RF - Regions Financial Q4 Earnings Preview: Deposit Stabilization Is Essential

2024-01-16 08:30:00 ET

Summary

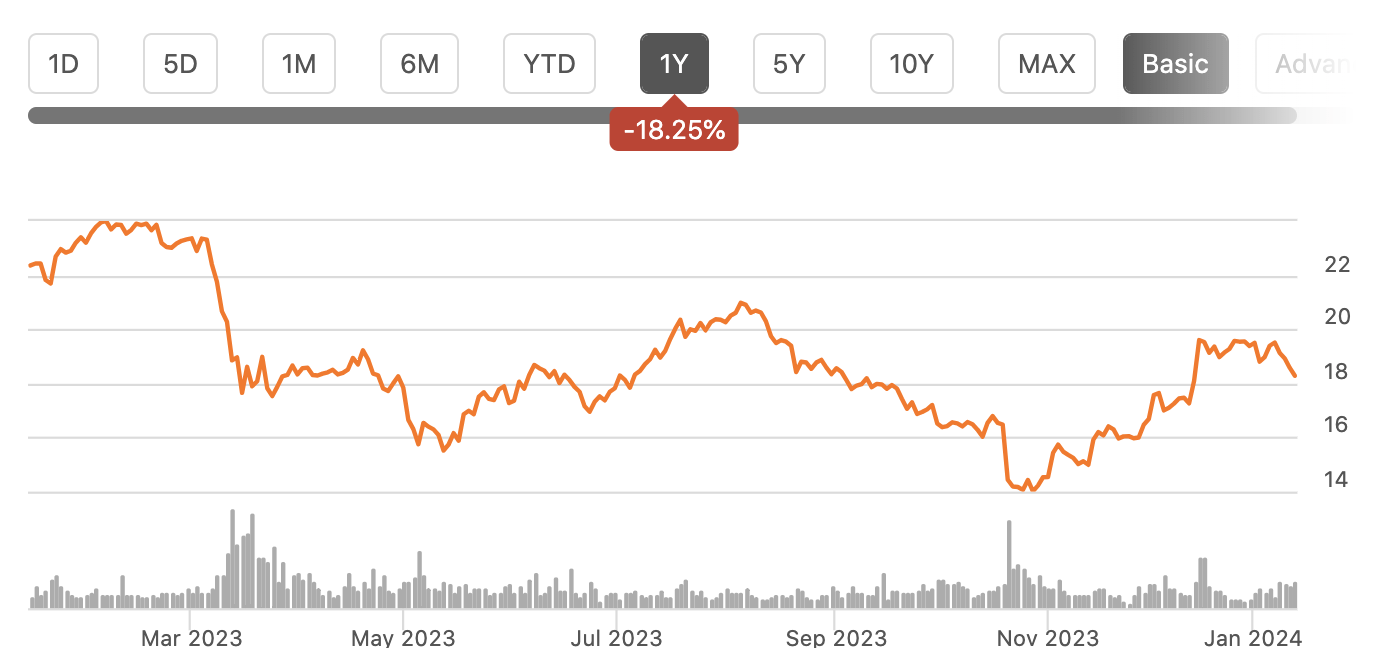

- Regions Financial has underperformed in the past year, losing about 18% of its value, though they have recovered from their October lows.

- The company's Q4 earnings report will be critical for its shares to continue rallying.

- Investors should focus on deposit costs and flows, as well as credit quality, to gauge the company's outlook.

- With RF shares near 10x earnings and a large earnings beat unlikely, I am cautious on shares given its deposit positioning.

Like many regional banks, Regions Financial ( RF ) has been a material underperformer over the past year, losing about 18% of its value. In the wake of several bank failures, increased deposit costs have squeezed Regions’ net interest margin. While shares have underperformed considerably, they have rallied substantially since the last earnings report.

