RGA - Reinsurance Group Of American - Sup-Par Performance Since March BUY

2023-10-23 18:58:33 ET

Summary

- Reinsurance Group of America (RGA) has underperformed indices and portfolios, but still has upside potential.

- RGA's 2Q23 results show improvements in earnings, new business, and dividend growth.

- The company's long-term trends are solid, and analysts estimate a potential upside for RGA.

Dear readers/subscribers,

In this article, I'll be providing an update on Reinsurance Group of America ( RGA ). The company has been a sup-par performer since my last article about 6-7 months ago. You can find this coverage here. In this article, I held a positive thesis on the company, considering it a "BUY" with an upside to a fair valuation - but not the greatest opportunity on the market today.

By sup-par performance, I mean that it has actually underperformed both most indices and my own portfolio performance in the meantime. It actually tumbled in conjunction with the regional banking crisis and has only slightly recovered since, trading sideways for some time.

This is one of those companies, in my experience, that a lot of people look at, but few people actually seem to invest in. RGA can show volatility - and to be clear to you, from a yield and RoR perspective on a historical basis, many reinsurers and insurers are more attractive than RGA. But this hasn't always been the case, and I'm convinced that RGA still has an upside to deliver here.

Let's look at what this company has been doing and what we can expect on a forward basis.

Reinsurance Group of America - A dud since the 54% RoR back in March of 2023.

Last I wrote about RGA, it provided outperformance in a very volatile environment. Being a Fortune 500 reinsurer working with assets of over $3T, the company automatically earns a place on my watchlist. It's one of the largest life/health reinsurers on the planet. Aside from working with assets of over $3T, it also directly holds dozens of billions of assets.

Unlike many of the "dragons" in this industry like Munich RE ( OTCPK:MURGY ), this company does not have a century-old history. It's around 40 years old, and that history includes Metlife ( MET ). How Reinsurance works and how RGA makes money is in turn described in my initial article on the company. I suggest you read it here to get an overview of facultative, reinsurance/other types of reinsurance so that you at least know the basics of what you're potentially getting into. It's a difficult field to understand unless you work in it full-time, but you should never go into anything unless you at least know the basics.

Reinsurance businesses need even better analytics and data processing capabilities than standard insurance firms - because Reinsurers work with, as the name suggests, insurers. History has proven that RGA's claims of understanding morbidity and shared medical underwriting knowledge are true - and the company usually outperforms on a longer basis. The company's claims are backed up by a long history of outperformance, and the latest results more or less confirm this. If you need further confirmation as to the company's expertise, all you need to is look at what the rating companies say about RGA. As late as april of 2023, Fitch had this to say about RGA.

Fitch Ratings considers Reinsurance Group of America, Incorporated’s ( RGA ) company profile to be “favorable,” compared with all other reinsurance organizations globally. This ranking aligns with Fitch’s ‘aa–’ credit factor score and has a higher influence on RGA’s rating. This company profile score is improved from “moderate” (‘a+’ credit factor score) as RGA weathered the challenges of the coronavirus pandemic and continued to maintain its leading position in the U.S. and Canadian ordinary life recurring premium markets, with a focus on mortality risk, and ranks among the top five global life and health reinsurance companies.

(Source: Fitch Ratings )

