RGA - Reinsurance Group of America: Downgrade To Hold

2023-05-09 12:15:21 ET

Summary

- Back in December 2021, I rated RGA a Strong Buy.

- That rating has been vindicated with RGA providing strong returns from December 2021 to date.

- Today, the opportunity for future growth in the share price has decreased and investment portfolio values have declined significantly, with unrealized gains turning into unrealized losses.

- Lower investment portfolio value increases the risk of having to realize losses in the portfolio in the event of a period of higher levels of catastrophic events.

- Today, I downgrade RGA to a Hold.

Investment Thesis

I published my last article on Reinsurance Group Of America, Incorporated ( RGA ), " Reinsurance Group Of America: Look Beyond Covid For Strong Returns ", back on Dec. 7, 2021. My opening summary point was,

- Based on analysts' EPS estimates, returns for holding through the end of 2023 could average 20% to 30% per year.

That was going against the weight of opinion as shown in a copy of ratings summary at that time included in the abovementioned article,

SA Premium

Below is the summary provided by SA Premium for the December '21 article mentioned above as of May 8, 2023.

SA Premium

Clearly, my Strong Buy rating back then has been justified.

Below is the current ratings summary, available from SA Premium.

SA Premium

Once again, I find myself out of step with the general consensus.

My overriding concern with RGA is the impact of rising interest rates on the value of its investment portfolio. Revaluations, partly due to higher discount rates today, have caused large unrealized gains on the portfolio to change to unrealized losses, since my previous article. Net assets employed in the business have reduced from $13,345 million (end Q3 2021) at the time of my last article to $8,787 million at the end of March 2023. Portfolio assets could recover in value over time, but an increased level of claims in the short to medium term could cause those losses to be realized before there is an opportunity for that to occur. Another concern is the current share price level is associated with a current TTM March 2023 EPS of $19.13. Looking forward, analysts consensus EPS estimates are: FY 2023 $17.16, FY 2024 $17.86, and FY 2025 $19.16. With FY 2025 consensus EPS estimates similar to current TTM March 2023, the only way the share price can grow through 2025 is through multiple expansions. Without multiple expansions, the share price in 2025 will be similar to the current share price. In that event, total return would be limited to the dividend yield, presently 2.11%. There is every possibility of multiple expansions through the end of 2025. I calculate a historical median P/E multiple for RGA of 12.75, well above the current multiple of 7.75. At that multiple, and if analysts consensus EPS estimate for 2025 is achieved, total return of over 20% per year is indicated. However, RGA attracts a relatively low multiple for good reason. There is portfolio risk and catastrophic event risk. RGA appears to be very competent in managing to ameliorate these risks. But the possibility of a recession and unforeseen climate change events have the potential to affect both earnings and sentiment, which in turn can affect multiples. While I believe it is a soundly managed business, for the reasons outlined above, I will at this point in time downgrade RGA to a Hold. A more detailed financial analysis follows below.

A More Detailed Financial Analysis

Just because the operations of a listed business perform well does not mean buying shares in that business at any given point in time will result in that investment performing well. My main aim in this more detailed financial analysis is to analyze financial data with regard to -

Total Return, Dividends, and Share Price

The only way an investor can achieve a positive return on an investment in shares is through receipt of dividends and/or an increase in the share price above the buy price. It follows what really matters in share value assessment is the expected price at which a buyer will be able to exit shares, and expected cash flow from dividends.

Changes in Share Price

From a purely mathematical/statistical point of view, changes in share price are driven by increases or decreases in EPS and changes in P/E ratio. Changes in P/E ratio are driven by investor sentiment toward the stock. Investor sentiment can be influenced by many factors, not necessarily stock-specific.

"Equity Bucket"

Earnings are tipped into the "Equity Bucket" for the benefit of shareholders. It's prudent to check whether distributions out of and other reductions in the "Equity Bucket" balance are benefiting shareholders.