{kind=link}

Seeking Alpha

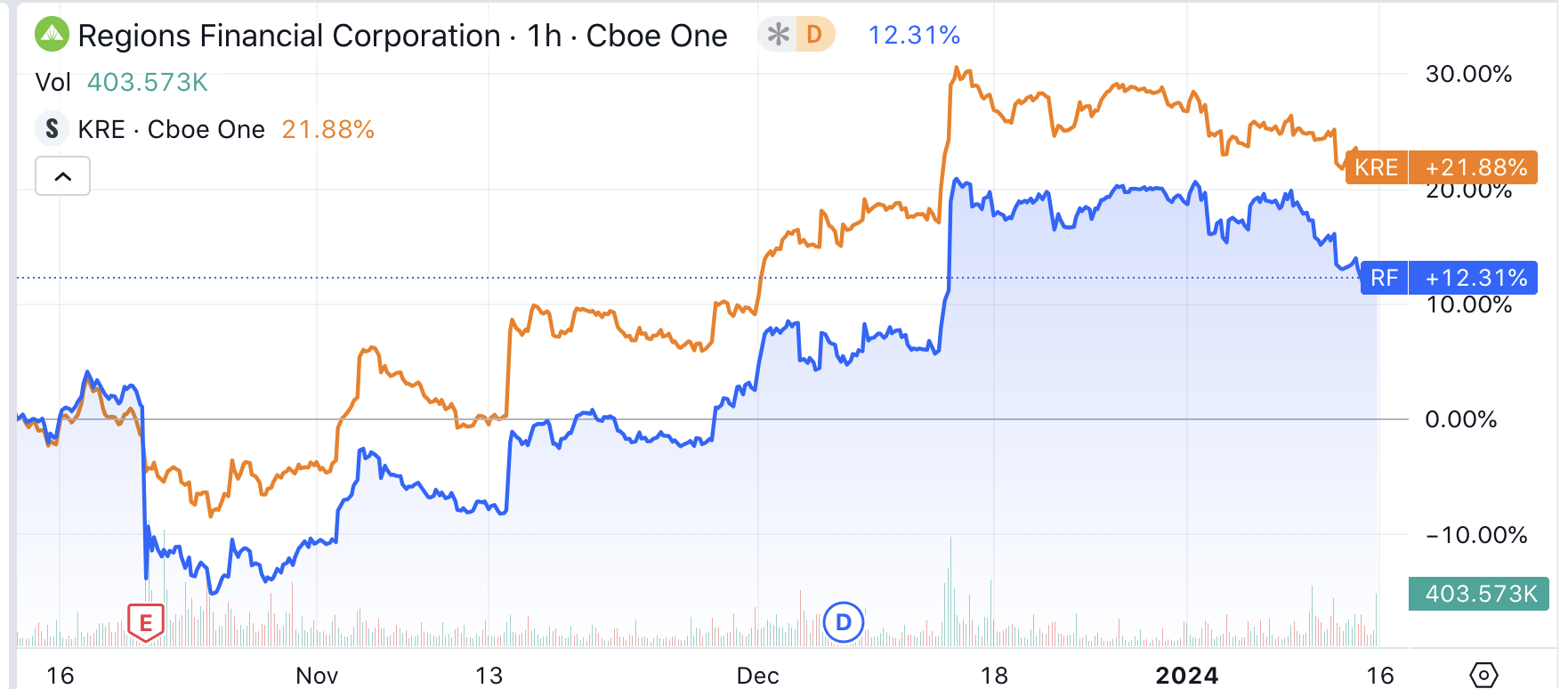

As you can see, RF has rallied over 12% in the past three months, more than recovering losses in the wake of its weak Q3 earnings report. Within my coverage of regional banks, I have rated RF a “ sell ” because of concerns over its deposit funding. As you can see below, since reporting earnings, shares have risen considerably, but this has largely been in keeping with the recovery in regional bank shares ( KRE ).

{kind=link}

Seeking Alpha

What to Expect from Regions Financial's Q4 Earnings Report

For shares to continue rallying, the company’s Q4 earnings report on Friday January 19 will be critical. In the company’s third quarter , Regions earned $0.49, missing consensus by $0.09, which is what sparked the sell-off. In Q4, consensus is for Regions to earn $0.42 on a GAAP basis and $0.48 on an adjusted basis. Regions expects to pay about $111 million in one-time FDIC assessments being charged to make the insurance fund whole from its cost of saving depositors in Silicon Valley Bank and First Republic Bank. This will be in GAAP numbers but not adjusted EPS, and there will be about a one-time impact of ~$0.08/share. This is slightly wider than the $0.06 GAAP-normalized EPS consensus, which could cause some volatility.

I expect investors to focus more on ex-FDIC earnings to better gauge Regions’ run-rate earnings power. Currently, in 2024, earnings are forecast to decline about 10% to $1.96. That implies the company continuing to earn about the $0.48 expected in Q4 2023. In order to do that, we are going to need to see improving net interest margins and no further material degradation in credit quality. There are several key items to watch in Q4 results.