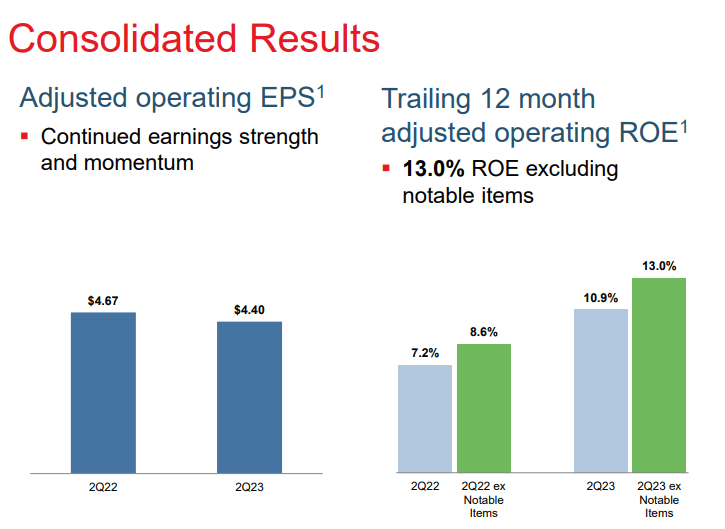

2Q23 results from August are still the latest set that we have to look at. The 2Q23 results come in with $4.4 of adjusted operating income per share, which in turn came from good earnings across almost all regions and business lines. The decline in US morbidity as we're moving out of COVID-19 trends obviously has improvements in results as a consequence for a reinsurer like RGA. The company has also been able to report significant improvements in new business, which at this time is growing organically. The company is also deploying capital to in-force and other transactions, while increasing the company dividend over 6%, meaning the current yield for RGA comes to just south of 2.3%. This is one of the lowest yields in the entire reinsurance sector, and given that most of these companies are A-rated, like RGA, the company safety isn't really something that I see as an excuse.

The fact is, if RGA had a better yield and better stability over time and not the reliance on Life/health that sent it spiraling during COVID-19, I probably would have invested as much into the company as I did into MURGY back when we saw COVID-19. Munich Re as an investment turned out extremely favorably for me. RGA did as well - at least during the short term, meaning from my initial buy up until early 2023 -, but unlike MURGY I haven't sold my investment and reinvested it, and the company has unfortunately been trading sideways for over half a year.

On the positive side, the results for the company are really quite good.

{kind=link}

RGA IR (RGA IR)

RGA is able to report traditional premium growth at over 5% at constant currency levels, though most of this comes from growth in Global Financial solutions - because premium volumes in Canada, and EMEA are down while APAC is up less than that at non-constant currency levels. FX is having an impact on the latest set of results.

Investment yields are also narrowing. What was a 4.4-4.45% yield in late 2022 and was up to 4.7% in 1Q23, is down to 4.42% in 2Q23. On the other hand, new money rates are up a full 100 bps and more in around a year, reflecting better market yields and overall returns on money in both securities and private assets.

RGA continues to hold mostly investment-grade bonds. Its exposure to mortgage loans is less than 10%, and high-yield bonds is less than 4%. Out of its fixed investments, over 94% are IG-rated, and over 63% are either A, AA or AAA. RGA continues to be very conservatively structured. In terms of its CML sector, the company has no traditional malls in its retail, and what office properties it has are in suburban locations with geographical diversification and an average loan size of around $11M.

Liquidity never has been as long as I've reviewed it, nor seem to be now, a problem for RGA. It has $2.6B in cash and equivalents with access to $850M from syndicated credit facilities and other sources.

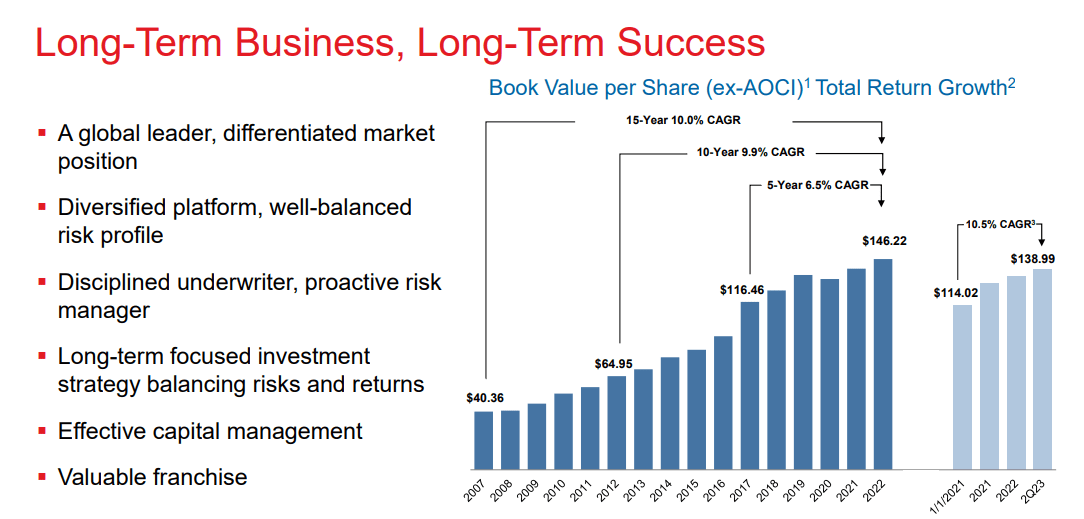

The company's long-term trends are solid, with the clear exception of the COVID-19 period.