Summarized in Tables 1, 2, and 3 below are the results of compiling and analyzing financial data with the foregoing in mind.

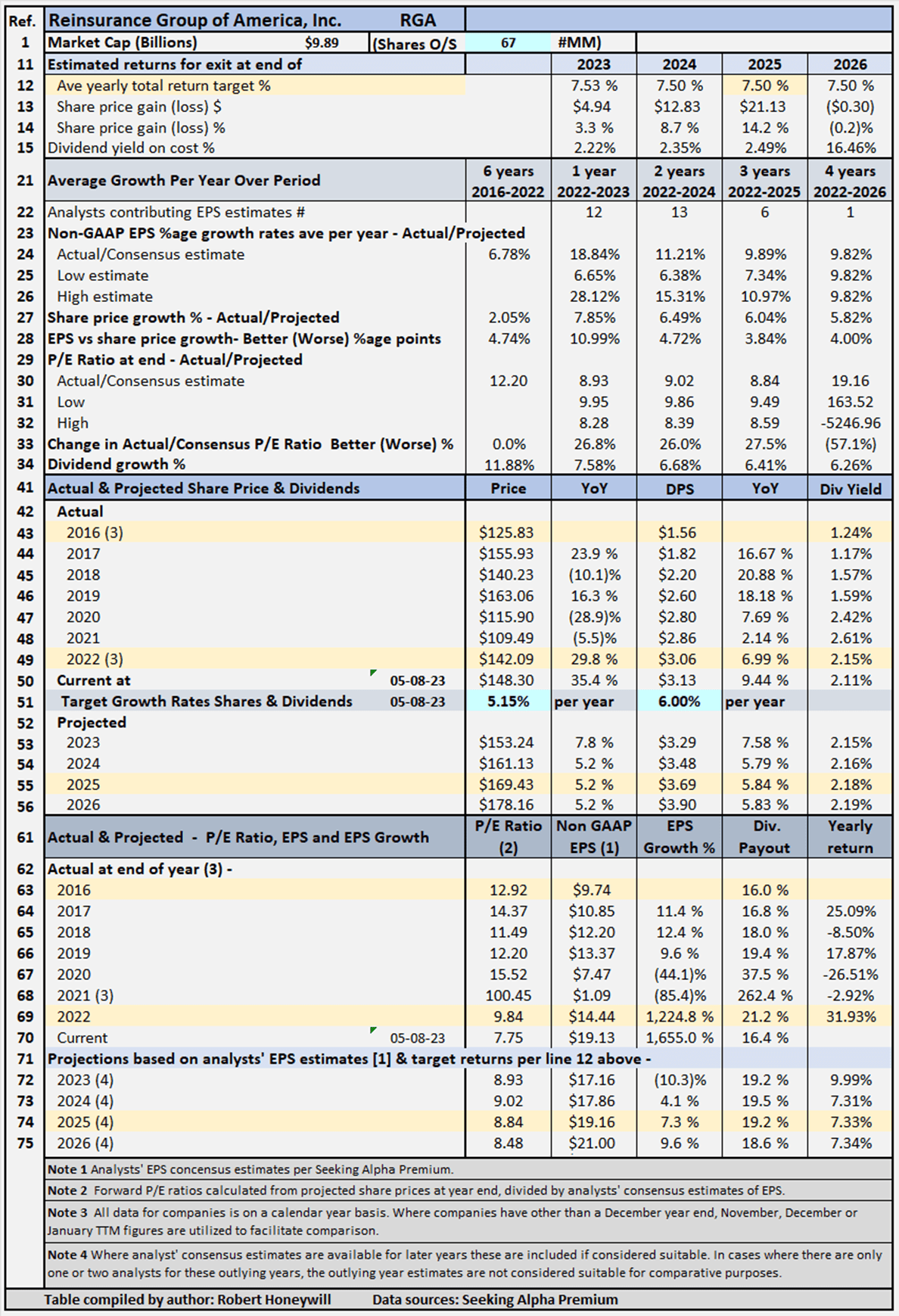

Table 1 - Detailed Financial History And Projections

{kind=link}

Table 1 analyses historical data from 2016 to 2022, including share prices, P/E ratios, EPS and DPS, and EPS and DPS growth rates. For the six years 2016 to 2022, RGA has grown both EPS and DPS at an average yearly rate of 6.78%. Average yearly share price growth of 2.05% is below the EPS growth rate of 6.78% due to P/E multiple contractions from 12.92 at the end of 2016 to 9.84 at the end of 2022.

The table also includes estimates out to 2026 for share prices, P/E ratios, EPS and DPS, and EPS and DPS growth rates (note - while estimates are shown for analysts' EPS estimates out to 2023 through 2026 where available, estimates do tend to become less reliable the further out the estimates go. These estimates are generally only considered sufficiently reliable if there are at least three analysts' contributing estimates for the year in question). Table 1 allows modeling for target total rates of return. In the case shown above, the target set for a total rate of return is 7.5% per year through the end of 2025 (see line 12), based on buying at the May 8, 2023, closing share price level. As noted above, estimates become less reliable in the later years. In the case of RGA, I have decided to input a target return based on 2025 year, which has EPS estimates from six analysts. The table shows that to achieve the 7.5% return, the required average yearly share price growth rate from May 8, 2023, through December 31, 2025, is 5.15% (line 51). Dividends, including estimated dividend increases, account for the balance of the target 7.5% total return.

RGA's Projected Returns Based On Selected Historical P/E Ratios Through End Of 2025

