FPI - REIT Earnings Halftime Report

2023-08-02 09:00:00 ET

Summary

- We're at the halfway point of another consequential real estate earnings season with roughly 60 equity REITs and 16 mortgage REITs representing 50% of the total market capitalization reporting results.

- Per FactSet data, 75% of REITs have topped consensus FFO estimates thus far, a "beat rate" that slightly lags the even more impressive 80% EPS beat rate for the broader S&P 500.

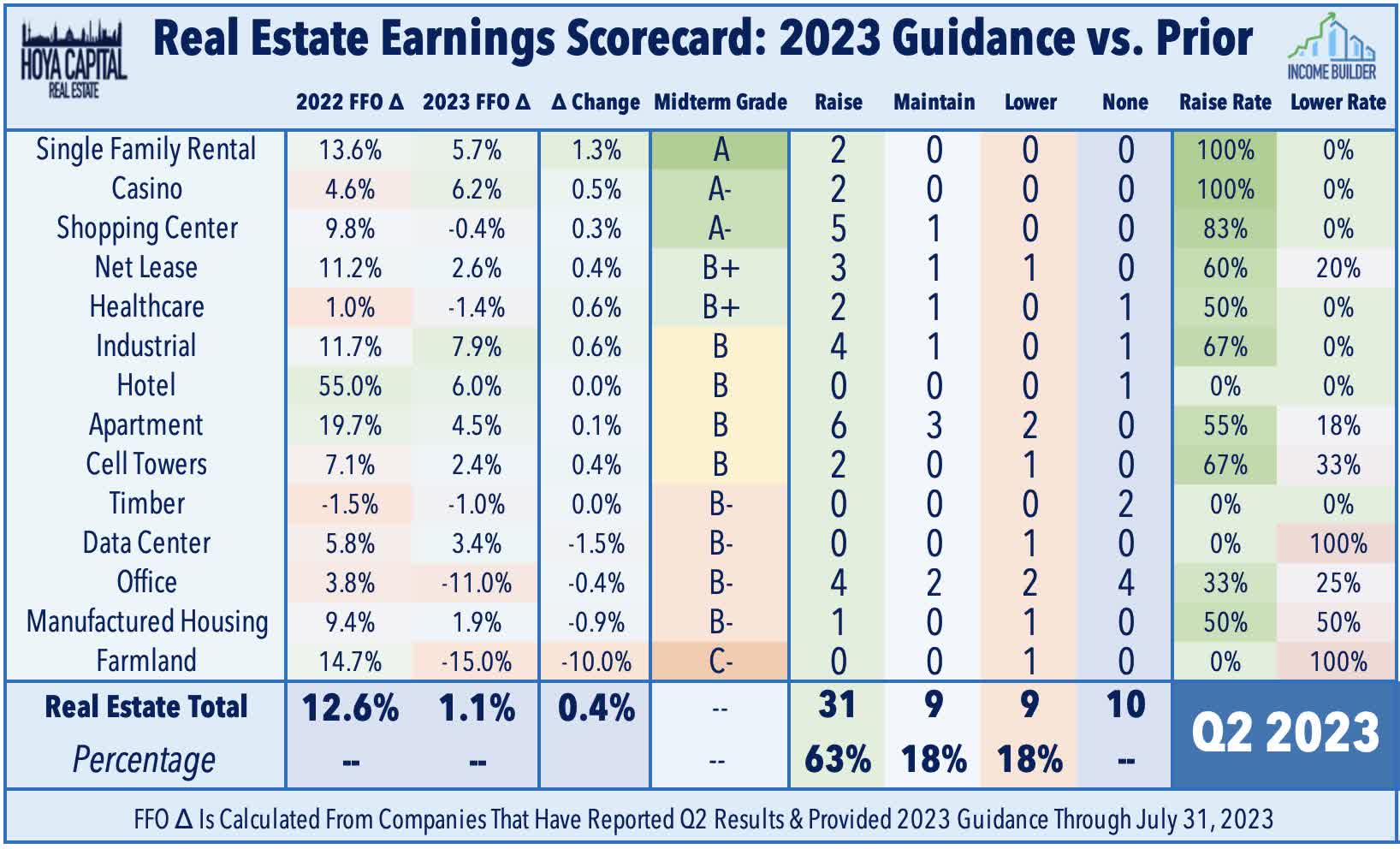

- More importantly, of the 49 REITs that provide guidance, 21 (63%) raised their full-year earnings outlook, while 9 (18%) lowered guidance, a "raise rate" well above the S&P 500 average.

- The single-family residential sector has been the upside standout thus far as tailwinds from the lingering undersupply of single-family homes and via disinflationary relief on expense pressures have fueled very strong reports from SFR REITs and homebuilders.

- Office REITs have posted double-digit gains this earnings season as results have been "less bad" than feared, confirming early reports showing a rebound in leasing activity in Q2, particularly in Sunbelt markets and New York City.

Real Estate Earnings Halftime Report

{kind=link}

We're at the halfway point of another consequential real estate earnings season, with roughly 60 equity REITs and 16 mortgage REITs representing 50% of the total market capitalization reporting results. Per FactSet data, 75% of REITs have topped consensus Funds from Operations ("FFO") estimates thus far, a "beat rate" that slightly lags the even more impressive 80% EPS beat rate for the broader S&P 500. More importantly, however, REITs are more optimistic about the second half of 2023 than most other industry groups. of the 49 REITs that provide guidance, 21 (63%) raised their full-year earnings outlook, while 9 (18%) lowered guidance, a "raise rate" that is above the S&P 500 average of 58%. The guidance "raise rate" was stronger at the property level than at the corporate level, with only two REITs (3%) lowering their full-year Net Operating Income ("NOI") outlook while 35 (74%) raised their full-year NOI outlook.

{kind=link}

The single-family residential sector has been one of the upside standouts thus far on a fundamental basis, as tailwinds from the lingering undersupply of single-family homes and from disinflationary relief on expenses have fueled very strong reports from SFR REITs, homebuilders, and senior housing REITs. Office REITs have posted double-digit gains this earnings season as results have been "less bad" than feared, confirming early reports showing a rebound in leasing activity in Q2, particularly in Sunbelt markets and New York City, offsetting deepening weakness in several West Coast cities. Industrial REITs continue to report stellar results, but potential headwinds loom from disruptions in the transportation sector, notably the bankruptcy this weekend of shipping giant Yellow. Technology REIT results have been hit-and-miss so far. Earnings season remains young for retail and hotel REITs, but the early returns have been quite strong, buoyed by a still-healthy U.S. consumer.

{kind=link}

Results from multifamily REITs showed surprising buoyant rent growth as well, but also showed some effects of the elevated supply growth that will persist into early 2024 before trailing off amid a tight financing environment. As with the prior quarter, the handful of earnings "misses" and downward earnings revisions have been driven predominately by elevated debt servicing expenses - notably Piedmont ( PDM ), NexPoint Residential ( NXRT ), and Farmland Partners ( FPI ) - underscoring the continued challenges facing more-highly-levered real estate portfolios from the higher rate environment. International underperformance has also been a headwind for several normally steady-handed REITs, including Sun Communities ( SUI ), while several other large-cap REITs that were heralded last year for their CPI-linked rent escalators - notably net lease REIT W.P. Carey ( WPC ) and casino REIT VICI Properties ( VICI ) - have been on the wrong side of that trade this earnings season. Below, we discuss our halftime analysis and grades for each property sector.

