RZB - Reinsurance Group of America: I'm Extending My Targets For Additional Upside

Summary

- RGA has generated 4.91% alpha since October 2022, when I initiated coverage of the stock. It has hit my original target price.

- I am extending my targets to capture an additional 22% upside due to new bullish drivers that became apparent after the Q4 FY22 results.

- APAC is set to be a meaningful growth driver, driven partly by a rebound in Chinese demand.

- I contend that the Q4 FY22 earnings miss is nothing to worry about as odds are it is a temporary blip. Premium growth is more important and that is trending well.

- There continue to be opportunities for positive surprises in investment yields as the rates environment continues to be hawkish.

Thesis Update

I previously shared my analysis on Reinsurance Group of America ( RGA ) in early October 2022, rating the stock a 'Strong Buy' due to a favorable growth outlook, improving operational metrics and opportunities for upside potential driven by interest rate hikes. So far, the thesis has played out well and the stock has generated 4.91% of alpha over the S&P 500 ( SPY ) ( SPX ) in almost 5 months.

Although my initial target price for RGA has been hit, the Q4 FY22 earnings call has given me more reasons to continue my bullish outlook as I identify APAC and China as key incremental growth levers, look past a temporary earnings disappointment, and recognize room for further positive surprises in investment income.

Premiums Growth Analysis

{kind=link}

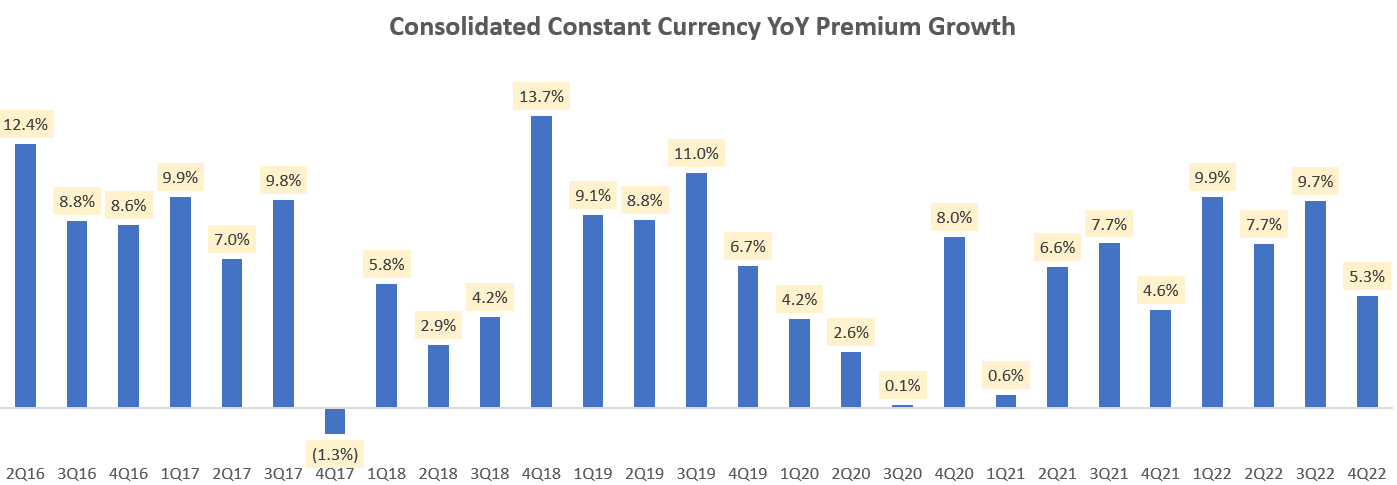

Consolidated Constant Currency YoY Premium Growth (Company Filings, Author's Analysis)

Premium growth continues to be quite healthy on a constant currency basis (which better reflects the health of operating results). Note that the growth drop from 9.7% YoY to 5.3% YoY in the last quarter is partly due to a high-base effect of APAC operations in Q4 FY21:

APAC net premiums (Company Filings, Author's Analysis)

The steep drop in 2022 was due to COVID-related restrictions that curbed new business activity. However, there are signs that a growth recovery is underway in the APAC region:

APAC expected to be a premiums growth leader

CEO Anna Manning remarked in the Q4 FY22 earnings call that:

Most, if not all, those restrictions have now been lifted, so we see momentum really picking up.

Connecting the dots together, I assume she is referring to Chinese operations, as the country has lifted its strict COVID restrictions in December 2022. Going forward, management expects to see Asia grow premiums at above company rates.