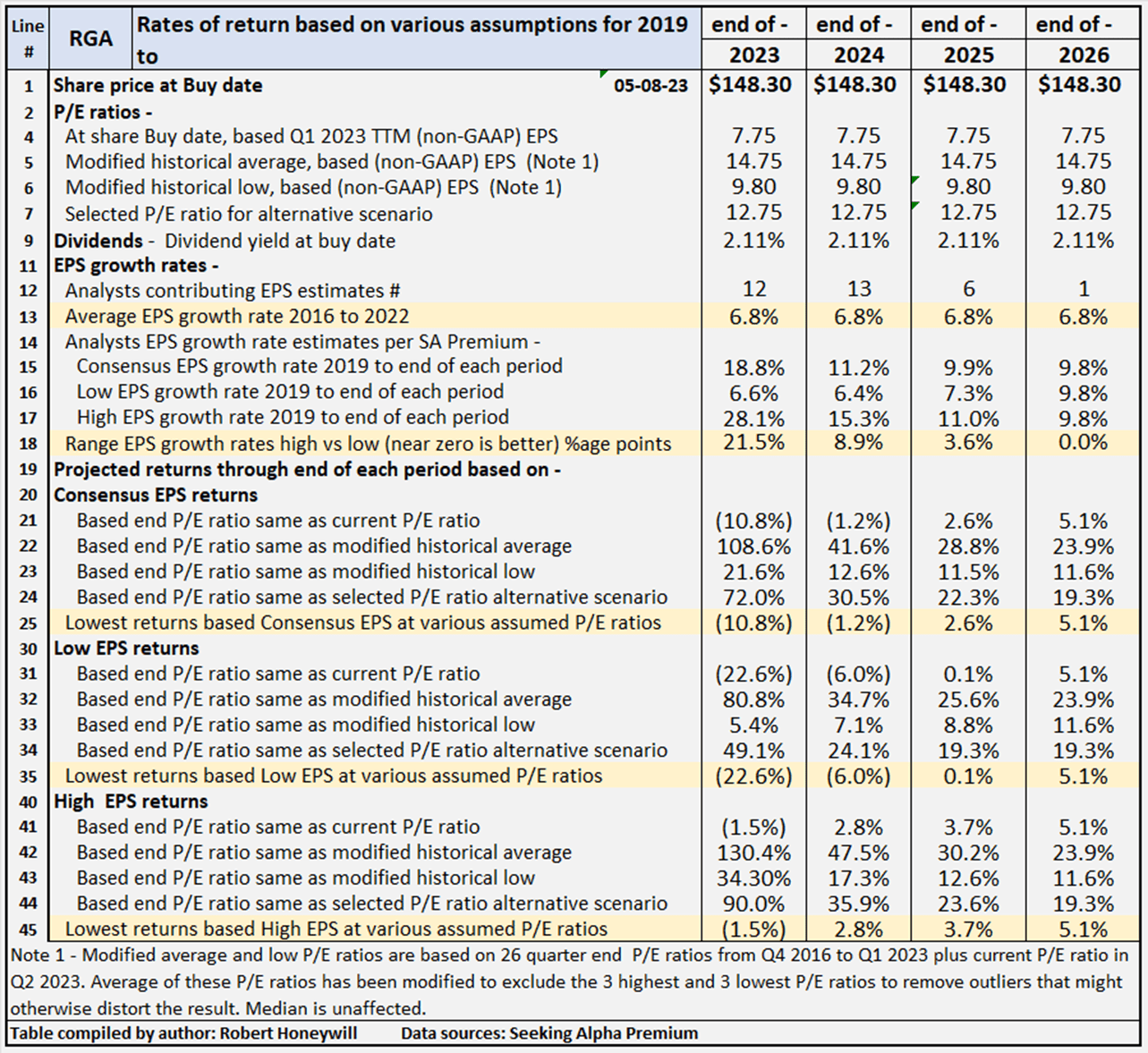

Table 2 below provides scenarios projecting potential returns based on select historical P/E ratios and analysts' consensus, low, and high EPS estimates per Seeking Alpha Premium through the end of 2026.

Table 2 - Summary of relevant projections RGA

{kind=link}

Table 2 provides comparative data for buying at the closing share price on May 8, 2023, and holding through the end of 2026. There's a total of twelve valuation scenarios for each year, comprised of three EPS estimates (SA Premium analysts' consensus, low, and high) across four different P/E ratio estimates, based on historical data. RGA's P/E ratio is presently 7.75, based on TTM Q1 2023 non-GAAP EPS. For RGA, the present P/E ratio is below the modified average of historical P/E ratios over the last six years. Table 2 shows potential returns from an investment in shares of the company at a range of historical level P/E ratios. This analysis, from hereon, assumes an investor buying RGA shares today would be prepared to hold through the end of 2025, if necessary, to achieve their return objectives (2026 year is not considered as there is only one analyst providing an estimate). Comments on contents of Table 3, for the period to 2025 column follow.

Consensus, low, and high EPS estimates

All EPS estimates are based on analysts' consensus, low, and high estimates per SA Premium. This is designed to provide a range of valuation estimates ranging from "low" to "most likely" to "high" based on analysts' assessments. I could generate my own estimates, but these would likely fall within the same range and would not add to the value of the exercise. This is particularly so in respect of well-established businesses such as RGA. I believe the "low" estimates should be considered important. It's prudent to manage risk by knowing the potential worst-case scenarios from whatever cause.

Alternative P/E ratios utilized in scenarios

- The current P/E ratio . This scenario provides a range of potential returns if the P/E ratio remained at the current level through the end of 2025.

- A modified average P/E ratio based on 26 quarter-end P/E ratios from Q4 2016 to Q1 2023 plus current P/E ratio in Q2 2023. The average of these P/E ratios has been modified to exclude the three highest and three lowest P/E ratios to remove outliers that might otherwise distort the result.

- A modified historical low P/E ratio calculated using the same data set used for calculating the modified average P/E ratio, with the three highest and lowest P/E ratios excluded. In this instance, the current P/E ratio of 7.75 is one of the three excluded "outliers", so the modified low P/E ratio of 9.80 is greater than the current multiple.