{kind=link}

Office REIT Halftime Report

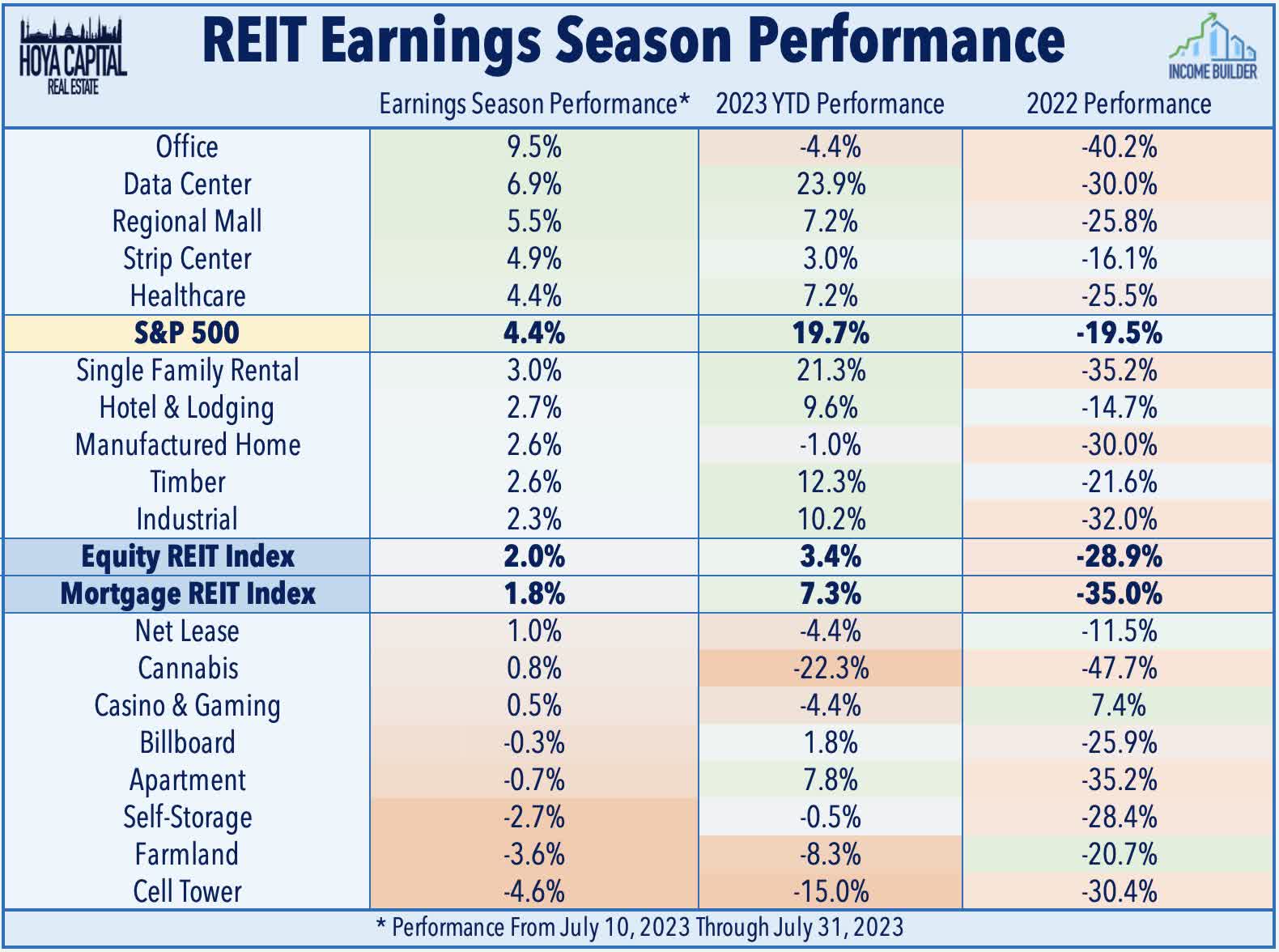

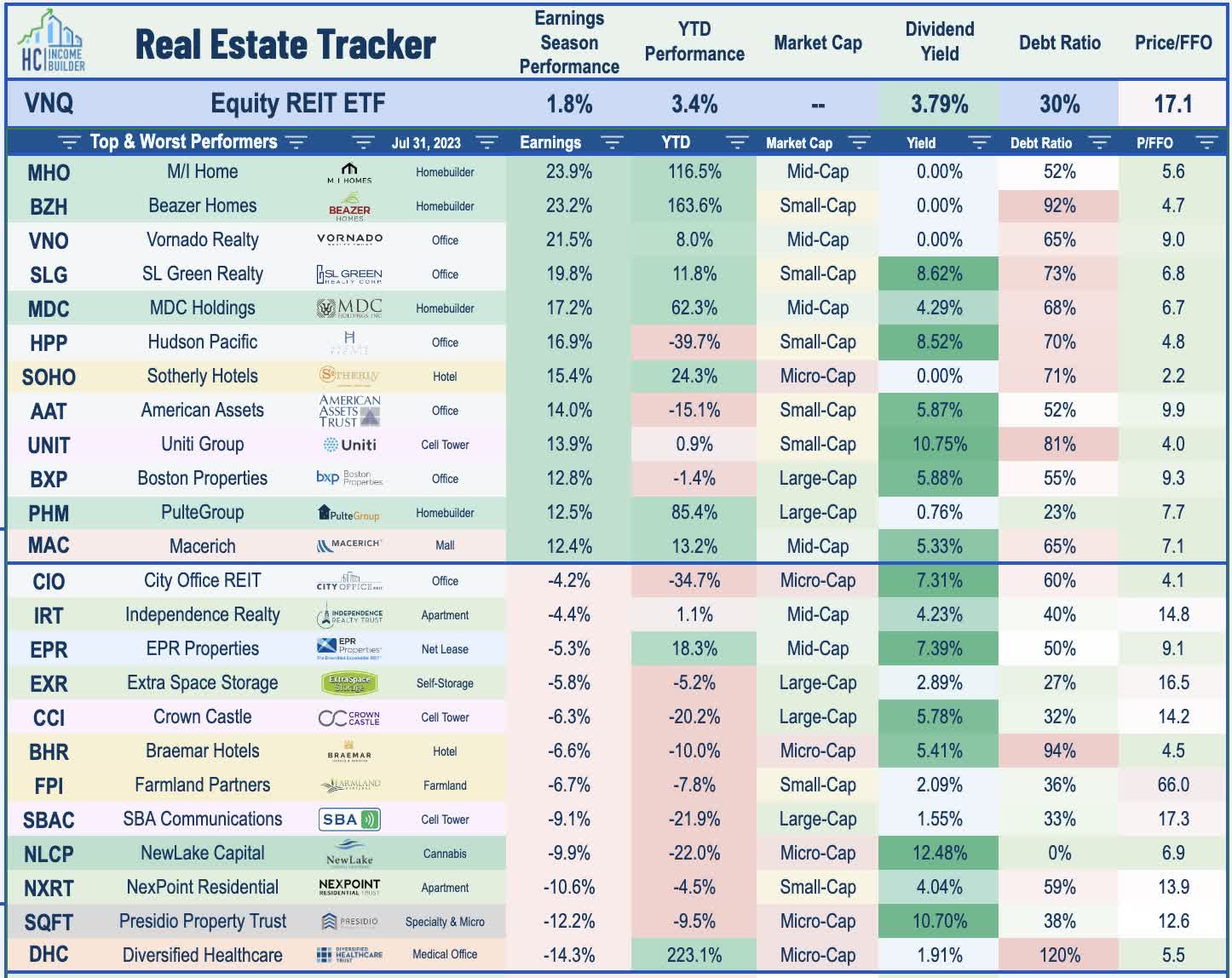

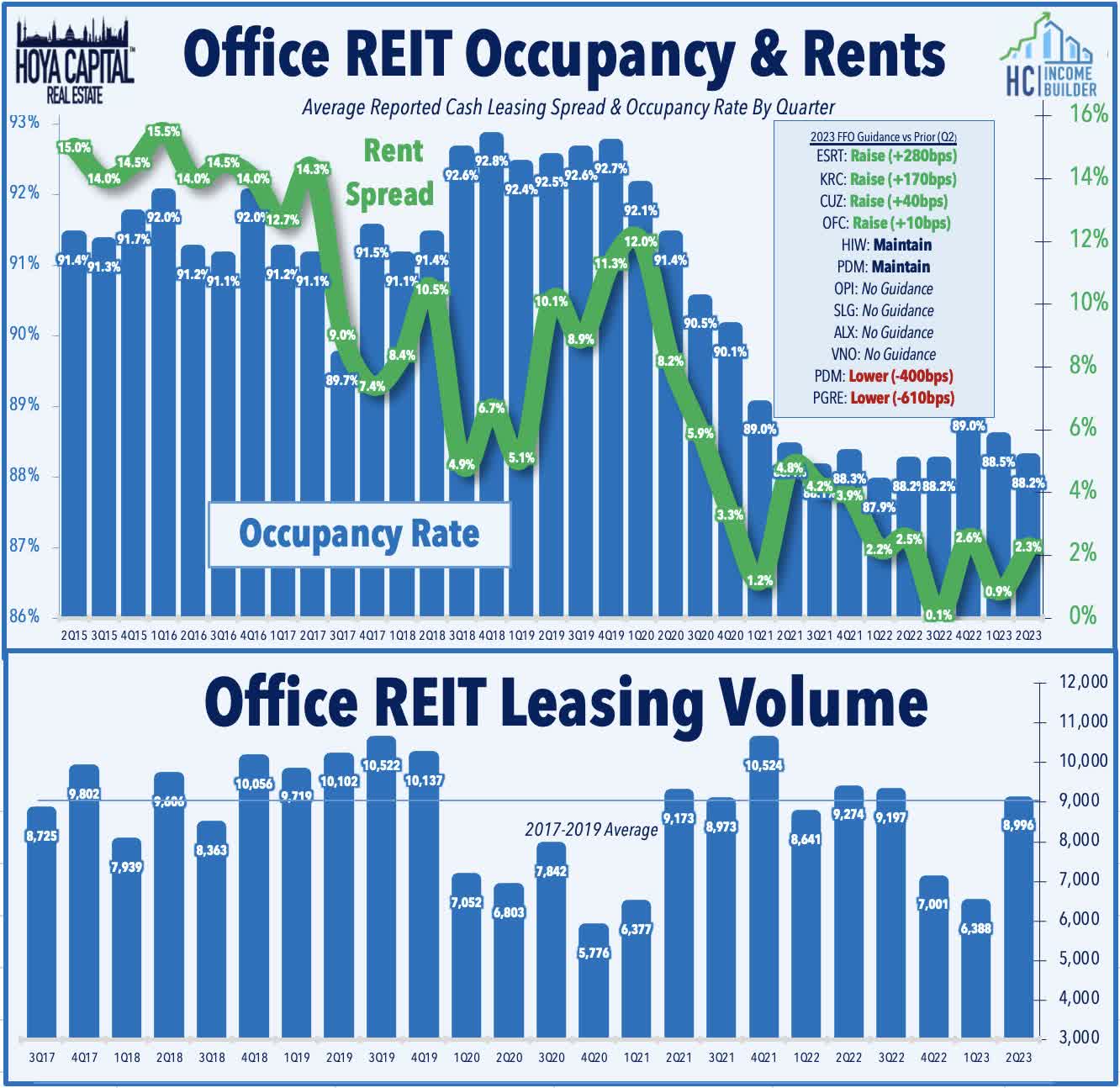

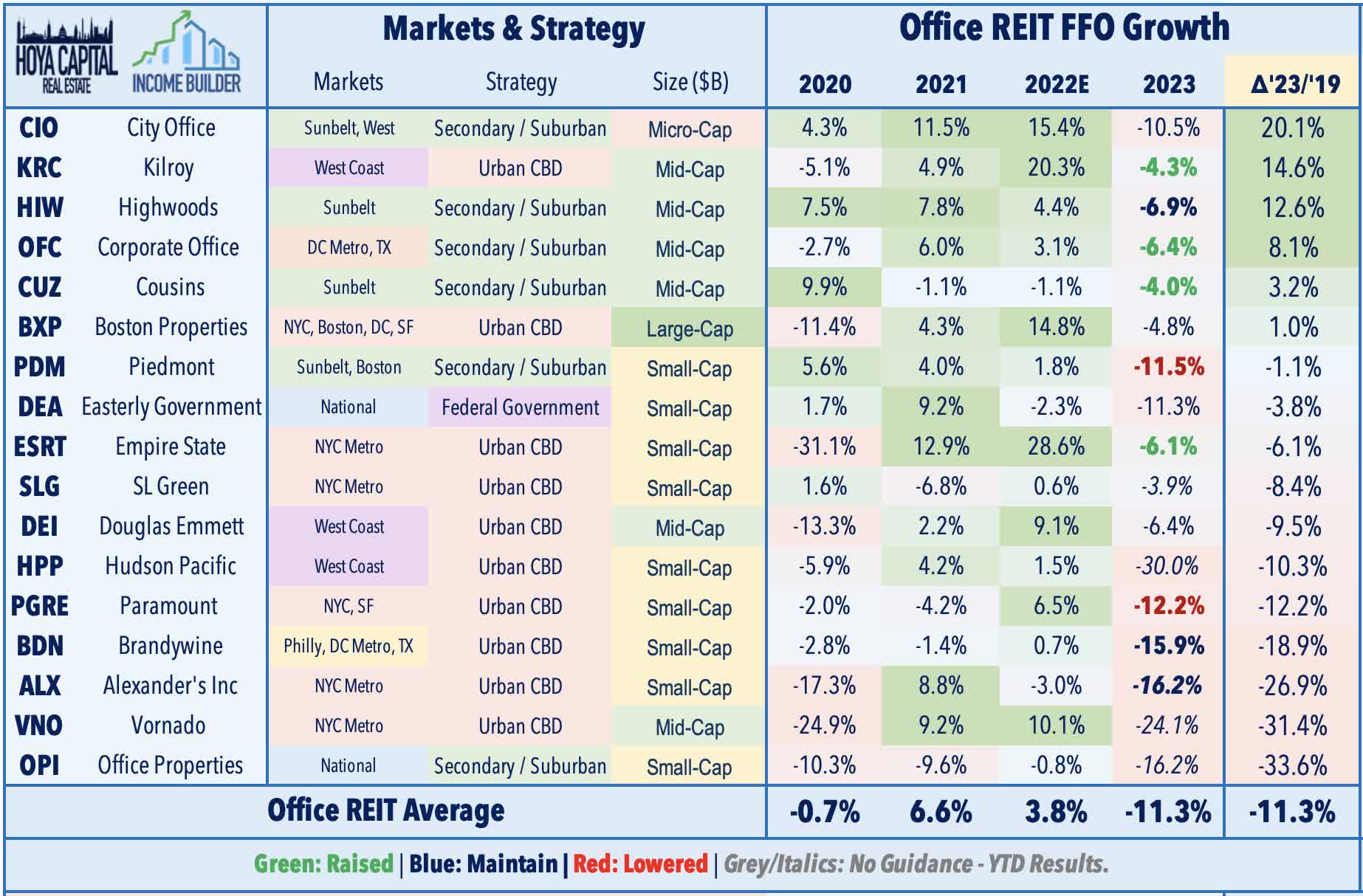

Office : (Halftime Grade: B-) The battered office REIT sector has led the gains this earnings season on the heels of a slate of surprisingly solid reports showing that leasing activity and pricing trends do indeed appear to have rebounded in recent months, with total volume trending towards levels that are only slightly below the pre-pandemic averages after two historically weak quarters. Four office REITs have actually raised their full-year outlook this earnings season, including NYC-focused Empire State Realty ( ESRT ), which reported impressive leasing volume of 336k square feet - above its pre-pandemic average from 2017-2019 - and achieved effective rent increases of 10.1% on these leases. Sunbelt-focused Cousins ( CUZ ) also raised its full-year FFO growth outlook and recorded rent growth of 7.9% on leasing volume of 435k square feet - each an acceleration from last quarter. Corporate Office ( OFC ) - another Sunbelt-focused REIT - also boosted its full-year FFO growth outlook and recorded its strongest quarter of leasing activity and occupancy since 2021. The third Sunbelt REIT - Highwoods ( HIW ) - reported leasing activity of 918k square feet - 16% above its four-quarter average - and achieved cash rent growth of 0.5% on these leases.

{kind=link}

Results from West Coast-focused REITs have been notably weaker than their Sunbelt-focused and even their NYC-focused peers. Paramount ( PGRE ) plunged after reporting very weak results and significantly lowering its full-year outlook driven by the bankruptcy of First Republic - its largest tenant - and deepening distress in the San Francisco office market. PGRE leased just 72k square feet of space in Q2 - 70% below its pre-pandemic average from 2017-2019 - with just 12k SF leased in San Francisco Back in June, PGRE slashed its dividend