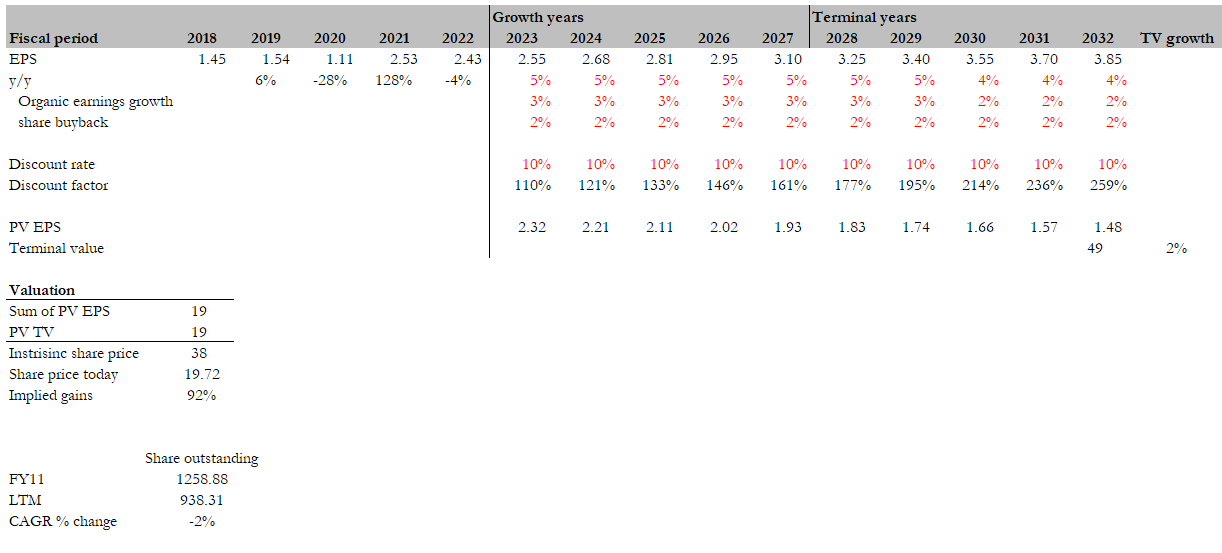

Following my coverage of Regions Financial Corp. ( RF ), which I recommended a buy rating as performance as a whole remains strong and the bank is unlikely to be affected by the normalization of credit across the industry. This post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for RF given its strong 2Q23 performance and my DCF model that suggests RF is worth $38, based on 3% organic earnings growth and 2% share buyback, driving mid-single digit EPS growth in the coming years.

Investment thesis

During 2Q23 , RF reported EPS of $0.59. PPNR (pre provision net revenue) was reported at $858 million, and after removing the effects of a few unusual factors like branch consolidation, etc., the core PPNR should be closer to $950 million. PPNR's NII was $1.39 billion, with core fees of $585 million helping to offset some of the slight increase in expenses attributable to incremental fraud expense. Average earning assets within NII increased by 0.5% sequentially to $138.2 billion, and average loans increased by 1.3% sequentially.

As for deposits, EOP deposits were down 1.2% from the previous period, which was in line with prior guidance. In particular, I highlight that the IB deposit cost increase of 42bps sequentially, which implies an 86% incremental beta and brings the cumulative beta to 26%, which is very strong relative to industry. Loan yields also increased by 26 bps on a sequential basis, which corresponds to an incremental beta of 54%.

Provisions of $118 million and a sequential decline in nonperforming loans indicate a healthy credit environment. The FY23 forecast was also revised by management, which they mildly reduced forecast for loans and deposits while reiterating their forecast for adjusted revenues, core expenses, and non-cash outlays.

With the expected one-time incremental fraud losses removed, I think RF had a good quarter overall. Core PPNR is modestly better after adjusting for $82 million in one-time fraud losses. Importantly, C&I and residential mortgage loan average balances both increased by 1% and 3% sequentially, fueling average earning assets growth at RF. This robust expansion of the balance sheet during the quarter helped to counteract margin headwinds. This resulted in NII of $1.4 billion being delivered. That being said, I anticipate that going forward, NIM will come under increasing pressure as deposit betas speed up. The mitigating factor here to monitor is how well can management execute its hedging strategy to support its NIM.

More on RF"s balance sheet, RF's CET1 ratio increased by 20bps sequentially, from 9.9% to 10.1%, and I anticipate the bank will maintain a CET1 ratio of around 10% for the foreseeable future as management keeps excess capital despite economic and regulatory uncertainty. Until 4Q23, when management should have a clearer picture of capital needs, I believe RF will wait to resume buying back its shares.

Valuation

I believe the fair value for RF based on my DCF model is $38. My model assumptions are that: RF will grow EPS organically at its historical rate of ~3% (low single digits) in the growth years (next 5 years), followed by a deceleration to 2% in the terminal years. However, I expect RF to eventually restart its share buyback program, which should contribute to 2% EPS growth annually as the share count decreases. The 2% assumption is based on my historical analysis of RF share buyback rate between FY11 and LTM. Together, EPS should grow in the mid-single digits.

{kind=link}

Risk

While RF is a strong bank, the recent results clearly support this point. I believe it is still thrown together in the same basket as all the other regional banks, as can be seen in March, when the stock dipped to $14. In the event of another banking turmoil or negative news, RF's valuation and share price will still be impacted, regardless of its fundamentals.

Conclusion

In conclusion, RF performance in 2Q23 has instilled confidence in me to remain bullish on the stock. With strong earnings, solid core PPNR, and healthy credit environment, the bank demonstrated resilience amid industry credit normalization. The increase in average earning assets and loans contributed to positive results. RF's conservative approach to maintaining excess capital and potential share buyback also supports my investment thesis.

For further details see:

Regions Financial: Q2 2023 Performance Instills Confidence To Remain Bullish