{kind=link}

RGA IR (RGA IR)

Despite a lackluster performance over the past 6 or so months if we work from the price level at which I last wrote on RGA, I actually believe the company has ways to go from here - and the estimates for the business confirm my upside and expectation. Some headwinds in US mortality remain - but my overall long-term thesis and case for the company haven't materially changed in the last few months.

I still believe that the unwinding of COVID-19 impacts will result in a significant improvement of GAAP EPS over time - as well as adjusted operating income improvements. Dividend improvements are likely to come along as well.

The current picture of the company is of one trading significantly below where historical valuation patterns imply the company should be trading long-term. However, we do know that the company can also stay there for years. During the GFC, the company troughed in -08 and did not really recover significantly until 2012-2013. But when it did recover, it resulted in investor ROR of more than 25% annualized even until 2015, and well more until the pre-COVID-19 levels.

Given that the company is backed by the assets and operations of one of the largest reinsurance businesses in the entire world, I remain favorably inclined to this business and to this company as an investment.

The following valuation trends are likely here, as I see them, and the following returns are likely in the long term, which is also why I remain long RGA.

Reinsurance Group of America - The upside remains.

Just as before, my conviction for RGA is high, but I do believe the company is substantially less attractive than it once was. The yield we're seeing here is simply only somewhat good enough - and that's before we're even comparing it to any other investment, not just RGA's own historical yield.

My previous PT for the company was $155/share. I maintain this PT here, but the PT is one of high conviction and one where you can really expect an upside in the longer term.

To be clear, $155 for RGA is not even 10x P/E for the 2025E period - and the company typically warrants around a 13x PE, despite currently trading at around 8-9x, depending on where you normalize the earnings and what you expect.

The unwinding of COVID-19 trends is expected to bring about a significant, double-digit, 25%+ improvement in adjusted EPS for this year (Source: FactSet). This is then followed by further growth in the next 2 years, an average of about 5% per year. If this materializes, then the company simply sticks to that 8-9x P/E range, which would be a substantial discount, still comes with a double-digit annualized upside, upwards of 14% at 9.3x P/E. If the company reaches double-digit P/E, we would be at 20% annualized, almost 21% for 2025E.

A full reversal in valuation trends for the company would imply no less than 33.3% annualized, or 88.36% until 2025E. Any of these scenarios are likely, in my view, but as usual, I tend towards the more conservative ones. In this case, estimating around 9-10x P/E for an A-rated insurer, and therefore expecting a double-digit RoR annualized, but at a relatively low yield.

On a positive note, RGA mostly hits its targets - 75-80% of the time even with a considerable and non-trivial margin of error.

Analysts would not only agree with my view, but they would go further. They would estimate the company at an 11-12x P/E on a current basis, estimating a $170/share average from a $151 low to a $199/share high. 13 analysts follow the company, and out of those, 9 are at "BUY" or similar levels of outperformance and positive recommendations.

Where I firmly agree with their stance is that at anything even close to $150/share, this company is a firm "BUY".

With regards to the upcoming earnings, I do not expect anything "life-changing", if you pardon the pun for a reinsurance company in the Life/Health segment, for RGA. I continue to expect morbidity to unwind as COVID-19 effects start to decline more and more. This in turn will result in the current forecast for the 2023E full year, materializing more or less according to the expected $18-18.2/share level or above, which would be a 20%+ improvement from the last fiscal. My current official forecast, and what I work from, is for that $18, which is about the midpoint between current analyst estimates, and where I see the company going after 1Q and 2Q results. What could impact the thesis are new money yields going down - or up more or less than expected, much as new money rates have gone up over the last few months. Aside from that, I don't see much potential instability in the forecast as it looks for 2023E.

And for that, here is my current and updated thesis for RGA.

Thesis

- Reinsurance Group of America is a quality reinsurer that has seen solid development over the past few years. I've seen returns of over 50% on this investment, and from that perspective, it's been extremely successful.

- RGA stock is still a "BUY" for me - but the price target is now closer to the current share price, and I don't see a massive upside beyond that - not on a realistic basis, at least. The upside here is less than 5-6%.

- I've updated my thesis for the company, and while the unwinding continues, the low yield makes the company a tricky investment prospect in those respects.

- My PT for the company is $155/share.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

The company is a "BUY" here, albeit less than it was.

For further details see:

Reinsurance Group Of American - Sup-Par Performance Since March, "BUY"