by more than 50%, one of nine office REITs to lower its dividend this year. Kilroy ( KRC ) noted that its occupancy rate dipped 300 basis points from the prior quarter, driven by several significant lease expirations in its Seattle portfolio. On the upside, KRC still managed to raise its full-year outlook for both same-store NOI and FFO, and was able to secure an 11-year $375M secured loan at a 5.90% fixed interest rate - relatively attractive pricing compared to recent large debt raises in the office sector. On that note, Piedmont has also lagged after it announced the refinancing of $400M in debt at a sharply higher interest rate - 9.25% compared to its maturing 4.45% note - which prompted a downward revision to its FFO outlook. PDM also became the 9th office REIT this year to reduce its dividend, trimming its quarterly payout by about 40%.

{kind=link}

Residential REIT Halftime Report

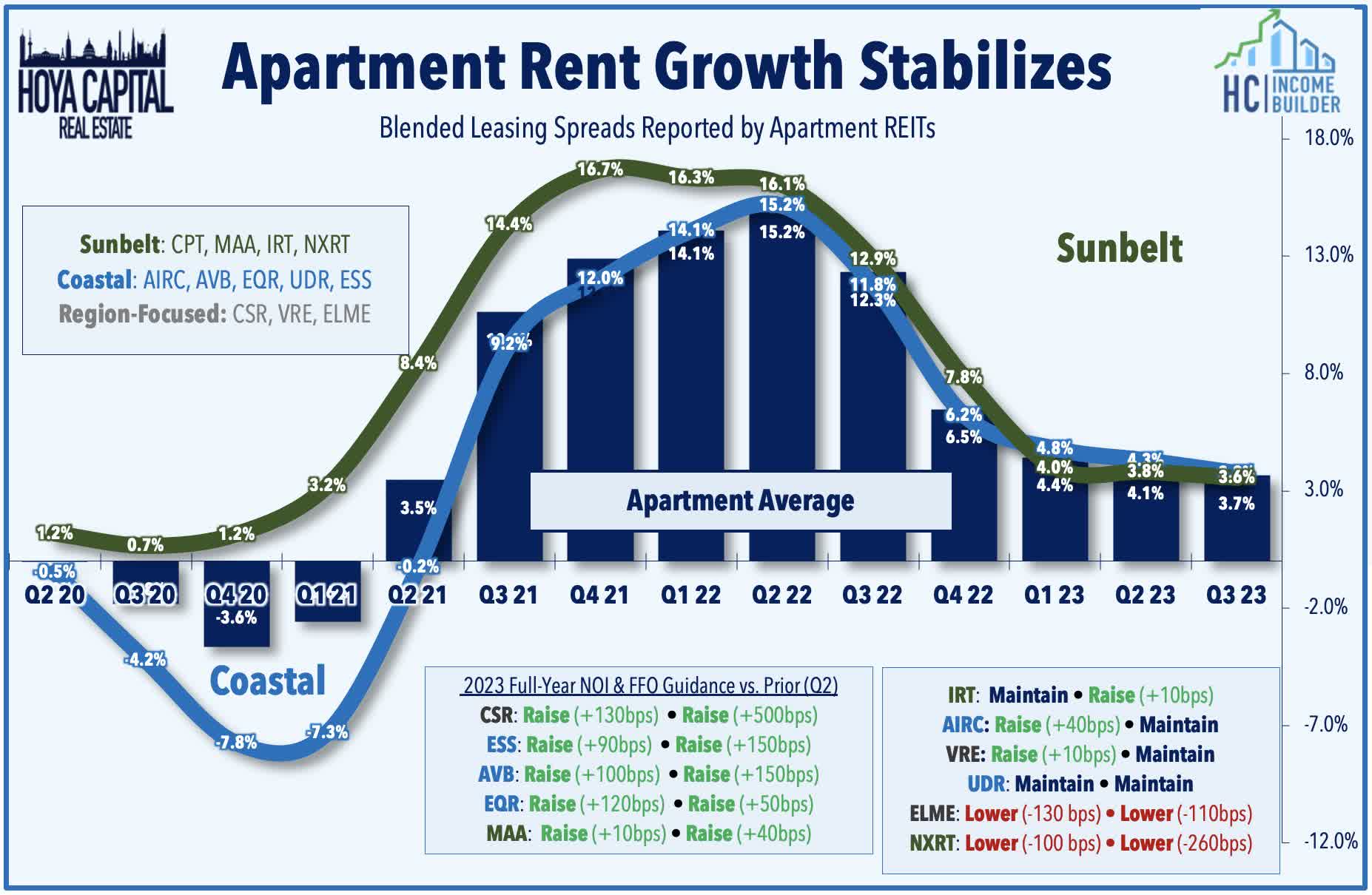

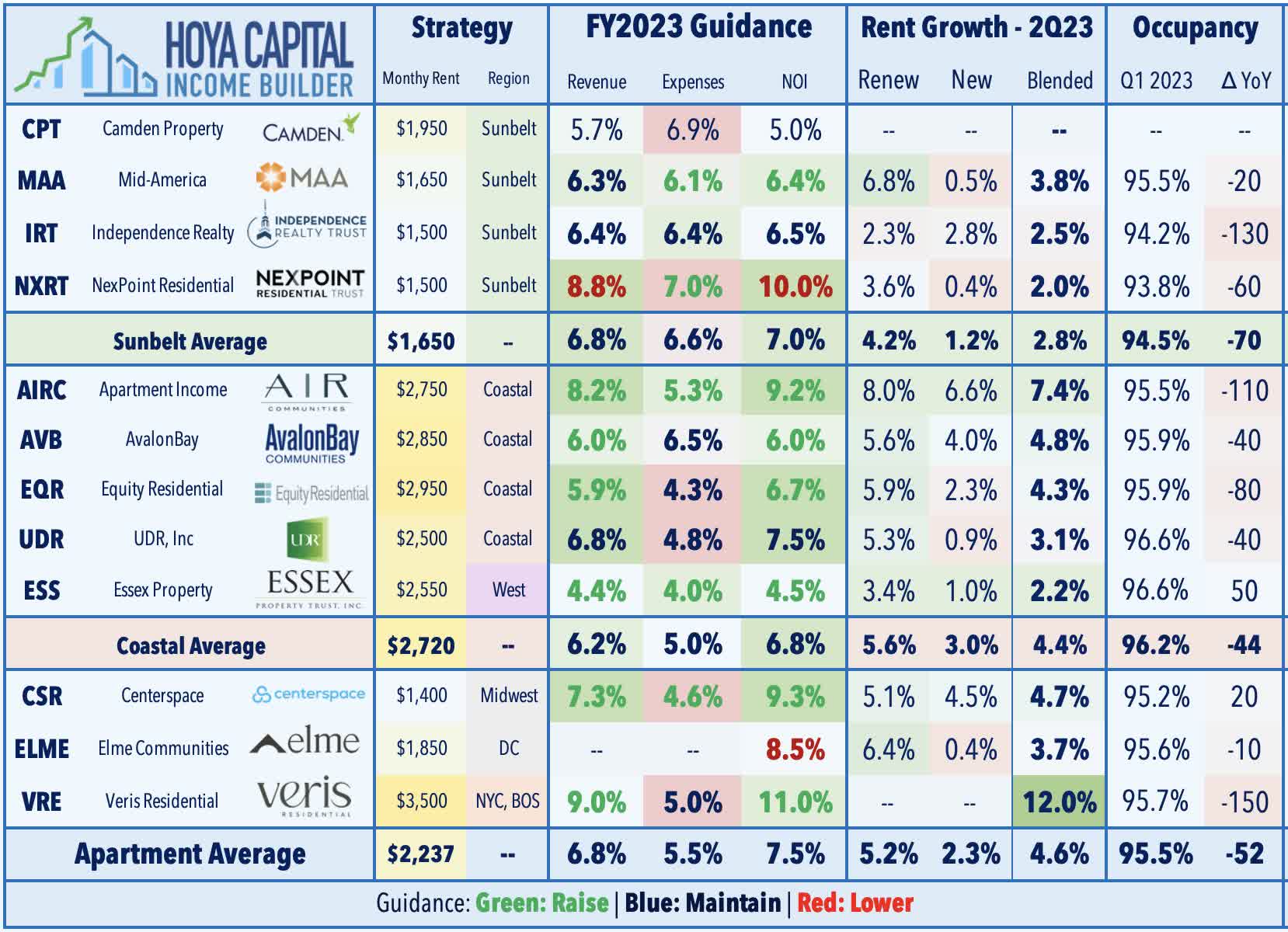

Apartment : (Halftime Grade: B) While several property sectors haven't yet started earnings season, apartment REIT earnings season is essentially complete, with eleven of the twelve largest apartment REITs reporting results. Rent growth has indeed moderated from the historic pace seen from mid-2021 through mid-2022, but contrary to the bearish consensus late last year calling for a rent "correction" with negative growth, we've instead seen stabilization in the typical "inflation-plus" range between 4-5%. Six of the eleven REITs raised their full-year FFO outlook while eight of the eleven raised their same-store NOI outlook, upward revisions helped by moderating expense pressures. Impacts from a historically large multifamily development pipeline are beginning to become more visible as all but two REITs reported a year-over-year occupancy decline, but there was an overwhelming consensus on earnings calls that supply pressures will abate into 2024 given the extremely challenging financing environment for new ground-up development.