- A selected P/E ratio to provide an alternative P/E scenario to take into account other factors that might be relevant to assessing potential returns. For example, if analysts' forward estimates reflected EPS growth rates significantly higher or lower than historical EPS growth rates. In such cases, the forward P/E ratio might be expected to trend higher or lower than the historical average. In the case of RGA, the median P/E ratio is 12.75, which falls between the low of 9.80 and the average of 14.75. This has been selected as suitable for an additional alternative scenario.

Reliability of EPS estimates (line 18)

Line 18 shows the range between high and low EPS estimates. The wider the range, the greater disagreement there is between the most optimistic and the most pessimistic analysts, which tends to suggest greater uncertainty in the estimates. There are six analysts covering RGA through the end of 2025. In my experience, a range of 3.6% difference in EPS growth estimates among analysts is not overly high, suggesting some degree of certainty, and thus a degree of reliability.

Projected returns per Table 2 above (lines 20 to 45)

Lines 25, 35, and 45 show if RGA's P/E multiple were to remain at the current level of 7.75, returns of 0.1% to 3.7% could be expected through the end of 2025, based on the range of analysts' EPS estimates. The 0.1% is based on analysts' low estimates and the 3.7% on their high estimates, with a consensus of 2.6%. On the other hand, if the multiple reverted to the historical average of 14.75, almost double the current level of 7.75, returns of 25.6% to 30.2% are indicated, with a consensus of 28.8%. If the P/E ratio should increase to the level of the modified low of 9.80, returns of 8.8% to 12.6% are indicated, with a consensus of 11.5%.

Checking RGA's "Equity Bucket"