This marks a change from the growth pattern seen in the prior 3 years, where APAC was the growth laggard with a 3.1% CAGR:

3-yr CAGR of Net Premiums (Company Filings, Author's Analysis)

I believe RGA's Chinese operations will have a meaningful role in contributing to incremental growth in the APAC region since will largely be fueled by RGA's Chinese operations, where the company has established relationships with over 60 Chinese life insurance companies. According to GlobalData, Chinese life insurance industry is expected to grow at a CAGR of 6.1% over the next 4 years. I anticipate this growth accretion to not come at the expense of other regions, leading to an overall uptick in net premiums written over the medium to long term.

Importantly, there is evidence of growth traction already building up in the background; the APAC region makes up 22.2% of overall net written premiums in Q4 FY22 and has contributed toward a more than 20% mix to overall net premiums written for the past 24 quarters. On the other hand, APAC's mix of active policies stands at 15.4%. As written premiums lead active policies, this flashes early signs of the active policy mix being weighted more towards APAC over upcoming quarters.

Operating Margins Analysis

{kind=link}

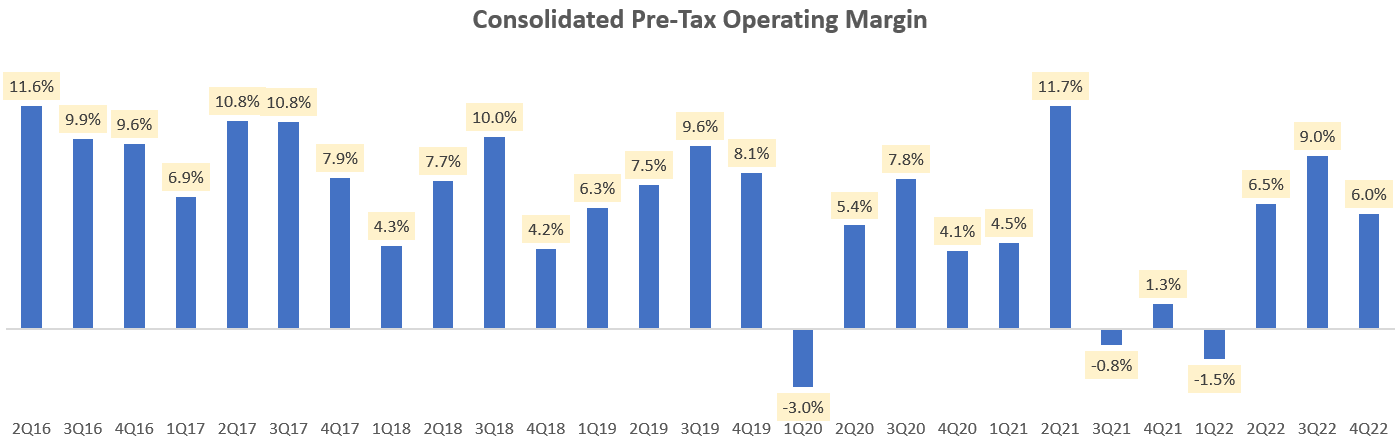

Consolidated Pre-Tax Operating Margin (Company Filings, Author's Analysis)

In Q4 FY22, company-wide pre-tax operating margins witnessed a fall to 6.1% from 9.4% in the prior quarter. This was mostly due to the US & LATAM region, which makes up 46% of total pre-tax operating income:

{kind=link}

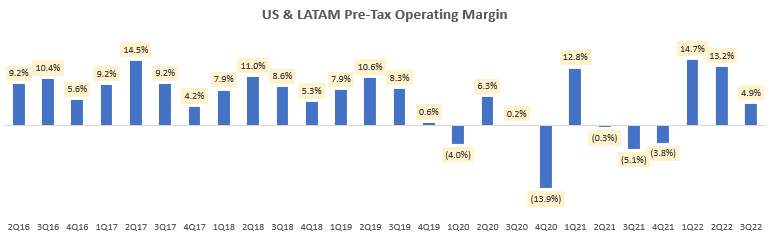

US & LATAM Pre-Tax Operating Margin (Company Filings, Author's Analysis)

This region's pre-tax operating margins dropped from 15.2% to 4.9% due to due to higher individual mortality claims related to COVID and an early flu-season impact. RGA's Chief Risk Officer noted that:

...influenza cases peaked about 8 to 10 weeks earlier than historic norms, which we believe shifted the majority of deaths into the fourth quarter.