{kind=link}

Results from Coastal-focused REITs have been marginally stronger than their Sunbelt-focused peers. NYC-focused Veris Residential ( VRE ) has been the top-performer this earnings season after raising its full-year outlook and announcing that it completed a $520M buyout from its joint-venture partner Rockpoint - a major step towards simplifying its business structure as a pure-play multifamily REIT. The biggest upside surprise, however, came from West Coast-focused Essex ( ESS ), which reported surprisingly solid results and significantly raising its full-year FFO and NOI growth outlook, citing strength in Southern California markets, which offset relative weakness in Northern California and Seattle. Downside surprises have come from REITs focused on the middle-tier market segment, where we've seen an uptick in bad debt expense and a more pronounced deceleration in rent growth. Small-cap NexPoint Residential ((NXRT)) has been the laggard after lowering its NOI outlook citing weakness in its Class B properties in Atlanta and Las Vegas, and lowering its FFO outlook as it works through disruptions in asset sale plans.

{kind=link}

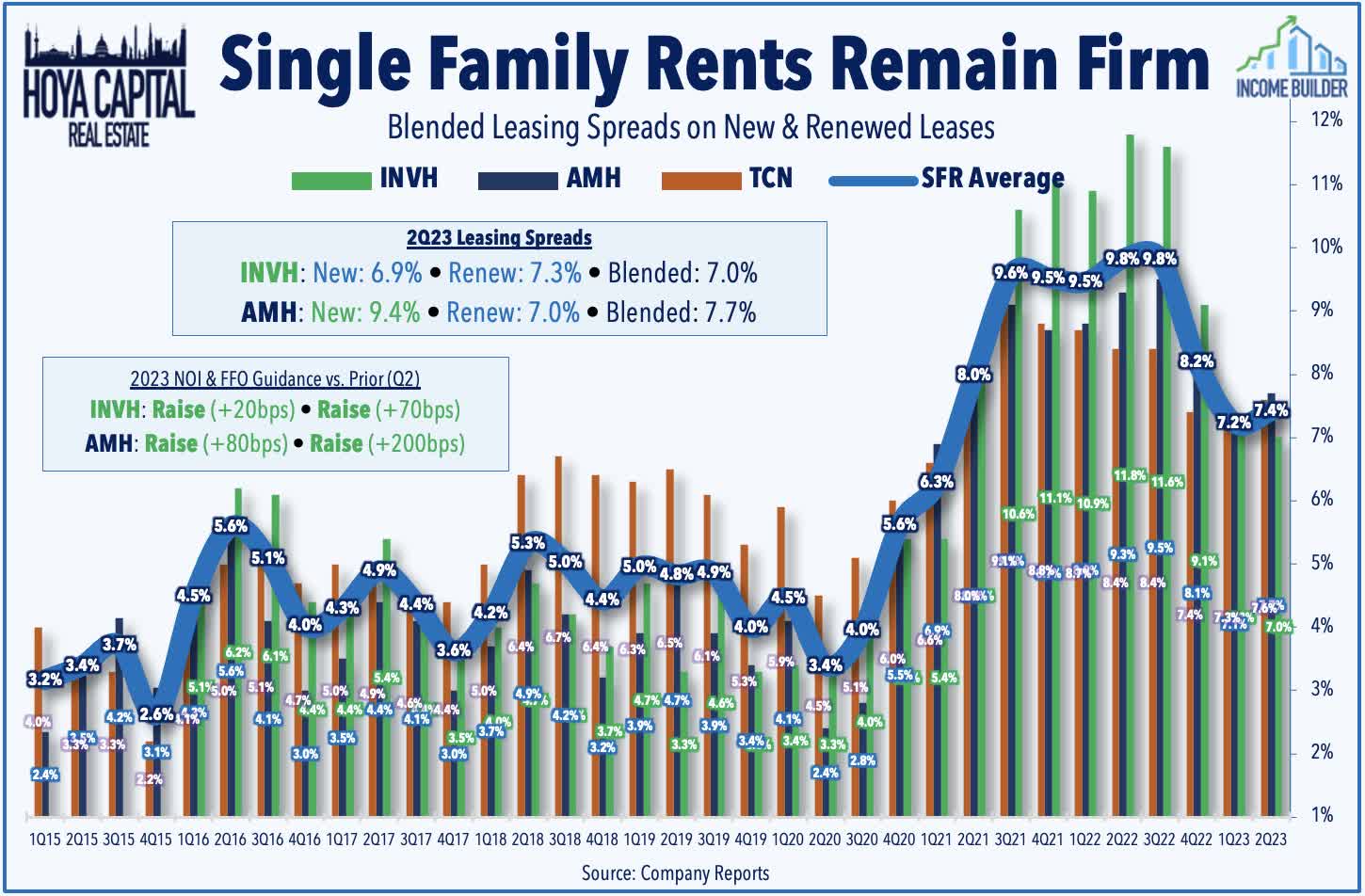

Single-Family Rental : (Halftime Grade: A) SFR REITs reported impressive "beat and raise" results last week fueled by buoyant rent growth across the SFR sector, which is not facing the same supply headwinds as the multifamily side. American Homes recorded blended leasing spreads of 7.7% in Q2 - which was actually an acceleration from the 7.1% rate in Q1 - which drove a boost to its full-year earnings outlook. AMH now expects full-year FFO growth of 6.5% - up 200 basis points from last quarter and sees NOI growth of 4.8% at the midpoint - up 80 basis points from last quarter. AMH also noted that it entered into a $625M second strategic joint venture with J.P. Morgan Asset Management to construct "built to rent" homes. Invitation Homes recorded blended leasing spreads of 7.0% in Q2 - which was down only slightly from the 7.3% blended increase in Q1 - and drove a boost to its full-year earnings outlook. INVH now expects full-year FFO growth of 5.0% - up 70 basis points from last quarter. INVH also reported that it acquired 1,900 homes for $650 million from Starwood Capital's non-traded REIT platform dubbed "SREIT" which has faced similar redemption requests as Blackstone's BREIT.

{kind=link}

Manufactured Housing : (Halftime Grade: B-) After snapping a decade-long streak of outperformance over the REIT Index last year, MH REITs are pacing for a second-straight year of underperformance, but property-level fundamentals in the core manufactured housing segment are certainly not to blame. Sun Communities ((SUI)) - the best-performing REITs in the 2010s - appears to have made an operational misstep with its push into the European market, a segment that has posted disappointing performance since its acquisition in mid-2022. SUI lowered its full-year FFO outlook as upward guidance boosts to its core manufactured housing and marina outlook were more than offset by a significant downward revision to its UK Home Sales NOI forecast. Results from Equity Lifestyle ( ELS ) were stronger, however, which raised its full-year FFO and NOI guidance, "driven by continued strength in annual revenue and reduced expenses throughout our portfolio." ELS was given an added boost by its inclusion in the S&P 400 Index , replacing Life Storage. While COLA increases have helped to drive record-high rent growth across the MH portfolio, the RV segment has been a recent issue for both SUI and ELS after several years of stellar performance. RV utilization rates have slumped amid a post-COVID normalization, while pressure from higher interest rates has resulted in a roughly 40% plunge in new RV sales this year.

{kind=link}

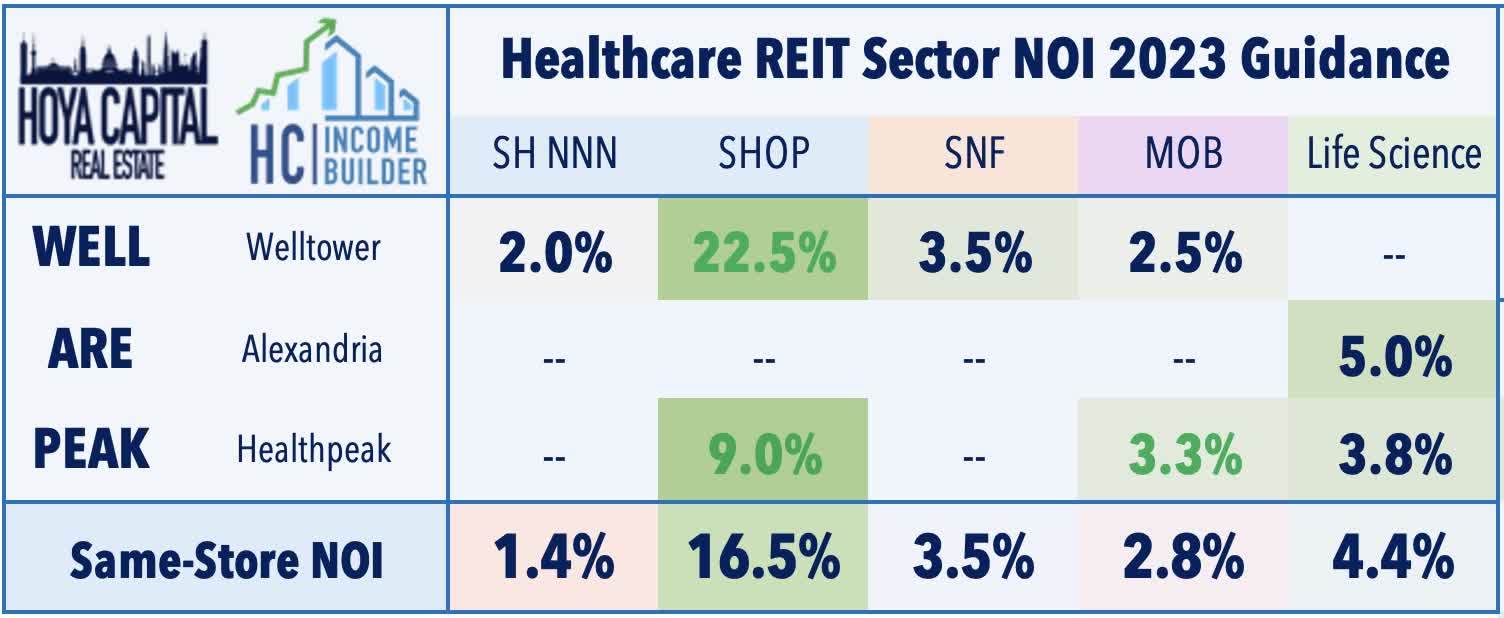

Healthcare REIT Halftime Report

Healthcare : (Halftime Grade: B+) We've seen results from five of the fifteen healthcare REITs. Abating expense pressures has lifted the outlook for senior housing and skilled nursing REITs in recent months as crisis-level staffing issues at these facilities were a major headwind from late 2021 through early 2023. Senior housing REIT Welltower ( WELL ) boosted its full-year guidance driven by another upward revision to its NOI expectations for its Senior Housing Operating Portfolio ("SHOP"). Benefiting from COLA increases, pricing power remains robust as well, with WELL recording record-high rent growth of 6.7% in its occupied facilities, which combined with moderating expense pressures, has driven a meaningful improvement in operating margins. Positively for senior housing REITs, supply growth has finally cooled following a decade of elevated inventory growth, as NIC reported that units under construction amounted to 4.9% of total inventory, which is the lowest seen since 2014. Tenant operator health will be a major focus in the back half of earnings season across the skilled nursing and hospital sub-sectors, REITs that have come into the cross-hairs of short-sellers in recent quarters.