Focus on Deposit Costs

One of the more distressing aspects of RF’s Q3 results was that the bank’s net interest margin compressed by 31bps sequentially to 3.73%, driving net interest income ((NII)) down by $91 million to $1.3 billion. Now, management is guiding to a 5% sequential decline in NII, with stabilization in H1 2024 and recovery thereafter. Assuming this 5% impact is realized, this will be a $0.04-$0.05 impact on adjusted EPS.

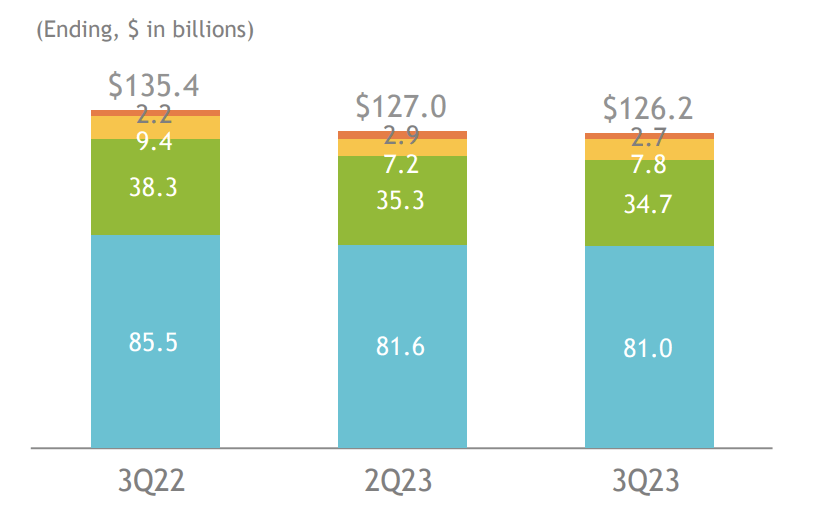

The primary culprit of weakening NIM has been increased competition for deposits. As you can see below, deposits are down by $9 billion over the past year. While the pace has slowed, they ended Q3 $800 million lower than in Q2. Deposits are expected to be “ stable to modestly lower ” in this report. I would view this guidance as implying $125.8-126.2 billion of deposits, and I would view a $500 million decline as concerning while growth would be a surprising positive.

In order for the company to grow loans, it needs deposits to stabilize. Indeed, we saw Regions pull back from lending with loans falling by $300 million in Q3 to end at $98.9 billion. Still, the bank’s loan to deposit ratio of 78% was up from 70% in Q3 2022. I would expect management to guide to slower loan growth than deposit growth to bring this ratio down and increase liquidity over 2024.

{kind=link}

Regions Financial

The other challenge for Regions is that its deposit mix has worsened—this is true of the industry. As you can see below, non-interest-bearing ((NIB)) deposits fell by $2.3 billion sequentially in Q3 while interest-bearing deposits rose by $1.6 billion. The entire YoY decline in deposits has been driven by NIBs, which are obviously a very attractive funding source.

{kind=link}

Regions Financial

These deposits are typically transactional (i.e. an account used to make payroll every two weeks). When rates were near-zero, there was little cost to maintaining extra cash in NIBs for customers. As rates have risen, clients have brought these balances down to invest elsewhere. Now, in practice, there should be a lower bound to these balances, as customers need sufficient cash to meet transactions. If we see NIBs decline by less than $1 billion, I would view this as a positive sign that RF is nearing its floor. If they continue to fall by over $2 billion, that would be a negative signal.

I will also be focused on the cost of interest-bearing deposits. In Q3, its average cost rose to 1.81%. I would expect a further increase in Q4 as rate increases instituted during Q3 impact an entire quarter’s results. With the Fed not raising rates, there should be less funding cost pressure. On the other hand, this rate is below many peer banks; for comparison, Capital One ( COF ) is paying 2.85%. I would expect Regions’ Q4 deposit costs to rise to about 1.95%, and an increase above 2% would be a more concerning sign that its deposit rates have not been competitive enough to retain customers.