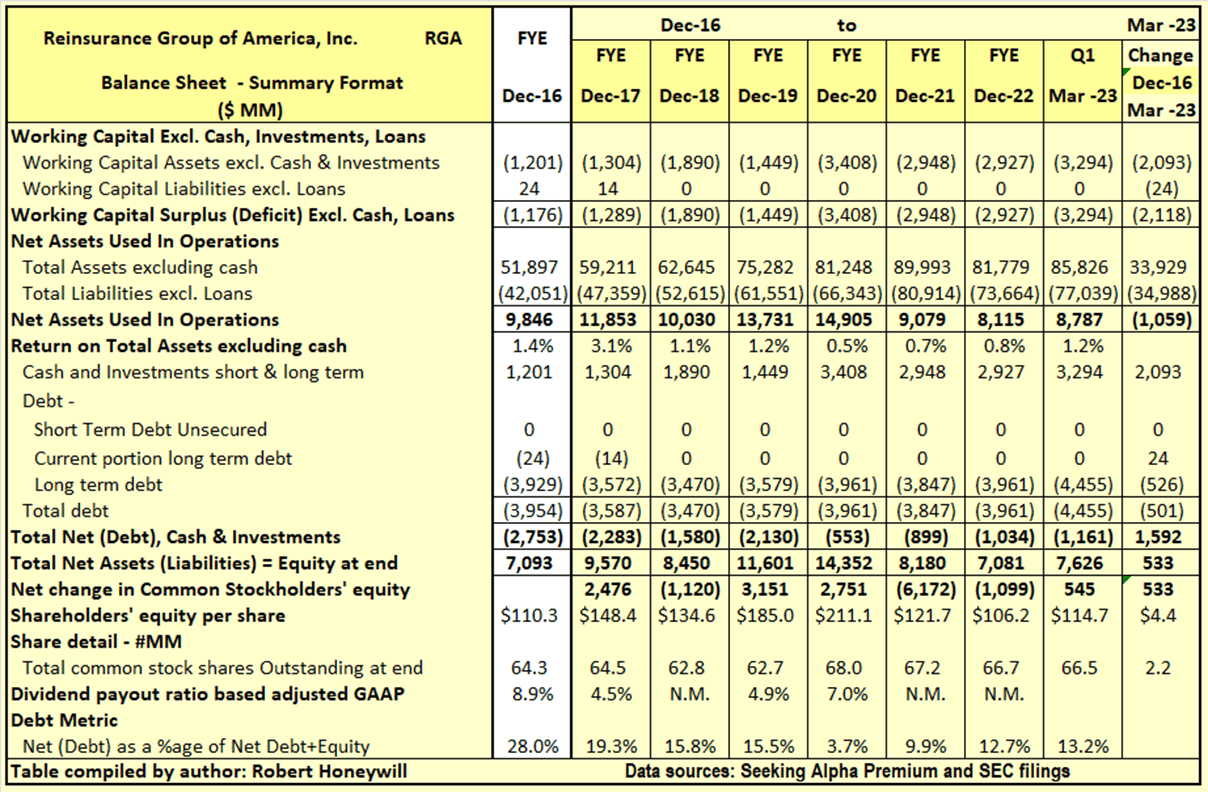

Table 3.1 RGA Balance Sheet - Summary Format

{kind=link}

Over the 6.25 years end of 2016 to the end of Q1-2023, RGA's Net Assets Used In Operations decreased by $1,059 million, and debt net of cash decreased by $1,592 million, resulting in an increase of $533 million in shareholders' equity. Net debt as a percentage of net debt plus equity decreased from 28.0% at the end of 2016 to 13.2% at the end of Q3-2021. Outstanding shares increased by 2.2 million from 64.3 million to 66.5 million over the period due to shares issued to raise capital for general operating expenses and for stock compensation, partially offset by share repurchases. The $533 million increase in shareholders' equity over the last 6.25 years is analyzed in Table 3.2 below.