{kind=link}

Lab space operator Alexandria Real Estate ( ARE ) - a REIT that came into the cross-hairs of short-sellers in recent months - recorded total leasing volume of 1.3M square feet in Q2 - up slightly from the 1.2M SF signed in Q1 - and on these leases, it achieved cash rent increases of 8.3%, a rate of increase that was down from its record-high spreads in Q1 of 24.2%. ARE maintained the midpoint of its outlook for full-year adjusted FFO at $8.96 - representing a 6.5% increase from 2022 - and maintained the midpoint of its outlook for full-year average occupancy at 95.1% and for cash rental rate spreads at 14.5%. However, ARE downwardly revised its full-year unadjusted FFO guidance to reflect several recent asset sales and the previously-announced impairment related to a Boston property - 275 Grove Street - where it dropped plans to convert the office space into lab space.

{kind=link}

Industrial & Technology REIT Halftime Report

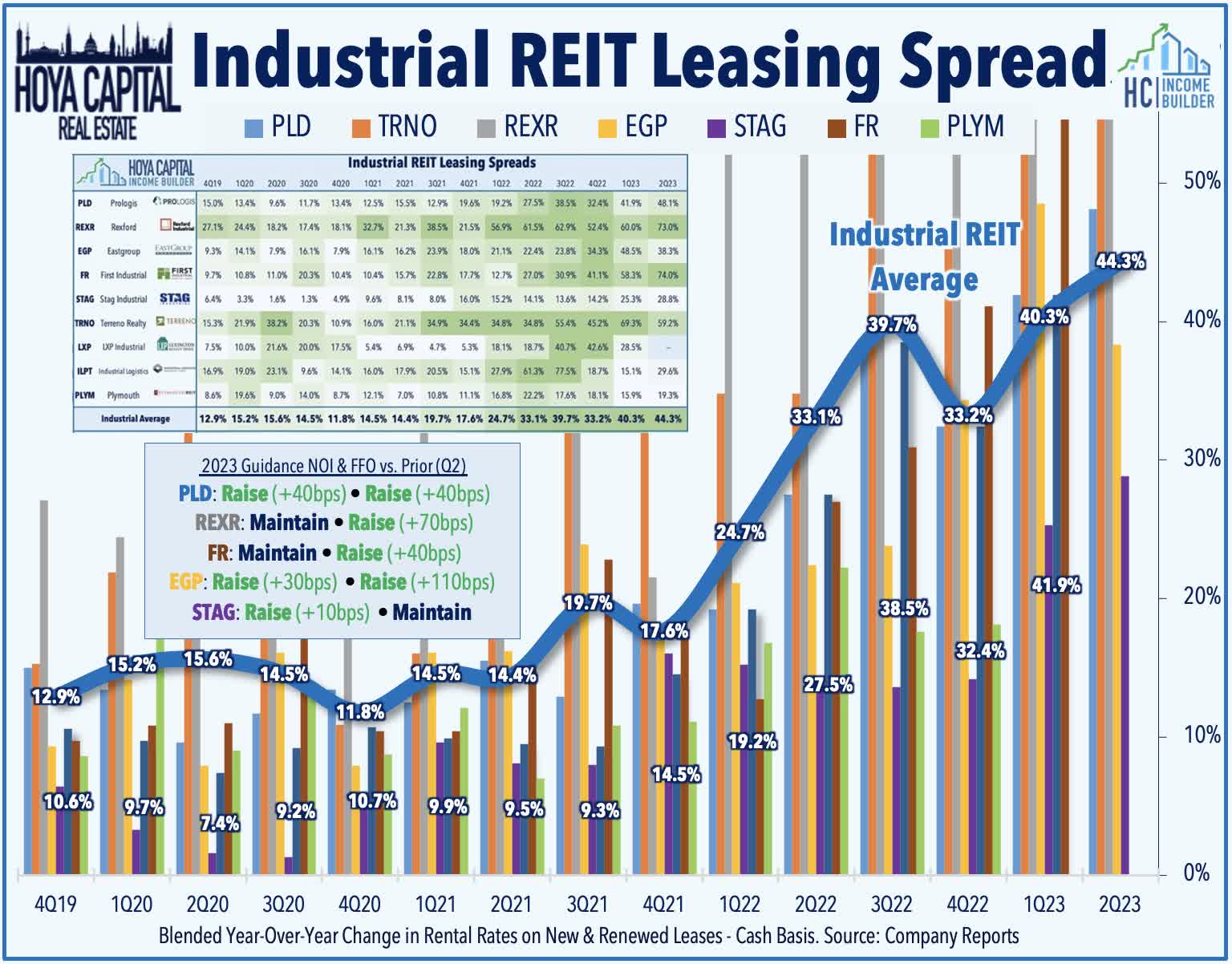

Industrial : (Halftime Grade: B) We've seen results from the five largest industrial REITs, where we've seen similar themes of strong-but-normalizing fundamentals that we observe in the multifamily space. We've been accustomed to seeing across-the-board guidance increases from these REITs since the start of the pandemic, so second-quarter results were slightly softer than expected as 3-of-5 REITs raised their NOI outlook while 4-of-5 REITs raised their FFO outlook. Tenant-related concerns also pressured logistics-focused REITs over the past month amid mounting issues seen across the broader transportation sector, underscored by the bankruptcy this week of shipping giant Yellow ( YELL ). EastGroup ( EGP ) has been the upside standout this earning season, raising its full-year outlook for both NOI and FFO. Driven by rent increases of 52.8% on new and renewed leases, Echoing commentary from other industrial REITs, EGP noted that it has seen "normalizing" demand in recent quarters and cautioned of a near-term supply overhang over coming quarters but commented that its "seeing supply taper off." Prologis' ( PLD ) earnings call commentary also indicated expectations of near-term softness in the back half of 2023 before re-tightening in 2024.

{kind=link}

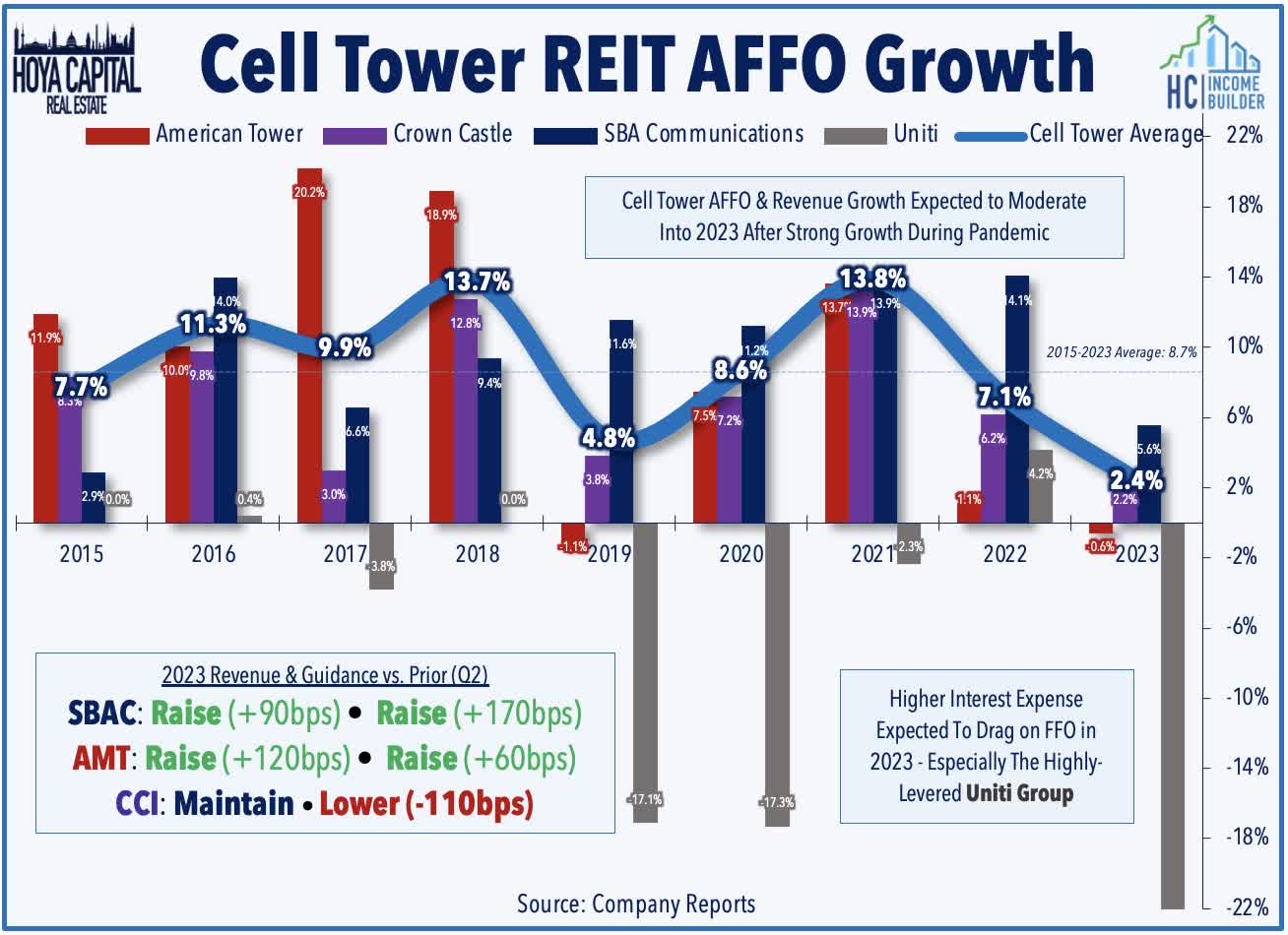

Cell Tower : (Halftime Grade: B) We've now seen results from all three cell tower REITs. Earnings season began on a sour note with Crown Castle ( CCI ) lowering its full-year adjusted FFO outlook citing a "significant" slowdown in carrier network spending. We were surprised by CCI's sudden downbeat industry commentary, with CCI commenting that "the initial surge in tower activity [related to the 5G rollout] has ended." Subsequent results from American Tower ( AMT ) and SBA Communications ( SBAC ) - both of which raised their full-year revenue and FFO guidance - allayed some industry-level concerns and provided evidence to our suspicion that CCI's downbeat tone may have been related to its later-announced restructuring plan to reduce costs - which includes a reduction in employee headcount by about 15%. Combined, cell tower REITs upwardly revised their full-year FFO outlook by an average of roughly 0.5%. Last week, we published Cell Tower REITs: Toxic Telecom, which noted that industry headwinds are rooted primarily in the ongoing disintermediation of legacy wireline business segments towards fully wireless deployments and the mounting competition on the two industry juggernauts. This disintermediation has trended on a path from wired to wireless infrastructure, disruptions which actually serve to further solidify the longer-term favorable competitive positioning of cell tower REITs.