A reason bank stocks have rallied over the past two months is the hope that several Federal Reserve rate cuts could allow banks’ funding costs to decline as they lower deposit rates in sympathy. Given the fact Regions is already paying relatively low rates, I am concerned it may not be able to cut rates as quickly as some are expecting, meaning its floating loans’ yields could come down while deposits stay relatively sticky, keeping NIM from expanding as some hope. Seeing how deposits perform in Q4 and what management expects their “beta” to be to lower rates will be critical to gauging this outlook.

Credit quality matters too

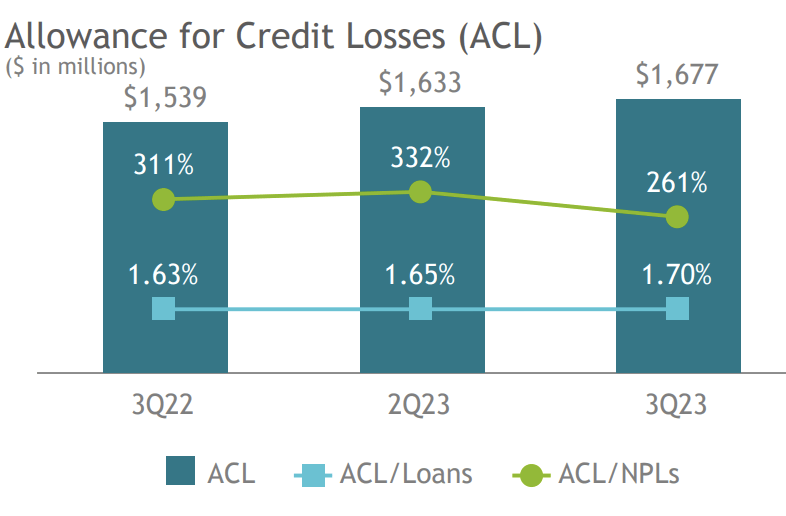

While NIM will be the primary focus on Q4 results, investors should also track Regions’ credit performance. Q3 was a unique quarter with weakness that has been accepted as “one-time.” It will be important to see validation of this in Friday’s results. I describe it this way because there were $145 million in provisions for credit losses in Q3, up 23% sequentially, adding $44 million to reserve. This increase was driven by a 30% jump in nonperforming loans to $632 million.

However, there was not a broad-based increase in delinquencies. Rather, there were three large loans that drove this increase, one large corporate and two senior housing entities. Chunky, one-time delinquencies can occur and distort results, rather than point to systemic problems with underwriting. To validate this, I would expect Regions to report a much smaller sequential increase in NPLs. If we see another $100+ million sequential increase, credit concerns will be more top of mind to investors. On balance, I do feel better about Regions’ credit positioning than interest rate exposure.

Even with the Q3 jump, I am comfortable with Regions’ current provisioning. Due to NPL growth, its NPL provisioning coverage fell from 332% to 261%--this is still above the 2.5x level I feel is important to maintain. As such, I would expect a smaller build in reserves in Q4 than Q3.I would also note that Regions has built reserves assuming a base case of unemployment ending 2024 at 4.3%. Given increased soft-landing hopes, this forecast seems reasonable if not conservative.

{kind=link}

Regions Financial

I would also pay attention to any commentary on its commercial real estate exposure. One area where we may see reserve growth is in office, where allowances are 3.1% of loans. Given the secular challenges facing the asset class, there is risk of further reserving over time here. However at 2% of total loans, Regions’ exposure should be manageable, and reserves are more likely to be a steady drip than a sudden large increase.

{kind=link}

Regions Financial

Capital and the Impact of lower rates

Finally, like many regional banks, Regions has paused its buybacks to build capital. In Q3, its common equity tier 1 ratio (CET1) was 10.3%, and management is aiming for 10+% capital in the near term. I would expect Q4 to be 10.3-10.4%. This is a strong level of capital, but beginning next year, RF will need to phase in its unrealized losses in accumulated other comprehensive income (AOCI) into its capital calculation. Including this $4.2 billion AOCI loss, Q3 CET was just 7.6%.

Now, management guided to this loss declining by about $900 million by the end of 2024 as bonds bought when rates were lower pull to par or mature. With the market now pricing in several rate cuts this year, these losses may shrink somewhat more quickly than expected. At its previous AOCI guidance, the AOCI capital headwind should shrink by 0.6% in 2024, bringing capital to 8.2% by year-end before retained earnings. Regions will likely want pro-forma capital above 8.5% before considering buybacks, which is more likely a 2025 than 2024 event, though there could be further clarity on the earnings call.