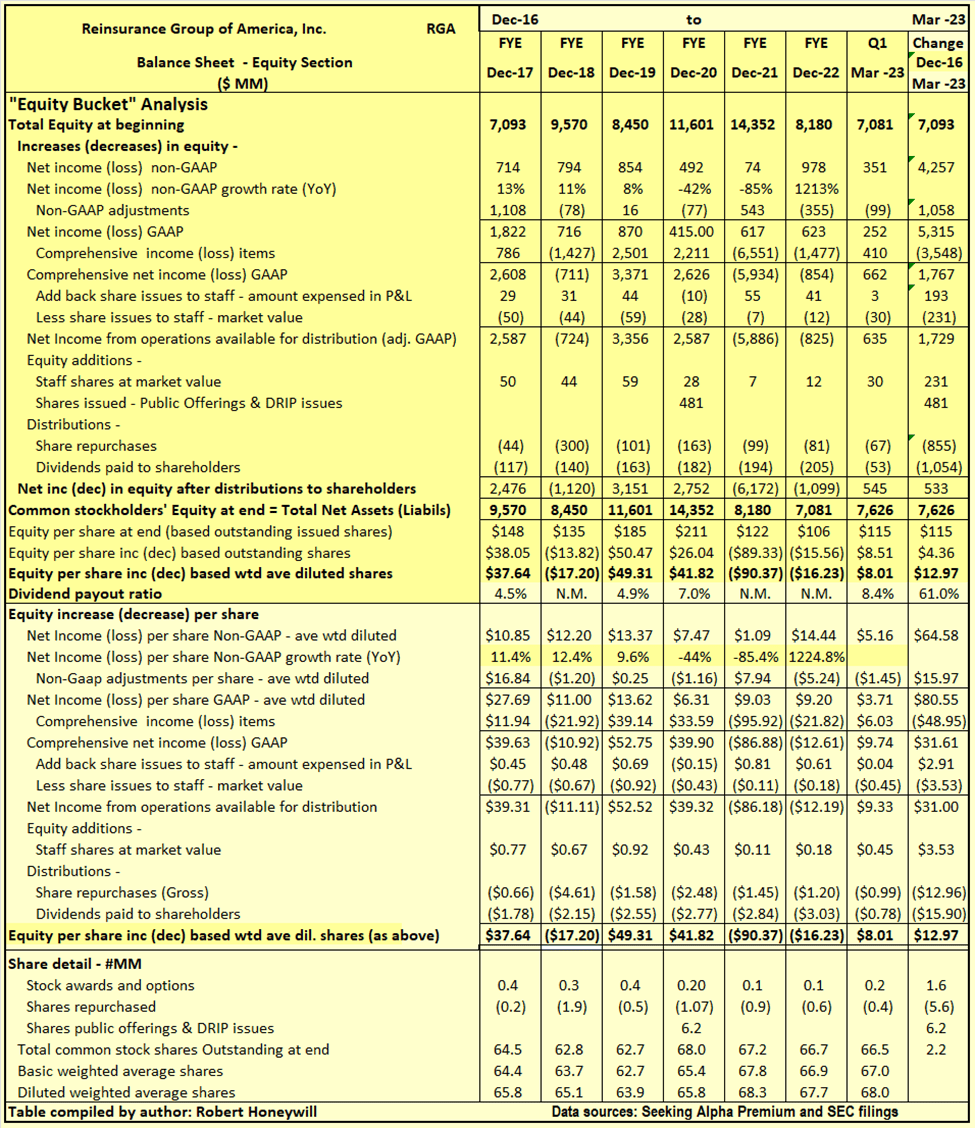

Table 3.2 RGA Balance Sheet - Equity Section

{kind=link}

I often find companies report earnings that should flow into and increase shareholders' equity. But often the increase in shareholders' equity does not materialize. Also, there can be distributions out of equity that do not benefit shareholders. Hence, the term "leaky equity bucket." I look for evidence of this in my analysis of changes in shareholders' equity.

Explanatory comments on Table 5.2 for the period end FY-2016 to end Q1-2023.

- Reported net income (non-GAAP) over the 6.25-year period totals $4,257 million, equivalent to diluted net income per share of $64.58.

- Over the 6.25-year period, the non-GAAP net income excludes a significant $1,058 million of net income items, which are included in arriving at GAAP net income.

- GAAP net income for the 6.25 years of $5,315 million is arrived at before accounting for $3,548 million in accumulated comprehensive losses. The magnitude of these items relates largely to the accounting requirements for insurance companies.

- Amount taken up in equity to account for shares issued to staff over the 6.25 years is $193 million. This compares to an estimated market value of $231 million at the time of issue of these shares. The difference of $38 million is not material in the context of reported non-GAAP earnings of $4,257 million.

- By the time we take the above-mentioned items into account, we find, over the 6.25-year period, the reported non-GAAP EPS of $64.58 ($4,257 million) has increased to $31.00 ($1,729 million) increase in funds from operations available for distribution to shareholders.

- Distributions by way of dividends of $1,054 million, and share repurchases of $855 million totaled $1,909 reducing the $1,729 million increase in equity from operations to a deficit of $180 million.

- Equity issues to staff of $231 million, and share issues of $481 million more than offset the $180 million deficit from operations, resulting in the $533 million increase in shareholders' funds per Table 3.1 above.

RGA: Summary and Conclusions

RGA is obviously a well-run business, skilled at managing risk. But taking on risk is what the business is about. However well managed, it is always possible for a succession of catastrophic events to occur. In addition, earnings tend to be lumpy. This is evidenced by the fact that the current TTM March 2023 EPS is not expected to be matched again until FY 2025. I perceive risks for the investment portfolio from rising interest rates and the possibility of a recession. Meeting claims out of a portfolio which has unrealized losses, locks in those losses. Those risks together with high numbers of catastrophic events could put downward pressure on both earnings and the P/E multiple, magnifying the pressure on the share price.

For further details see:

Reinsurance Group of America: Downgrade To Hold