{kind=link}

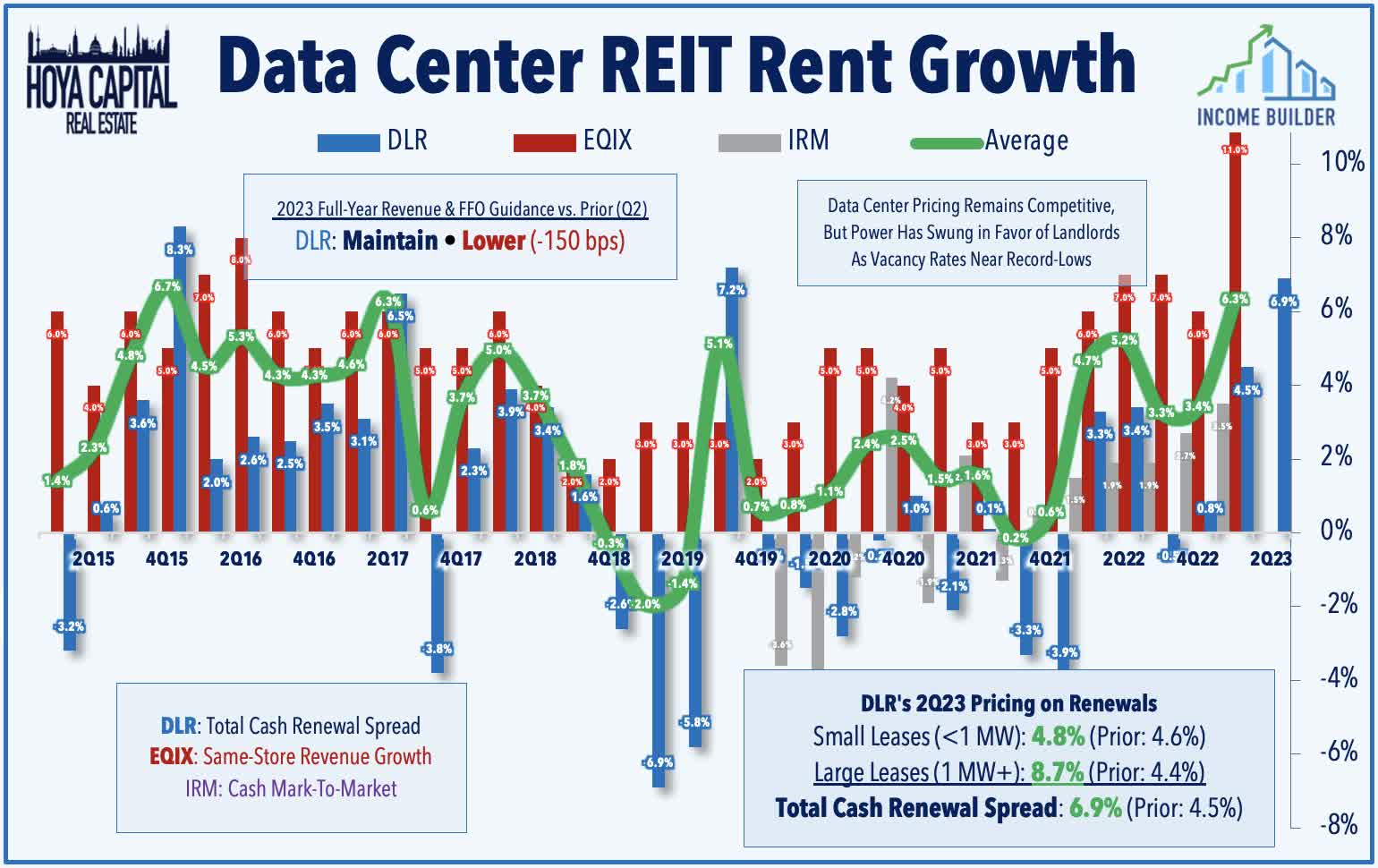

Data Center : (Halftime Grade: B-) We've seen results from one of the two major data center REITs. Digital Realty ( DLR ) reported solid second-quarter results highlighted by impressive pricing trends and the successful $1.3B capital raise through a majority sale of a portfolio in Northern Virginia to TPG Real Estate at a 6.0% cap rate. While DLR trimmed the midpoint of its full-year FFO outlook due to unpaid rent from Cyxtera - which declared bankruptcy earlier this year - it raised its outlook for cash re-leasing spread and same-store NOI growth by 100 basis points each. Rent growth trends continued on an upward trajectory in Q2 with cash re-leasing spreads of 6.9% - the highest in three years - with notable strength from larger leases which posted rent spreads of nearly 9%, which had been an area of weakness in recent years. Equinix ( EQIX ) and Iron Mountain ( IRM ) report results later this week.