For this reason, I believe the margin miss is not structural. Hence, I pay more attention to the positive sign that pre-tax operating margins in RGA's main US & LATAM region before this impacted quarter is printing more than 12%; a feat that the company has not achieved since Q2 FY17 . I will be monitoring these margin levels for sustainability at above 10% in the quarters ahead.

Improved interest rate environment continues to be a robust tailwind

In my first article on RGA, I had identified upside potential the investment yields by virtue of a higher interest rate environment:

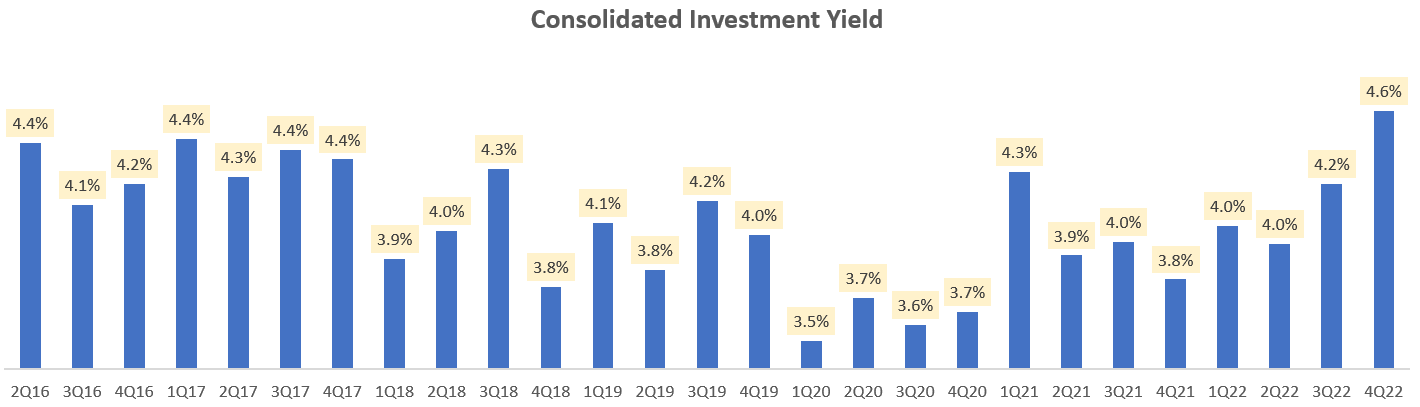

RGA can benefit from a higher nominal spread above inflation. This is likely to push its investment yields higher, possibly to 6-year highs towards 5.0%.

This seems to be playing out as anticipated as Q4 FY22 investment yields shot up 4.6%; a 32-quarter high:

{kind=link}

Consolidated Investment Yield (Company Filings, Author's Analysis)

Currently, net investment income makes up 316% of the company's pre-tax operating earnings. And I believe there are further upside risks to the investment yields since I anticipate the Fed to continue hiking rates especially after the meaningful 30bps positive surprise on January's producer price inflation ((PPI)) figures.

My article on Sanmina ( SANM ) explores my view on inflation expectations in more depth.

Performance Review and Valuation

Since early October when I last covered RGA, consensus estimates for FY23 earnings have risen 22% from $13.19 to $16.00 . However, the 1-yr forward PE multiple has only gone up 5.1% to 9.3x from 8.9x.

My original target of $147.12 has been hit as the current share price stands at $149.06. We have hunted down 4.91% of alpha over the S&P 500 from a total shareholder perspective over almost 5 months.

Now, I am revising my targets to reflect the elevated earnings expectations for RGA stock. Still applying a 11.2x PE multiple like last time to FY23's EPS expectation of $16.00, I derive an implied fair value of $179.2, which represents a further 22% upside.

Takeaway & Positioning

RGA has already hit my target price and generated 4.91% alpha over the S&P500 since my initial coverage of it in October 2022. Yet, I am extending my targets to capture an additional 22% upside.

This is due to my optimism on the company's APAC growth prospects, fueled by a Chinese demand rebound. I believe the negative earnings surprise is nothing to cause any worry as it seems to be a temporary phenomenon due to an early flu season. Instead, I have my eye on premiums growth, which is trending well. I believe this is the more controllable business driver. Lastly, I recognize continued room for upside surprises on investment yields as I believe further interest rate hikes are on the horizon.

For further details see:

Reinsurance Group of America: I'm Extending My Targets For Additional Upside