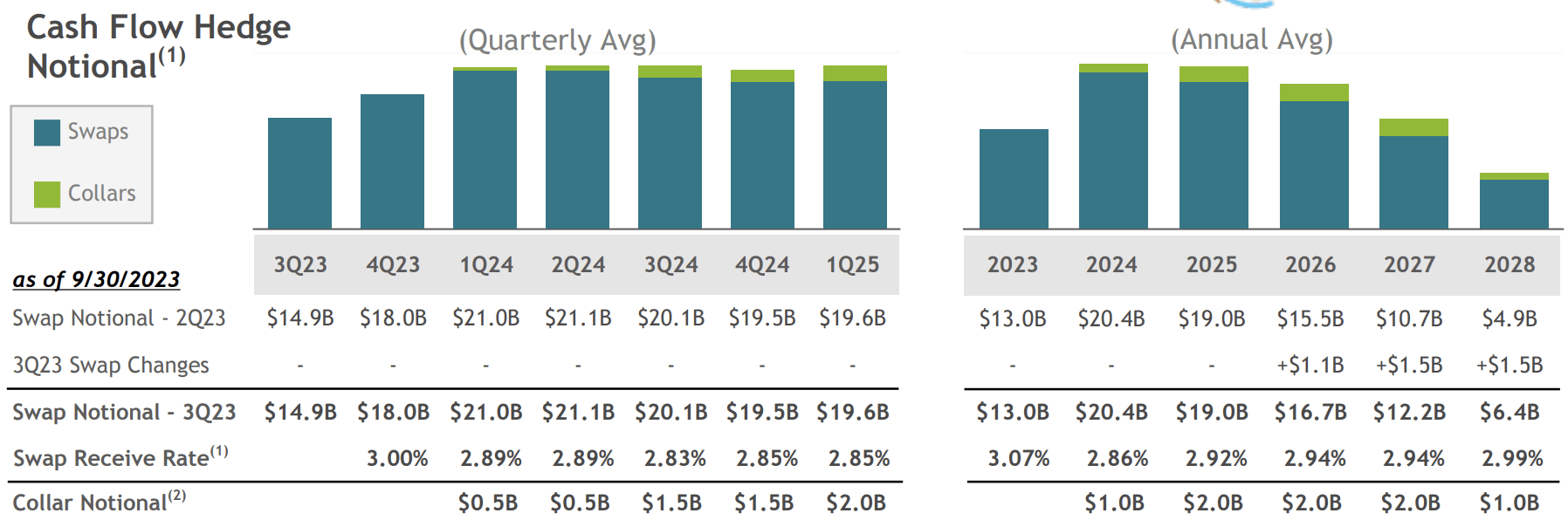

RF also has unrealized losses from swapping floating rate to fixed rate exposures at below 3%. These swaps are costly, but if the Fed does begin cutting rates, they do become less costly. It will take about 10 rate cuts to bring these into the money, which is unlikely before 2025, though the magnitude of their drag should decline.

{kind=link}

Regions Financial

Concluding thoughts

While I have generally been bullish on the regional bank sector over the past four months, rating firms like Capital One, Comerica ( CMA ), Citizens ( CFG ), Huntington Bank ( HBAN ), and several others as “buys,” I have viewed Regions more negatively because I have placed a significant emphasis on deposit stability. With about $0.05 of net interest headwinds, and $0.02 of reserving benefits vs Q3, I see a risk that normalized earnings come in at $0.46-0.47 vs the $0.48 consensus, though expense management could bridge this gap.

Just given its NIB deposit flows and where its deposit rates are, I do not foresee a significant beat, and so I remain cautious into Friday’s report particularly as shares have rallied so much alongside the sector whereas Regions’ fundamental performance has been disappointed relative to peers, in my view. I believe investors should continue to focus on deposit costs and flows. If we see another weak quarter, RF shares are likely to react poorly. Conversely, I will re-evaluate my view if we see a better than feared deposit outcome.

Given my expectation for NIM to decline in H1 and recover more slowly, I currently expect about $1.85-$1.95 in 2024 earnings, leaving RF at 9.6x times, with most regional banks struggling to get much past 10x earnings. Considering this, I remain cautious on shares into this critical earnings report, viewing RF as a sell relative to other regional banks, unless we see concrete evidence of improved deposit fundamentals.

For further details see:

Regions Financial Q4 Earnings Preview: Deposit Stabilization Is Essential