{kind=link}

Retail REIT Halftime Report

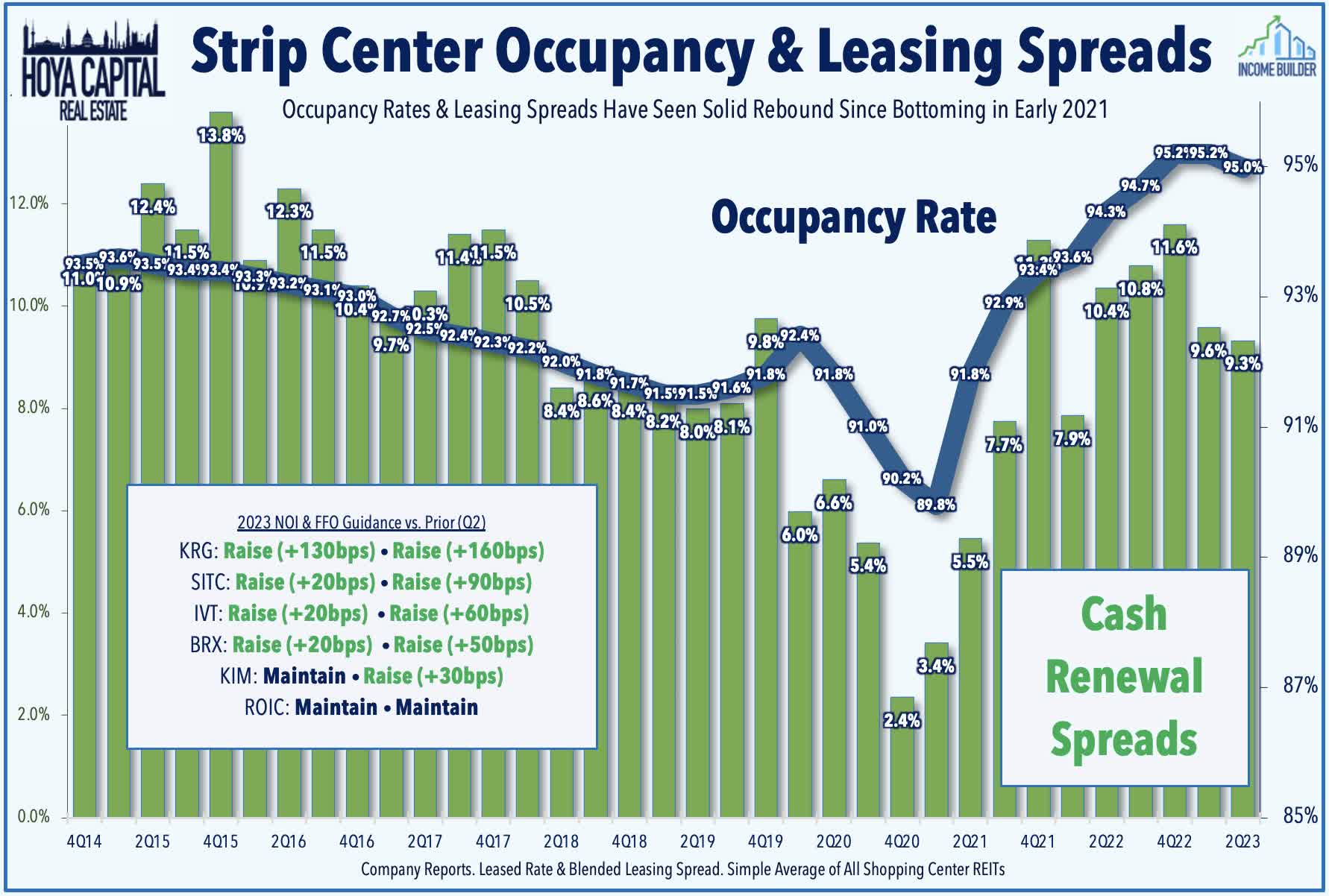

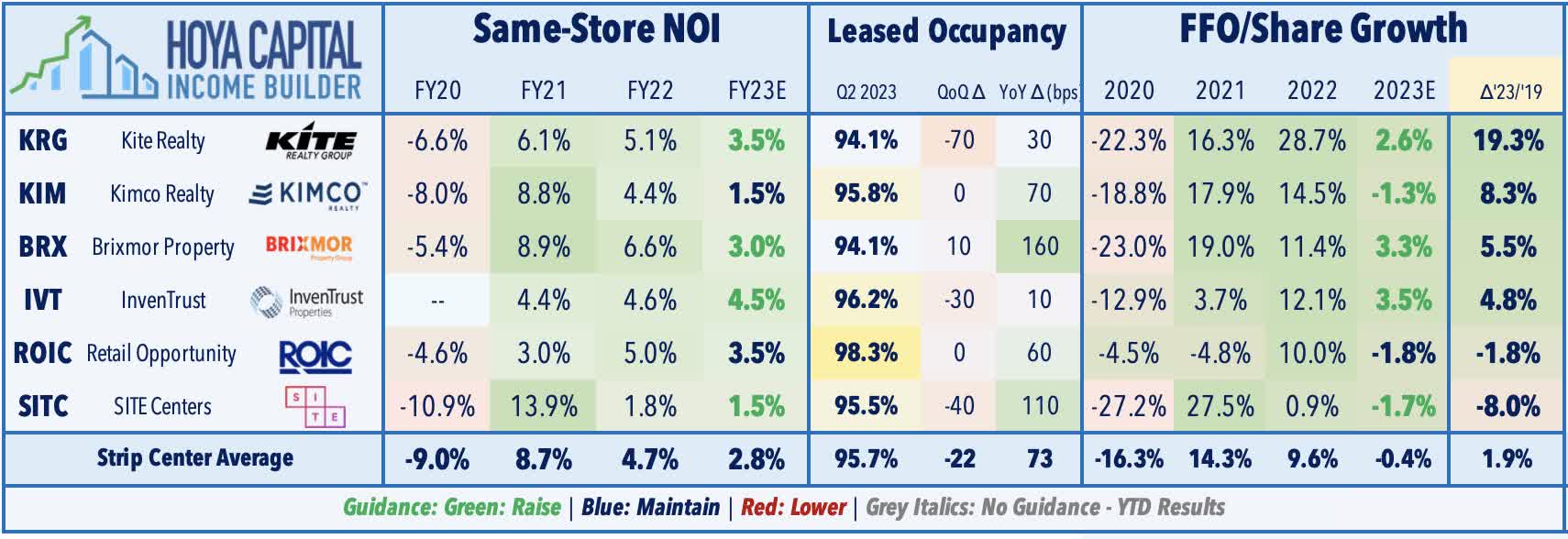

Strip Centers : (Halftime Grade: A-) Earnings season is still young for the retail sector, but results thus far have been quite solid - continuing a trend of better-than-expected results stretching back to late 2021 as demand for "big box" space has significantly exceeded the available supply even despite the recent high-profile bankruptcies of Bed Bath and Party City. Five of the six strip center REITs have raised their full-year FFO outlook, while four of the six have boosted their NOI guidance. Rent spreads have decelerated a bit over the past two quarters while vacancy rates have also ticked slightly higher amid a modest overhang from the pending vacancies from Bed Bath and others, but Q2 is still pacing to post an eight-straight quarter of blended spreads of at least 7.5%. Results from Kite Realty ( KRG ) were the most impressive of the group, reporting blended cash leasing spreads of 14.8%, which drove a 130 basis point upward revision to its same-store NOI outlook and a 160 basis point boost to its FFO outlook.

{kind=link}

Elsewhere, Site Centers ( SITC ) has also been an upside standout with a double guidance boost and provided more color on the vacated Bed Bath space, noting that roughly 60% of the space has already been released and that SITC is on target to achieve a "20% to 25% increase" to the existing in-place Bed Bath rents. InvenTrust ( IVT ) boosted its FFO growth outlook to 3.5% - up 60 basis points from last quarter - and raised its NOI outlook to a sector-high of 4.5% - up 20 basis points from last quarter. Brixmor ( BRX ) completed the trio of double-boosts by raising its full-year NOI outlook to 3.3% - up 20 basis points - and its FFO outlook to 3.3% - up 50 basis points from the prior quarter. Notably, BRX recorded blended leasing spreads of 15.4% - down slightly from the prior quarter but currently the leader in the clubhouse within the strip center sector.

{kind=link}

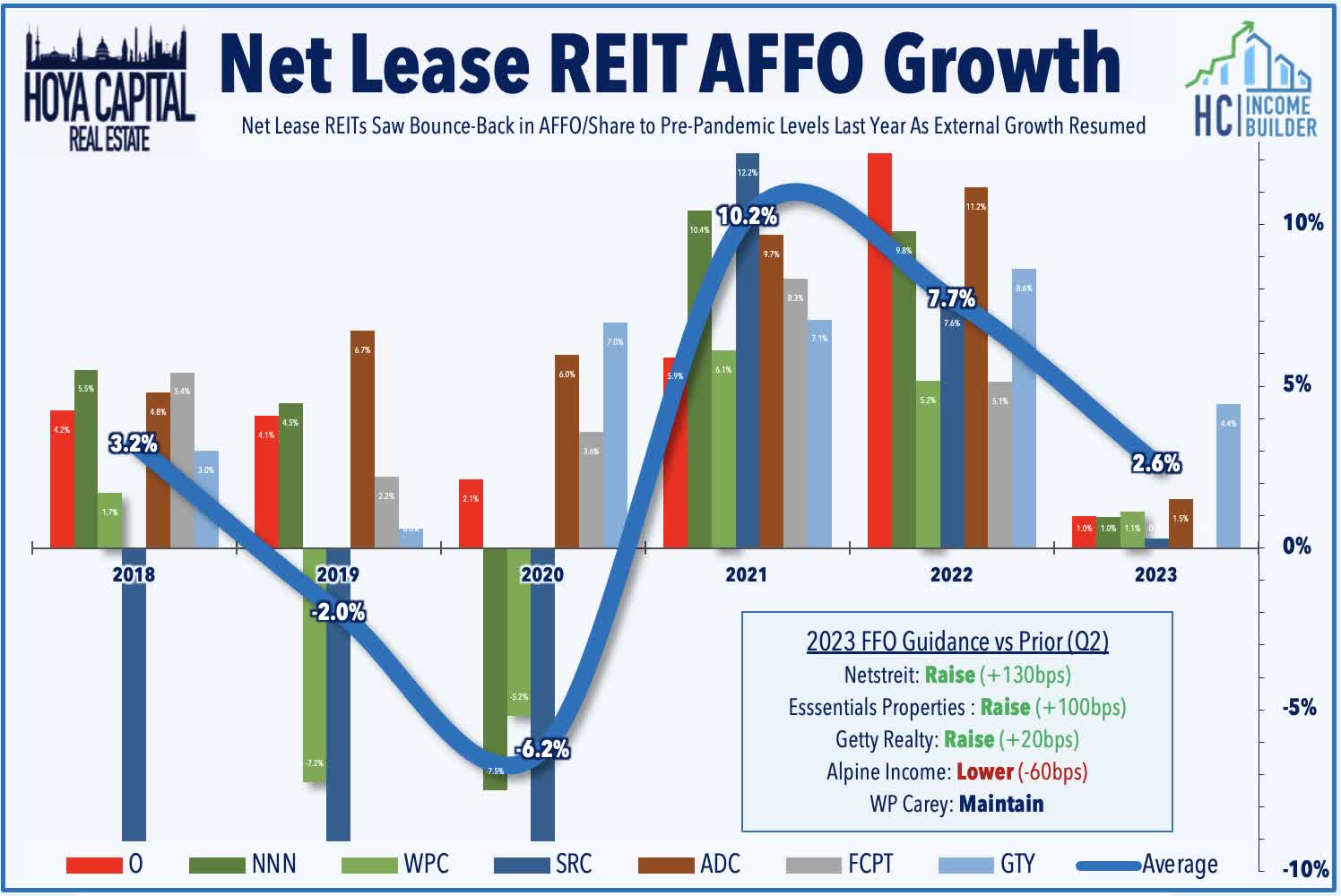

Net Lease : (Halftime Grade: B+) While still very early in net lease earnings season with results from just 5 of 16 REITs, results thus far have been positive, with three of the five REITs raising their full-year outlook. Netstreit ( NTST ) raised its full-year FFO outlook to 4.7% (up 130 basis points from last quarter), Essential Properties ( EPRT ) raised its full-year FFO growth outlook by 100 basis points to 6.9%, and Getty Realty ( GTY ) increased its FFO growth outlook by 20 basis points to 4.4%. On the downside, W. P. Carey ((WPC)) maintained its full-year outlook, a bit of a disappointment after the trio of its net lease peers raised their outlook earlier in the week. WPC continues to expect FFO growth of roughly 3% this year, while it also maintained its full-year acquisitions guidance which calls for investment volume between $1.75 billion and $2.25 billion. Notably, WPC sees its rent growth "peaking" this year at around 4% this year as the tailwinds from the CPI linkage may potentially become modest headwinds into 2024 given the recent inflation trends.

{kind=link}

Mortgage REITs Halftime Report

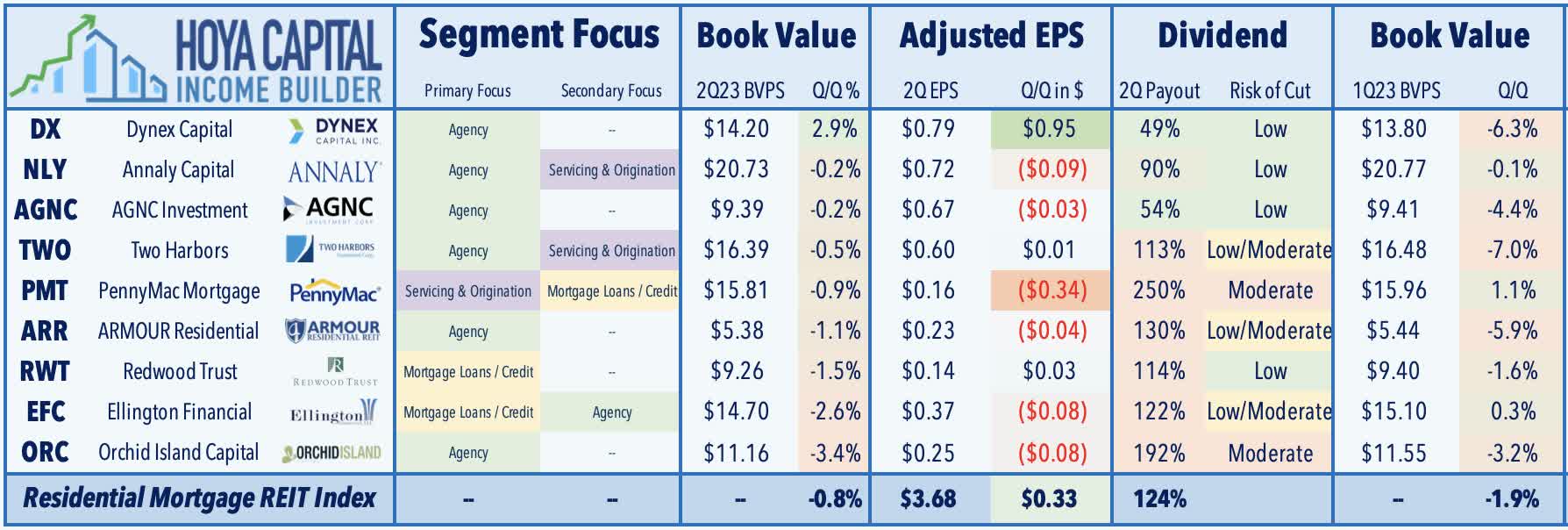

Residential mREITs : (Halftime Grade: B) We've seen results from 9 of the 24 residential mREITs. Consensus expectations called for Book Value Per Share ("BVPS") to be roughly flat in Q2, and thus far, we've roughly hit that target. Agency-focused mREITs have generally fared better this earnings season, with both AGNC Investment ( AGNC ) and Annaly ( NLY ) beating Street EPS estimates driven by improved net investment spreads. AGNC remarked, "we are at the forefront of one of the most constructive investment environments in our 15-year history." Credit-focused residential mREIT Redwood ( RWT ) has also been an upside standout after reporting EPS of $0.14 - up from $0.11 last quarter and beating Street estimates. On the downside, PennyMac ( PMT ) reported disappointing results driven by underperformance from its interest-rate sensitive strategies and elevated hedge costs. PMT reported EPS of $0.16 in Q2 - down from $0.50 last quarter and short of its $0.40/share dividend - while noting that its BVPS declined about 1% to $15.81.

{kind=link}

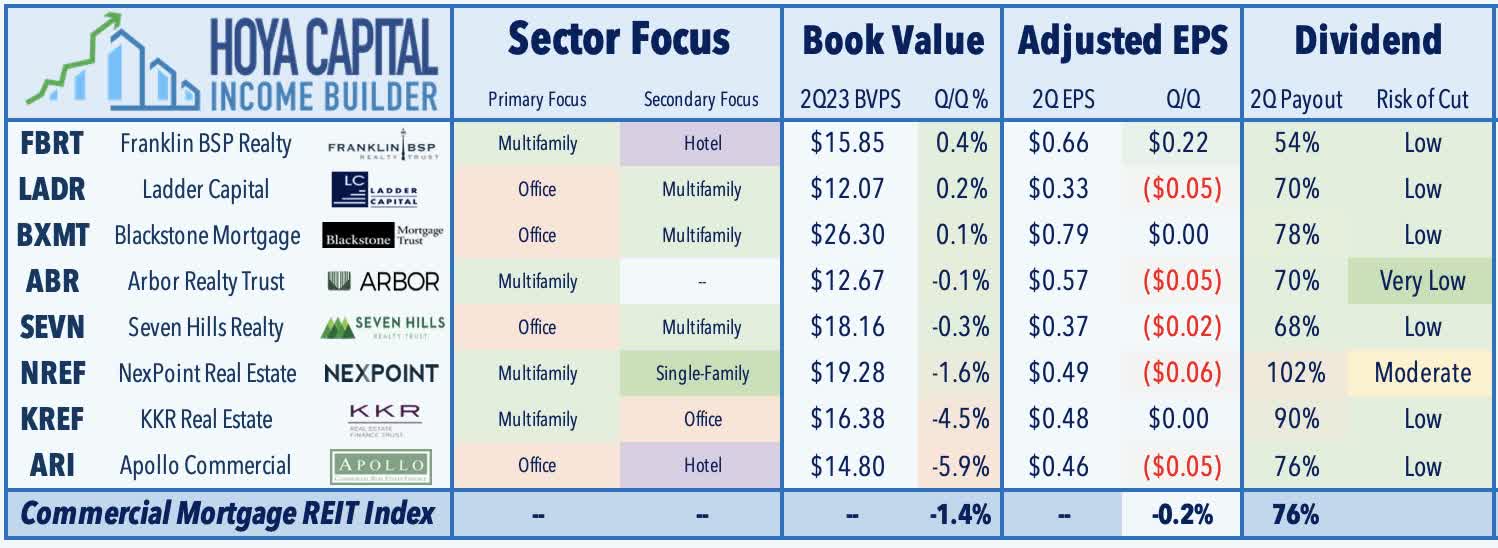

Commercial mREITs : (Halftime Grade: B+) On the commercial mREIT side, we've seen results from 8 of the 17 commercial mREITs, where the movement in BVPS remains far more muted on a quarter-to-quarter basis. On the upside, multifamily-focused lender Arbor Realty ( ABR ) - which had come into the cross-hairs of short-sellers earlier this year - reported stronger-than-expected results and raised its dividend to $0.43. NexPoint Real Estate ( NREF ) also reported solid results and declared a special dividend of $0.185/share in addition to maintaining its regular quarterly dividend. Commercial lender Blackstone Mortgage ( BXMT ) reported EPS of $0.79/share, which covered its $0.62/share dividend, while its BVPS increased to $26.30 - up 0.1% from last quarter. BXMT - which has 35% of its collateral in office-backed loans - noted that 96% of its portfolio is currently performing - down from 97% last quarter and 99% from a year earlier. Other more office-focused lenders haven't fared as well, including Apollo Commercial ( ARI ), which dipped double-digits after reporting a nearly 6% decline in its BVPS and a dip in its EPS driven by a sizable $0.33/share increase in its loan loss reserve. KKR Real Estate ( KREF ), meanwhile, noted that its BVPS dipped 4.5% in Q2 driven by increased loan loss reserves allocated to its office loans. KREF's CECL allowance increased by $0.82/share, driven by a revision in its risk rating from 4 to 5 on its $250M loan backed by five California office properties.

{kind=link}

Specialty REIT Halftime Report

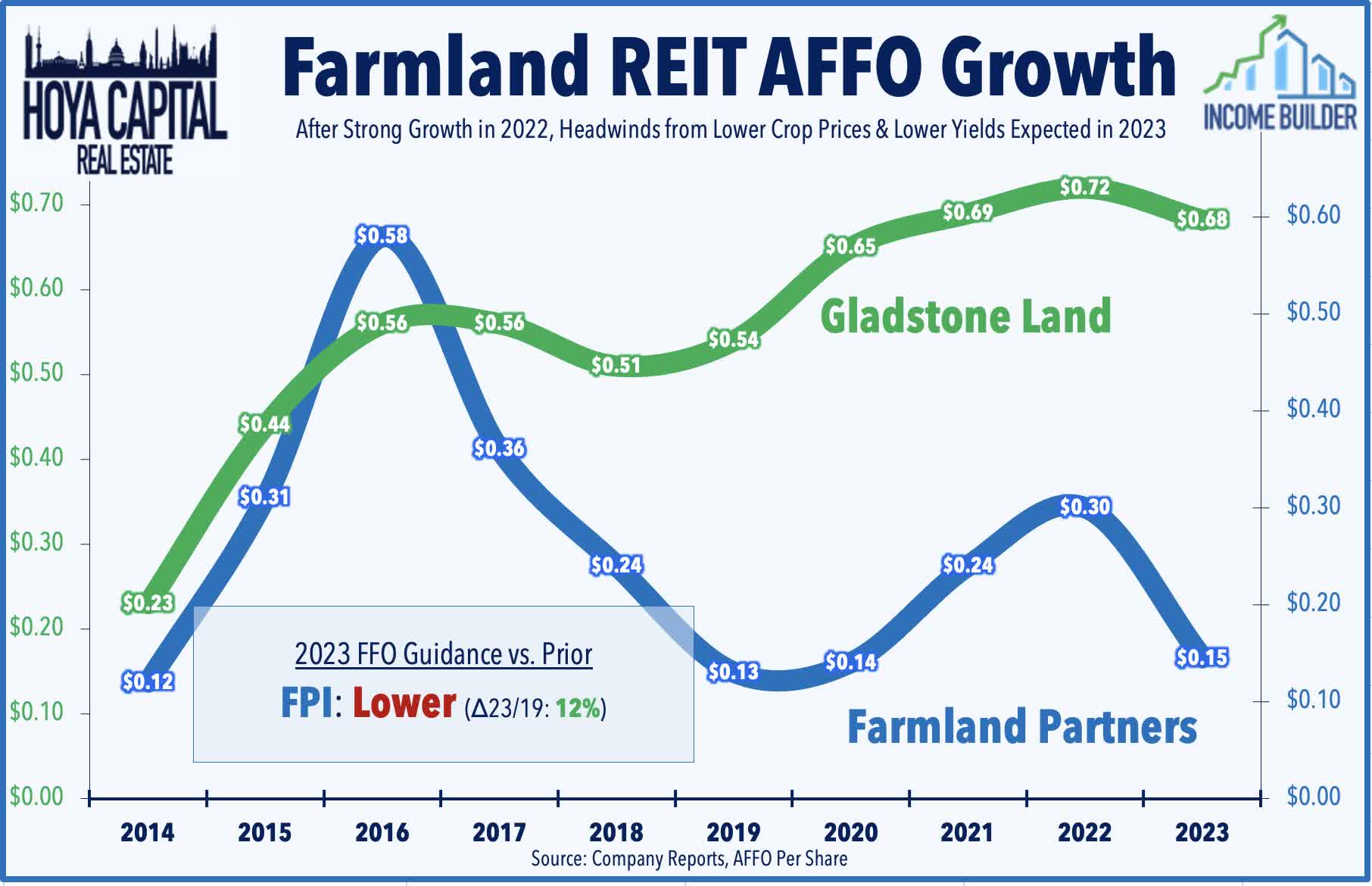

Farmland : Small-cap farmland REIT Farmland Partners ((FPI)) has been one of the most significant laggards this earnings season after it significantly lowered its full-year FFO outlook prompted by rising interest expense. FPI now expects its full-year FFO to dip over 50% this year compared to 2022, but to levels that are still about 12% above its full-year 2019 FFO before the pandemic. As discussed in our recent Land REIT report , farmland REITs have been pressured by a "triple whammy" of headwinds - lower crop yield due to extreme weather, lower crop prices, and significantly higher interest rate expense. One of the hottest "inflation hedges" during the pandemic, land REITs have fallen out of favor as rising rates and normalizing supply chains have created disinflationary - and even deflationary - headwinds for commodities. Grains prices have declined 25% from their 2022 peak despite the ongoing Russia/Ukraine War, but remain 50% above 2019-levels.

{kind=link}

Previewing The Second-Half of Earnings

At the halfway point of REIT earnings season, results have generally topped consensus estimates with nearly two-thirds of REITs raising their full-year outlook, a "raise rate" that exceeds that of the broader S&P 500. That said, the back half of earnings season tends to be more volatile with a composition of reports that skews towards smaller and more specialized REITs. As with the prior quarter, the handful of earnings "misses" and downward earnings revisions have been driven predominately by elevated debt servicing expenses, underscoring the continued challenges facing more-highly-levered real estate portfolios from the higher rate environment. International underperformance has also been a headwind for several normally steady-handed REITs, while disinflationary trends have become a headwind for a handful of REITs as well given their direct CPI linkage.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

REIT Earnings Halftime Report